- Bulk Chemicals

- India Solvents Market

India Solvents Market Size, Share, and Growth Forecast, 2025 - 2032

India Solvents Market By Product Type (Alcohols, Chlorinated Solvent, Ketones), Source (Bio-based, Petrochemical-based), Application (Printing Ink, Paints and Coatings, Metal Working, Industrial Cleaning), and Zone Analysis for 2025 - 2032

India Solvents Market Size and Trends Analysis

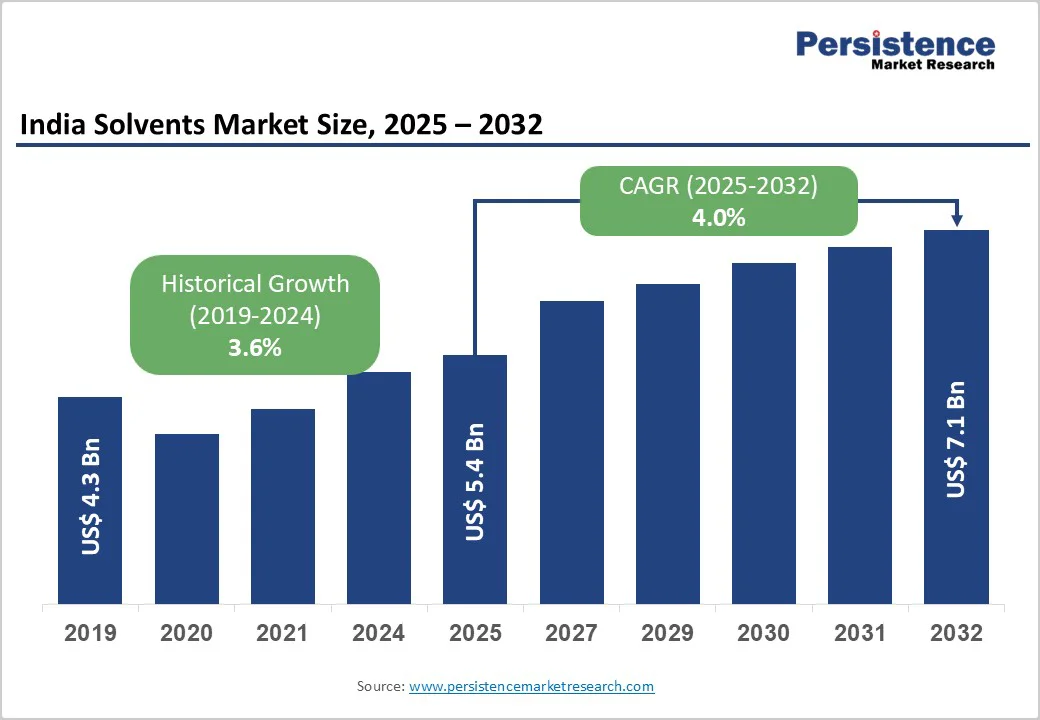

The India solvents market size is likely to be valued at US$5.4 Billion in 2025 and is estimated to reach US$7.1 Billion in 2032, growing at a CAGR of 4.0% during the forecast period 2025 - 2032, fueled by expanding end-user industries and the evolving environmental standards. Rapid growth in the pharmaceutical, paints and coatings, and adhesives sectors is spurring consistent demand.

