- Processed Food

- Cannabis Infused Edible Products Market

Cannabis Infused Edible Products Market Size, Share, and Growth Forecast, 2026 - 2033

Cannabis Infused Edible Products Market by Food (Gummies, Chocolate, Mints & Tarts, Brownies & Cookies), Distribution Channel (Offline, Online), Beverages (Energy Drinks, Herbal Tea, Fruit Juices), and Regional Analysis for 2026-2033.

Cannabis Infused Edible Products Market Share and Trends Analysis

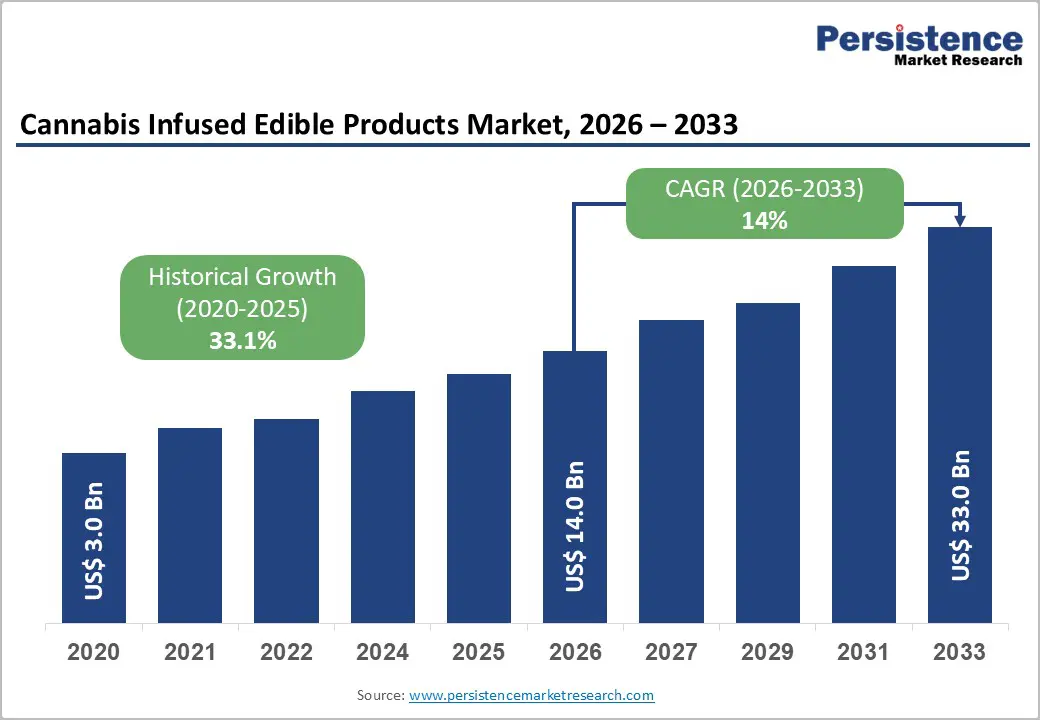

The global cannabis infused edible products market size is likely to be valued at US$ 14.0 billion in 2026, and is projected to reach US$ 33.0 billion by 2033, growing at a CAGR of 14% during the forecast period 2026−2033. Market expansion is primarily driven by the continued rollout of progressive legalization and decriminalization frameworks across North America, Europe, and selected Asia Pacific jurisdictions. Regulatory clarity is enabling formal retail channels, standardized product labeling, and quality controls, which are collectively strengthening consumer confidence.

At the same time, rising acceptance of cannabis-based products for both recreational use and medical applications is expanding the addressable consumer base across age groups and lifestyle segments. Product innovation is increasingly shaping competitive differentiation within the cannabis infused edibles market. Manufacturers are investing in research and development to improve taste profiles, dosing precision, and bioavailability while ensuring longer shelf life and consistent potency. Advances in food science, encapsulation technologies, and controlled-release formulations are supporting the development of gummies, chocolates, baked goods, and beverages that deliver predictable effects and improved user experiences. Companies are also tailoring product formats and cannabinoid compositions to meet diverse consumer needs, including wellness-oriented, low-dose, and functional edible offerings. These developments are expected to position cannabis infused edibles as a preferred consumption format, particularly among first-time users and health-conscious consumers seeking smoke-free alternatives.

