- Specialty & Fine Chemicals

- Solvent Recovery Systems Market

Solvent Recovery Systems Market Size, Share, and Growth Forecast 2026 - 2033

Solvent Recovery Systems Market by Technology (Distillation System, Membrane System, Adsorption System, Other), Solvent Type (Non-Azeotropic, Aqueous Azeotropic, Heterogeneous Azeotropic, Aqueous Homogeneous Azeotropic), Operating Mode (Batch, Continuous), Installation Type (On-site, Off-site), Industry, and Regional Analysis for 2026 - 2033

Solvent Recovery Systems Market Size and Trend Analysis

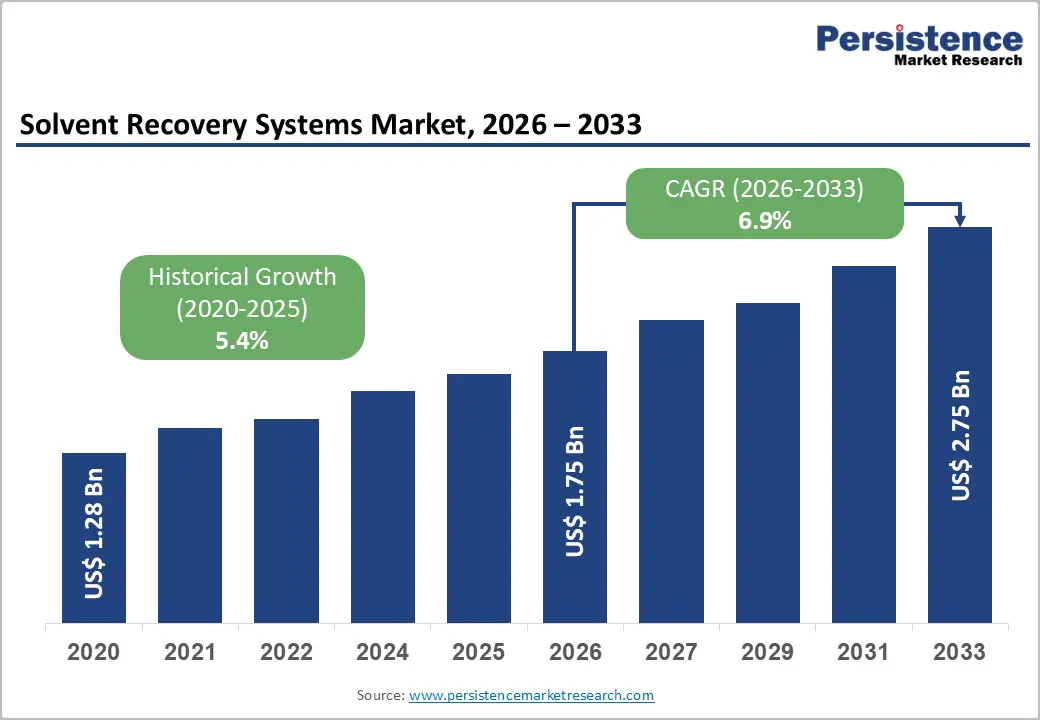

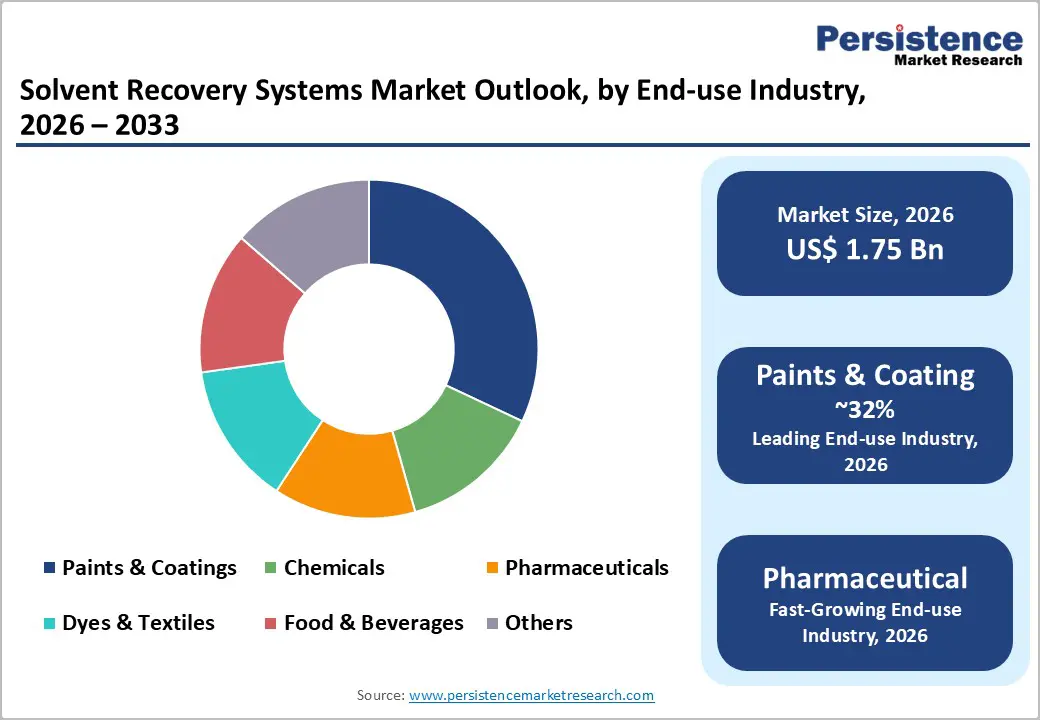

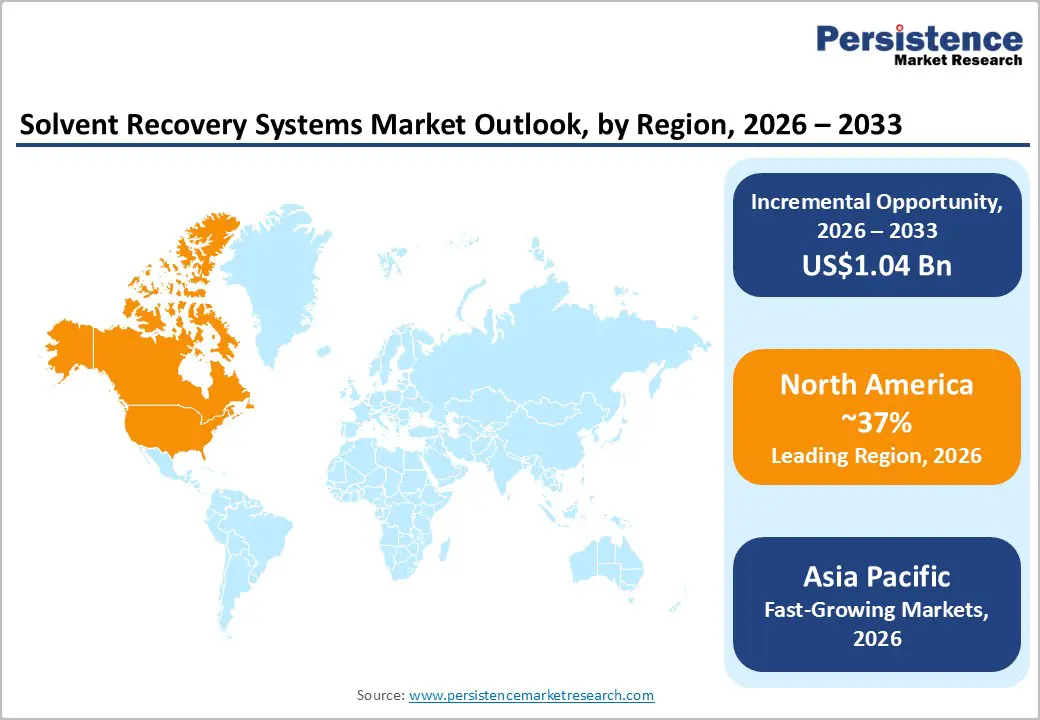

The global solvent recovery systems market size is supposed to be valued at US$ 1.75 Bn in 2026 and is projected to reach US$ 2.75 Bn by 2033, growing at a CAGR of 6.9% between 2026 and 2033.

