- HVAC

- Large Bore Vacuum Insulated Pipe Market

Large Bore Vacuum Insulated Pipe Market Size, Share, Trends, Growth, Regional Forecasts from 2026 - 2033

Large Bore Vacuum Insulated Pipe Market by Installation Type (Above Ground, Underground, Under Sea), Application (Cryogenic, Chemical, Aerospace, Others), and Regional Analysis 2026 - 2033

Large Bore Vacuum Insulated Pipe Market Share and Trends Analysis

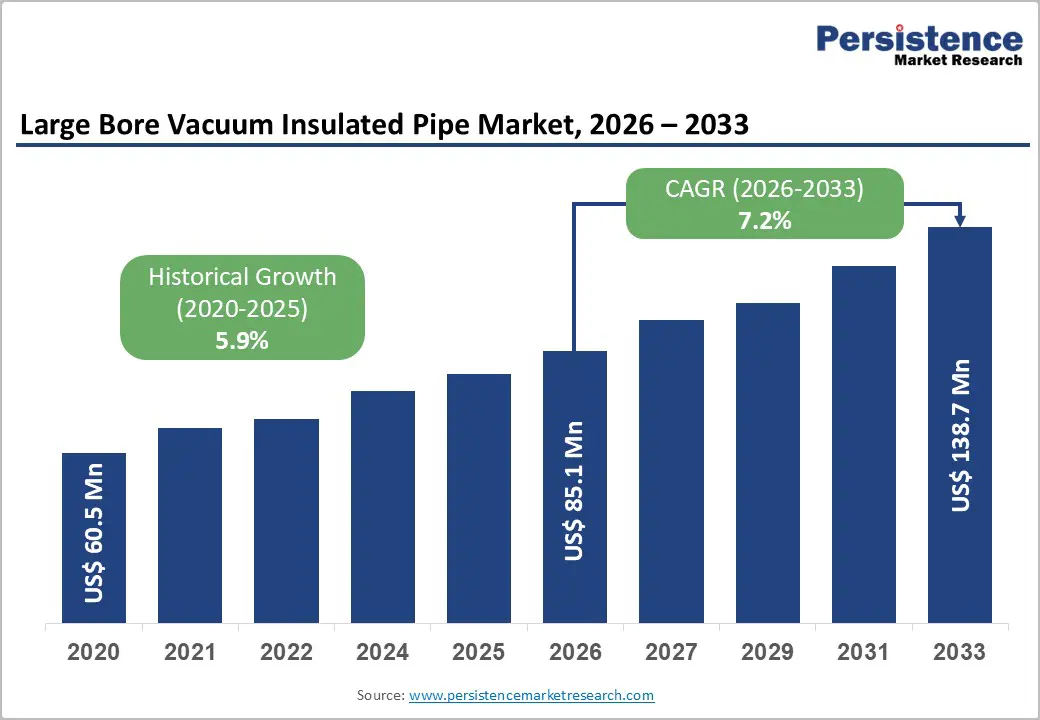

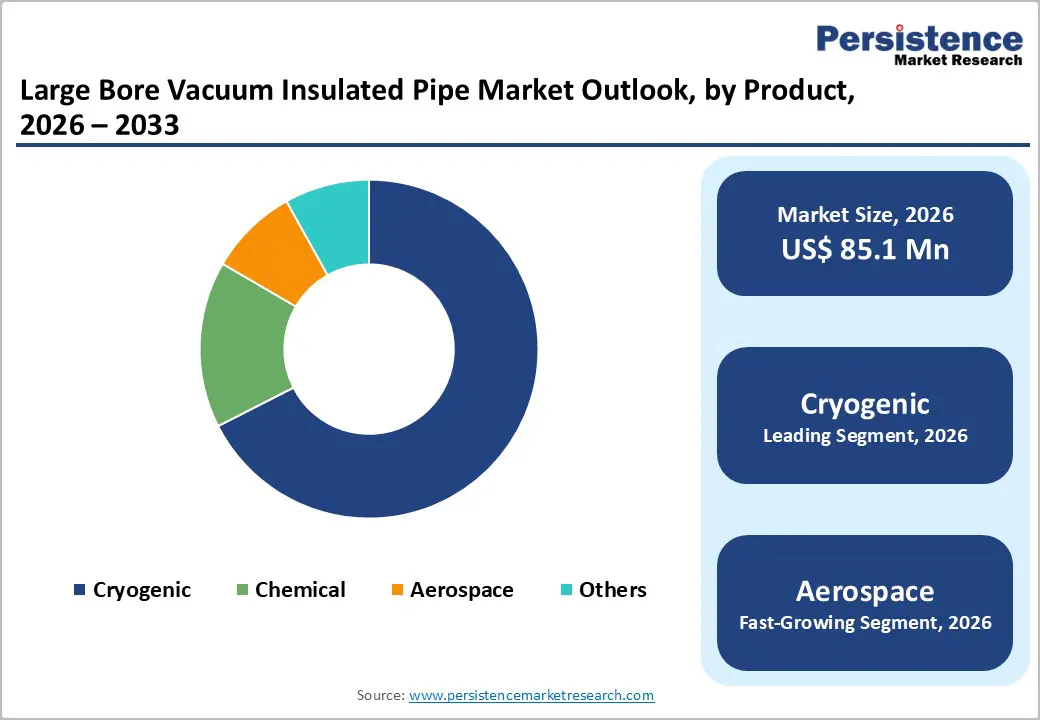

The global large bore vacuum insulated pipe market size is likely to be valued at US$ 85.1 million in 2026 and is projected to reach US$ 138.7 million by 2033, growing at a CAGR of 