Key Industry Highlights

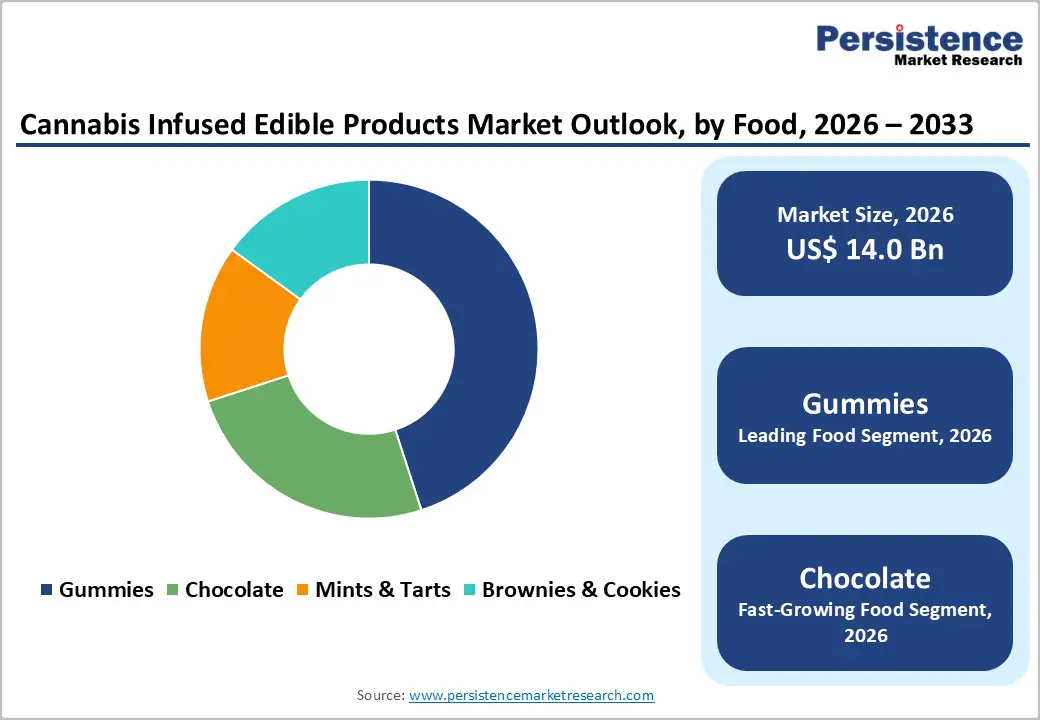

- Food Leadership: Gummies are poised to lead, with approximately 45% revenue share in 2026, while chocolate posts the highest CAGR during the 2026-2033 forecast period.

- Beverage Dominance: Fruit juices are likely to dominate at 52% in 2026, while energy drinks are expected to be the fastest-growing segment over the 2026-2033 forecast period.

