- Home Care & Utilities

- Household Food Storage Container Market

Household Food Storage Container Market Size, Share, and Growth Forecast, 2026 - 2033

Household Food Storage Container Market by Material (Plastic, Glass, Others), Product Type (Airtight Containers, Vacuum Sealed, Others), Distribution Channel, and Regional Analysis for 2026 - 2033

Household Food Storage Container Market Size and Trends Analysis

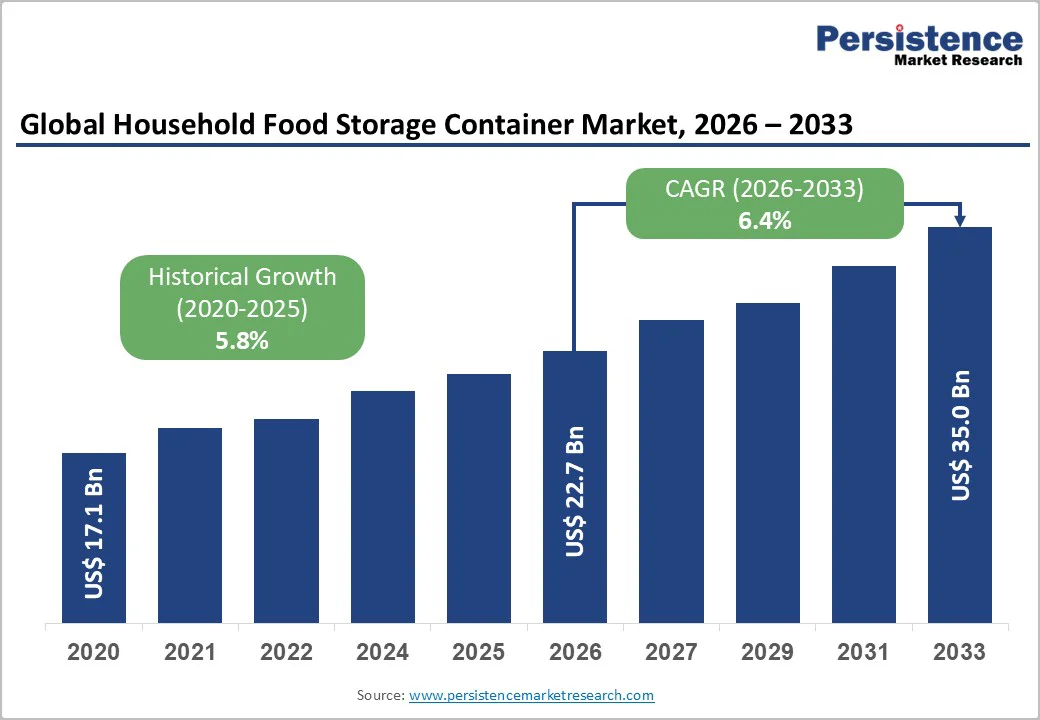

The global household food storage container market size is likely to be valued at US$22.7 billion in 2026 and is expected to reach US$35.0 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

Sustained household shifts toward meal-prepping, home cooking, and bulk purchasing are raising demand for durable, multi-functional storage solutions. Strong consumer substitution toward safer and reusable materials is reshaping product mixes.

Urbanization, expansion of e-commerce, and longer grocery supply chains are reinforcing the importance of preservation, convenience, and transit-safe packaging. Regulatory pressure on single-use plastics is also accelerating transitions toward certified materials, premium glass, and advanced sealed systems.