7.2% between 2026 and 2033. Market expansion is driven by accelerating demand for efficient cryogenic liquid transportation across energy infrastructure, particularly in liquefied natural gas (LNG) distribution systems, aerospace applications requiring liquid hydrogen fuel transfer, and industrial chemical processing.

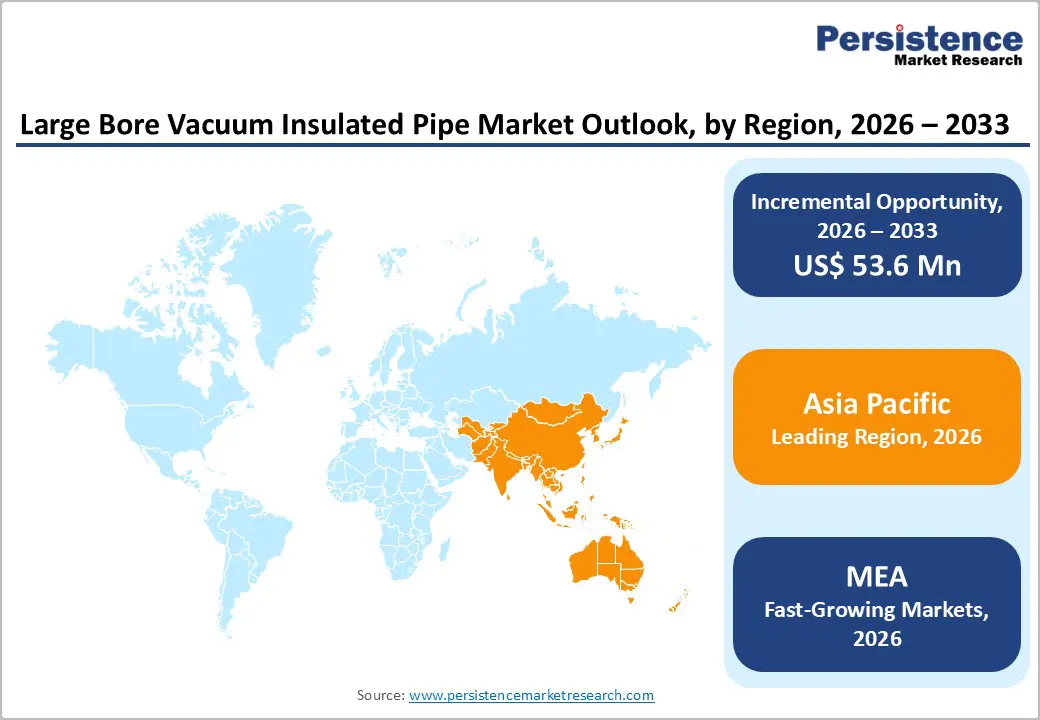

Asia Pacific has emerged as the dominant growth region, commanding 36% of the global market share, while North America and Europe maintain strong established positions supported by significant investments in hydrogen economy development and regulatory frameworks mandating energy-efficient infrastructure solutions.

