- Power Generation, Transmission, & Distribution

- Vacuum Contactor Market

Vacuum Contactor Market Size, Share, and Growth Forecast 2026 - 2033

Vacuum Contactor Market by Contact Rating (Low Voltage Less than 1 kV, Medium Voltage 1-36 kV, High Voltage Greater than 36 kV), by Product Type (Spring Type Vacuum Contactors, Bellows Type Vacuum Contactors, Magnetic Latching Vacuum Contactors, Non-Latching Vacuum Contactors), by Application (Motors, Transformers, Capacitors, Reactors), by End Use (Utilities, Industrial, Oil & Gas, Mining, Others), by Regional Analysis, 2026 - 2033

Vacuum Contactor Market Size and Trend Analysis

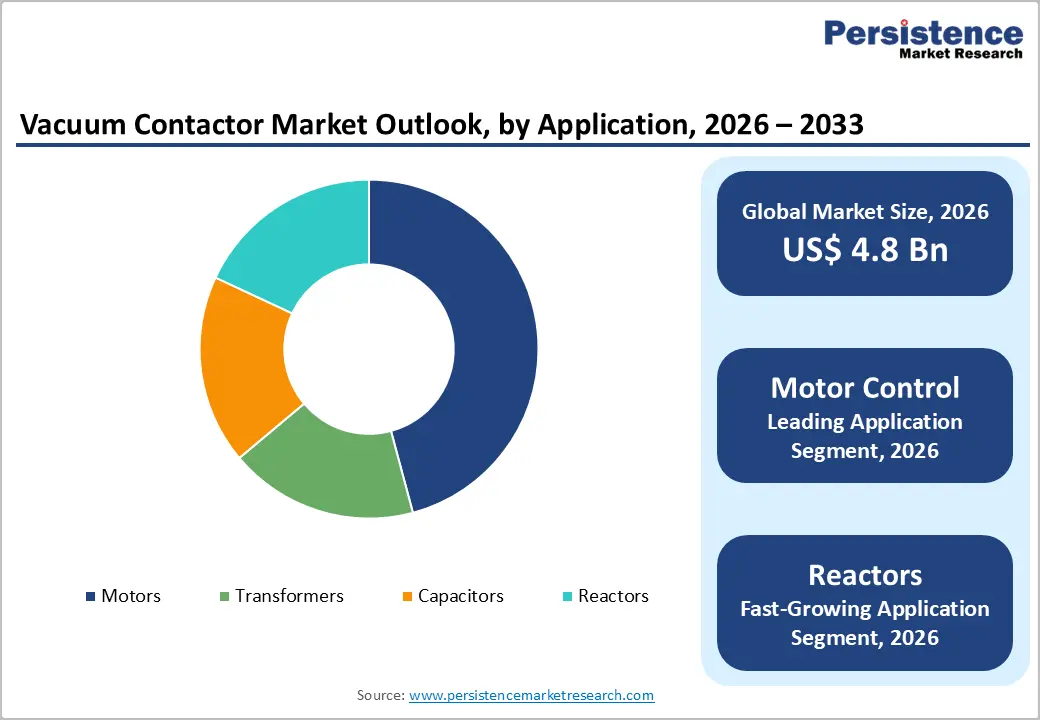

The global vacuum contactor market size is expected to be valued at US$ 4.8 billion in 2026 and projected to reach US$ 7.0 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The vacuum contactor market is experiencing steady growth driven by escalating demand for reliable electrical switching solutions across power distribution, industrial manufacturing, and renewable energy applications. Transformer switching losses are reduced by 20% or more utilizing vacuum contactors, establishing compelling value propositions supporting widespread adoption across utilities and industrial power management systems. Smart grid technologies and renewable energy integration initiatives drive sophisticated vacuum contactor deployment enabling automated load shedding, peak demand control, and enhanced grid stability with AI-enabled voltage analysis capabilities supporting real-time load balancing and fault prediction algorithms.