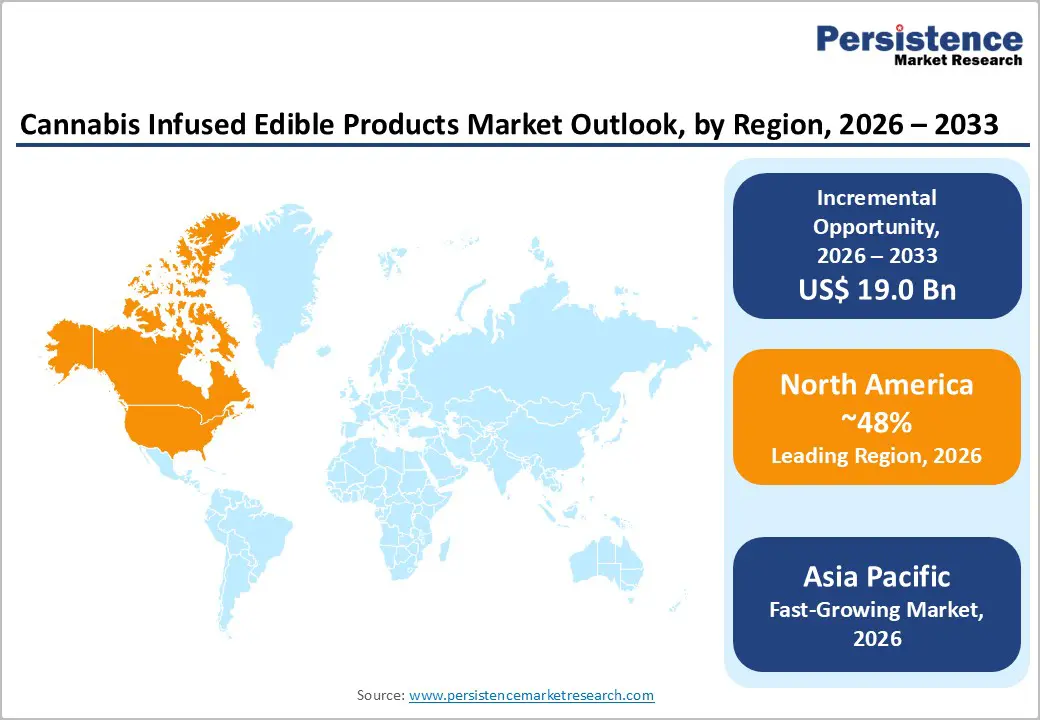

- Dominant Region: North America is projected to command about 48% of the market share in 2026, on account of supportive regulatory frameworks and substantial investment capital.

- Fastest-growing Region: The Asia Pacific market is set to be the fastest-growing through 2033, due to medical cannabis legalization in Southeast Asian countries and Oceania.

- Key Driver: Health-conscious consumers actively choose cannabis edibles over traditional smoking methods as they increasingly value the perceived health advantages and discreet consumption options.

- Key Opportunity: Progressive legalization of cannabis across multiple countries and the U.S. has created substantial growth opportunities for the cannabis-infused edibles market.

- January 2026: Aurora Cannabis secured European Union (EU) Community Plant Variety Rights for its proprietary Farm Gas and Sourdough strains, strengthening its international medical cannabis genetics portfolio.

| Key Insights | Details |

|---|---|

| Cannabis Infused Edible Products Market Size (2026E) | US$ 14.0 Bn |

| Market Value Forecast (2033F) | US$ 33.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14% |

| Historical Market Growth (CAGR 2020 to 2025) | 33% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Consumer Health Consciousness and Alternative Consumption Preferences

Health-conscious consumers actively choose cannabis edibles over traditional smoking methods. They value the perceived health advantages and discreet consumption options. Professionals manufacture these edibles with precise dosing controls. This approach meets consumer needs for consistent effects and reliable experiences. They prioritize wellness benefits such as stress reduction, improved sleep quality, and effective pain management. Manufacturers integrate functional ingredients into these products. Common additions include adaptogens (stress-reducing botanicals), vitamins, and herbal extracts. These enhancements align cannabis edibles with established nutraceutical trends. Nutraceuticals deliver health benefits beyond basic nutrition through natural products.

This strategic positioning creates multiple business opportunities. Companies achieve easier market entry through familiar wellness channels. Consumers recognize these patterns from mainstream health products. Repeat purchases increase as trust in predictable outcomes develops. Businesses gain expanded distribution options. Retailers in health food stores and pharmacies welcome these aligned offerings. Product developers secure flexibility to innovate. They create hybrid formulations that combine cannabis benefits with proven nutraceutical compounds. Market acceptance accelerates when brands emphasize transparency in sourcing and testing.

Product Safety Concerns and Quality Inconsistencies

Unintentional overconsumption incidents create significant challenges for cannabis edibles manufacturers. Inexperienced users often misjudge appropriate dosages. This problem worsens because edible products feature a delayed onset of effects. Consumers frequently consume additional servings before the initial effects appear. Pediatric accidental exposures also generate substantial negative publicity. These events damage brand reputations and erode public trust. Less mature markets face additional challenges with quality control. Contamination risks and inaccurate potency levels undermine consumer confidence. Inconsistent labeling practices further complicate safe usage. Regulatory authorities respond with stringent measures. Governments impose lower potency caps and mandate child-resistant packaging. Extensive warning labels become standard requirements across jurisdictions.