This growth trajectory is driven by a rise in environmental regulations worldwide that mandate the reduction of volatile organic compound (VOC) emissions and the increasing cost burden of virgin solvent procurement, coupled with hazardous waste disposal expenses. Industries are recognizing that implementing advanced solvent recovery systems can achieve up to 95% solvent reclamation rates while simultaneously reducing carbon footprint by significant margins, with facilities like Veolia's Liverpool plant demonstrating annual savings of 172,000 tonnes CO2e compared to virgin solvent usage.

Key Market Highlights

- Leading Region: North America dominates the solvent recovery systems market, with 37% market share, driven by stringent EPA Clean Air Act enforcement, sophisticated pharmaceutical manufacturing infrastructure, and innovation leadership.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing market, fueled by manufacturing expansion in China, India, and regulatory VOC controls.

- Leading Segment: Distillation technology commands approximately 48% market share as the leading technology segment due to its broad applicability across diverse solvent types and proven efficiency in complex separations.

- Fastest Growing Industry: Pharmaceutical Industry represents the fastest-growing application segment driven by expanding API manufacturing in Asia Pacific, stringent GMP requirements, and documented economic benefits, including $2.2 million annual savings with 94.1% recovery efficiency and 99.9% product purity.

- Key Market Opportunity: Circular economy mandates and ESG reporting requirements create substantial opportunities as European Union eco-design standards and corporate sustainability frameworks compel industries to implement quantifiable solvent recovery programs.

| Key Insights | Details |

|---|---|

| Solvent Recovery Systems Market Size (2026E) | US$ 1.75 Bn |

| Market Value Forecast (2033F) | US$ 2.75 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth (2020 - 2025) | 5.4% |

Market Dynamics

Drivers - Stringent Environmental Regulations Driving Adoption of VOC Control Technologies

Governments worldwide are implementing increasingly stringent regulations on VOC emissions, creating significant compliance pressures on solvent-intensive industries. In the U.S., the Environmental Protection Agency's Clean Air Act enforces Maximum Achievable Control Technology (MACT) standards with substantial penalties, including fines or facility shutdowns for non-compliance. The European Union's Industrial Emissions Directive (IED) mandates companies to implement Best Available Techniques (BAT) to minimize emissions, with particularly strict requirements for VOC-intensive sectors such as coatings and chemical manufacturing.

The Asian Development Bank reported in 2024 that industrial solvent consumption in Asia Pacific grew by 35% from 2020 to 2023, prompting regional regulatory bodies like China's National Medical Products Administration (NMPA) and India's Central Drugs Standard Control Organization (CDSCO) to establish stricter emission standards and pharmaceutical compliance frameworks. These regulatory pressures are compelling industries to invest in solvent recovery infrastructure as a cost-effective compliance strategy rather than facing escalating penalties.

Economic Benefits and Rapid Return on Investment

The economic viability of solvent recovery systems has become increasingly attractive, with payback periods often falling below two years. Koch Modular Process Systems documented a pharmaceutical industry case where a $3.8 million solvent recovery system installation generated annual savings of $2.2 million from recovered solvent, achieving greater than 99.9 wt% product purity and 94.1% recovery efficiency of tetrahydrofuran (THF). The system's operating costs of $200,000 per year for utilities and manpower were substantially offset by eliminating virgin solvent procurement and hazardous waste disposal expenses.