Key Market Highlights

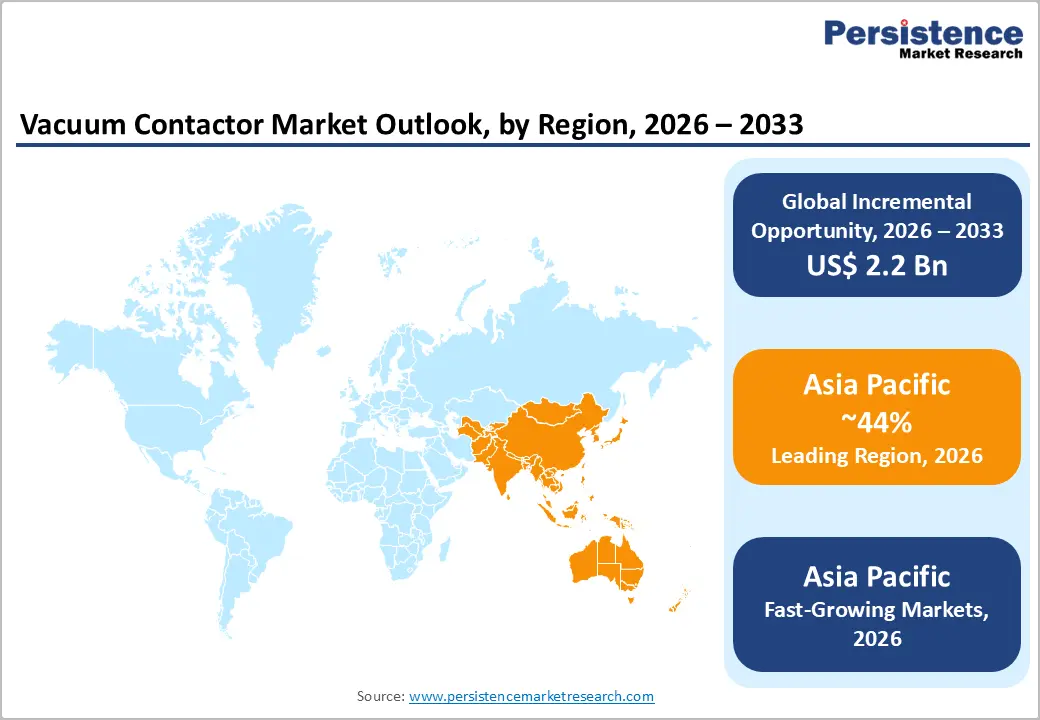

- Leading Region: Asia Pacific holds around 44% market share, supported by strong investments in grid modernization, automation, energy efficiency regulations, and renewable energy integration.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a CAGR of 9.2% during 2026 - 2033 due to rapid industrialization, smart city development, and renewable expansion.

- Dominant Segment: Spring type vacuum contactors dominate the market with approximately 62% share, driven by their simple design, proven reliability, and cost-effective deployment across applications.

- Fastest Growing Segment: Medium voltage vacuum contactors (1-36 kV) are the fastest-growing segment, expanding at a CAGR of 7.1% due to increasing use in utilities, industry, renewables, and smart grids.

- Key Market Opportunity: Self-healing vacuum interrupters combined with AI-based monitoring present the strongest opportunity by enabling predictive maintenance, extended equipment life, and reduced operational downtime.

| Global Market Attributes | Key Insights |

|---|---|

| Market Size (2026E) | US$ 4.8 Billion |

| Market Value Forecast (2033F) | US$ 7.0 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 6.5% |

Market Dynamics

Market Growth Drivers

Escalating Adoption of Smart Grids and Renewable Energy Integration

Global transition toward smart grid infrastructure and renewable energy projects including wind and solar power installations is driving unprecedented demand for advanced vacuum contactor solutions enabling sophisticated power distribution management. Smart grid adoption reduces grid failure probability by approximately 30%, delivering compelling reliability improvements justifying capital investments in advanced switching infrastructure. Utilities sector accounts for 39.9% of global vacuum contactor market share, leveraging vacuum switching technology for load balancing, short-circuit protection, and arc-free switching eliminating mechanical wear associated with traditional electromechanical alternatives.