Manufacturers must implement proactive risk mitigation strategies. Companies establish rigorous quality assurance protocols from cultivation through final packaging. Third-party laboratory testing verifies potency accuracy and screens for contaminants. Clear dosage education campaigns address delayed onset characteristics. Brands develop consumer guidance materials that provide precise serving recommendations. Packaging innovations enhance child safety while maintaining adult accessibility. Executives prioritize transparent communication about product limitations. Forward-thinking firms invest in user education platforms and dosage calculators. Strategic partnerships with healthcare professionals lend credibility to safety messaging. Regulatory compliance teams monitor evolving standards across jurisdictions.

Increasing Legalization and Regulation of Cannabis across Various Regions

Progressive legalization of cannabis across multiple countries and U.S. states creates substantial growth opportunities for the cannabis-infused edibles market. Governments increasingly authorize both medical and recreational cannabis use, which expands addressable consumer populations significantly. Medical legalization attracts healthcare-focused consumers seeking therapeutic benefits such as pain management and sleep support. Recreational legalization captures younger demographics, prioritizing social consumption experiences. This dual-market expansion generates predictable revenue streams for manufacturers who establish early compliance infrastructure.

Companies that navigate complex regulatory landscapes gain sustainable competitive advantages. Effective compliance teams monitor evolving potency limits, packaging requirements, and labeling standards across jurisdictions. Legal experts secure the necessary production licenses and distribution permits before market openings. Operations leaders standardize quality assurance protocols compatible with multiple regulatory frameworks. Forward-thinking executives prioritize geographic diversification strategies that balance mature markets with emerging markets poised for legalization. Firms demonstrating regulatory excellence attract premium partnerships with mainstream retailers and healthcare providers.

Category-wise Analysis

Food Insights

Gummies are projected to dominate in 2026, commanding approximately 45% of the cannabis-infused edible products market revenue share. This leadership position stems from precise dosing capabilities enabling consistent 5mg or 10mg tetrahydrocannabinol (THC) units, extended shelf life of 12-18 months, extensive flavor variety appealing to diverse taste preferences, and discreet consumption characteristics. Manufacturing efficiency allows competitive pricing while maintaining quality standards. The segment benefits from established gummy vitamin familiarity, child-resistant packaging compatibility, and regulatory acceptance across most legalized jurisdictions, positioning gummies as the preferred entry point for cannabis-curious consumers.

Chocolate is likely to be the fastest-growing segment during the 2026-2033 forecast period. These products are particularly appealing due to their variety in flavors, textures, and forms, providing consumers with multiple choices. Chocolates can be easily infused with precise dosages of THC or CBD, making them a favored option for both recreational and medical use. The popularity of these products is further enhanced by their discreet nature, allowing consumers to enjoy cannabis without drawing attention.

Beverages Insights

Fruit juices are poised to emerge as the dominant application segment, capturing an estimated 52% of the market revenue share in 2026. This dominance reflects consumer familiarity with juice formats, natural flavor profiles effectively masking cannabis taste, and perceived health associations with fruit-based beverages. Products range from traditional orange and cranberry juices to exotic blends incorporating superfruits and functional ingredients. The segment benefits from established beverage manufacturing infrastructure, straightforward formulation processes, and broad demographic appeal. Major producers include Canopy Growth's Quatreau line and Lagunitas Hi-Fi Hops. Regulatory advantages exist, as juices face fewer marketing restrictions than other cannabis products in certain jurisdictions, facilitating mainstream positioning.

Energy drinks are expected to be the fastest-growing segment over the 2026-2033 forecast period. Energy drinks combine THC, caffeine, B vitamins, and adaptogens to deliver targeted energy, focus, and stress-resilience benefits. Younger demographics aged 21-35 actively seek these alternatives to conventional energy drinks and pre-workout supplements. Health-conscious consumers value cleaner formulations that avoid synthetic stimulants and excessive sugars. Mainstream retail partnerships validate product legitimacy and accelerate distribution.

