- Automotive

- Usage-based Insurance for Automotive Market

Usage-based Insurance for Automotive Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Usage-based Insurance for Automotive Market by Policy Type (Pay-As-You-Drive (PAYD), Pay-How-You-Drive (PHYD), Manage-How-You-Drive (MHYD)), Technology (OBD-II-based UBI, Smartphone-based UBI, Black Box-based UBI, Embedded System-based UBI, Others), Vehicle Age (New Vehicles (Connected/OEM-integrated systems), Used Vehicles (Aftermarket telematics devices)), Vehicle Type (Passenger Vehicles (Dominant Segment), Commercial Vehicles (Fleet-focused adoption)), and Region Analysis for 2026 to 2033

Usage-based Insurance for Automotive Market Trends & Analysis

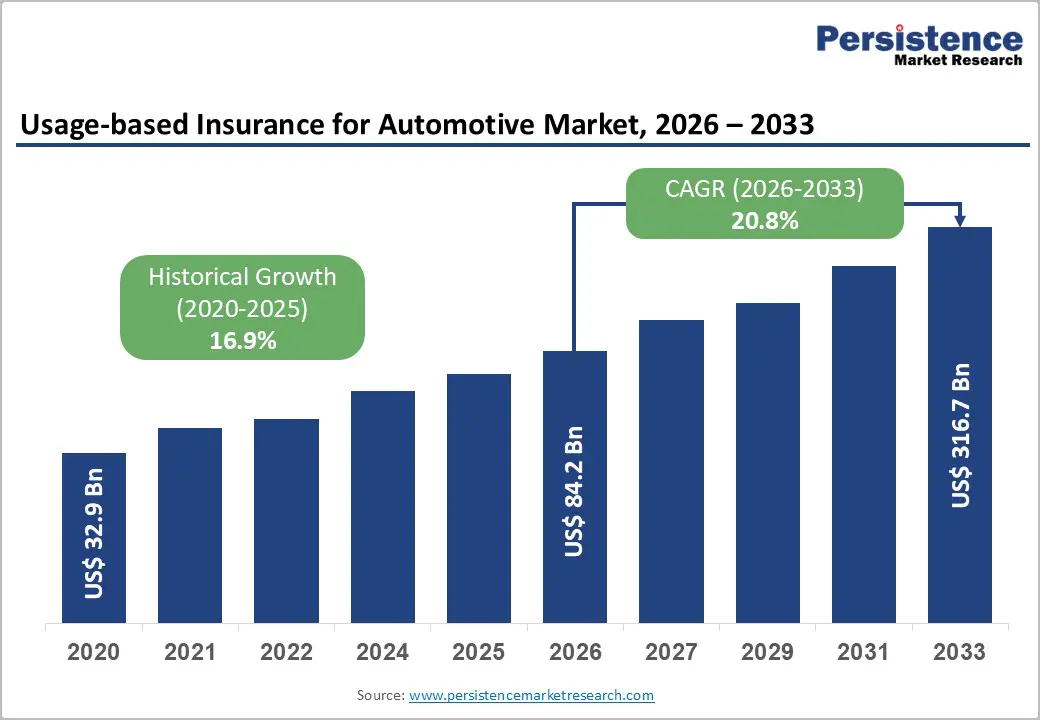

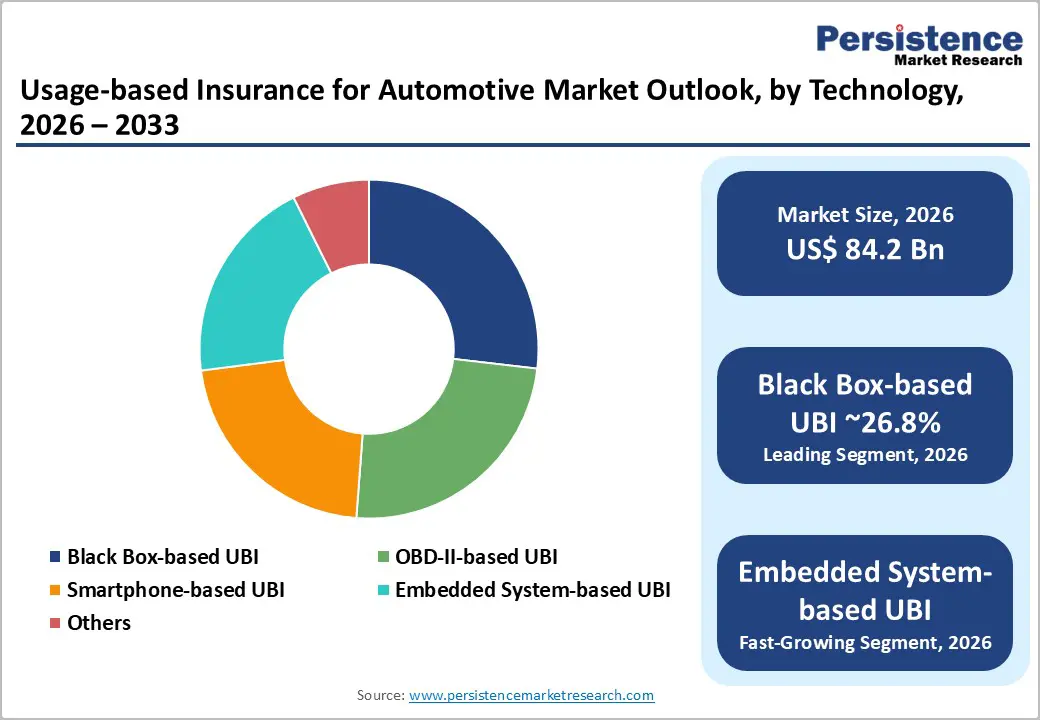

The global usage-based insurance for automotive market size is projected at US$ 84.2 billion in 2026 and is projected to reach US$ 316.7 billion by 2033, growing at a CAGR of 20.8% between 2026 and 2033.

Over 61% of newly registered U.S. vehicles in 2023 were OBD-telematics compatible; IoT-based OBD integration in connected European cars grew 48% between 2022 and 2023; India's OBD adoption rose 53% in 2023 under smart mobility mandates, confirming telematics-driven UBI as a structurally accelerating global insurance transformation.

Key Industry Highlights:

- Leading Policy Type: PAYD leads at 38.3% share; MHYD grows fastest at 23.2% CAGR, driven by AI-powered fleet driver coaching, behavioral risk analytics, and insurer-telematics platform MHYD product innovation globally.

- Leading Technology: Black Box leads at 26.8% share; Embedded System-based UBI grows fastest at 27% CAGR, driven by OEM factory-fitted telematics enabling seamless UBI enrollment at vehicle purchase globally through 2033.

- Leading Vehicle Type: Passenger Vehicles lead at 72.2% share; Commercial vehicles are poised to reach a leading CAGR, driven by fleet telematics penetration expansion and MHYD-enabled fleet risk management platform adoption globally.

