- Advanced Materials

- Vacuum Insulation Panel Market

Vacuum Insulation Panel Market Size, Share, and Growth Forecast, 2026 - 2033

Vacuum Insulation Panel Market by Material Type (Silica Core, Fibreglass Core, Others), Panel Type (Flat Panels, Special Shape / Customised Panels), Panel Type (Flat Panels, Special Shape / Customized Panels), Industry (Building & Construction, Cold Chain & Logistics, Food & Beverage, Healthcare & Pharmaceuticals, Consumer Appliances, Misc.), and Regional Analysis from 2026 to 2033

Vacuum Insulation Panel Market Size and Trends Analysis

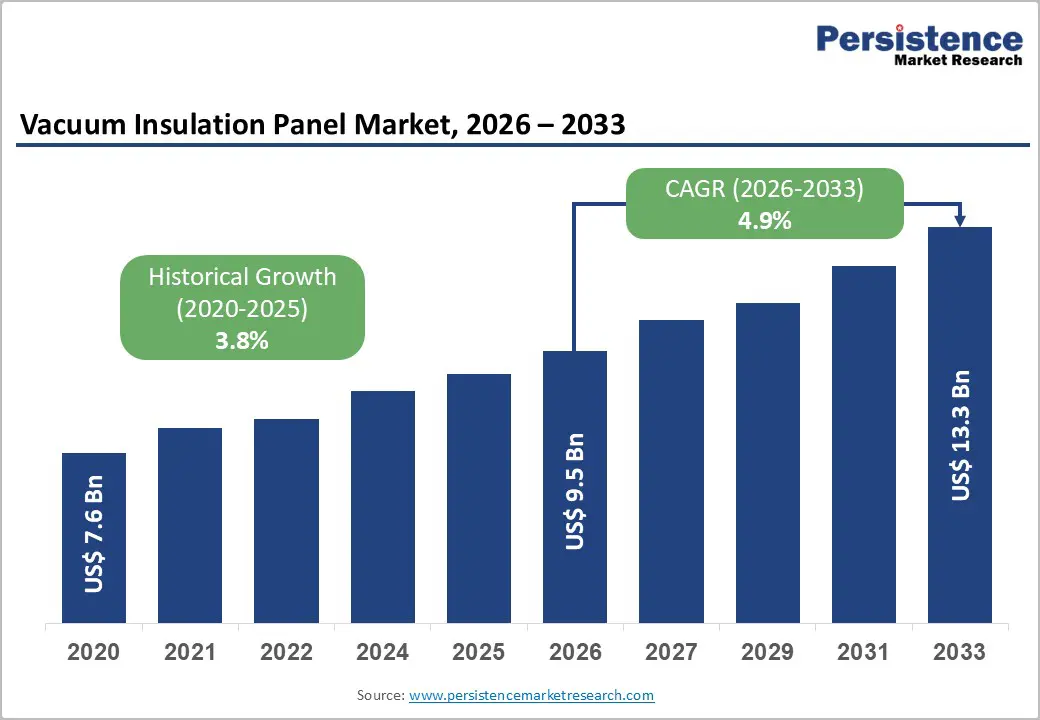

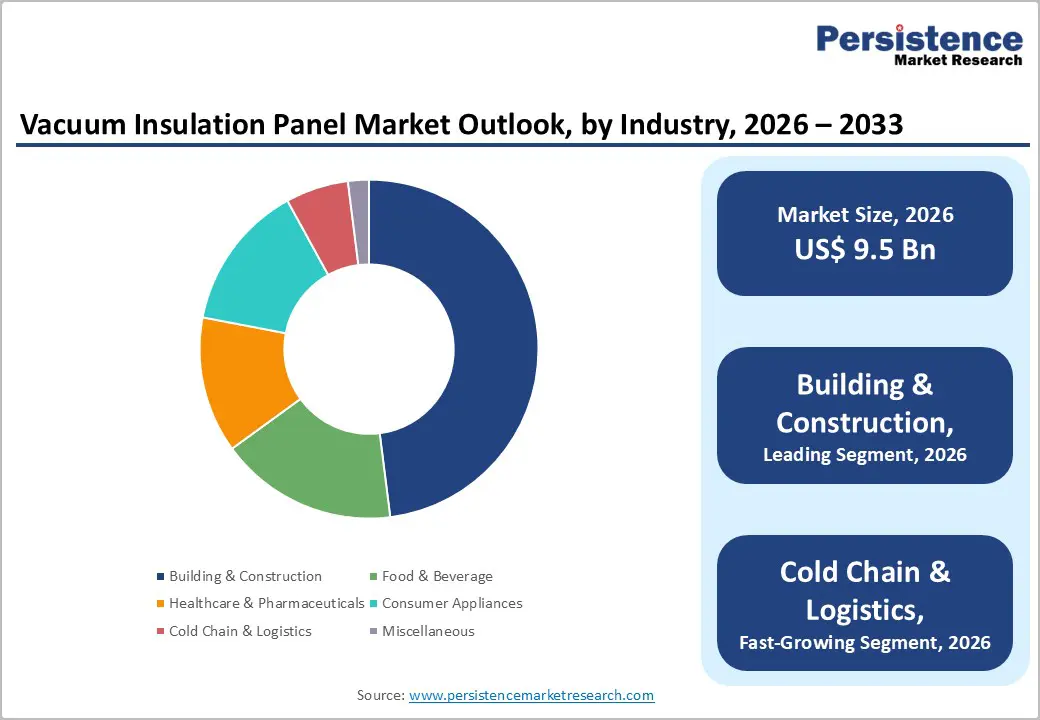

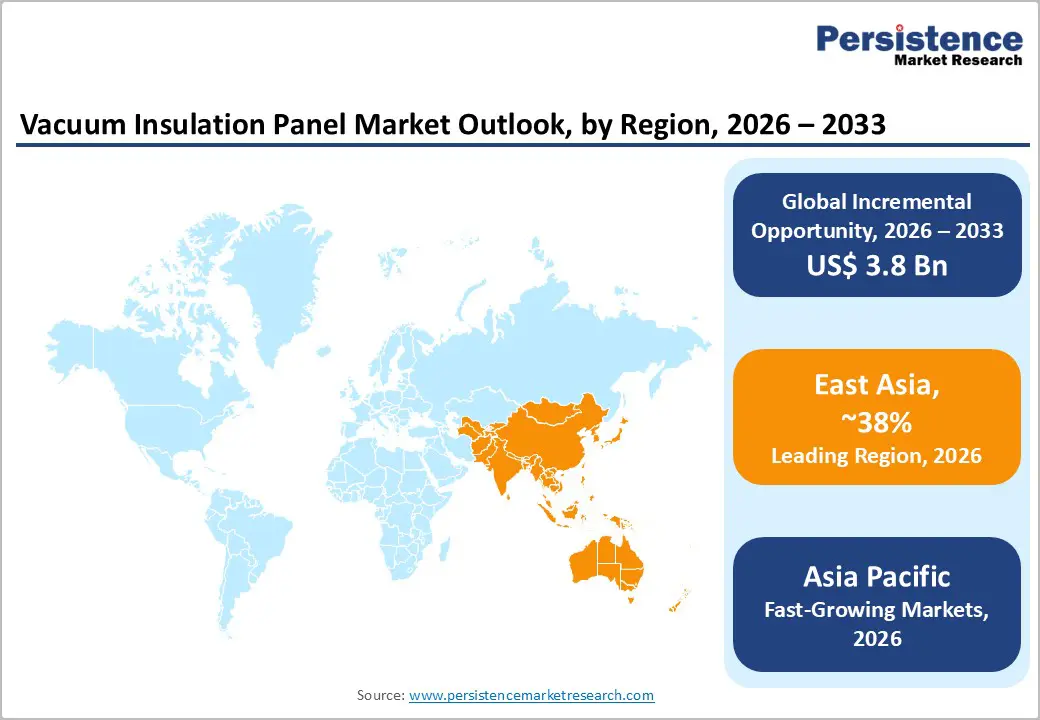

The global vacuum insulation panel market size is likely to be valued at US$ 9.5 billion in 2026 and is projected to reach US$ 13.3 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

This trajectory reflects the market's transition from early-stage technology adoption to mainstream industrial deployment across built environments and temperature-sensitive supply chains. The market expanded from US$ 7.4 billion in 2020 to its 2026 valuation, demonstrating a historical CAGR of 4.2%, indicating steady acceleration in adoption cycles, signals intensifying market momentum driven by regulatory tightening, capital infrastructure spending, and rising energy costs.

