- Healthcare Services

- U.S. Short-Term Care Insurance Market

U.S. Short-Term Care Insurance Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Short-Term Care Insurance Market by Type of Plan (Preferred Provider Organisation, Point of Service, Health Maintenance Organisation, Exclusive Provider Organisation, Miscellaneous), Distribution Channel (Direct Sales, Brokers/Agents, Banks, Others, Misc), Age Group (Senior Citizens, Adults, Minors, Misc), End-user( Groups, Individuals, Misc) and Regional Analysis for 2026 - 2033

U.S. Short-Term Care Insurance Market Size and Trends Analysis

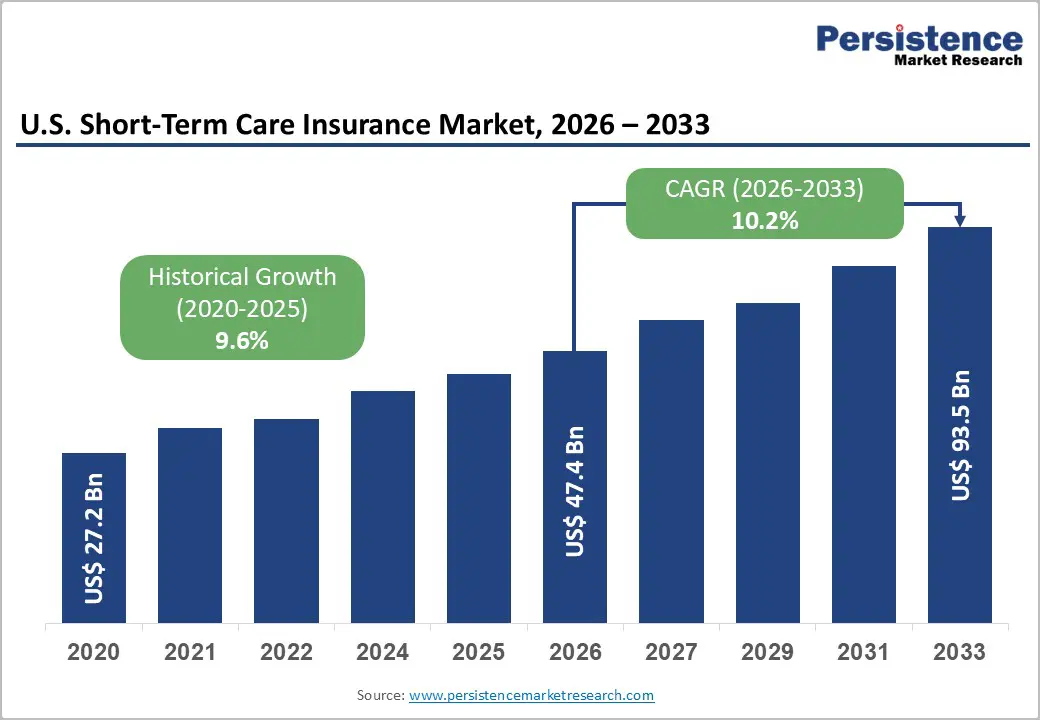

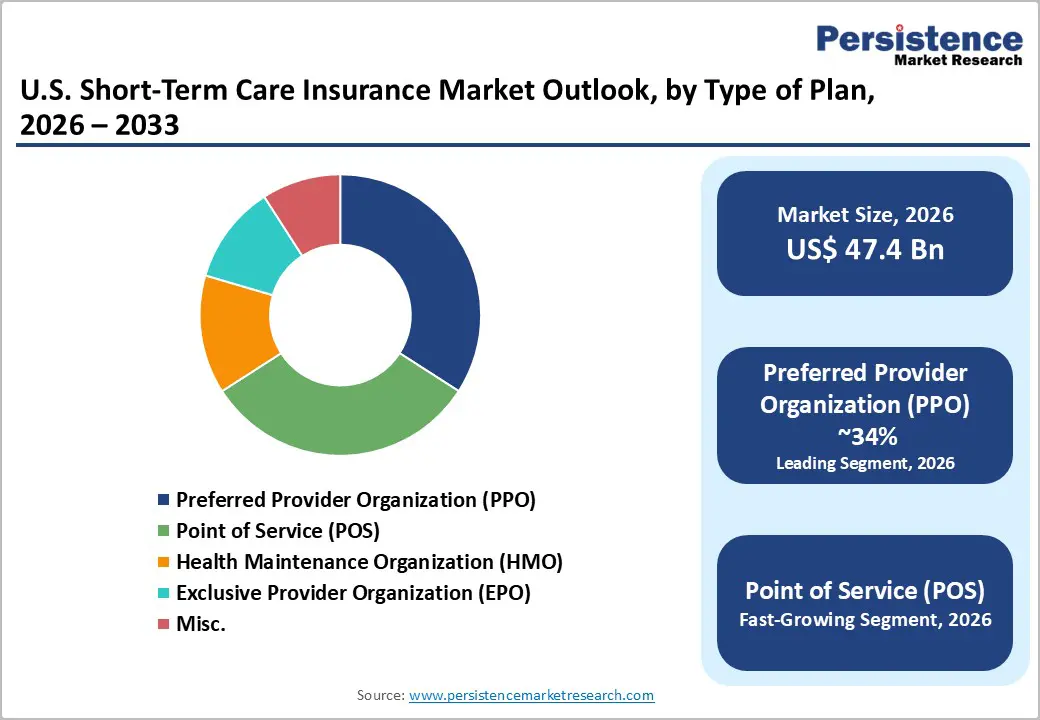

The U.S. Short-Term Care Insurance Market size was valued at US$ 47.4 Bn in 2026 and is projected to reach US$ 93.5 Bn by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

The market expanded from US$ 27.2 Bn in 2020, compounding at a historical CAGR of 9.6% through 2026 a trajectory shaped by structurally elevated demand for flexible, cost-effective alternatives to traditional ACA-compliant health coverage. Three converging forces underpin continued momentum: a shifting federal regulatory posture that is broadening STLDI product permissibility, a confirmed post-2025 reduction in ACA Marketplace subsidy support projected to displace 4–5 million Americans from comprehensive coverage, and an ageing population base that is systematically expanding the addressable consumer pool for short-duration care products.

The expiration of enhanced premium tax credits implemented under the American Rescue Plan Act of 2021 and the Inflation Reduction Act of 2022 is expected to raise Marketplace premiums materially, channelling a measurable volume of health-cost-sensitive consumers toward STLDI plans that are already available in 36 states as lower-cost, non-ACA alternatives.

Key Industry Highlights

- Federal Policy Expansion Drives Market Growth: Regulatory liberalisation in 2025 restored STLDI as a viable coverage option, enabling longer-duration policies and broader access for employers and individuals.

- ACA Coverage Gap Boosts Demand: Expiration of enhanced ACA premium tax credits at end-2025 is projected to push 4–5 million Americans toward affordable STLDI alternatives.