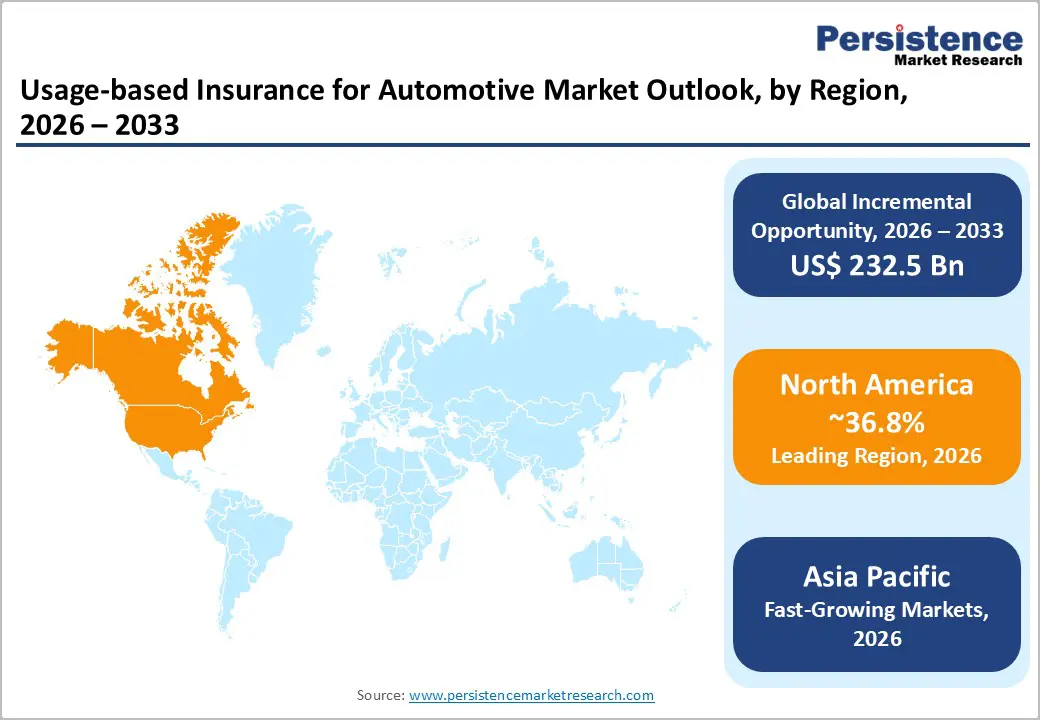

- Regional Leader: North America leads at 36.8% share; Asia Pacific is likely to witness fast-growth with China and India at leading positions, driven by EV telematics and IRDAI sandbox UBI pilots.

- Strategic Milestone: Kia-LexisNexis's 28-country OEM-native UBI integration (July 2025) and CMT's DriveWell Fusion 25-country expansion (September 2024) signal OEM-embedded telematics as the defining UBI market access and enrollment infrastructure investment theme through 2033.

Market Dynamics Analysis

Drivers - Connected Vehicle Ecosystem Proliferation and OEM-Embedded Telematics Mandates Accelerating UBI Adoption

The global connected vehicle installed base exceeded 400 million active vehicles in 2024 (GSMA Connected Car Report), with the European Union's eCall regulation mandating factory-fitted emergency telematics systems in all new passenger vehicles and light commercial vehicles since March 2018, creating a continuously expanding embedded telematics data infrastructure that enables insurer access to real-time vehicle usage and driving behavior data without aftermarket device installation.

ACEA data confirms IoT-based OBD device integration in European connected cars grew 48% between 2022 and 2023, while NHTSA reported 61% of newly registered U.S. vehicles in 2023 were OBD plug-and-play telematics compatible, establishing the hardware prerequisite for mass UBI enrollment at scale across North American and European markets.

Cambridge Mobile Telematics (CMT) expanded its DriveWell Fusion platform across 25+ countries in September 2024, combining smartphone, IoT, and dashcam data for multi-modal driving behavior scoring, demonstrating the scalability of cloud-native telematics platforms enabling insurers to deploy UBI programs in markets where embedded telematics penetration remains below critical mass. Kia's July 2025 partnership with LexisNexis Risk Solutions, integrating driving behavior analytics into its app across 28 countries, exemplifies OEM-insurer ecosystem convergence that progressively automates UBI enrollment within vehicle purchase workflows globally through 2033.

AI and Big Data Analytics Transforming UBI Underwriting Accuracy and Enabling Real-Time Premium Personalization

AI and machine learning-powered driving behavior analytics platforms, processing telematics data streams including hard braking frequency, acceleration profiles, cornering behavior, time-of-day driving patterns, and distracted driving detection, are enabling UBI underwriters to build predictive risk models 3.5x more accurate than demographic-based traditional actuarial models (LexisNexis Risk Solutions, 2024 U.S. Insurance Demand Meter), directly reducing loss ratios and improving portfolio profitability at scale.

Progressive's Snapshot UBI program, enrolling over 7 million active policies in 2024 with an average premium reduction of US$ 231 per qualifying safe driver annually, demonstrates the commercial proof-of-concept for AI-enabled behavior-based UBI pricing at mass market scale across U.S. personal auto insurance segments.

The global insurance telematics market, valued at US$ 6.8 Bn in 2024 at 18.9% CAGR (GMI), is the underlying technology infrastructure investment layer enabling UBI AI analytics platform scaling across insurer, OEM, and insurtech ecosystem participants globally. AI-driven UBI platforms that integrate predictive loss modeling, automated claims adjudication, real-time premium adjustment, and fraud detection, reducing insurer claims settlement costs by an estimated 12-18% per claims cycle, provide the margin improvement business case for sustained insurer UBI platform investment through 2033.