Key Industry Highlights

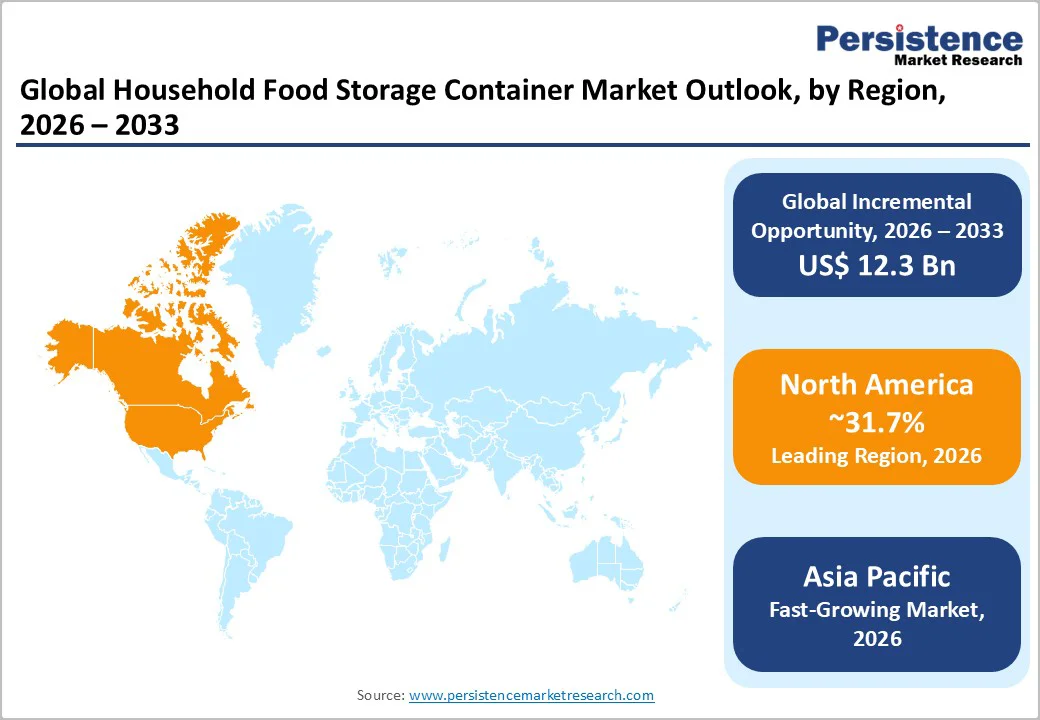

- Leading Region: North America is anticipated to lead with an estimated 31.7% of market share in 2026, driven by high household spending, strong meal-prep culture, and established retail networks.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region with sustained double-digit volume expansion, supported by urbanization, rising incomes, and strong manufacturing capacity.

- Investment Plans: Manufacturers are expanding injection-molding automation, glass-tempering capacity, and recycled-polymer processing, with notable upgrades across the U.S., Germany, China, and India to meet demand for sustainable, reusable containers.