- Senior Population Supports Uptake: With 18% of the U.S. population aged 65+ in 2024, projected to reach 23% by 2050, demand for cost-accessible short-term care products is rising.

- PPO Leads Plan Type Share: Preferred Provider Organisation plans dominate with 44% market share, offering in-network and out-of-network access critical for transitional coverage.

- POS Fastest-Growing Plan Type: Point of Service plans are expanding rapidly, combining primary care coordination with flexible specialist access, appealing to cost-conscious enrollees.

- Leading Individual End-User Segment: Individual enrollees hold ~62% market share, driven by affordability, broad geographic availability across 36 states, and coverage for transitional or pre-Medicare periods.

| Key Insights | Details |

|---|---|

|

U.S. Short-Term Care Insurance Market Size (2026E) |

US$ 47.4 Bn |

|

Market Value Forecast (2033F) |

US$ 93.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.6% |

Market Dynamics

Growth Drivers - Federal Regulatory Liberalisation Restoring STLDI as a Viable Coverage Architecture

Federal policy governing short-term, limited-duration insurance has undergone the most consequential structural realignment in nearly a decade, directly widening the operational and product boundaries of the U.S. Short-Term Care Insurance Market. The direction of this shift from restrictive to permissive has created new product design headroom for insurers and new benefit access pathways for employers and individuals.

In Aug 2025, the U.S. Departments of Labour, Treasury, and Health and Human Services announced that STLDI policies would no longer be confined to the previously mandated three-month limit, effectively restoring them as legitimate employer-sponsored benefit options, while signalling low enforcement priority for non-compliant insurers until new rulemaking is finalised. This was reinforced in August 2025, when the same agencies formally initiated a notice-and-comment rulemaking process to potentially amend STLDI definitions, providing insurers and small businesses with expanded operational leeway.