Industries in Asia Pacific reported recovering 12 million liters of solvents annually in 2023, reducing waste disposal costs by 20%. The paints and coatings market, which extensively utilizes solvents in production processes, is witnessing significant cost reductions through the implementation of fractional distillation and adsorption-based recovery technologies that convert waste streams into reusable resources.

Restraints - High Initial Capital Investment Requirements

The substantial upfront capital expenditure required for installing sophisticated solvent recovery systems presents a significant barrier, particularly for small and medium-sized enterprises. Complete modular solvent recovery systems with distillation columns, storage tanks, and tanker loading bays require multi-million dollar investments, as evidenced by Veolia's expansion project that installed 17 new storage tanks and multiple distillation columns to increase capacity to 86,000 tonnes annually.

While payback periods can be favorable for high-volume operations, smaller facilities generating inconsistent solvent waste volumes struggle to justify the capital allocation, especially when competing against other operational priorities and facing uncertain future solvent prices that could impact ROI calculations.

Technical Complexity in Handling Diverse Solvent Mixtures

The heterogeneity of industrial solvent waste streams creates significant technical challenges in achieving effective separation and purification. Azeotropic mixtures, where conventional distillation becomes inefficient, require specialized entrainers and advanced separation techniques. The textile and dyes industry generates particularly complex effluents containing multiple organic solvents alongside dyes, surfactants, and other chemical additives, with VOC concentrations varying from 10 mg/m³ to 350 mg/m³ depending on the specific process.

High-viscosity waste streams from paint manufacturing pose additional complications requiring specialized heating systems like induction heating coils for effective solvent vaporization. These technical complexities necessitate customized engineering solutions and extensive testing, which in turn increase both implementation costs and the requirements for operational expertise.

Opportunity - Expanding Pharmaceutical Manufacturing in the Asia Pacific

The pharmaceutical solvents market is experiencing robust growth, particularly in the Asia Pacific, where pharmaceutical manufacturing is expanding rapidly, driven by increasing generic drug production and the development of active pharmaceutical ingredient (API) synthesis capabilities. China and India account for 50% of the region's solvent waste generation, with solvent recovery system adoption increasing by 25% and recovering 8 million liters annually. The pharmaceutical industry's strict quality requirements under Good Manufacturing Practice (GMP) regulations create substantial opportunities for advanced recovery systems that can achieve virgin-quality solvent purification or better.

Technologies incorporating closed-loop systems are gaining traction in high-volume pharmaceutical facilities across China and India, where they capture and purify used solvents from reactor vent streams, centrifuge and dryer exhausts, storage tank venting, and laboratory fume hoods. Companies can capitalize on the Recover for Sale (R4S) model, where recovered solvents achieving appropriate purity levels become tradable commodities for non-pharmaceutical applications, transforming waste liabilities into revenue-generating assets while avoiding greenhouse gas emissions from incineration.

Circular Economy Initiatives and Sustainable Manufacturing Mandates

The accelerating transition toward circular economy principles in Europe and globally presents substantial growth opportunities for solvent recovery technology providers. The European Union's eco-design standards and "right to repair" legislation are creating systematic change in how industries approach resource utilization, with emphasis on regenerative models that create multiple cycles of value from finite materials. Chemical industry leaders like Itelyum in Italy have demonstrated successful business models, achieving high levels of circularity in industrial oils and developing advanced solvent recovery technologies as part of integrated chemical recycling strategies.

The membrane technology market is experiencing innovation in semi-permeable barriers that enable selective solvent filtration with reduced energy consumption compared to conventional distillation, making recovery economically viable for previously challenging applications. Environmental, Social, and Governance (ESG) reporting requirements under frameworks including GRI, CDP, and SASB are compelling corporations to implement measurable sustainability initiatives, with solvent recovery providing quantifiable metrics, including hazardous waste reduction, and circular economy contributions.