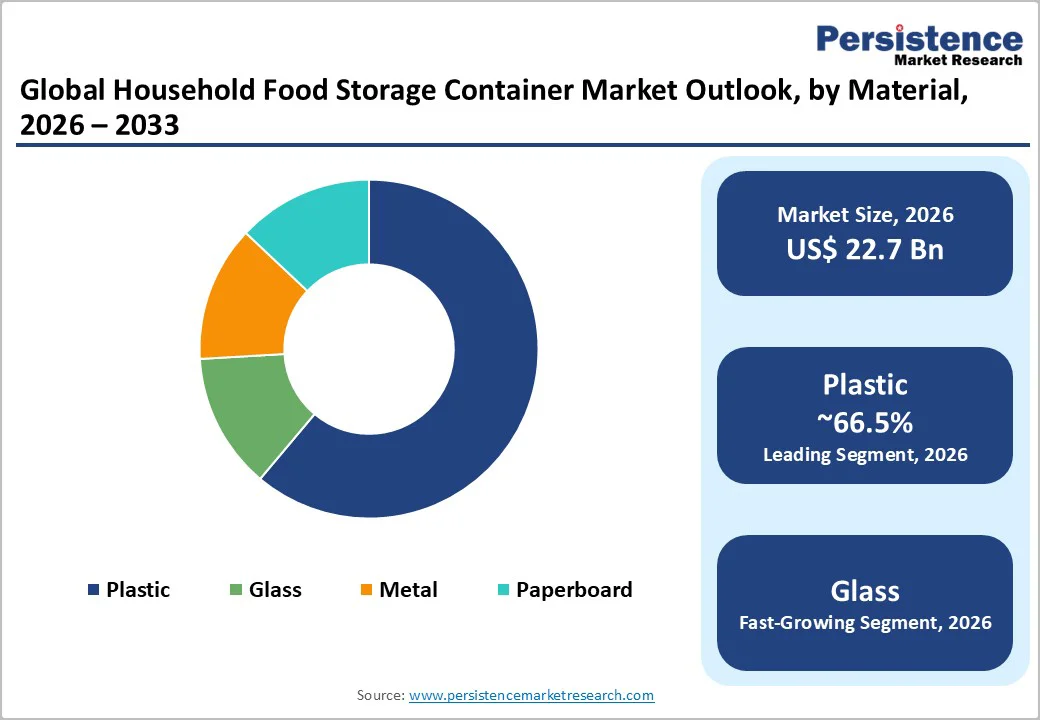

- Dominant Material: Plastic is anticipated to be the dominant segment with an anticipated 66.5% market share in 2026, supported by cost efficiency, versatility, and high retail turnover.

- Leading Product Type: Airtight containers are anticipated to be the leading product type with an expected 54.5% of market share in 2026, driven by their essential role in everyday food preservation and broad supermarket distribution.

| Key Insights | Details |

|---|---|

| Household Food Storage Container Market Size (2026E) | US$22.7 Bn |

| Market Value Forecast (2033F) | US$35.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Shifts in Consumer Behavior toward Meal-Prep, Convenience, and Preservation

Households are adopting meal-prep routines, leftover management habits, and bulk buying at a faster pace, raising the number of containers used per home. Multi-size storage sets, vacuum systems, and microwave-safe or refrigerator-safe lines see strong rotation as families seek to reduce food waste.

Consumers moving from single-item purchases to full multi-piece sets are lifting average selling prices, while e-commerce expansion increases direct-to-consumer sales of premium bundles. Meal-kit services and online grocery retail rely on robust, resealable containers during transit, which intensifies demand for airtight and impact-resistant categories.

These factors collectively sustain a mid-single-digit global growth rate and shift value toward modular and sealed systems.

Regulatory and Safety Pressures Pushing Material Innovation

Food-contact safety regulations and restrictions on specific single-use plastics are pushing manufacturers toward compliant materials with lower migration risk. Regulatory frameworks in major markets require traceability, testing, and documentation for any container used in direct food applications.

Compliance demands investment in improved formulations such as high-quality PET, recycled food-grade resins, and hybrid materials that pair glass with silicone closures. These requirements raise production costs for non-compliant producers but create advantages for companies with certified lines.

The market impact becomes visible in product redesign cycles, reformulated engineered plastics, and increased use of durable alternatives. Regulatory scrutiny is lifting the importance of material safety as a premium feature.

Sustainability Economics and Consumer Willingness to Pay

Sustainability has become an economically relevant differentiator in household storage. A measurable share of consumers now pay a premium for containers with recycled content, long life cycles, or environmentally responsible materials.

This trend is accelerating demand for glass, high-quality plastics with improved durability, and premium sealed systems. Reuse models, refillable packaging programs, and returnable container pilots validate the long-term potential of durable storage solutions.

Manufacturers investing in tempered glass, silicone-sealed hybrid lids, and high-durability polymers capture higher margins through premium price tiers. As sustainability benchmarks rise across the packaging ecosystem, household storage becomes a natural extension of this demand shift.

Barrier Analysis - Raw Material and Input Price Volatility

Volatile resin and plastic feedstock prices create ongoing margin pressure for manufacturers. Many producers operate with thin unit margins in commodity SKUs, where a modest increase in input cost can significantly impact profitability.