Key Industry Highlights:

- East Asia Market Scenario: East Asia dominates with ~38% share, driven by rapid urbanization, government infrastructure investment, and stringent energy-performance regulations in China, Japan, and South Korea.

- Europe’s Regulatory Push: Europe commands ~20% share, with strict energy-efficiency directives and green financing programs driving demand for VIPs in building retrofits and data centre insulation.

- Building & Construction Dominance: The sector accounts for ~48% of market demand, driven by regulatory mandates for thermal performance and interior-space preservation in new and existing structures.

- Cold-Chain Logistics Growth: The fastest-growing segment, fueled by pharmaceutical and biotech supply chain expansion, vaccine distribution, and high-value temperature-controlled transport needs.

| Key Insights | Details |

|---|---|

| Vacuum Insulation Panel Market Size (2026E) | US$ 9.5 Bn |

| Market Value Forecast (2033F) | US$ 13.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Dynamics

Drivers - Regulatory Energy Efficiency Mandates and Building Code Evolution

Governments globally are implementing stricter thermal performance standards that fundamentally reshape insulation material specifications. The regulatory environment has emerged as the primary structural driver of the Vacuum Insulation Panel Market, with standards increasingly mandating superior thermal performance in constrained building envelopes. The United Kingdom's Future Homes Standard 2025 requires wall U-values of 0.18 W/m²K and roof U-values of 0.13 W/m²K, performance levels achievable only through advanced insulation technologies.

The updated U.S. appliance standards are projected to deliver US$ 36.4 billion in cumulative consumer savings over 30 years, compelling manufacturers to adopt superior insulation solutions to achieve compliance. These regulatory frameworks translate directly into market demand: VIPs deliver R-values of 25 to 50 per inch, enabling effective insulation at thicknesses of 4-50mm, compared to conventional foam requiring significantly greater depth. The Vacuum Insulation Panel Market benefits from this performance delta as architects and building engineers specify VIPs to simultaneously meet energy codes and preserve valuable interior space.

Regional variations in building codes from EU renovation directives to China's net-zero building mandates create differentiated but universally positive demand drivers.

Infrastructure of Capital Expenditure Cycles and Urbanisation in Emerging Markets

Massive capital allocation by governments toward infrastructure modernisation directly feeds the Vacuum Insulation Panel Market growth, particularly in the Asia-Pacific regions undergoing rapid urbanisation. India's government increased capital expenditure by 11.1% to US$ 133 billion in FY 2024-25, equivalent to 3.4% of GDP, with significant allocation to build environment modernisation. The nation's real estate market is projected to reach US$ 5.8 trillion by 2047, contributing 15.5% to total GDP, while government-backed housing programs (PMAY-U) have sanctioned 1.18 crore houses with 86.6 lakh completed structures.

Warehousing infrastructure development, driven by e-commerce and manufacturing growth, represents particularly acute demand for VIP insulation: India's logistics sector projects demand for 159 million square feet of warehousing by 2047 at a 4% CAGR. Similarly, government industrial cluster investments of US$ 120.5 billion spanning 27 industrial complexes create demand for temperature-controlled manufacturing and storage facilities, where Vacuum Insulation Panel Market products provide essential thermal separation with minimal footprint impact. These capital cycles translate to multi-year procurement pipelines that stabilize and amplify annual demand growth, particularly in building and cold-chain segments.

Restraint - Manufacturing Complexity and Capital Intensity of Production Infrastructure

Vacuum insulation panel production presents significant technical and capital barriers that constrain supply-side capacity expansion and market penetration rates. VIP manufacturing demands proprietary vacuum-sealing technology, precision core-material processing, and high-barrier film integration processes requiring specialised equipment and quality-control validation that limit production scalability.

The vacuum integrity requirement, maintaining pressures below 10 Pa over product lifetime, necessitates sophisticated gas-permeability testing and barrier-film specifications that only established manufacturers reliably achieve. Capital costs for greenfield VIP production facilities exceed typical insulation manufacturing by 200-300%, creating substantial barriers to market entry and constraining supply-side competitive intensity. This manufacturing complexity translates directly into product pricing: VIPs command 3-5x premium pricing relative to conventional foam insulation, limiting adoption in price-sensitive segments and slowing penetration in emerging markets where cost sensitivity remains acute.