Restraints - Consumer Data Privacy Regulation Fragmentation Creating Cross-Border UBI Compliance Complexity

GDPR in Europe, CCPA in California, and India's Digital Personal Data Protection Act (DPDPA) 2023 impose distinct data minimization, consent management, and cross-border data transfer requirements on telematics data collection in UBI programs, with compliance frameworks varying across 50+ national and sub-national jurisdictions creating legal architecture complexity that delays multinational insurer UBI program launches by 12-24 months per new market entry.

Non-compliance penalties, up to €20 Mn or 4% of global annual turnover under GDPR, create material regulatory exposure for insurers deploying UBI programs using cross-border telematics cloud data processing architectures not aligned to local data residency requirements in each operating jurisdiction.

Telematics Device Interoperability and Aftermarket Installation Standardization Barriers

The global UBI technology ecosystem encompasses OBD-II dongles, black boxes, smartphone apps, and embedded OEM systems, each generating proprietary data formats incompatible across insurer and telematics vendor platforms without costly middleware integration layers.

Over 65% of the global vehicle parc consists of used vehicles without factory-fitted telematics, requiring aftermarket device installation programs where standardization gaps between Bluetooth OBD-II dongles, hardwired black boxes, and cellular-connected GPS trackers create data quality inconsistencies that reduce UBI risk model accuracy by an estimated 18-25% versus OEM-integrated embedded telematics data streams for used vehicle UBI policy underwriting programs globally.

Opportunities - Commercial Fleet UBI and MHYD-Enabled Fleet Risk Management Creating High-Value Procurement Programs

Commercial fleet operators, managing over 285 million commercial vehicles globally (IRF World Road Statistics, 2024), represent the highest-value UBI segment outside personal passenger insurance, with fleet telematics and driver behavior scoring programs demonstrating 15-25% fleet accident rate reductions and 12-18% fuel cost savings per fleet per annum through structured MHYD-based driver coaching platforms.

Each commercial fleet UBI contract generates significantly higher annual premium volume per policy than personal auto, with enterprise fleet operators sustaining multi-year, multi-vehicle UBI platform contracts generating recurring telematics analytics subscription revenue in addition to insurance premium income for integrated insurer-telematics ecosystem participants.

Emerging Market UBI Expansion Across India, Brazil, and ASEAN Mobile-First Consumer Ecosystems

India's Insurance Regulatory and Development Authority (IRDAI) Sandbox Framework enabling UBI telematics-based pilot programs, combined with Citroen India and ICICI Lombard's PAYD program for the eC3 EV, demonstrates regulatory openness to behavior-linked premium models across a 350+ million vehicle market where young, urban, smartphone-native consumers represent the primary UBI enrollment opportunity.

PwC India's 2024 insurance sector report confirms India's non-life insurance sector grew 15% YoY, with telematics-based motor insurance as the highest-growth sub-segment, establishing India as the highest-potential emerging UBI market globally through 2033.

Brazil and Indonesia, each with rapidly expanding smartphone penetration above 80% and mobile-first consumer financial service adoption patterns, represent addressable UBI expansion markets where smartphone-based UBI eliminates hardware installation barriers for first-time UBI policyholders at scale. Combined, India, Brazil, Mexico, Indonesia, and UAE represent an estimated US$ 28-35 Bn in incremental UBI addressable market by 2030, making mobile-first emerging market UBI program deployment the most consequential geographic expansion opportunity for global insurers and insurtech platforms through 2033.

Category-wise Analysis

Policy Type Insights

Pay-As-You-Drive (PAYD) leads the policy type segment with a 38.3% market share in 2026, estimated at approximately US$ 32.2 Bn, anchored by its accessible mileage-based premium model that delivers immediate, transparent cost savings for low-mileage urban and hybrid remote-work commuter populations who represent the fastest-growing UBI enrollment demographic globally. PAYD's simplicity, premium directly proportional to miles driven without requiring behavioral scoring data consent, reduces consumer enrollment friction compared to PHYD and MHYD models, sustaining its policy type volume leadership across mature North American and European UBI markets.