Key Industry Highlights

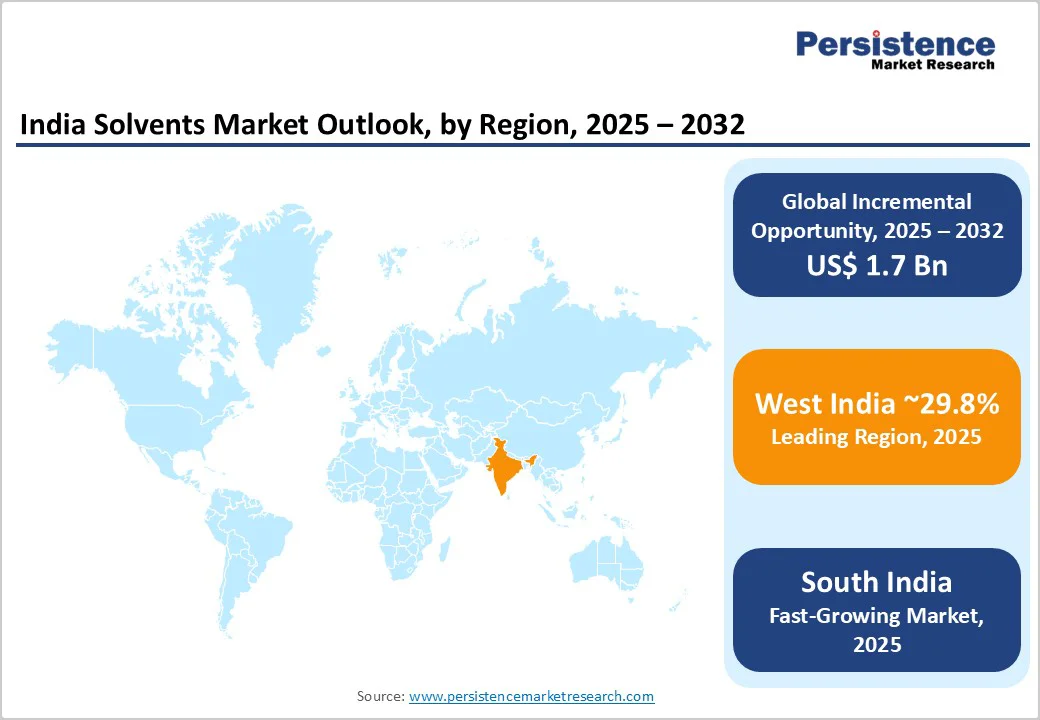

- Leading Region: West India, with about 29.8% share in 2025, due to a well-established petrochemical infrastructure.

- Fastest-growing Region: South India, owing to expanding pharmaceutical and agrochemical industries in Telangana, Andhra Pradesh, and Tamil Nadu.

