- Bulk Chemicals

- Isoparaffin Solvents Market

Isoparaffin Solvents Market Size, Share, and Growth Forecast, 2025 - 2032

Isoparaffin Solvents Market By Product Type (C8–C9 Isoparaffins, C10–C12 Isoparaffins, Others), Application (Paints & Coatings, Metalworking Fluids, Others), End-user Industry, and Regional Analysis for 2025 - 2032

Isoparaffin Solvents Market Size and Trends Analysis

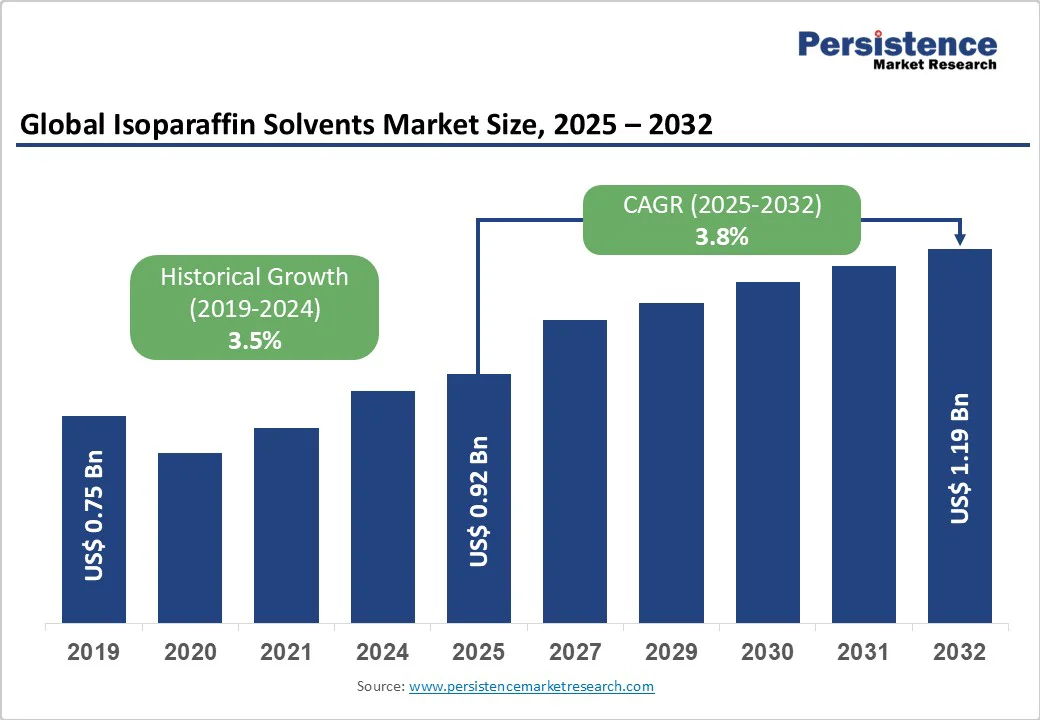

The global isoparaffin solvents market size was valued at US$0.92 Billion in 2025 and is projected to reach US$1.19 Billion by 2032, growing at a CAGR of 3.6% between 2025 and 2032, driven by rising demand from paints and coatings, industrial cleaning applications, and emerging usage in personal care and agrochemical formulations. The shift to low-odor, low-VOC solvents driven by environmental standards is boosting market growth, while feedstock volatility and regulatory pressures impact margins and production costs.