Data centers increasingly deploy vacuum contactors supporting real-time power management and load balancing capabilities enabling seamless transition between renewable and traditional energy sources. Government initiatives promoting carbon neutrality and sustainable energy transition establish regulatory mandates supporting vacuum contactor procurement across utility, industrial, and transportation sectors. AI-enabled voltage analysis integrated with real-time load balancing algorithms enable proactive transformer maintenance strategies, supporting grid stability improvements and operational efficiency enhancements across distributed power networks.

Rising Demand from Industrial Automation and Power Distribution Modernization

Industrial manufacturing, oil and gas, and mining sectors are systematically upgrading legacy power distribution infrastructure with advanced vacuum contactor solutions supporting improved operational safety, extended equipment life, and reduced maintenance downtime. Vacuum contactors provide superior arc extinction capabilities compared to traditional contactors, delivering longer contact life, minimal contact erosion, and superior dielectric strength supporting demanding industrial applications.

Transformer protection applications increasingly utilize vacuum contactors achieving higher switching frequencies exceeding 10,000 operations, enabling efficient repetitive duty cycles required in industrial power factor correction systems. Motor control applications throughout manufacturing facilities leverage vacuum contactor capabilities supporting high-frequency switching and precise load management optimizing energy consumption across production systems. Manufacturers prioritize low-maintenance solutions reducing operational downtime and supporting lean manufacturing objectives, with vacuum contactors requiring minimal maintenance compared to oil or gas-filled alternatives. Compact designs in vacuum contactor development enable space-saving installations within constrained industrial facilities supporting retrofit applications across existing switchgear infrastructure.

Market Restraints

High Upfront Capital Costs and Complex Integration Requirements

Vacuum contactor systems require substantial upfront capital investment including sophisticated hardware components, specialized installation procedures, and system integration expertise limiting adoption across price-sensitive markets and smaller industrial operators. Complex integration with existing multi-phase power systems and industrial control infrastructure demands specialized engineering support and extended commissioning timelines, creating deployment barriers for organizations lacking technical expertise. Ultra-high-frequency switching applications exceed current vacuum contactor capabilities, limiting market expansion into emerging technology domains requiring advanced switching performance. Specialized components including vacuum interrupters and precision mechanical elements depend on concentrated manufacturing capabilities, creating supply chain vulnerabilities and constrained production capacity limiting market growth during periods of elevated demand.

Technology Transition Uncertainty and Competitive Pressure from Hybrid Solutions

Hybrid solid-state switching solutions and advanced semiconductor technology present competitive alternatives to traditional vacuum contactors, creating technology transition uncertainty and market pressure on established suppliers. Traditional air-insulated contactors continue serving cost-sensitive applications where capital cost reduction outweighs long-term operational efficiency benefits, limiting market expansion opportunities. Rapid technological evolution in smart grid technologies and IoT-enabled devices requires continuous manufacturer investment in research and development supporting capability upgrades, straining financial resources for smaller market participants.

Market Opportunities

Development of Self-Healing Vacuum Interrupters and AI-Powered Monitoring Systems

Next-generation vacuum interrupter technologies incorporating self-healing mechanisms and enhanced durability characteristics enable extended operational life and superior reliability supporting mission-critical applications in nuclear, marine, and oil & gas industries. AI-based predictive maintenance algorithms trained on massive datasets of vacuum contactor operating parameters enable early fault detection, failure prediction, and proactive maintenance scheduling reducing unplanned downtime by 30-38%. Transformer analytics platforms leveraging artificial intelligence enable optimization of switching strategies, transient suppression, and arc mitigation supporting enhanced grid stability.

Self-monitoring vacuum contactors equipped with integrated IoT sensors provide real-time operational diagnostics, enabling condition-based maintenance strategies supporting data-driven asset management. Hybrid solid-state switching solutions combining vacuum contactor reliability with semiconductor switching speed enable exceptional performance characteristics supporting emerging applications in renewable energy control and distributed energy resource management. Advanced material science innovations including ceramic composite materials and nano-engineered contact surfaces enable superior contact erosion resistance supporting extended operational lifespan and reduced replacement frequency.