While MHYD is the fastest-growing segment driven by AI behavioral analytics, PAYD's low-complexity enrollment advantage across price-sensitive consumer segments maintains its leading share through 2033 without material near-term displacement risk.

Manage-How-You-Drive (MHYD) is the fast-growing policy type at 23.2% CAGR by 2033. MHYD's integration of real-time driver coaching, gamified safety rewards, fleet risk management dashboards, and continuous behavioral feedback loops, enabled by AI telematics platforms, drives insurer retention improvement and commercial fleet risk reduction simultaneously, creating the highest-value UBI product innovation frontier through 2033 globally.

Technology Insights

Black Box-based UBI leads the technology segment with a 26.8% market share in 2026, estimated at approximately US$ 22.6 Bn, anchored by its established prevalence across European personal auto UBI markets (particularly Italy, U.K., and Spain) where black box telematics devices provide tamper-resistant, always-on driving behavior recording with cellular data transmission that meets insurer evidentiary standards for premium adjustment and claims adjudication programs.

Black box systems' superior data completeness over smartphone-based alternatives, achieving 98%+ trip capture rates versus 72-85% for smartphone apps, sustains insurer preference for black box platforms in high-value, high-frequency driving markets despite higher per-device installation costs. Embedded System UBI is growing faster, but black box installed base dominance across European markets maintains its technology segment leadership through 2033.

Embedded System-based UBI is the fast-growing technology at 27% CAGR by 2033. OEM-factory-fitted embedded telematics, activated at vehicle purchase with seamless insurer API integration, eliminating aftermarket device installation, is becoming the standard UBI enrollment pathway for new vehicle buyers globally as connected vehicle penetration expands, driving Embedded System UBI's accelerating technology segment share gain through 2033.

Vehicle Age Insights

New Vehicles (Connected/OEM-integrated systems) lead the vehicle age segment with a 60.6% market share in 2026, estimated at approximately US$ 51.0 Bn, reflecting OEM-embedded telematics prevalence across premium and mid-range new vehicle segments enabling seamless UBI enrollment at the point of vehicle purchase without aftermarket device friction.

New vehicle UBI's data quality advantage, with factory-calibrated embedded sensors delivering continuous multi-parameter telematics streams, sustains insurer preference for new vehicle OEM-integrated UBI programs over used vehicle aftermarket telematics alternatives across all major global markets. New vehicle connected car penetration will expand further as all EU new vehicle registrations carry mandatory eCall telematics, sustaining New Vehicle UBI segment leadership without reversal risk.

Used Vehicles (Aftermarket telematics devices) are growing at 17% CAGR. Over 65% of the global vehicle parc comprises used vehicles, representing a structurally large addressable UBI enrollment pool as OBD-II plug-and-play dongles and low-cost aftermarket black box devices make telematics-based UBI enrollment financially accessible for used vehicle owners across emerging and developed markets globally.

Vehicle Type Insights

Passenger Vehicles lead the vehicle type segment with a 72.2% market share in 2026, estimated at approximately US$ 60.8 Bn, reflecting the global personal auto insurance market's structural scale, with over 1.4 billion passenger vehicles in global operation creating the world's largest UBI addressable enrollment base concentrated in North American and European personal auto insurance markets.

Passenger vehicle UBI's dominance reflects both policy volume scale and consumer-facing product innovation investment concentration across Progressive, Allstate, AXA, and Allianz UBI program portfolios. Commercial vehicle UBI is growing faster at fleet level, but passenger vehicle UBI's sheer enrollment base and insurer premium volume scale sustains its segment leadership through 2033 without material structural displacement risk.

Commercial Vehicles (Fleet-focused adoption) are the fastest-growing vehicle type at 23.1% CAGR through 2033. Fleet telematics penetration expanding from below 8% toward 25-30% by 2033, MHYD-enabled fleet driver coaching programs demonstrating 15-25% accident reduction, and logistics operators' structured multi-vehicle fleet UBI contract procurement are collectively driving commercial vehicle UBI adoption acceleration globally through 2033.

Regional Market Insights

North America Usage-based Insurance for Automotive Market Trends

North America leads with a 36.8% share of the global usage-based insurance for automotive market in 2026, estimated at approximately US$ 31.0 billion, anchored by Progressive Snapshot's 7 million active UBI policies, Allstate Drivewise's nationwide program, State Farm Drive Safe & Save, and NHTSA OBD telematics compatibility across 61% of newly registered U.S. vehicles driving the world's most mature and commercially scaled UBI market.