Further cementing this trajectory, Executive Order 14219 directed federal agencies to reduce regulatory burdens and make health coverage more flexible and cost-efficient. The cumulative impact of these policy signals is a measurable expansion in the addressable product and distribution landscape for STLDI carriers, creating a structural demand catalyst for the market heading into the 2026–2033 forecast period.

ACA Subsidy Cliff and Coverage Gap Demand Surge

A quantified and time-bound structural demand driver for the U.S. Short-Term Care Insurance Market is the expected reduction in ACA Marketplace enrollment following the expiration of enhanced premium tax credits that have anchored affordable coverage access for millions of Americans since 2021. This transition does not represent speculative risk it is a confirmed legislative outcome with a measurable projected impact on insured population volume.

As of mid-2024, the U.S. uninsured rate had fallen to 7.6%, with over 300 million Americans insured under various health coverage structures supported by subsidies that allowed 4 in 5 consumers to find Marketplace coverage for $10 or less per month. However, the scheduled expiration of these enhanced tax credits at the end of 2025 is projected to raise premiums substantially, with 4–5 million Americans expected to lose Marketplace coverage as a direct consequence.

As highlighted by KFF in October 2025, STLDI plans sold across 36 states offer materially lower premiums than ACA-compliant alternatives, positioning the market to capture a measurable share of newly coverage-gap populations during and immediately following the 2025 ACA Open Enrollment period. This confluence of expiring subsidies and a proven STLDI affordability advantage creates a durable, near-term demand inflexion for the market.

Demographic Shift and Senior-Oriented Product Accessibility

Long-term demographic transformation in the U.S. population structure represents a foundational, demand-generative driver for the U.S. Short-Term Care Insurance Market, particularly as the senior population moves beyond accessible income thresholds for traditional long-term care insurance and seeks affordable intermediate-coverage alternatives.

According to the U.S. Census Bureau's 2024 Vintage Population Estimates, the population aged 65 and older rose 3.1% year-over-year to 61.2 million in 2024, now representing 18.0% of the total U.S. population, up from 12.4% in 2004. By 2050, this cohort is projected to reach 82 million, comprising an estimated 23% of the total population (Population Reference Bureau, 2026).

The American Association for Long-Term Care Insurance (AALTCI) documented in its 2024 report that short-term care products now offer gender-neutral premiums and broader underwriting criteria covering home care and skilled nursing services at relatively low cost, making them particularly accessible to older women and individuals with pre-existing health conditions who are typically ineligible for standard long-term care policies. As the working-age-to-senior population ratio continues its projected decline from 2.8:1 in 2025 to 2.2:1 by 2055 the fiscal case for cost-accessible, short-duration care coverage strengthens considerably.

Restraint - Limited Consumer Protections and Adverse Selection Dynamics

A persistent structural challenge constraining broader adoption in the U.S. Short-Term Care Insurance Market is the inherent coverage limitation of STLDI products relative to ACA-compliant plans. Standard STLDI plans exclude pre-existing conditions, impose aggregate benefit caps, and frequently require completion of invasive health questionnaires exposing enrollees to catastrophic out-of-pocket costs if significant medical events occur during the coverage period.

Research cited by the Urban Institute has demonstrated that the unchecked expansion of short-term plans can drive premium increases of up to 18.2% in ACA-compliant market segments due to adverse selection effects, as healthier individuals exit comprehensive pools. These dual risks inadequate protection for enrollees and systemic market destabilization generate ongoing reputational risk and regulatory scrutiny, limiting mass-market adoption, particularly among individuals with chronic conditions or those who require continuity of comprehensive care.

State-Level Regulatory Fragmentation and Geographic Market Constraints

The U.S. Short-Term Care Insurance Market operates under a highly heterogeneous regulatory framework across jurisdictions, creating meaningful compliance complexity and geographic market restrictions for insurers with national product ambitions. As confirmed by KFF , STLDI plans are available in only 36 states, indicating that approximately 28% of the U.S. geographic market is subject to restrictive or prohibitive state-level regulations that preclude meaningful STLDI market participation.