Category-wise Analysis

Technology Insights

Distillation systems command approximately 48% market share as the dominant technology in solvent recovery applications due to their broad applicability and proven efficiency in separating mixtures based on differential boiling points. Distillation technology has evolved significantly, with Veolia implementing advanced multi-stage distillation columns at its Liverpool facility to separate residues from waste streams and further fractionate solvent mixtures into products meeting industrial customer specifications.

The technology's superiority stems from its capability to handle both simple and complex separations, including azeotropic distillation using entrainers for challenging mixtures, as demonstrated by Koch Modular Process Systems' continuous-mode operations that dry isopropyl alcohol (IPA) using isopropyl ether as the entrainer. Praj Industries' patented Rh-Grid trays exemplify technological advancement, enabling strippers to deliver maximum efficiency even at higher concentrations. Distillation's versatility across diverse solvent types, from low-boiling alcohols to high-boiling glycol ethers, and its scalability from laboratory to industrial-scale operations solidify its market leadership despite higher energy consumption compared to membrane alternatives.

Solvent Type Insights

Non-azeotropic solvents represent approximately 41% market share as the leading segment, driven by their straightforward separation characteristics that enable efficient recovery using conventional distillation without requiring specialized techniques or entrainer chemicals. Non-azeotropic systems benefit from predictable vapor-liquid equilibrium behavior where components can be separated based solely on boiling point differences, resulting in lower operational complexity and reduced processing costs. Industries processing single-solvent waste streams or binary mixtures with sufficient boiling point separation, common in pharmaceutical API manufacturing and paint formulation, preferentially generate non-azeotropic waste amenable to cost-effective recovery.

The pharmaceutical industry's extensive use of methanol, ethanol, acetone, and tetrahydrofuran (THF) in crystallization and purification operations creates substantial volumes of non-azeotropic waste streams suitable for high-purity recovery, with documented cases achieving greater than 99.9% purity in recovered products. Market dynamics favor non-azeotropic recovery as it requires less sophisticated equipment, consumes lower energy per unit recovered, and achieves faster payback periods compared to azeotropic mixture processing.

Operating Mode Insights

Continuous operating mode systems hold approximately 54% market share, reflecting industrial preferences for sustained high-volume processing capabilities that maximize throughput and operational efficiency. Continuous systems are particularly advantageous for large-scale chemical manufacturing and pharmaceutical production facilities, generating consistent solvent waste streams requiring uninterrupted processing to avoid the accumulation of hazardous materials. Koch Modular Process Systems designs modular recovery units that operate continuously after initial batch-mode startup sequences, transitioning seamlessly to steady-state continuous processing for maximum productivity.

The continuous mode's dominance is reinforced by its superior economics at scale, where fixed costs are amortized across larger processing volumes, and automated control systems maintain optimal separation conditions without manual intervention. Veolia's expanded Liverpool facility exemplifies continuous operation advantages, processing 86,000 tonnes annually through integrated distillation columns fed by high-throughput tanker loading bays that manage logistics for continuous waste offloading and product delivery.

Installation Type Insights

On-site installation accounts for approximately 67% market share, driven by compelling economic advantages including elimination of transportation costs, immediate solvent availability for production operations, and enhanced control over material quality and intellectual property. On-site systems enable pharmaceutical manufacturers to implement closed-loop solvent management where recovered materials are immediately reintroduced into manufacturing processes without supply chain delays, particularly critical for high-value specialty solvents subject to price volatility.

Koch Modular's outdoor-situated modules with 12-foot by 12 feet footprints facilitate on-site installation through off-site manufacturing and expedited deployment timelines compared to traditional stick-built projects, reducing implementation complexity at facility locations. The on-site model supports Scope 1 emissions reductions by avoiding transportation-related carbon footprint from off-site recovery services and enables real-time quality control, ensuring recovered solvents meet stringent production specifications.