Key Highlights Summary

- Above-ground installations dominate the market with a 62% share, while subsea applications are the fastest-growing segment at an 8.3% CAGR, driven by the offshore energy transition and marine bunkering infrastructure modernization supporting decarbonization-focused shipping operations.

- Cryogenic applications command 68% market share as the leading application segment, while aerospace is the fastest-growing category at an 8.7% CAGR, supported by the expansion of commercial space exploration and hydrogen-powered aircraft development research initiatives.

- Asia Pacific leads regional markets with 36% market share and 7.8% CAGR growth, followed by North America at 26% share and Europe at 24% share, growing at 6.1% CAGR, with sustained infrastructure investment momentum across LNG, hydrogen, and industrial gas sectors.

- Major market consolidation activity, including the June 2025 Chart Industries-Flowserve merger, which creates a USD 19 billion value entity, and Linde's USD 2 billion hydrogen facility investment in Canada, demonstrates leading players' strategic commitment to integrated solutions and to hydrogen economy infrastructure development.

- Chart Industries, Air Products, Linde, Parker-Hannifin, and Flowserve represent market-leading positions supported by comprehensive cryogenic equipment portfolios, global operational footprints, and integrated service capabilities enabling system-level optimization and customer value delivery across distributed industrial operations.

| Key Insights | Details |

|---|---|

|

Large Bore Vacuum Insulated Pipe Market Size (2026E) |

US$ 85.1 million |

|

Market Value Forecast (2033F) |

US$ 138.7 million |

|

Projected Growth CAGR (2026-2033) |

7.2% |

|

Historical Market Growth (2020-2025) |

5.9% |

Market Dynamics Analysis

Drivers - Infrastructure Expansion in the Liquefied Natural Gas (LNG) Sector

The global demand for LNG is growing substantially, with projections indicating an annual increase of 3.4% through 2035, requiring 100 million metric tons of additional capacity to meet demand growth and replace declining existing projects. This expansion directly translates into heightened demand for specialized vacuum-insulated piping systems capable of efficiently transporting massive volumes of cryogenic liquids over extended distances with minimal thermal losses. The strategic development of liquefaction plants, storage facilities, and regasification terminals across key markets, particularly in Asia Pacific where China, India, and Southeast Asian nations are constructing new LNG receiving terminals and satellite stations, necessitates sophisticated cryogenic transfer infrastructure. The market intensity in the Asia Pacific is particularly pronounced, with China consuming ~45% of incremental global LNG demand in 2024, while India targets ~15% gas share in its energy mix by 2030, creating sustained infrastructure investment cycles.

Hydrogen Economy Acceleration and Clean Energy Transition

Hydrogen adoption is accelerating globally as governments and industries pivot toward decarbonization, with hydrogen identified as the fastest-growing cryogen type by application demand. The European Union's Hydrogen Strategy, the United States Department of Energy Hydrogen Shot Initiative (2021), and substantial public funding mechanisms are driving the commercialization of hydrogen liquefaction and transportation infrastructure. Linde's US$2 billion investment in Alberta, Canada, to build a world-scale clean hydrogen facility scheduled for 2028 completion exemplifies the capital intensity and scale of infrastructure development. Similarly, Air Liquide has committed US$50 million for hydrogen infrastructure upgrades in Texas, expanding pipeline capacity and distribution systems to meet long-term supply contracts with industrial refiners. The TACOMA project, a collaborative aviation research initiative running from 2023 to 2026, focuses specifically on developing cryogenic hydrogen tanks in composite design for passenger aircraft, demonstrating the aerospace sector's commitment to hydrogen-powered flight systems.