Expansion into Data Centers and Electric Vehicle Charging Infrastructure

Data center power distribution systems increasingly incorporate vacuum contactors supporting redundant power management, load balancing, and seamless energy source transition enabling sustainability objectives and operational reliability improvements. Electric vehicle (EV) charging infrastructure development creates specialized demand for high-speed vacuum switching supporting dynamic power management and grid stability as EV adoption accelerates globally. Microgrids serving renewable energy projects and industrial facilities require sophisticated switching infrastructure enabling decentralized energy production and demand response optimization.

Renewable energy substations throughout Asia-Pacific, Europe, and North America represent fastest-growing application segments requiring advanced vacuum contactor solutions supporting wind farm integration, solar energy management, and battery storage coordination. Energy storage systems including grid-scale batteries and pumped hydro facilities require advanced switching infrastructure supporting seamless integration with vacuum contactor technology enabling efficient renewable energy management.

Category-wise Insights

Contact Rating Analysis: Medium Voltage Vacuum Contactors

Medium Voltage Vacuum Contactors operating in the 1-36 kV range represent the fastest-growing segment with projected CAGR of 7.1% during 2026-2033, capturing approximately 58% market share in 2025 driven by widespread adoption across utility distribution systems, industrial manufacturing, and renewable energy applications. AC3 current ratings up to 800A at operating frequencies exceeding 10,000 operations enable medium voltage contactors to address demanding industrial motor control applications supporting high-speed switching and repetitive duty cycles.

Modular designs with multi-stage contact arrangements enable manufacturers to address unique application requirements while maintaining manufacturing efficiency and cost-effectiveness. Withdrawable-style contactors incorporating primary protection fuses provide flexible deployment options across diverse electrical infrastructure configurations supporting retrofit applications and new installations.

Product Type Analysis: Spring Type Vacuum Contactors

Spring Type Vacuum Contactors command the dominant market position with approximately 62% market share in 2025, reflecting industry preference for simple mechanical designs, proven reliability, and cost-effective manufacturing processes. Spring-operated mechanisms eliminate electrical holding power requirements, reducing operational energy consumption and supporting sustainable power distribution objectives. Mechanical life ratings exceeding 500,000 operations establish exceptional durability supporting extended equipment lifecycles and reduced maintenance requirements compared to mechanical alternatives.

Standard utilization category ratings aligned with IEC 60470 standards enable straightforward system integration across diverse electrical infrastructure configurations. Single-pole and three-pole configurations provide flexible options addressing diverse application requirements including capacitor switching, motor control, and transformer protection across industrial and utility sectors.

Application Analysis: Motor Control

Motor Control applications represent the leading market segment, capturing approximately 45% of vacuum contactor demand in 2025, driven by industrial manufacturing, mining operations, and transportation sector electrification. High-frequency switching capabilities exceeding 10,000 operations enable efficient control of induction motors supporting frequent start-stop cycling characteristic of industrial production environments. Soft-starting capabilities achieved through vacuum contactor integration reduce mechanical stress on motor systems and extended motor lifespan supporting total cost of ownership reduction.

Oil and gas industries deploy vacuum contactors for critical motor applications requiring mission-critical reliability and minimal maintenance requirements. Transformer coupled motor control designs enable sophisticated load management and demand response optimization supporting industrial automation objectives. Integration with predictive maintenance algorithms enables data-driven maintenance scheduling optimizing operational availability and reducing unexpected production disruptions.

Regional Insights

North America Vacuum Contactor Market Trends and Insights

North America maintains a significant market position with approximately 28% regional share, driven by substantial investments in power grid modernization, automation infrastructure upgrades, and regulatory emphasis on energy efficiency and grid reliability. The United States leads regional adoption through FERC standards requiring advanced metering and renewable energy integration supporting widespread vacuum contactor deployment across utility distribution systems. Industrial automation throughout manufacturing heartland regions including Midwest and Southern states drives vacuum contactor adoption supporting motor control, power distribution, and energy management applications.