Companies investing in food-grade recycled resins or in dual-material tooling face high capital requirements, forcing them to choose between raising retail prices and absorbing margin erosion. Plastic-based container categories are the most sensitive, with typical contract structures experiencing 3-8%-point margin swings in 12 months when polymer markets fluctuate.

Fragmented Retail Landscape and Channel Margin Compression

Supermarkets, mass retailers, online marketplaces, and specialty stores exert considerable pricing pressure on suppliers. Retailers often demand promotions and feature pricing, while online channels increase costs through higher return rates, packaging for shipment, and logistics charges.

These dynamics favor large-scale suppliers and private-label programs that can operate at lower cost structures. Branded players face challenges maintaining premium pricing unless they differentiate through verified quality, certified materials, or enhanced product features.

Opportunity Analysis - Premiumization through Preservation Technology and Value-Added Features

Advanced features such as vacuum sealing, anti-spill gasket technology, antimicrobial coatings, and modular nesting systems unlock meaningful pricing power. Premium sealed systems reduce food waste, support meal-prepping, and extend shelf life, making them attractive to families and urban consumers.

Market assessments indicate that premium and technology-enhanced categories could contribute roughly 15-20% incremental market value by 2030 if current adoption patterns continue. Manufacturers with integrated accessories (pumps, replacement lids, seal subscription programs) can leverage subscription revenue and strengthen customer retention.

High-Growth Emerging Markets and Appliance Convergence

Asia Pacific and select Latin American markets present strong expansion opportunities driven by urbanization and rising middle-class purchasing power. Local manufacturing combined with export capability offers margin advantages, while alliances with appliance brands or meal-kit providers create integrated kitchen systems.

In APAC cities, rapid household formation contributes to faster unit turnover. Companies that focus on these markets could capture an additional 12-18% revenue uplift over a five-year horizon by tailoring product lines to compact, multi-functional, and value-enhanced designs.

Category-wise Analysis

Material Insights

Plastic remains the dominant segment, anticipated to hold 66.5% of market share, because it offers strong versatility, low cost, and high production throughput. The material’s lightweight profile simplifies logistics and supports supermarket distribution where bulk multipacks remain highly price-sensitive.

Polypropylene and PET lines form the backbone of most mass-market assortments, especially in private-label programs where scale purchasing reduces cost. Plastic’s shatter resistance, transparency options, and suitability for both rigid and flexible formats sustain its leadership position in households prioritizing convenience and affordability.

Manufacturers with large-scale injection molding facilities and integrated resin sourcing continue to outperform smaller players based on cost competitiveness. Brands such as Rubbermaid, LocknLock, and Tupperware maintain large plastic-dominant portfolios to serve high-rotation retail SKUs, demonstrating how entrenched plastic formats remain across global markets.

Glass is witnessing the fastest growth as health- and sustainability-minded consumers seek durable, long-life food-storage options. Innovations in lightweight tempered glass have reduced breakage risks, while silicone-sealed hybrid lids enhance usability and leak resistance. Consumers favor glass for its inert, non-reactive properties and premium look.

European restrictions on certain plastics are accelerating their regional uptake, while North American households increasingly adopt reusable, oven-to-fridge meal-prep sets. Brands such as Pyrex, Anchor Hocking, and IKEA’s 365+ series reflect this trend with heat-resistant lines suited for baking, reheating, and cold storage, supporting higher price points and strong cross-category growth.

Product Type Insights

Airtight containers dominate the market with an estimated 54.5% share, driven by their essential role in household food preservation, leak prevention, and everyday use for dry goods, leftovers, and meal prep. Their stackable, modular designs and compatibility with refrigerators and microwaves enhance convenience for busy households.

Retailers prioritize airtight assortments due to steady 3-5-year replacement cycles, strong repeat purchases, and high basket value. Popular lines such as OXO Good Grips POP, Tupperware One Touch, and Cello Checkers reinforce their appeal across premium and mass-market segments, often serving as entry points into upgraded silicone-gasket and click-lock formats.