While architectural demand for superior thermal performance is structurally positive, supply-side constraints dampen the Vacuum Insulation Panel Market's near-term growth trajectory, with established players (Panasonic, Evonik, va-Q-tec) maintaining protective competitive moats through manufacturing expertise rather than commodity-scale competition.

Opportunity - Retrofitting Existing Building Stock for Energy Performance Compliance

The global building stock retrofit opportunity represents a multi-trillion-dollar demand pool for Vacuum Insulation Panel solutions, as existing structures face mandatory energy performance upgrades to achieve net-zero carbon targets. Approximately 80-90% of buildings that will exist in 2050 have already been constructed, with the vast majority failing to meet emerging energy-performance standards.

Panasonic's ADVANC-R® platform, showcased at AIA 2025, specifically targets the retrofit and re-roofing market, delivering R-66 thermal performance at 0.94-inch thickness enabling building height constraint solutions and interior-volume maximization critical for existing structure modernisation. This application segment addresses a structural market opportunity: building owners and facility managers seek thermal upgrades that minimise disruption, preserve interior volume, and demonstrate regulatory compliance without facility redesign. The retrofit opportunity extends beyond commercial roofing to residential envelope upgrades, mechanical space insulation, and district heating network retrofits. European governments' renovation stimulus programs supported by EU green financing mechanisms create concentrated procurement windows for retrofit insulation materials, positioning the Vacuum Insulation Panel Market as a primary beneficiary of decarbonization capital allocation.

Pharmaceutical Cold-Chain Infrastructure Expansion and Biotech Logistics Standardisation

Pharmaceutical and biotech supply chains represent an emerging, high-value application segment where Vacuum Insulation Panel technology delivers critical performance advantages unachievable with conventional insulation. The pharmaceutical cold-chain sector's rapid expansion, driven by proliferating Speciality medicines, gene therapies, and biologics requiring ultra-precise temperature control (frequently -20°C to -80°C), creates demand for insulation solutions that maintain temperature stability with minimal active cooling. Regulatory requirements for validated thermal packaging and real-time temperature monitoring drive adoption of advanced materials, where VIPs' superior performance-to-weight ratios enable portable, compliant transport containers.

Celcius Logistics' 2025 launch of Celcius+, a specialised pharmaceutical logistics unit, exemplifies structural demand growth within this application vertical. Vaccine supply chains, now established as critical global infrastructure evidenced by post-pandemic distribution requirements and ongoing pandemic preparedness mandates, represent sustained, high-volume demand for temperature-controlled packaging where VIPs demonstrate clear technical superiority. The Vaccine Insulation Panel Market particularly benefits from this opportunity: pharmaceutical VIPs must maintain temperature stability across extreme geographic conditions (from equatorial distribution hubs to Arctic-exposure logistics nodes) while minimising weight and volume performance envelope that positions VIPs as preferred solution relative to polyurethane foam alternatives.

Beyond regulatory compliance, pharmaceutical manufacturers increasingly recognise cold-chain performance as a competitive differentiator and brand-risk mitigation factor. Investment in superior insulation technology reduces in-transit product loss, mitigates regulatory non-compliance risk, and demonstrates to customers and regulators a commitment to product integrity. This value perception drives pharmaceutical procurement decisions toward premium insulation solutions despite cost premiums, creating pricing power and margin potential for VIP manufacturers that establish dedicated pharmaceutical product lines and certifications.

India's healthcare sector expansion is projected as one of the nation's largest employment and revenue drivers, with rising government spending through initiatives like Ayushman Bharat creates subsidiary demand for pharmaceutical logistics infrastructure supporting domestic distribution of advanced therapeutics.

Category-wise Analysis

Material Type Insights

Silica-core vacuum insulation panels dominate the material segment, commanding 50% market share in 2026, driven by superior thermal insulation performance and manufacturing maturity. Fumed silica's microporous structure, featuring pore sizes near 100 nanometers and porosity exceeding 90%, enables thermal conductivity as low as 0.0018 W/mK, substantially outperforming alternative core materials. This superior performance translates into practical applications: silica VIPs achieve R-values of 25-50 per inch, enabling effective insulation in 4-50mm thickness ranges, flexibility critical for space-constrained applications from commercial roofing to portable refrigeration.