Canadian utilities increasingly deploy vacuum contactors supporting smart grid initiatives and renewable energy projects aligned with government climate objectives. Eaton Corporation and established suppliers maintain strong North American market positions through established relationships with major utilities, industrial operators, and system integrators. Energy efficiency regulations including NERC standards and state-level emissions requirements create regulatory tailwinds supporting vacuum contactor procurement across utility and industrial sectors.

Europe Vacuum Contactor Market Trends and Insights

Europe represents a mature market characterized by stringent energy efficiency standards, environmental regulations, and emphasis on renewable energy transition supporting vacuum contactor adoption. Germany, France, and United Kingdom lead regional deployment through smart grid modernization programs and industrial automation initiatives supporting power distribution infrastructure upgrades. EU Directive mandates including energy efficiency requirements and carbon reduction objectives create regulatory tailwinds supporting vacuum contactor procurement across utility and industrial sectors.

Siemens AG and Schneider Electric maintain dominant European positions through comprehensive product portfolios, established relationships with utilities and integrators, and deep expertise in regulatory compliance. Wind energy integration throughout Northern Europe drives vacuum contactor adoption supporting renewable energy management and grid stability improvements. Industrial retrofitting programs modernizing legacy power distribution infrastructure represent significant market opportunity throughout European industrial sectors.

Asia Pacific Vacuum Contactor Market Trends and Insights

Asia Pacific dominates globally with 44% regional market share, driven by explosive industrialization, smart grid investments, and renewable energy deployment. China leads regional adoption through industrial modernization initiatives, smart city projects, and aggressive renewable energy expansion supporting unprecedented vacuum contactor demand. Rapid manufacturing expansion throughout India supported by government incentives and infrastructure investment is catalyzing exceptional market growth exceeding 8% annually.

Japan maintains technological leadership through companies like Toshiba, Fuji Electric, and Mitsubishi Electric developing advanced vacuum contactor technologies and smart switching solutions. ASEAN manufacturing expansion in Vietnam, Thailand, and Indonesia supports growing regional demand through establishment of localized production facilities and supply chain development. Government electrification programs and industrial automation initiatives throughout South Asia and Southeast Asia establish fastest-growing market segments globally.

Competitive Landscape

Market Structure Analysis

The vacuum contactor market is characterized by a moderately concentrated structure, with a limited number of global suppliers complemented by several strong regional and niche participants. Competition is primarily shaped by product breadth, voltage coverage, manufacturing scale, and long-term relationships with utilities and industrial customers. Leading players leverage vertically integrated operations, global distribution networks, and standardized product platforms to secure large infrastructure and energy projects.

Strategic focus areas include innovation in vacuum interrupter design, integration of digital monitoring and diagnostics, compact and modular product architectures, and sustainability-oriented features that support lifecycle efficiency. Regional manufacturers strengthen their position through cost-competitive pricing, localized manufacturing, and responsiveness to domestic infrastructure programs. Smaller players remain competitive by targeting specific applications, offering customization flexibility, and providing faster service and technical support. Overall, business strategies emphasize differentiation through technology, reliability, and lifecycle value rather than aggressive price competition, reinforcing stable competitive dynamics.

Companies Covered in Vacuum Contactor Market

- ABB Limited

- Crompton Greaves Limited

- Fuji Electric

- Joslyn Clark

- Larsen & Toubro Limited

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- TDK Electronics AG

- Toshiba Corporation

- Eaton Corporation

- Mitsubishi Electric

- LS Electric

- Hyundai Electric

- Reinhausen Group

Frequently Asked Questions

The global Vacuum Contactor Market is expected to reach approximately US$ 4.8 billion in 2026.

Key drivers include smart grid deployment, renewable energy integration, industrial power distribution upgrades, and high-frequency motor control applications.

Asia Pacific is expected to lead the market with about 48% share during the forecast period.

The largest opportunity lies in self-healing vacuum interrupters and AI-based monitoring for predictive maintenance and improved reliability.

Major players include ABB, Siemens, Schneider Electric, Eaton, Toshiba, Fuji Electric, Larsen & Toubro, Crompton Greaves, and LS Electric.