U.S. Usage-based Insurance for Automotive Market: Progressive UBI Leadership, NHTSA Telematics Compatibility, and Insurtech Ecosystem

The United States holds approximately US$ 26.9 Bn in 2026, anchored by Progressive, Allstate, State Farm, and Liberty Mutual collectively holding 54% of North American UBI market share. NHTSA OBD telematics mandate frameworks, LexisNexis Risk Solutions' U.S. Insurance Demand Meter confirming growing UBI consumer appetite, and CMT's DriveWell deployment across 25+ countries originating from U.S. insurer partnerships sustain North American UBI innovation leadership globally. Canada contributes through Intact Insurance and Desjardins Group UBI telematics-enabled programs across Ontario and Quebec.

North America's sustained leadership is driven by Progressive Snapshot AI analytics platform maturity, NHTSA telematics vehicle compatibility mandates, and LexisNexis-OEM behavioral data partnership ecosystem depth sustaining premium-tier UBI innovation and commercial scaling by 2033.

Europe Usage-based Insurance for Automotive Market Trends

Europe is likely to achieve a growth holding approximately 22.3% of global usage-based insurance for automotive market in 2026, estimated at approximately US$ 18.8 Bn, driven by EU eCall embedded telematics mandate, GDPR-structured data consent frameworks enabling trusted UBI enrollment, and Italian, Spanish, and U.K. UBI market pioneering programs creating Europe's established black box UBI commercial foundation.

Germany Usage-based Insurance for Automotive Market: Black Box Telematics Pioneer Markets and EU eCall Embedded UBI Scaling

Germany holds approximately US$ 5.3 Bn in 2026, with Allianz, AXA Germany, and HUK-COBURG telematics-based UBI programs expanding through OEM partnerships with BMW ConnectedDrive and Mercedes-Benz mbOS vehicle data platforms. The U.K. sustains Insurethebox and Admiral LittleBox black box UBI market maturity.

Italy pioneered Europe's black box UBI model with UNIPOLSAI and Generali, achieving 20%+ Italian market penetration. Spain expands through MAPFRE GPS-enabled PAYD programs. EU eCall generating pan-European embedded telematics data foundations from all new vehicle registrations accelerates UBI scaling.

Europe's EU eCall embedded telematics infrastructure, GDPR-compliant UBI consent frameworks, and Germany-Italy-U.K. black box UBI commercial maturity create the regulatory and technology foundation for UBI scaling to pan-European mass market enrollment volumes.

Asia Pacific Usage-based Insurance for Automotive Market Trends

Asia Pacific is the fastest-growing region at 25.6% CAGR through 2033, commanding approximately 28.4% of global UBI Automotive Market share in 2025, driven by China's world-leading EV and connected vehicle ecosystem, India's IRDAI sandbox-enabled UBI pilots, and ASEAN smartphone-first consumer adoption enabling mobile-based UBI enrollment without aftermarket hardware barriers.

China Usage-based Insurance for Automotive Market: EV Telematics, IRDAI Sandbox, and Mobile-First UBI Adoption

China holds US$ 7.3 Bn in 2026, driven by world-leading EV sales exceeding 10 million units in 2024, PICC and Ping An Insurance OBD and embedded telematics UBI programs, and DiDi fleet mobility MHYD data partnerships expanding commercial vehicle UBI. India at US$ 3.0 Bn is accelerating through IRDAI sandbox UBI pilots, ICICI Lombard-Citroen PAYD program, and OBD adoption growing 53% YoY. Japan sustains Aioi Nissay Dowa's Toyota-integrated G-Link telematics UBI leadership. ASEAN markets expand through Grab fleet telematics and smartphone UBI programs.

Asia Pacific's China EV telematics UBI ecosystem leadership, India IRDAI sandbox UBI regulatory enablement, and ASEAN mobile-first consumer UBI enrollment scale position the region as the dominant long-term UBI volume and revenue growth engine globally through 2033.