Silica's market leadership reflects its technical superiority and the established manufacturing ecosystem supporting its production at scale.

Major manufacturers, including Panasonic, va-Q-tec, and Evonik, have optimised silica-core production across multiple generations, creating manufacturing advantages that translate into reliability, cost efficiency, and supply-chain maturity. Panasonic's Vacua Series, unveiled at ACREX India 2025, exemplifies advanced silica-core technology: delivering thermal conductivity of 0.0013 W/mK with 5-8mm thickness, the fifth-generation product achieves approximately 20× better insulation performance than polyurethane foam, reinforcing silica's performance leadership.

Silica's dominance reflects both technical performance and the critical mass of installed base, creating path-dependent procurement preferences among specifiers and architects familiar with silica material properties and performance profiles.

Industry Insights

Building and construction commands 48% of the vacuum insulation panel market in 2026, reflecting the sector's scale and energy-performance regulatory environment. This dominance reflects the applied logic: buildings consume approximately 40% of global primary energy and contribute 30% of energy-related CO2 emissions, creating a policy priority for building envelope insulation performance. Regulatory standards progressively tightening thermal performance requirements create mandated demand for superior insulation materials in new construction and renovation projects.

Cold chain and logistics represent the fastest-growing end-use segment within the Vacuum Insulation Panel Market, driven by e-commerce expansion, pharmaceutical supply-chain transformation, and biotech logistics growth. This segment's growth trajectory exceeds building and construction, reflecting structural supply-chain transformation and the sector's relative nascency in VIP adoption. Tiger Corporation's 2025 deployment of stainless-steel vacuum insulation panels in Osaka-Kansai Expo refer containers and cold-chain transport boxes marks the segment's technological maturation and commercialisation.

Regional Insights and Trends

North America Market Trend

North America commands approximately 20% of the global vacuum insulation panel market, with the United States representing the dominant regional market driven by commercial construction activity and building retrofit demand. The U.S. construction sector, spending US$ 2.2 trillion annually, employs 8.2 million workers and encompasses 3.7 million construction businesses, providing a substantial commercial foundation for VIP adoption. Housing construction remains robust, with 1.6 million new homes built in 2024, indicating sustained residential demand for insulation materials.

Regulatory environment remains supportive: updated U.S. appliance standards deliver projected consumer savings of US$ 36.4 billion over 30 years, driving appliance manufacturers toward superior insulation solutions where VIPs provide a competitive advantage. The commercial retrofitting market, driven by corporate sustainability commitments and building improvement initiatives, represents significant demand concentration. Panasonic's ADVANC-R® platform specifically targets North American re-roofing applications, reflecting the region's retrofit demand priorities.

North American market growth remains modest relative to Asia-Pacific, reflecting market maturity and slower urban density increases compared to emerging-market dynamics. Building codes emphasizing thermal performance exist but lack the regulatory acceleration driving Asia-Pacific markets. Price sensitivity in residential construction constrains VIP penetration despite technical superiority.

East Asia Vacuum Insulation Panel Market Trends

East Asia dominates the global market with approximately 38% market share, driven by rapid urbanization, massive government infrastructure capital allocation, and building energy-performance regulatory acceleration across China, Japan, and South Korea. China's construction sector, as part of its economic stimulus and urban development priorities, represents the world's largest construction market by absolute value, with urbanisation continuing to expand projected urban population reaching 65-70% of the total by 2030.

Government industrial cluster investments of US$ 120.5 billion spanning 27 complexes create concentrated demand for infrastructure insulation and temperature-controlled logistics facilities.

Manufacturing intensity in East Asia, particularly in electronics, automotive, and precision industries, creates demand for climate-controlled production facilities where VIPs minimise operational energy costs while maintaining equipment-critical temperature stability. Japan's ageing demographic profile and real estate saturation create retrofit and renovation market dynamics analogous to Europe, supporting sustained VIP demand in residential and commercial renovation sectors. South Korea's technology-intensive manufacturing and premium residential market position favor VIP adoption driven by specification preference for superior performance materials.