Key Industry Highlight

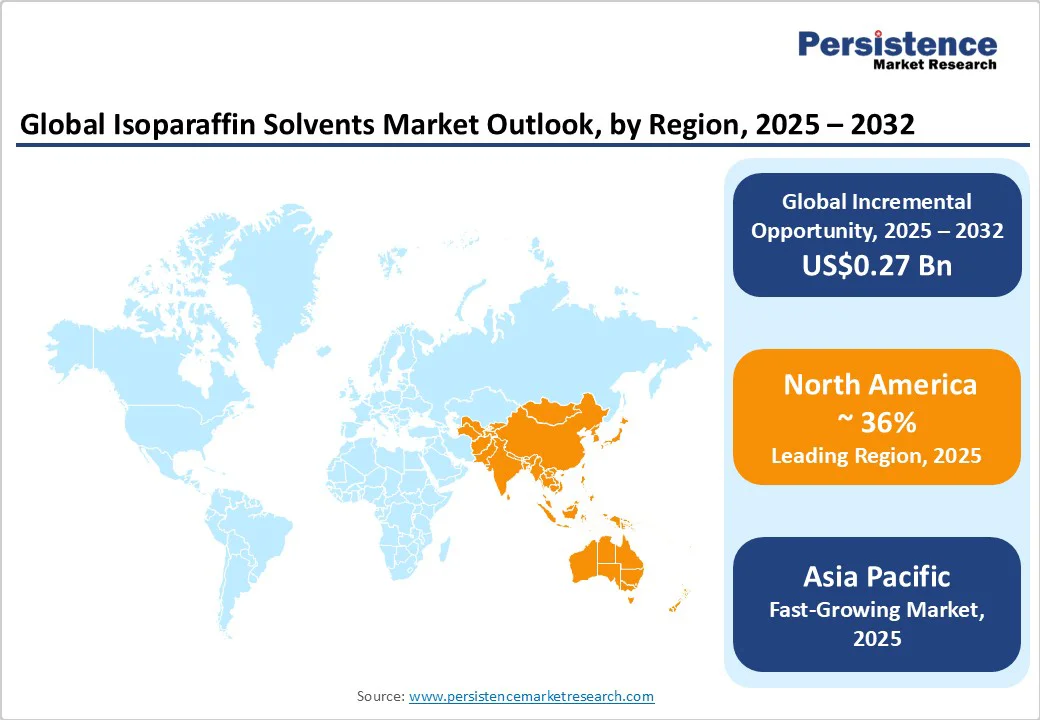

- Leading Region: North America, commanding approximately 36% of the global market revenue in 2025, supported by robust industrial, automotive, and coatings sectors.

- Fastest-growing Region: Asia Pacific, driven by industrialization and rising demand from personal care and coatings applications.

- Investment Plans: Major producers such as ExxonMobil, Shell, and Idemitsu Kosan are investing in low-VOC solvent technology and capacity expansion projects across the U.S., China, and South Korea to strengthen regional self-sufficiency.

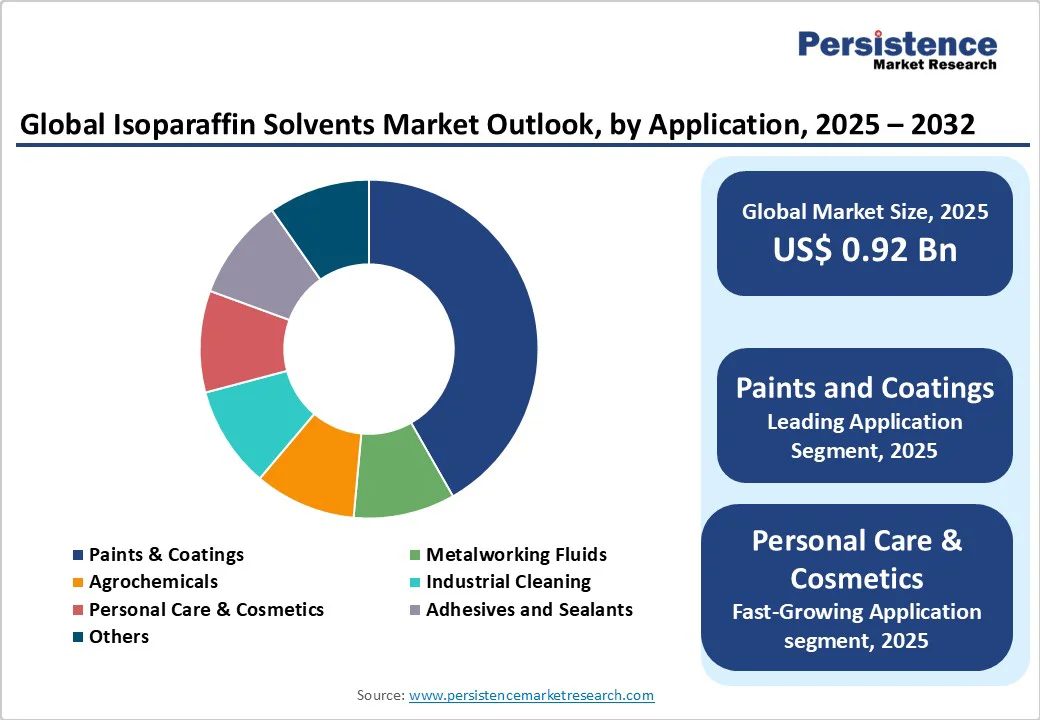

- Dominant Product Type: C10–C14 chain isoparaffins account for nearly 44.8% of the total market share, favored for their balanced solvency and widespread use in coatings and cleaning applications.