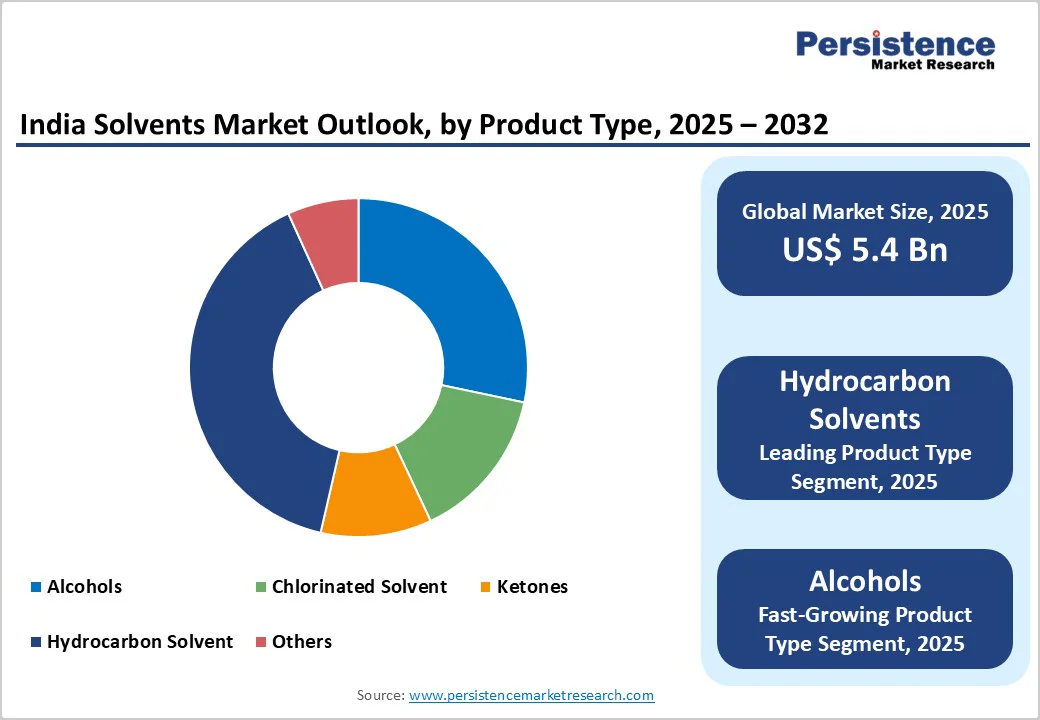

- Leading Product Type: Hydrocarbon solvents hold nearly 39.6% share in 2025, backed by their excellent dissolving power and fast evaporation.

- Dominant Source: Bio-based solvents, approximately 65.7% of the India solvents market share in 2025, boosted by the push for sustainable manufacturing.

- Key Application: Paints and coatings recorded about 42.1% share in 2025, spurred by increasing infrastructure projects and automotive production activities.

- Development Center: Lanxess recently launched its India Application Development Center in Thane, Mumbai, to broaden its research and development as well as innovation footprint for chemicals and coatings.

| Key Insights | Details |

|---|---|

| India Solvents Market Size (2025E) | US$5.4 Bn |

| Market Value Forecast (2032F) | US$7.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surging Pharmaceutical Production Boosting Solvent Demand

India’s expanding pharmaceutical sector is pushing the demand for high-purity solvents used in drug formulation, extraction, and purification processes. The country’s rising export base, accounting for nearly 20% of global generic drug supply, has led to surging demand for GMP-compliant and low-residue solvents.

Companies such as Sun Pharma and Dr. Reddy’s are increasing API and formulation capacity, requiring stable supplies of solvents, including acetone, ethanol, and isopropyl alcohol. The rise of contract manufacturing, as well as research and development partnerships with global pharma firms, is creating opportunities for specialized solvent suppliers capable of meeting stringent regulatory and quality standards.

Industrial Growth Spurring Solvent Consumption across Applications

Rapid growth in manufacturing sectors such as paints and coatings, automotive, adhesives, and agrochemicals is expanding solvent usage in India. The government’s Make in India initiative and the Production-Linked Incentive (PLI) schemes have led to new industrial investments, especially in chemical and automotive hubs.

For example, Nippon Paint and Tata Motors have extended local production facilities, which rely heavily on solvent-based coatings and cleaning agents. This industrial push, combined with infrastructure and construction growth, continues to strengthen solvent consumption across multiple downstream industries.

Barrier Analysis - Environmental Risks from Unsafe Handling and Disposal Practices

In India, the lack of proper solvent waste management infrastructure poses a serious challenge. Various small and mid-sized manufacturers still dispose of spent solvents or residues without adequate treatment, leading to contamination of nearby water bodies and soil.

Industrial belts in states such as Gujarat and Maharashtra have reported cases where solvent leakage and poor storage have caused local pollution concerns. Such incidents not only damage ecosystems but also result in strict inspections and operational shutdowns for non-compliant facilities, thereby affecting production continuity.

High Cost and Regulatory Burden of Hazardous Waste Treatment

Managing solvent waste is both technically complex and expensive. Companies handling large volumes of solvents must comply with stringent hazardous waste norms under the Central Pollution Control Board (CPCB), which require costly treatment systems and disposal permits.

Small chemical units often struggle to meet these compliance costs, making solvent recovery and recycling less feasible. Recent policy tightening around hazardous waste transportation and disposal has further increased operational expenses, discouraging small-scale players from extending their solvent-based production lines.

Opportunity Analysis - Rising Demand for Eco-friendly and Low-emission Solvents

India is witnessing rising adoption of low-VOC and bio-based solvents as industries shift toward green formulations. Sectors such as paints and coatings, adhesives, and pharmaceuticals are replacing traditional petrochemical solvents with sustainable alternatives to meet tightening emission norms and consumer demand for safe products.