Restraints - High Capital Investment Requirements and Cost Barriers

Large-bore vacuum-insulated pipe systems represent significant capital commitments for end-users, with installation, engineering, and specialized manufacturing incurring substantial upfront costs that can delay project timelines or discourage adoption among price-sensitive industrial segments. The double-wall construction, vacuum maintenance systems, and precision manufacturing standards required for large bore applications (6 to 24 inches inner diameter) involve specialized equipment and skilled labor, constraining supply flexibility during demand surges. Stringent regulatory compliance requirements, including ASME B31.3 standards for chemical plant and petroleum refining piping systems operating at elevated pressures, mandate rigorous testing protocols and quality certifications that extend manufacturing lead times and increase operational expenses for suppliers, ultimately shifting cost burdens to customers in competitive-bidding environments.

Supply Chain Complexity and Manufacturing Capacity Constraints

Manufacturing large bore VIP systems requires highly specialized fabrication capabilities and aerospace-grade quality standards, with only a limited number of global suppliers possessing the technological expertise, manufacturing infrastructure, and certification credentials to meet end-user specifications. Geopolitical tensions, raw material supply volatility, and trade policy uncertainties create disruption risks that manufacturers must manage through inventory buffering strategies that increase operating costs. Extended manufacturing lead times, often exceeding 6-12 months for customized large-bore systems, limit market responsiveness, while capacity constraints in key manufacturing regions (North America, Western Europe, Japan) create bottlenecks that restrict market growth regardless of demand intensity, particularly during infrastructure investment acceleration phases requiring simultaneous project executions across multiple geographic markets.

Opportunity - Renewable Energy Infrastructure and Hydrogen Storage Markets

The global transition toward renewable energy systems is creating significant opportunities for the deployment of vacuum-insulated piping in hydrogen storage, distribution, and utilization applications. South Korea's USD 38 billion investment in hydrogen technologies has driven momentum for the development of hydrogen refueling infrastructure, with CIMC Enric's modular VIP systems already installed at over 100 hydrogen refueling stations across the country, establishing proof-of-concept frameworks for commercial scaling. Green hydrogen projects across Europe, North America, and the Asia Pacific are creating derived demand for specialized cryogenic equipment capable of maintaining extremely low temperatures during hydrogen liquefaction, temporary storage, and transport phases. India's rapidly expanding industrial sector and the government's commitment to natural gas infrastructure development present substantial opportunities for large-bore VIP adoption in emerging markets where infrastructure is being built rather than retrofitted, enabling greenfield deployment with optimized system specifications.

Aerospace and Space Exploration Sector Expansion

Aerospace applications represent a high-value, growth-oriented market segment for large-bore vacuum-insulated piping, driven by advancing rocket propulsion systems, commercial space exploration programs, and potential hydrogen-powered aircraft development initiatives. Chart Industries' established position supplying vacuum-insulated pipe to aerospace launch facilities, delivering extremely high flow rates of liquid hydrogen and oxygen, demonstrates proven system performance under mission-critical conditions requiring precision engineering and rigorous quality standards. Emerging commercial space exploration ventures, including reusable rocket development programs and satellite constellation expansion, are increasing demand for reliable cryogenic transfer infrastructure capable of supporting rapid turnaround operations and launch-pad efficiency requirements, creating sustained revenue opportunities for equipment manufacturers throughout market cycles.

Category-wise Analysis

Installation Type Insights

Above-ground installation is the dominant segment, accounting for 62% of the global large-bore VIP market, driven by deployments in industrial facilities, LNG terminals, refining complexes, and aerospace launch centers, where accessibility, visibility, and monitoring are prioritized. These systems support distribution networks linking liquefaction plants, storage terminals, transfer stations, and end-use facilities within controlled environments. Above-ground VIPs enable regulatory inspections, preventive maintenance, and rapid access for repairs, reducing downtime and extending operational life. The segment benefits from mature engineering standards, proven methodologies, and lifecycle cost optimization. Growth remains strong across Asia Pacific LNG terminals and hydrogen distribution networks.