Distribution Channel Insights

Offline channels are expected to lead with an approximate 70% revenue share in 2026. Dispensaries and licensed specialty cannabis retailers provide compliance assurance, knowledgeable budtender staff offering consumption guidance, immediate product availability, and trusted environments, particularly valuable for first-time consumers. These channels enable tactile product examination, face-to-face education on dosing questions and effect profiles, and curated selections that emphasize quality over quantity. Regulatory requirements in most jurisdictions mandate licensed retail, ensuring offline channel primacy. The segment benefits from experiential retail trends, community-building, and consultation services, thereby differentiating cannabis retail from conventional commerce.

Online channels are predicted to be the fastest-growing during the 2026-2033 forecast period. Online shopping transforms cannabis edibles purchasing through unmatched convenience and information access. Consumers compare products side-by-side, evaluating potency levels, flavor profiles, ingredient transparency, and pricing across multiple brands. Verified customer reviews provide authentic usage experiences, dosage guidance, and quality assessments unavailable through traditional retail channels. Direct-to-doorstep delivery eliminates dispensary visits and maintains complete purchase privacy. Platforms enhance decision-making with comprehensive educational resources. Dosage calculators help determine appropriate serving sizes based on tolerance and desired effects.

Regional Insights

North America Cannabis Infused Edible Products Market Trends

North America is set to command a significant share of the cannabis-infused edible products market, at about 48% in 2026. The regional market benefits from advanced regulatory frameworks and substantial investment capital. Progressive state-level legalization expands consumer access across multiple jurisdictions. Mature markets demonstrate sophisticated consumer preferences and intense competitive dynamics. The United States leads regional performance through established production infrastructure and distribution networks. Canada maintains federally regulated systems that enable banking access and interprovincial commerce. These structural advantages support consistent market expansion and operational predictability.

Strategic investment flows target vertical integration and technology innovation. Venture capital and private equity firms prioritize manufacturers that demonstrate mastery of regulatory compliance. Companies build multi-brand portfolios to capture diverse consumer segments. Advancements in technology enhance cultivation efficiency, extraction precision, and product formulation consistency. Innovation centers drive global trends in nano-emulsification techniques and effect-specific cannabinoid delivery systems. Executives position operations for potential federal legalization scenarios through multi-state footprints and scalable manufacturing platforms. Regulatory evolution discussions include banking reform legislation and potential Food and Drug Administration (FDA) oversight frameworks.

Europe Cannabis Infused Edible Products Market Trends

Europe is an instrumental market for cannabis-infused edible products. Germany leads recreational legalization efforts across the continent. This development establishes Europe's largest addressable consumer population. The Netherlands maintains established tolerance policies while advancing formal regulatory structures. Switzerland implements pilot programs that test commercial viability and generate policy insights. The United Kingdom sustains restrictive recreational policies while expanding medical cannabis prescription capabilities through the National Health Service (NHS). France and Spain advance medical frameworks through active regulatory consultations.

Strategic market entry requires positioning across diverse regulatory environments. Good Manufacturing Practice (GMP) compliance creates substantial barriers that favor established pharmaceutical and food manufacturers. Executives prioritize therapeutic benefit validation through clinical partnerships and healthcare provider networks. These models balance business-to-business (B2B) pharmaceutical channels with direct-to-consumer wellness distribution. Regulatory monitoring teams track harmonization opportunities across EU member states. These capabilities position firms to capture disproportionate market share during accelerated liberalization phases while maintaining compliance excellence.

Asia Pacific Cannabis Infused Edible Products Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for cannabis infused edible products through 2033. Countries such as Australia and Thailand have been advancing medical cannabis legalization through structured regulatory frameworks. For example, Australia has established clear licensing pathways for cultivation and distribution, with the Therapeutic Goods Administration (TGA) approving compliant manufacturing facilities. On the other hand, Thailand has opened commercial operation opportunities following decriminalization measures. Healthcare providers integrate cannabis therapeutics into established treatment protocols. Pharmaceutical companies explore formulation partnerships with regional botanical producers. Consumers gain familiarity with medical benefits through professional medical guidance.