Vacuum-sealed containers are growing the fastest as consumers adopt advanced preservation methods to reduce waste and extend the freshness of produce, grains, prepared meals, and high-value proteins. Improved manual and electric pumps, paired with integrated valve lids, have lowered system costs and simplified use.

Adoption is also rising among small restaurants, bakeries, and hospitality operators buying in bulk. Strong direct-to-consumer marketing, featuring starter kits, subscription valve replacements, and accessory bundles, has accelerated uptake. Brands such as Zwilling Fresh & Save, FoodSaver, and Status Slovenia illustrate this expanding multichannel momentum.

Regional Insights

North America Household Food Storage Container Market Trends - Premiumization, Safety-Driven Material Shifts & Retail Innovation

North America is projected to hold the largest market share at 31.7%, driven by high per-capita kitchenware spending, a strong meal-prep culture, and widespread adoption of durable, premium storage solutions. The U.S. leads consumption due to higher household incomes, frequent home cooking, and robust omnichannel retail networks.

Urban households increasingly favor modular glass sets, upgraded airtight systems, and silicone-lid hybrids as they prioritize durability, organization, and food-waste reduction. Brands such as Rubbermaid, Pyrex, and OXO continue to influence expectations through improved sealing technologies and dishwasher-safe premium lines.

Consumer preferences across the region are increasingly shifting toward reusable, health-aligned, and eco-friendly materials. Substitution from basic plastics to glass and hybrid formats is accelerating, partly influenced by the FDA reviews on food-contact materials and public scrutiny of BPA alternatives.

In Canada, the demand rises for children’s lunch storage, leak-proof travel containers, and silicone-based products. Major retailers, including Canadian Tire and Loblaws, have expanded eco-labeled private-label assortments, strengthening consumer trust and boosting adoption of safer, reusable solutions.

The regulatory landscape is stringent, with U.S. federal and state-level requirements shaping material formulation and design choices. California’s restrictions on certain additives and ongoing PFAS reviews are pushing manufacturers toward safer resin blends and alternative materials.

These expectations create high entry barriers but strengthen the position of established brands with compliant supply chains. Regional investments include automation upgrades by Newell Brands and expansions in recycled-polymer processing. Mid-sized companies are also increasing direct-to-consumer channels, while producers offering modular designs, replacement lids, and premium sealing systems continue to gain market share.

Europe Household Food Storage Container Market Trends - Sustainability-Led Upgrades, Circular Design & Regulatory Compliance

Europe is a mature yet value-expanding market where sustainability and premium materials significantly influence consumer choices. Value growth is driven by rising demand for durable glass containers, silicone-sealed hybrids, and recyclable materials.

Germany, the U.K., France, and Spain remain the leading markets, with Northern Europe leaning toward premium-quality modular sets. Companies such as IKEA, Curver, and Luminarc enhance category momentum through product lines built around recyclability, long-use durability, and aesthetic appeal. Consumers increasingly prioritize lifecycle value, transparency in materials, and proven recyclability.

Retailers such as Sainsbury’s, REWE, and Carrefour have strengthened store-brand sustainability standards, accelerating the transition away from single-use plastics. This creates a favorable environment for producers specializing in recyclable and certified containers.

Europe’s regulatory influence remains strong, with bans on certain single-use plastic formats, rigorous food-contact testing, and design-for-recyclability requirements. Extended Producer Responsibility obligations add operational costs but reward brands with advanced compliance systems.

Investment activity in Europe includes capacity modernization in glass production facilities, such as Arc International’s upgrades in France, and expansion of silicone technology manufacturing in Italy and Germany. Producers increasingly adopt circular-economy initiatives, including take-back pilots and recycled-content programs.

For market entrants, Europe rewards high-quality materials, verified certifications, and clear sustainability narratives. Established brands maintain strong positions by combining design innovation with retailer partnerships and compliance-focused production systems.