Subsea vacuum-insulated piping is the fastest-growing installation category, expanding at an 8.3% CAGR, driven by offshore oil and gas operations, subsea LNG systems, and marine bunkering for decarbonizing shipping fleets. High technical complexity, deepwater installation, corrosion resistance, and extreme pressure requirements elevate value. Offshore hydrogen, carbon capture, and IMO-driven adoption of zero-emission fuels further accelerate subsea VIP infrastructure investments globally.

Application Insights

Cryogenic applications dominate the market, representing 68% of total demand, covering LNG transport, liquid nitrogen, liquid oxygen, liquid helium, and industrial gas processing requiring extreme temperature control. This segment reflects the core value of vacuum-insulated piping, enabling efficient, low-loss transfer of high-value cryogenic fluids across complex networks. LNG forms the largest subsegment, supported by global infrastructure expansion and its role as a transitional fuel. Industrial gas use in the pharmaceutical, semiconductor, healthcare, and research sectors demands ultra-high-purity delivery. Mature supply chains, ASME standards, certifications, and decades of proven performance underpin predictable adoption and reliability across global industrial energy ecosystems.

Aerospace is the fastest-growing application segment, expanding at an 8.7% CAGR, driven by commercial space acceleration, reusable launch systems, and hydrogen-powered aircraft research, which require advanced cryogenic transfer solutions. Aerospace demands extreme precision, vibration tolerance, and mission-critical reliability. Growth is reinforced by reusable rockets, hypersonic platforms, space manufacturing concepts, and hydrogen aviation programs, thereby establishing new global liquid hydrogen distribution requirements.

Regional Market Insights

North America Large Bore Vacuum Insulated Pipe Market Trends

North America maintains a prominent market share of approximately 26% of the global large-bore VIP market, driven by mature industrial infrastructure, substantial investments in LNG export capacity, and an innovation-intensive aerospace sector that supports research and development activities. The United States dominates regional market dynamics, with established LNG export terminals along the Gulf Coast supporting global energy markets, while expanding hydrogen infrastructure initiatives leverage existing petrochemical industry expertise and government support through the Bipartisan Infrastructure Law and Inflation Reduction Act, which allocated over USD 97 billion for clean energy infrastructure deployment. The U.S. market benefits from strong purchasing power, sophisticated end-user technical capabilities, and mature supply chain relationships between equipment manufacturers and industrial operators, enabling premium product positioning for high-performance systems.

Regional growth is supported by advances in modular VIP design, manufacturing automation, and digital monitoring, enabling predictive maintenance. Aerospace activity, space companies in California and Texas, drives specialty large-bore VIP fueling systems. Collaborations among materials scientists, engineers, and technology firms accelerate the development of next-generation designs. Public–private partnerships for district heating, industrial cooling systems, and cryogenic infrastructure resilience sustain investment momentum through 2033.

Europe Large Bore Vacuum Insulated Pipe Market Trends

Europe commands a considerable market share of 24%, with strong growth dynamics at a 6.1% CAGR, supported by ambitious decarbonization objectives, hydrogen economy development, and stringent regulatory frameworks mandating energy-efficient industrial infrastructure. Western Europe, particularly Germany, France, and the United Kingdom, exhibits mature market characteristics, with sophisticated end users prioritizing sustainability performance alongside operational efficiency. Germany's industrial base, combined with the government's commitment to hydrogen technology commercialization and the renewable energy transition, is driving substantial demand for cryogenic equipment to support industrial gas production, chemical processing, and emerging hydrogen fuel-cell applications. The European Union's harmonized product standards and safety regulations create favorable conditions for equipment manufacturers meeting certification requirements, while a multi-country market structure necessitates localized distribution approaches and technical support capabilities.