- Leading Application: The paints and coatings segment represents about 43% of global consumption, driven by infrastructure growth and industrial maintenance demand worldwide.

| Key Insights | Details |

|---|---|

|

Isoparaffin Solvents Market Size (2025E) |

US$0.92 Bn |

|

Market Value Forecast (2032F) |

US$1.19 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expanding Demand in Paints and Coatings Applications

Isoparaffin solvents are extensively used as diluents and carriers in coatings formulations due to their low odor, high purity, and fast evaporation characteristics. They enhance flow properties and improve finish quality, making them essential in automotive, industrial, and architectural coatings. Global construction and automotive production growth are directly boosting consumption. According to industry data, the coatings segment accounts for around 40% of total isoparaffin consumption, creating a stable base for long-term market demand. Regulatory initiatives aimed at reducing VOC emissions are further supporting the substitution of traditional aromatic solvents with isoparaffins.

Rising Utilization in Personal Care and Agrochemicals

The personal care and cosmetics industry is witnessing increased adoption of isoparaffin solvents as emollients and carriers owing to their excellent sensory profile, low irritation potential, and safety compliance. Similarly, in agrochemical formulations, isoparaffins serve as effective diluents and dispersants, improving product spreadability. The Asia Pacific region, particularly China, India, and ASEAN countries, has become a key consumption hub due to growing manufacturing capacities and rising disposable incomes. This expanding application base is creating multi-sectoral growth opportunities for both integrated producers and specialty formulators.

Innovation in Low-Carbon and High-Purity Solvent Grades

Producers are increasingly focusing on developing low-VOC, high-purity isoparaffin solvents aligned with global environmental standards. Refiners such as ExxonMobil and Shell have introduced low-odor and high-flash-point products targeting premium formulations for coatings, cosmetics, and cleaning agents. This technological shift supports both product differentiation and higher profit margins. The emergence of low-carbon solvent grades that reduce Scope 3 emissions is also gaining attention, aligning with sustainability goals set by multinational end users.

Barrier Analysis - Feedstock Price Volatility

Isoparaffin solvents are derived from paraffinic hydrocarbons sourced from crude oil and natural gas liquids. Volatility in crude oil prices directly impacts production costs, thereby affecting profit margins for manufacturers. During periods of high crude prices, refiners often divert feedstocks to more profitable streams, tightening solvent supply and pushing up prices. This volatility not only pressures downstream users but can also encourage temporary switching to oxygenated or bio-based alternatives.

Environmental and Regulatory Compliance Pressures

Despite being relatively cleaner than aromatic hydrocarbons, isoparaffin solvents are subject to VOC emission limits and REACH-style registration requirements in several markets. The cost and complexity of compliance, coupled with the increasing availability of greener alternatives, create barriers for small and mid-sized producers. The European Union and U.S. states with stringent environmental standards require expensive testing and documentation, increasing operational burdens and affecting new market entries.

Opportunity Analysis - Specialty Grades for Personal Care and Pharmaceutical Formulations

The demand for ultra-high-purity isoparaffin solvents in cosmetics, skincare, and pharmaceutical excipients is rising rapidly. These specialty grades are characterized by low odor, minimal aromatic content, and consistent quality, making them ideal for sensitive formulations. They command 10–25% higher average selling prices than standard grades and provide an opportunity for producers to enter high-margin niche markets. Global cosmetics and healthcare sector expansion, especially in Asia and Europe, offers a long-term growth avenue.

Expanding Industrial Base in Asia Pacific

Asia Pacific represents the largest incremental growth opportunity due to expanding industrial activity, infrastructure investment, and rapid manufacturing growth in coatings, adhesives, and agrochemicals. Countries such as China and India are increasing their production capacity for solvents to reduce dependency on imports. Local partnerships and joint ventures between multinational producers and regional refiners are enhancing distribution reach and supply stability, supporting sustained market penetration.

Technological Convergence Toward Bio-Based and Hybrid Solvents

Innovation in hybrid formulations combining bio-based and synthetic hydrocarbons offers a promising opportunity for market participants. Companies investing in low-carbon refining processes and hybrid blending technologies can capture customers seeking eco-friendly solvent options. The ability to balance regulatory compliance with performance benefits will be a decisive differentiator over the coming decade.