The Washington State Office of the Insurance Commissioner's January 5, 2026, announcement of a public hearing on proposed rules for supplemental long-term care insurance under ESSB 5291 covering premium adequacy, mandatory disclosures, and marketing practice oversight illustrates the intensifying state-level scrutiny that creates incremental compliance burdens and actuarial pricing uncertainty for carriers. This regulatory fragmentation raises operational costs, limits standardised national product portfolios, and creates inconsistent consumer experiences that challenge market scaling

Opportunities - Small Business Employer Channel Expansion via STLDI Legislative Reform

The employer-sponsored benefits segment, particularly among small and mid-size enterprises, represents one of the most actionable and policy-supported near-term opportunities in the U.S. Short-Term Care Insurance Market. Recent federal and legislative signals have created a materially favourable environment for insurers to develop purpose-built, group-oriented STLDI products targeting the underserved small business workforce.

On March 11, 2026, the National Federation of Independent Business (NFIB) formally proposed legislative reforms to expand STLDI access for small businesses, explicitly emphasising extended coverage periods, plan flexibility, and employer cost containment as the primary rationale.

This legislative push is directly supported by deteriorating small business benefit coverage trends: among employers with 10–24 employees, the share offering health benefits declined from 64.9% to 51.8% between 1996 and 2024 (EBRI, 2024), while the take-up rate for medical benefits in small firms dropped from 71% in 2014 to 60% in 2024 (U.S. Bureau of Labor Statistics, 2025). With family coverage, employer premiums at small firms reaching $1,232.59 per month in 2024, a consistent multi-year increase, STLDI products that combine affordability with the newly restored flexibility to exceed three-month duration limits are positioned to fill a measurable employer benefit gap at scale.

Technology-Enabled Digital Distribution and Telehealth Integration

Digital transformation in insurance distribution infrastructure presents a high-impact strategic opportunity to lower customer acquisition costs, enhance plan transparency, and accelerate enrollment for the Short-Term Care Insurance Market. The convergence of AI-driven underwriting, digital quote platforms, and telehealth-integrated plan designs is directly addressing the historical friction points of STLDI adoption, namely, consumer confusion around coverage limitations and enrollment complexity.

Carriers such as Pivot Health (Companion Life Insurance) have already demonstrated the viability of this model by integrating telehealth access with STLDI products, meeting both cost-conscious consumer demands and the transparency standards championed by United States of Care's September 2023 CMS comment letter, which called for clearer benefit disclosures and improved enrollment communications. As the U.S. Departments of Labour, HHS, and Treasury initiate formal notice-and-comment rulemaking to potentially amend STLDI definitions, insurers have a well-defined operational window to redesign and relaunch digital-first product architectures before new compliance frameworks crystallise.

Platforms that embed mandatory, plain-language disclosures, a regulatory expectation reinforced by the March 28, 2024, finalisation of STLDI consumer protection rules, while streamlining enrollment for individuals transitioning between employer plans, ACA Marketplace, or Medicare-eligibility windows, are structurally positioned to capture disproportionate market share.

Category-wise Analysis

Type of Plan Insights

The Preferred Provider Organisation (PPO) segment holds the dominant position in the U.S. Short-Term Care Insurance Market with approximately 44% of total market share in 2026, driven by its structural alignment with the core consumer needs of STLDI enrollees. PPO plans offer access to both in-network and out-of-network providers without mandatory referral requirements, a critical feature for individuals in transitional coverage situations who require care continuity across provider relationships established under prior comprehensive plans.

The PPO model's compatibility with short-term coverage contexts is reinforced by leading STLDI carriers leveraging existing national PPO network infrastructure, exemplified by National General utilising Aetna and Cigna PPO networks to deliver broad provider access at competitive price points. As the federal regulatory environment stabilises following the ongoing STLDI definition rulemaking process, PPO structures are expected to remain the preferred plan architecture for both individual enrollees and employer-sponsored short-term benefit designs.

The Point of Service (POS) segment is the fastest-growing plan type within the U.S. Short-Term Care Insurance Market, reflecting a measurable consumer shift toward hybrid plan models that combine care coordination features with out-of-network access flexibility. POS plans uniquely integrate primary care physician referral pathways characteristic of HMO models with the out-of-network access optionality of PPO structures, offering a cost-management mechanism that resonates with cost-sensitive enrollees who also value specialist access. This dual-value proposition is particularly relevant as the market absorbs a larger cohort of enrollees transitioning from comprehensive ACA plans, who are familiar with care coordination models and seek managed-cost primary care pathways alongside specialist flexibility. The NFIB's March 2026 legislative advocacy for plan flexibility and affordability for small business employees further reinforces POS adoption prospects within the employer-sponsored STLDI channel.