Industry Insights

The paints and coatings industry represents approximately 32% market share as the dominant industry segment, generating massive solvent waste volumes from formulation, application, and cleaning operations that create compelling economics for recovery system investments. The paints and coatings market extensively utilizes aromatic and aliphatic hydrocarbons, esters, ketones, and alcohols as carriers and thinners, with waste streams including spent paint thinners and solvent-based paint suitable for regeneration into recycled products, replacing virgin materials.

The segment's leadership is reinforced by regulatory pressures, with the EPA's MACT standards imposing strict VOC emission limits on coating operations and the EU's Industrial Emissions Directive requiring BAT implementation. Recovery systems in coating applications achieve dual benefits of regulatory compliance and substantial cost savings, as documented recovery rates reach 95% with product quality meeting original specifications for paint formulation.

Regional Insights

North America Solvent Recovery Systems Trends

The U.S. maintains market leadership in North America, driven by stringent EPA Clean Air Act enforcement and sophisticated pharmaceutical manufacturing infrastructure requiring high-purity solvent recovery capabilities. The pharmaceutical sector's concentration in New Jersey, Massachusetts, and North Carolina creates regional clusters of solvent recovery demand, with facilities implementing systems achieving tetrahydrofuran (THF) recovery at 94.1% efficiency and greater than 99.9% purity.

The regulatory framework continues evolving with Maximum Achievable Control Technology (MACT) standards becoming progressively stricter, compelling industries to upgrade legacy systems or implement new recovery infrastructure to avoid penalties, including facility shutdowns. The innovation ecosystem benefits from collaboration between equipment manufacturers, engineering firms, and end-users to develop customized solutions for challenging applications, including viscous waste streams and complex azeotropic mixtures requiring specialized entrainers.

Europe Solvent Recovery Systems Trends

Europe demonstrates leadership in circular economy implementation with the Industrial Emissions Directive (IED) establishing comprehensive Best Available Techniques (BAT) requirements that mandate solvent recovery for VOC-intensive sectors. Germany, the U.K., France, and Spain are spearheading regulatory harmonization efforts that create consistent standards across the European Union, facilitating cross-border technology deployment and economies of scale for equipment manufacturers. Veolia's expansion of its Garston, Liverpool facility in August 2024 to 86,000 tonnes annual capacity exemplifies Europe's commitment to sustainable industrial operations, with the installation saving an estimated 172,000 tonnes CO2e annually compared to virgin solvent production.

The region's GreenUp strategy and eco-design standards promote regenerative resource usage models, with companies like Itelyum in Italy achieving advanced circularity in industrial oils and solvents as part of integrated chemical recycling initiatives. The chemical industry in Europe is actively investing in closed-loop systems and resource recovery technologies, supported by the European Chemicals Agency (ECHA) guidelines and national-level sustainability mandates that position solvent recovery as essential infrastructure for maintaining industrial competitiveness while meeting climate commitments.

Asia Pacific Solvent Recovery Systems Trends

Asia Pacific represents the fastest-growing regional market, with solvent recovery system adoption increasing by 25% as industrial solvent consumption grew 35% from 2020 to 2023, according to the Asian Development Bank. China and India collectively account for 50% of regional solvent waste generation, driven by the rapid expansion of chemical processing, pharmaceutical manufacturing, and textile production. China's National Medical Products Administration (NMPA) and India's CDSCO have implemented stricter emission standards and pharmaceutical compliance frameworks, accelerating technology adoption among manufacturers seeking to maintain export market access.

Manufacturing advantages, including relatively lower installation costs and availability of technical workforce, support the rapid deployment of solvent recovery infrastructure across the region. The presence of leading global manufacturers offering customized solutions tailored to specific industrial needs, including high-viscosity waste from paint and coating operations, complex pharmaceutical solvent mixtures, and textile industry effluents, has accelerated market penetration.