Category-wise Analysis

Product Type Insights

The C10–C14 chain isoparaffin range remains the dominant segment with a market share of 44.8% due to its optimal balance of solvency power, evaporation rate, and cost efficiency. These medium-chain hydrocarbons are widely utilized across industrial cleaning, metalworking fluids, adhesives, and coatings applications, where consistent performance and safety are critical. For example, in automotive coatings, C10–C14 isoparaffins are used as carrier solvents that ensure uniform paint film formation and faster drying times. Their low toxicity and favorable flash point make them suitable for large-scale manufacturing plants where worker safety and environmental compliance are key considerations. This segment accounts for approximately 50% of total isoparaffin consumption, reflecting its versatility and broad industrial relevance.

The low-VOC (volatile organic compounds) and high-purity isoparaffin grades are experiencing the fastest growth, fueled by stringent environmental regulations such as the U.S. EPA VOC limits, the EU Solvent Emissions Directive, and rising global sustainability standards. These grades are increasingly adopted in premium cosmetic formulations, electronic cleaning fluids, and pharmaceutical excipients, where impurities or residual odors can compromise product quality. For instance, high-purity isoparaffins are used as solvent carriers in semiconductor cleaning and skincare products, enabling low-irritation formulations. Their growth is further accelerated by consumer demand for safer, environmentally compliant products and by formulators seeking regulatory-friendly alternatives to aromatic solvents.

Application Insights

The paints and coatings segment remains the largest consumer of isoparaffin solvents, representing approximately 43% of global consumption. Urbanization, industrial expansion, and infrastructure development are driving demand for architectural coatings, industrial protective coatings, and automotive paints. In automotive refinish applications, isoparaffins are used to control viscosity, improve leveling, and reduce pinholes in paint films, while in industrial coatings, they facilitate rapid drying without compromising surface finish. Companies such as PPG Industries and Sherwin-Williams frequently rely on these solvents for waterborne and solvent-borne coating systems. The segment benefits from consistent end-use demand and acts as a foundational market for isoparaffin producers globally.

The personal care and cosmetics segment is the fastest-growing. Rising consumer preference for non-irritant, odorless, and fast-absorbing products is increasing the use of isoparaffins as emollients, skin-conditioning agents, and solvent carriers in creams, lotions, and haircare products. For example, C10–C13 isoparaffins are widely used in lip balms, foundation creams, and deodorants for their smooth application, non-greasy feel, and stability. Growth is particularly strong in Asia Pacific, driven by premium skincare brands such as Shiseido and L’Oréal, and in emerging markets where cosmetic penetration is rising rapidly. Expansion of manufacturing facilities in India, China, and ASEAN countries further supports this growth trajectory, creating a robust market for specialty, low-odor grades.

Regional Insights

North America Isoparaffin Solvents Market Trends - Low-VOC Solvent Innovation Driven by Regulations and R&D

North America represents the largest regional market, accounting for approximately 36% of global revenue. The U.S. leads the region due to strong demand from industrial coatings, automotive refinishing, and specialty chemical applications. Major chemical producers headquartered in the U.S., such as ExxonMobil Chemical, Chevron Phillips, and Eastman Chemical, are investing in the development of high-performance, low-odor, and low-VOC solvent systems that comply with the EPA regulations and state-level environmental standards.

Key growth factors in the region include a robust R&D infrastructure, advanced refining capacity, and a strong innovation ecosystem supporting specialty solvent formulations for industrial and consumer applications. Stable feedstock supply from domestic crude and natural gas liquids provides cost efficiency, while established downstream distribution networks ensure reliable delivery to end-users.

Regulatory frameworks, including VOC emission restrictions and worker safety standards, have accelerated the adoption of low-VOC isoparaffin products, particularly in coatings and cleaning formulations. Recent developments include ExxonMobil’s 2024 expansion of its low-VOC isoparaffin production facility in Texas, aimed at strengthening regional self-sufficiency and export capacity, and Chevron Phillips’ investment in specialty solvent technology for advanced coatings.

Europe Isoparaffin Solvents Market Trends - Sustainability and Regulatory Pressure Shape Solvent Development

Europe maintains a significant share of global demand, supported by its mature automotive, construction, and specialty chemical sectors. Countries such as Germany, the U.K., France, and Spain are the primary contributors, emphasizing eco-friendly and sustainable solvents in industrial applications. Stringent environmental regulations under the EU VOC Directive and REACH framework serve both as challenges and catalysts, compelling formulators to replace aromatic solvents with cleaner hydrocarbon alternatives, including high-purity isoparaffins.

The European market is characterized by a trend toward process integration and lifecycle analysis (LCA) compliance, ensuring solvent products meet sustainability metrics. Consumer and industrial emphasis on green chemistry has stimulated innovation in bio-based and hybrid solvent formulations, while collaborative R&D programs and joint ventures between regional and multinational producers enhance the region’s competitiveness.