Eastern European markets present emerging growth opportunities, with cost-competitive manufacturing platforms and increasing adoption of advanced insulation solutions that support industrial modernization initiatives. European manufacturers possess significant technological expertise in precision engineering and cryogenic systems, with established engineering firms and equipment suppliers maintaining global competitiveness through innovation-focused strategies. Regulatory frameworks emphasizing product traceability, environmental compliance, and worker safety create compliance costs that are offset by market premiums for certified, high-performance systems that command sustainable competitive advantages.

Asia Pacific Large Bore Vacuum Insulated Pipe Market Trends

Asia Pacific emerges as the leading regional market, with a market share of 36%, expanding at approximately 7.8% CAGR, driven by rapid industrialization, massive LNG infrastructure investment, emerging hydrogen economy initiatives, and manufacturing capacity growth that supports regional and global demand. China dominates regional market dynamics, representing ~45.6% of the Asia Pacific industrial gases market in 2024, supported by record refining throughput and strategic gas storage capacity expansion targeting 60 billion cubic meters by 2025. China's industrial base expansion, semiconductor manufacturing growth, and government support for hydrogen technology development are creating sustained demand for large-bore VIP across LNG import terminals, industrial gas processing facilities, and emerging hydrogen refueling infrastructure networks.

India is the fastest-growing market, driven by industrial policy, healthcare oxygen demand, and expanding steel production. Government support for gas infrastructure and renewables favors the adoption of VIP. Southeast Asia, led by Vietnam and the Philippines, adds LNG regas capacity. Japan and South Korea retain premium demand. Regional manufacturing advantages, cost efficiency, supply chains, and technical expertise strengthen global competitiveness.

Competitive Landscape

The global large bore vacuum insulated pipe market shows moderate consolidation, with rising M&A activity reshaping competition. Leaders, including Chart Industries, Air Products, Parker-Hannifin, Flowserve, and Linde, leverage broad cryogenic portfolios and global support. High entry barriers limit rivals. Specialists like Cryofab, Demaco, and Cryocomp compete via customization, niche focus, and integrated system solutions, providing customers with procurement and lifecycle accountability.

Strategic Developments

- In June 2025, Chart Industries and Flowserve announced a merger of equals valued at ~USD 19 billion, combining cryogenic systems and fluid motion technologies to create an integrated global solutions provider with expected USD 300 million annual synergies by year three.

- In August 2024, Linde signed a long-term hydrogen supply agreement with Dow Chemical, investing USD 2 billion in a clean hydrogen and atmospheric gases facility in Alberta, Canada, supporting large-scale hydrogen production, carbon capture, and future cryogenic infrastructure demand.

- In August 2024, Linde Engineering partnered with Shell on the REFHYNE II project in Germany, developing a 100 MW renewable hydrogen plant producing 44,000 kg/day, reinforcing commercial-scale green hydrogen deployment and demand for advanced cryogenic transfer systems.

Companies Covered in Large Bore Vacuum Insulated Pipe Market

- Chart Industries

- Air Products and Chemicals

- Parker-Hannifin

- Flowserve

- Linde

- Air Liquide

- Nikkiso

- Demaco

- Cryofab

- Inox Group

- Emerson Electric

- HEROSE GmbH

- Fives Group

- Wessington Cryogenics

- Sulzer

Frequently Asked Questions

The global large bore vacuum insulated pipe market was valued at US$ 85.1 million in 2026 and is projected to reach US$ 138.7 million by 2033.

Market growth is driven by LNG capacity expansion, accelerating hydrogen economy investments, and rapid Asia Pacific industrialization, collectively increasing demand for efficient cryogenic transport infrastructure.

The market is expected to grow at a 7.2% CAGR from 2026 to 2033, supported by faster growth in subsea installations, aerospace applications, and Asia Pacific infrastructure investments.

Key opportunities arise from renewable hydrogen infrastructure expansion, commercial aerospace and hydrogen aviation development, and greenfield LNG and industrial gas projects in emerging Asia Pacific markets.

Key players include Chart Industries, Air Products, Parker-Hannifin, Flowserve, Linde, Air Liquide, and Nikkiso, alongside specialists such as Demaco, Cryofab, Inox Group, Emerson Electric, HEROSE, and Wessington Cryogenics.