Asia Pacific Household Food Storage Container Market Trends - Rapid Urban Demand, Multi-Functionality & Manufacturing-Driven Growth

Asia Pacific is the fastest-growing region, driven by rapid urbanization, rising household incomes, and strong regional manufacturing capabilities. China holds the largest volume share due to its extensive production base and broad distribution networks.

Leading brands such as Supor, LocknLock, and Joyoung are accelerating the shift toward reusable, microwave-safe, and multifunctional storage formats. Japan remains a premium market where companies such as Zojirushi and Hario shape consumer expectations through advanced glass technologies and precision-sealing mechanisms.

India and ASEAN markets are expanding quickly as home cooking rises, food-safety awareness improves, and consumers seek compact, stackable containers suitable for smaller living spaces.

Growing penetration of refrigerators and microwaves further increases demand for heat-resistant, leak-proof, and modular storage solutions. E-commerce platforms, including Shopee, Flipkart, and Tmall, play a critical role by offering wider SKU availability and promoting mid-tier and premium upgrades.

Regulatory frameworks vary significantly across the region. China’s GB standards and Japan’s strict food-contact regulations encourage higher documentation and improved material hygiene, while India and several ASEAN countries continue transitioning toward harmonized guidelines. Manufacturers often adapt formulations and certifications to meet local compliance expectations.

Investment momentum remains strong, with injection-molding and blow-molding capacity expanding across China, India, and Vietnam. Global companies such as Tupperware and LocknLock have strengthened APAC production lines to support both regional consumption and export demand. The region’s dual position as a manufacturing powerhouse and rapidly evolving consumer market ensures sustained growth across value-driven and premium product segments.

Competitive Landscape

The global household food storage container market is moderately fragmented, with a mix of multinational consumer-goods companies, regional manufacturers, and strong private-label participation. Global brands lead in premium airtight, glass, and vacuum-sealed systems, while private labels dominate supermarkets with high-volume plastic sets.

North America and parts of Europe favor consolidated branded portfolios, whereas Asia Pacific relies heavily on large OEM and ODM suppliers serving domestic and export demand. Competition centers on material quality, design, certifications, pricing, and channel reach. Leading players prioritize premiumization, sustainability, direct-to-consumer growth, and cost-efficient modular innovations to maintain a competitive advantage.

Key Industry Developments

- In May 2025, Rubbermaid unveiled its VentSmart line of leak- and spill-resistant glass and plastic food storage containers, incorporating vacuum-vent technology and modular designs to improve freshness retention and stackability.

- In March 2025, Coles Group partnered with Chef Curtis Stone to roll out a special-edition line of six leak-proof glass containers with a manual vacuum pump, designed for storing, cooking, and serving in one versatile solution, boosting consumer interest in multi-function storage.

Companies Covered in Household Food Storage Container Market

- Newell Brands (Rubbermaid)

- Tupperware Brands

- Lock & Lock

- Pyrex

- Anchor Hocking

- OXO

- IKEA

- Hamilton Housewares

- Sistema Plastics

- Ziploc (SC Johnson)

- Snapware

- Glasslock

- Wellberg

- Cello World

- Signoraware

- Milton (Hamilton Group India)

- Komax

- Ozeri

- Status Slovenia

- Trudeau Corporation

Frequently Asked Questions

The global household food storage container market size in 2026 is estimated at US$22.7 billion.

The household food storage container market is projected to reach US$35.0 billion by 2033.

The projected growth rate is 6.4% per year from 2026 to 2033.

Key trends include the rising consumer demand for reusable, durable, and sustainable materials; growing preference for airtight and vacuum-sealed containers to minimize food waste; and increasing sales through online retail channels.

Plastic is the leading material segment, accounting for approximately 66.5% of the household food storage container market.

Major players include Newell Brands (Rubbermaid), Tupperware Brands, Lock & Lock, and OXO.