Competitive Landscape

The solvent recovery systems market exhibits moderate consolidation with established players like Veolia, Sulzer, and Koch Modular Process Systems commanding significant market presence through integrated service offerings and technological expertise. Competition centers on key differentiators, including recovery efficiency rates, product purity guarantees, modular system designs enabling faster deployment, and comprehensive service packages encompassing engineering studies, installation, and long-term maintenance. Emerging business models include equipment leasing, tolling arrangements where manufacturers provide recovery services, and Recover for Sale (R4S) programs transforming waste into tradable commodities.

Key Market Developments

- August 2024: Veolia expanded its solvent recovery facility at Garston, Liverpool to 86,000 tonnes annual capacity through the installation of new distillation columns and 17 storage tanks, enabling the processing of waste paint thinners and solvent-based paints for industries including pharmaceuticals, semiconductors, and agrochemicals.

- December 2024: Koch Modular Process Systems highlighted successful solvent recovery implementation, achieving $2.2 million annual savings with 94.1% THF recovery efficiency and 99.9% product purity, demonstrating less than two-year payback periods for pharmaceutical manufacturers.

- May 2024: Donaldson Company, Inc., and PolyPeptide Group AG, announced their collaboration on the development of a production-scale solvent recovery system for use in peptide purification.

Top Companies in Solvent Recovery Systems Market

- Veolia (France) is a global leader in environmental services with extensive solvent recovery capabilities demonstrated through its Liverpool facility expansion to 86,000 tonnes annual capacity, saving 172,000 tonnes CO2e annually. The company's integrated approach combines waste collection, processing through multiple distillation technologies, and production of recycled solvents meeting virgin material specifications for industries including pharmaceuticals and agrochemicals.

- Koch Modular Process Systems (U.S.) specializes in engineered-to-order modular process systems with proven track records in pharmaceutical solvent recovery, delivering installations with documented payback periods under two years. The company provides comprehensive engineering studies, process performance guarantees, and modular units with 12 feet by 12-foot footprints, enabling expedited outdoor installation timelines.

- Praj Industries (India) offers solvent recovery systems featuring patented Rh-Grid tray technology optimized for maximum stripper efficiency across diverse operating conditions. The company's regional expertise in Asia positions it strategically to serve the rapidly expanding pharmaceutical and chemical manufacturing sectors in India and neighboring markets requiring cost-effective recovery solutions.

Companies Covered in Solvent Recovery Systems Market

- Veolia

- Sulzer

- Spooner AMCEC

- HongYi Environmental Equipment

- Praj Industries

- CBG Technologies

- Koch Modular Process Systems

- EPIC Modular Process Systems

- KIMURA Chemical Plants

- CycleSolv

- Clean Planet Chemical

- Maratek Environmental

Frequently Asked Questions

The global solvent recovery systems market is valued at US$ 1.75 Bn in 2026 and is projected to reach US$ 2.75 Bn by 2033, growing at a CAGR of 6.9% during the forecast period.

Stringent environmental regulations, including EPA's Clean Air Act and EU's Industrial Emissions Directive, mandate VOC emission reductions, while economic benefits, including $2.2 million annual savings, 95% recovery rates, and payback periods under two years, drive adoption across industries.

Distillation systems command approximately 48% market share as the dominant technology due to broad applicability across diverse solvent types and proven efficiency in complex separations.

North America leads the market, with 37% market share, driven by stringent EPA enforcement, sophisticated pharmaceutical manufacturing infrastructure requiring high-purity recovery capabilities, achieving 99.9% product purity.

Circular economy mandates and ESG reporting requirements under GRI, CDP, and SASB frameworks create substantial opportunities as European Union eco-design standards compel quantifiable sustainability initiatives, with solvent recovery delivering 172,000 tonnes CO2e annual savings and enabling Recover for Sale business models transforming waste into revenue-generating assets.

Leading market participants include Veolia, Koch Modular Process Systems, Praj Industries, Sulzer, Spooner AMCEC, CBG Technologies, EPIC Modular Process Systems, and KIMURA Chemical Plants, competing through technological innovation, capacity expansion, and comprehensive service offerings including engineering studies and process performance guarantees.