Europe Vacuum Insulation Panel Market Trends

Europe commands approximately 25% of the global vacuum insulation panel market, characterised by highly developed digital infrastructure, stringent energy efficiency regulations, and strong emphasis on sustainability. The European Union's information and communication services sector comprises 1.4 million enterprises generating US$ 667 billion in value added, with Internet penetration reaching 94% as of 2025. Germany is the largest single contributor to EU sectoral value added at 22.8%, followed by France, with the five largest EU economies collectively generating nearly two-thirds of total EU value added in information and communication services.

The regulatory environment in Europe is the most stringent, with the revised Energy Efficiency Directive mandating comprehensive reporting of data centre energy performance metrics and requiring implementation of waste heat utilisation systems in facilities exceeding 1 megawatt of power consumption. These regulatory requirements are driving substantial investment in advanced critical cooling technologies, particularly liquid cooling solutions that reduce energy consumption and support waste heat recovery requirements.

Germany's accelerated implementation of the EED, with 100% renewable energy requirements by 2027, is creating particularly strong incentives for efficient critical infrastructure solutions.

Competitive Landscape

The global vacuum insulation panel market is consolidated, dominated by a few technologically advanced companies that hold significant market share. Key players such as Panasonic Corporation, Tiger Corporation, va-Q-tec, AGC Inc., Dow, and Sekisui Chemical Co., Ltd. lead through innovation in ultra-thin, high-R-value, and low thermal conductivity panels. The market is driven by growing demand across construction, HVAC, refrigeration, and cold-chain logistics, with a strong emphasis on energy efficiency and sustainability. High entry barriers due to complex manufacturing processes, proprietary technologies, and patent protections limit new entrants.

Companies focus on R&D, product differentiation, and expansion into emerging markets to strengthen their positions. Strategic partnerships, joint ventures, and the adoption of VIPs in green buildings and energy-efficient appliances further reinforce the dominance of leading players. Overall, the market remains competitive but is controlled by a few major players with advanced technological capabilities.

Key Industry Developments

- In May 2025 - Panasonic Corporation: Panasonic announced the showcase of its ADVANC-R® Vacuum Insulation Panel at AIA 2025, introducing an ultra-thin VIP delivering an industry-leading R-Value of 66 at 0.94 inches thickness. The development targets low-slope roofing, retrofit, and re-roofing applications, addressing space constraints and tightening energy-efficiency codes while reinforcing VIP adoption in high-performance building envelopes.

- In February 2025 - Panasonic Industry (Panasonic Life Solutions India): Panasonic unveiled its fifth generation “Vacua Series” Vacuum Insulation Panels (VIP) at ACREX India 2025, targeting HVAC, appliances, transportation, and building applications. The panels feature an ultra-low thermal conductivity of 0.0013 W/mK, a slim 5–8 mm thickness, and an advanced glass-fibre core with an aluminium envelope, delivering insulation performance ~20 times better than polyurethane foam. This development strengthens VIP adoption in energy-efficient appliances, green buildings, and cold-chain infrastructure across India.

Companies Covered in Vacuum Insulation Panel Market

- Evonik Industries AG

- LG Hausys Ltd

- Panasonic Corporation

- DOW

- OCI Ltd

- Kevothermal, LLC

- Porextherm Dämmstoffe GmbH

- Thermocor

- Va-Q-Tec AG

Frequently Asked Questions

The global vacuum insulation panel market is projected to be valued at US$ 9.5 Bn in 2026.

The Flat Panels are expected to account for approximately 70% of the global Vacuum Insulation Panel Market by Panel Type in 2026.

The market is expected to witness a CAGR of 4.9% from 2026 to 2033.

Regulatory Energy Efficiency Mandates and Urban Infrastructure Expansion drive the Vacuum Insulation Panel Market by enforcing superior thermal performance standards and stimulating demand in building, cold-chain, and industrial applications.

Retrofitting Existing Building Stock and Expanding Pharmaceutical Cold-Chain Infrastructure drive the Vacuum Insulation Panel Market by enabling superior thermal performance in constrained spaces and ensuring precise temperature control in high-value logistics applications.

The key players in the Vacuum Insulation Panel Market include Evonik Industries AG, LG Hausys Ltd, Panasonic Corporation, DOW, OCI Ltd, Va-Q-Tec AG.