Notable developments include Shell Chemicals’ launch of low-carbon, high-purity isoparaffins in Germany in 2025 for premium coating and cosmetic applications, and INEOS’ partnership with a French specialty chemical company to produce environmentally compliant hydrocarbon solvents for industrial users.

Asia Pacific Isoparaffin Solvents Market Trends - Rapid Industrialization Fuels High-Purity Solvent Demand

The Asia Pacific region is the fastest-growing market, projected to register the highest CAGR through 2032. Key countries such as China, Japan, India, and South Korea are witnessing an upsurge in demand due to expanding coatings, adhesives, personal care, and agrochemical industries. Favorable labor costs, increasing industrialization, and government initiatives to attract foreign investment have established the region as a global hub for solvent production and consumption.

China dominates in volume, driven by large-scale industrial cleaning and coating operations in sectors such as automotive manufacturing and electronics. India’s rapidly expanding chemical manufacturing sector offers new growth opportunities, particularly in industrial and personal care applications. Japan and South Korea focus on high-purity and cosmetic-grade isoparaffin solvents to meet stringent quality standards for electronics, personal care, and pharmaceutical sectors.

Government programs promoting sustainable chemical manufacturing are fostering innovation in low-emission formulations, while infrastructure investments across ASEAN countries support expanding demand. Recent developments include Petronas Chemicals’ new specialty solvent facility in Malaysia (2024) to supply high-purity grades for cosmetic and industrial applications, and Yitai Ningneng Fine Chemicals’ expansion in China (2025) targeting both domestic and export markets.

Competitive Landscape

The global isoparaffin solvents market is moderately consolidated, dominated by major players such as ExxonMobil, Shell, Chevron Phillips, TotalEnergies, Idemitsu Kosan, and INEOS. North America and Europe show higher concentration, while Asia Pacific features a mix of global and local producers.

Leading companies focus on vertical integration, regional growth, low-VOC/odor innovations, sustainability, and customized solutions backed by strategic partnerships and secure feedstock supply.

Key Industry Developments

- In March 2024, ExxonMobil Chemical expanded its specialty hydrocarbon solvent capacity at facilities in the U.S. and Singapore, strengthening global supply reliability for low-VOC isoparaffin grades. The expansion aligns with the company’s focus on premium formulations for coatings and personal care.

- In July 2024, Idemitsu Kosan announced a regional investment in Japan to enhance its solvent production capabilities aimed at supporting domestic specialty chemical manufacturers. The initiative targets improved feedstock integration and cost efficiency.

- In February 2025, Shell Chemicals unveiled a new line of high-purity, low-carbon isoparaffin solvents designed to meet evolving regulatory and sustainability demands. This move reflects the industry’s shift toward environmentally compliant products and carbon-neutral operations.

Companies Covered in Isoparaffin Solvents Market

- ExxonMobil Chemical Company

- Shell Chemicals

- Chevron Phillips Chemical Company

- INEOS Group Holdings S.A.

- Idemitsu Kosan Co., Ltd.

- TotalEnergies

- Sasol Ltd.

- Petronas Chemicals Group

- Repsol S.A.

- Braskem S.A.

- Yitai Ningneng Fine Chemicals

- RB Products Inc.

- Haltermann Carless

- Univar Solutions

- SK Global Chemical

- LyondellBasell Industries

- Huntsman Corporation

- Mitsubishi Chemical Corporation

- Eastman Chemical Company

- Chevron Oronite

Frequently Asked Questions

The Isoparaffin Solvents Market is estimated to be valued at US$0.92 Billion in 2025, driven by the rising demand from coatings, adhesives, and personal care industries.

By 2032, the market is projected to reach US$1.190 Billion, reflecting a steady increase in consumption across industrial cleaning and specialty formulation applications.

Key trends include the shift toward low-VOC and eco-friendly solvent systems, increased adoption in cosmetics and personal care formulations, and the development of high-purity grades suitable for industrial coatings and metalworking fluids.

The industrial cleaning segment leads the market, accounting for a major share due to the widespread use of isoparaffin solvents in precision cleaning, degreasing, and maintenance applications across manufacturing and automotive industries.

The isoparaffin solvents market is expected to grow at a CAGR of 3.8% from 2025 to 2032, supported by steady expansion in construction coatings, printing inks, and personal care formulations that demand high-purity, odorless, and environmentally safe solvents.

Major players include ExxonMobil Chemical Company, Shell Chemicals, Chevron Phillips Chemical Company LLC, INEOS Group Ltd., and TotalEnergies SE.