End-user Insights

The Individual end-user segment commands approximately 62% of total market share in 2026, reflecting the market's foundational purpose of serving adults navigating temporary coverage interruptions, job transitions, ageing out of parental coverage, pre-Medicare eligibility gaps, and between-enrollment-period lapses. The individual segment's structural dominance is reinforced by the broad geographic availability of STLDI products across 36 states at premium points materially below ACA-compliant alternatives, as confirmed by KFF in October 2025. The AALTCI's 2024 findings further substantiate the segment's breadth, documenting the accessibility of short-term care products for seniors seeking home care and skilled nursing coverage under gender-neutral premium structures, demonstrating that the individual segment spans both younger transitional enrollees and older Americans seeking lower-cost alternatives to traditional long-term care insurance

The Groups segment represents the fastest-growing end-user category in the U.S. Short-Term Care Insurance Market, propelled by a convergence of deteriorating small business benefit coverage rates and targeted legislative and regulatory support for employer-sponsored STLDI access. The August 25, 2025, federal policy shift restoring STLDI policies beyond the three-month limit as viable employer-sponsored options confirmed by the U.S. Departments of Labour, Treasury, and HHS directly unlocked the structural conditions for employer group STLDI product expansion. Among employers with fewer than 10 employees, only 22.5% offered health benefits by 2024, down from 34.2% in prior years, creating a substantial unmet demand pool that short-term group care products are now positioned to address.

Competitive Landscape

The U.S. Short-Term Care Insurance market is fragmented in nature, with a mix of national insurers, specialized providers, and regional players offering a variety of short-term coverage options. While there are several well-established companies, no single player dominates the market entirely, leading to significant competition and innovation in policy offerings.

Key players in the market include UnitedHealthcare, Pivot Health, Everest, Cigna, Bankers Fidelity Life Insurance Company, and Guarantee Trust Life Insurance Company. These providers offer flexible plans with varying coverage durations, daily benefits, and premium structures, catering to both individual and group policyholders.

Distribution channels are diverse, including direct sales, brokers, online platforms, and financial advisors, which enables companies to reach a broad spectrum of consumers while maintaining competitive pricing. Plans vary widely in terms of daily benefits, elimination periods, and inflation protection, further intensifying competition among insurers.

The market’s fragmented nature allows new entrants and regional insurers to capture niche segments, particularly among seniors or those seeking coverage gaps not addressed by traditional long-term care insurance. Innovation in policy design, ease of enrollment, and cost-effectiveness are key differentiators that companies leverage to expand market share.

Key Industry Developments:

- In 2024, American Association for Long-Term Care Insurance (AALTCI) reported that the U.S. Short-Term Care Insurance market offers increasingly accessible options for seniors, with policies providing home care and skilled nursing coverage at relatively low and gender-neutral premiums, making them an attractive alternative to traditional long-term care insurance, especially for older women and those with existing health conditions.

- September 11, 2023,United States of Care (USofCare) highlighted the U.S. Short-Term Care Insurance market in its comment letter to CMS, supporting the 2024 Short-Term Limited-Duration Insurance rule for establishing stronger consumer protections, improving transparency, and ensuring that individuals understand coverage limitations when enrolling in short-term plans..

Companies Covered in U.S. Short-Term Care Insurance Market

- Guarantee Trust Life Insurance Company

- Bankers Fidelity Life Insurance Company

- Pivot Health

- UnitedHealth / Golden Rule

- Cigna

- Everest Re Group, Ltd.

- IHC Group

- National General Insurance

- Mutual of Omaha

- Transamerica

- Northwestern Mutual

Frequently Asked Questions

The U.S. Short-Term Care Insurance Market is projected to be valued at US$ 47.4 Bn in 2026.

The Preferred Provider Organisation (PPO) segment is expected to account for approximately 30% of the U.S. Short-Term Care Insurance Market by Type of Plan in 2026.

The U.S. short-term care insurance market is expected to witness a CAGR of 10.2% from 2026 to 2033.

U.S. Short-Term Care Insurance market growth is driven by federal regulatory liberalisation restoring STLDI as a viable coverage option, the ACA subsidy expiration creating coverage gaps, and the rising senior population seeking affordable short-term care alternatives.