Manufacturing hubs leverage existing botanical extraction infrastructure to achieve cost-efficient production. Investment capital prioritizes medical-grade facilities rather than recreational consumer branding. Cultural acceptance accelerates through healthcare professional endorsements instead of direct-to-consumer advertising campaigns. Companies develop region-specific formulations that combine cannabis active compounds with traditional ingredients such as turmeric, ginseng, or ashwagandha. Regulatory monitoring teams actively track policy evolution across ASEAN member states and bilateral trade frameworks.

Competitive Landscape

The global cannabis infused edible products market structure is moderately fragmented. Curaleaf Holdings, Trulieve Cannabis, Green Thumb Industries, Aurora Cannabis, and Cresco Labs collectively control an estimated 35–40% of market revenues. These players are strengthening their competitive positions by deploying multi-brand portfolio strategies that are targeting distinct consumer segments, including recreational users, medical patients, and wellness-focused buyers. Vertical integration across cultivation, processing, and retail operations is improving cost control, product consistency, and regulatory compliance, while geographic expansion across multiple state-level markets is reducing revenue concentration risk. Product differentiation is increasingly centered on formulation quality, dosage precision, and flavor innovation, which are supporting premium pricing strategies and brand loyalty in maturing markets.

Competitive dynamics are further evolving as conventional food, beverage, and pharmaceutical corporations are increasingly entering the cannabis infused edibles segment through strategic investments, partnerships, and selective acquisitions. These entrants are contributing advanced manufacturing capabilities, established distribution networks, and deep consumer analytics expertise, which are accelerating category professionalization. At the same time, companies are actively navigating complex regulatory frameworks that vary by jurisdiction, particularly around labeling, dosage limits, and marketing restrictions. As regulatory clarity continues improving, leading cannabis operators are expected to have strengthened their market positions by combining cannabis-specific operational expertise with consumer packaged goods discipline, positioning them to scale efficiently while responding to changing consumer preferences and compliance requirements.

Key Industry Developments

- In January 2026, Edible Brands launched Edibles.com, a nationwide e-commerce platform reaching 65% of Americans with lab-tested, hemp-derived THC edibles and drinks from premium brands such as Wyld, Wana, and Kiva. The platform offers same-day delivery and categorization by wellness outcomes such as sleep, stress relief, pain management, and energy.

- In December 2025, Curaleaf Holdings entered a binding Equity Purchase Agreement to acquire The Cannabist Company's Virginia operations, including a cultivation facility, five dispensaries, and rights to one additional store, for US$ 110 million. The deal is expected to close Q1 2026 pending approvals.

- In April 2025, North Dakota passed the signed House Bill 1203 into law, enabling medical cannabis patients to access regulated "cannabinoid edible products" such as soft or hard lozenges in geometric square shapes containing cannabis concentrate or dried leaves/flowers.

Companies Covered in Cannabis Infused Edible Products Market

- Curaleaf Holdings, Inc.

- Trulieve Cannabis Corp.

- Green Thumb Industries Inc.

- Canopy Growth Corporation

- Aurora Cannabis Inc.

- Cresco Labs Inc.

- Tilray Brands, Inc.

- Verano Holdings Corp.

- Wana Brands

- Kiva Confections

- Plus Products Inc.

- Sundial Growers Inc.

- Organigram Holdings Inc.

- HEXO Corp.

- The Cannabist Company Holdings Inc.

Frequently Asked Questions

The global cannabis infused edible products market is projected to reach US$ 4.4 billion in 2026.

Progressive legalization, therapeutic validation, and consumer preference for discreet non-smoking consumption drive the market.

The market is poised to witness a CAGR of 3.6% from 2026 to 2033.

Legalization of cannabis-infused edibles in Southeast Asia and Oceania, functional beverage innovation, and mainstream retail partnerships represent key market opportunities.

Curaleaf Holdings, Inc., Trulieve Cannabis Corp., Green Thumb Industries Inc., Aurora Cannabis Inc. and Cresco Labs Inc. are some of the key players in the market.