Competitive Landscape

The global UBI Automotive Market is moderately consolidated at the insurer tier, with Progressive, Allstate, AXA, Liberty Mutual, and UNIPOLSAI collectively holding approximately 54% of global UBI revenue share, while the telematics technology layer remains fragmented across CMT, LexisNexis, Octo, and 100+ regional insurtech platforms. Proprietary telematics data analytics IP, OEM ecosystem integration depth, and behavioral risk model accuracy are the primary competitive differentiation levers.

AI-powered driver behavior analytics deepening, embedded OEM telematics partnership expansion, commercial fleet MHYD platform scaling, and mobile-first emerging market UBI program deployment define the dominant competitive strategic investment themes across all major UBI market participants globally through 2033.

Strategic Developments

- In July 2025, Kia Motors partnered with LexisNexis Risk Solutions, integrating real-time driving behavior analytics into the Kia Connect app across 28 countries, enabling OEM-native UBI enrollment at vehicle purchase for Kia owners globally, supporting Europe's accelerating shift toward embedded telematics-based personalized insurance premiums.

- In 2024, AXA entered a strategic UBI telematics data partnership with Stellantis, integrating AXA's behavioral driving analytics directly with Stellantis STLA Brain vehicle operating system, enabling factory-activated UBI policy enrollment for Peugeot, Citroën, Jeep, and Vauxhall owners across European markets without aftermarket OBD device installation requirements.

- In August 2023, ICICI Lombard General Insurance partnered with Citroën India to launch a Usage-Based Insurance (UBI) program for ë-C3 customers, enabling personalized premiums based on vehicle usage and driving behavior through real-time telematics data and driver scoring, with enrollment available at purchase or via the MyCitroën app—positioning it as one of India’s first OEM-linked UBI initiatives promoting safe driving and dynamic insurance pricing.

Usage-based Insurance for Automotive Market Reprot Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 32.9 Bn |

| Current Market Value (2026) | US$ 84.2 Bn |

| Projected Market Value (2033) | US$ 316.7 Bn |

| CAGR (2026 - 2033) | 20.8% |

| Leading Region | North America |

| Dominant Vehicle Type | Passenger Vehicles - 72.2% |

| Top-ranking Policy Type | Pay-As-You-Drive / PAYD - 38.3% |

| Incremental Opportunity | US$ 232.5 Bn |

Companies Covered in Usage-based Insurance for Automotive Market

- Progressive Corporation

- Allstate Insurance Company

- State Farm Mutual Automobile Insurance

- Liberty Mutual Insurance

- AXA S.A.

- Allianz SE

- Assicurazioni Generali S.p.A.

- UNIPOLSAI Assicurazioni S.p.A.

- Aviva PLC

- MAPFRE S.A.

- Aioi Nissay Dowa Insurance Co., Ltd.

- Root Insurance Company

- Metromile Inc.

- Cambridge Mobile Telematics

- Octo Telematics

Frequently Asked Questions

The usage-based insurance for automotive market is valued at US$ 84.2 Bn in 2026, projected to reach US$ 316.7 Bn by 2033, delivering an incremental opportunity of US$ 232.5 Bn through 2033.

The usage-based insurance for automotive market is valued at US$ 84.2 Bn in 2026, projected to reach US$ 316.7 Bn by 2033, delivering an incremental opportunity of US$ 232.5 Bn through 2033.

Connected vehicle proliferation with 61% OBD telematics compatibility in new U.S. vehicles, AI behavioral risk analytics enabling 15-30% premium savings, and EU eCall-mandated embedded telematics generating pan-European UBI enrollment infrastructure are the primary growth drivers.

The usage-based insurance for automotive market grows at a CAGR of 20.8% from 2026 to 2033, building on a historical CAGR of 16.9% from 2020 to 2026.

Commercial fleet MHYD risk management platform contracts delivering 15-25% accident reduction and India, Brazil, and ASEAN mobile-first UBI expansion targeting US$ 28-35 Bn incremental market by 2030 are the most strategically significant growth opportunity pools.

Progressive, Allstate, State Farm, Liberty Mutual, AXA, Allianz, Generali, UNIPOLSAI, Aviva, MAPFRE, Aioi Nissay Dowa, Root Insurance, Metromile (Lemonade), Cambridge Mobile Telematics, and Octo Telematics are the leading global market participants.