For example, Berger Paints and Nerolac are developing low-VOC coatings to comply with green building standards. In addition, companies such as Godavari Biorefineries are expanding their bio-based chemical production from sugarcane feedstock, creating fresh opportunities for bio-derived solvent manufacturing across India.

Government Backing Encouraging Bio-derived Solvent Development

Supportive national policies are accelerating investment in bio-based chemistry. The National Biofuel Policy, which promotes the use of renewable feedstocks such as ethanol and biomass, is indirectly aiding bio-based solvent development.

Firms such as Praj Industries are using these initiatives to broaden biorefinery capacities, providing sustainable raw materials for solvent production. With increased government funding for renewable chemistry and circular economy projects, the policy framework is fueling long-term opportunities for solvent producers to transition toward bio-based and recyclable solvent ecosystems.

Category-wise Analysis

Product Type Insights

Hydrocarbon solvents are predicted to capture about 39.6% of the market share in 2025, backed by their excellent dissolving power, quick evaporation rate, and cost-effectiveness. They are essential in paints, coatings, and cleaning formulations where high solvency strength and uniform film formation are required.

Their availability from domestic refineries such as Indian Oil and Reliance ensures a stable supply, further boosting their usage. Recent capacity expansions in automotive and industrial coatings have also increased reliance on hydrocarbon solvents for efficient drying and surface finishing.

Alcohols such as ethanol and isopropyl alcohol (IPA) are gaining traction due to their low toxicity, versatility, and suitability for both industrial and pharmaceutical use. The post-pandemic growth of sanitizers and disinfectants drastically expanded IPA production in India, with Deepak Fertilizers and INEOS increasing output.

Also, their compatibility with water-based formulations and reduced environmental footprint make alcohols an ideal choice for eco-friendly coatings, adhesives, and personal care formulations.

Source Insights

Bio-based solvents are leading with approximately 65.7% of the share in 2025, as industries adopt clean production methods to reduce carbon emissions. Derived from renewable sources such as corn, sugarcane, or soybean oil, these solvents deliver low VOC content and biodegradability.

Companies such as Godavari Biorefineries and Praj Industries are expanding their biorefinery operations to supply green solvents for paints, inks, and cleaning products. With global brands demanding sustainable sourcing, bio-based solvents have emerged as a strategic alternative to fossil-derived counterparts.

Petrochemical-based solvents continue to see demand growth due to their high purity, consistent performance, and wide industrial applications. India’s expanding petrochemical infrastructure, such as Indian Oil’s upcoming PX/PTA plant in Paradip, ensures steady feedstock availability.

These solvents remain indispensable in paints, pharmaceuticals, and adhesives where precise formulation control is required. Developments in refining technologies have further enabled the production of low-aromatic and clean variants, helping retain their competitiveness amid tightening environmental norms.

Application Insights

Paints and coatings are anticipated to dominate with nearly 42.1% of the share in 2025, boosted by ongoing construction activity, vehicle production, and decorative paint demand. Solvents are essential for dissolving resins, controlling viscosity, and ensuring smooth film application.

Asian Paints and Berger Paints are investing heavily in new plants and premium product lines, many of which rely on solvent-borne systems for durability and finish. The shift toward protective and industrial coatings for infrastructure projects has also reinforced this dominance.

The printing ink segment relies heavily on solvents for pigment dispersion and drying control. The rise of flexible packaging, e-commerce, and food labeling has expanded demand for solvent-based inks that provide superior adhesion and quick drying on diverse substrates.

India-based manufacturers such as Sakata Inx and Toyo Ink India are improving production capacities to meet packaging industry growth. Also, the transition to solvent blends that reduce VOCs without compromising print quality has sustained the importance of this segment in the regional market.

Regional Insights

West India Solvents Market Trends

West India is speculated to account for around 29.8% of the share in 2025, as Gujarat and Maharashtra are the zone’s main solvent manufacturing hubs due to their well-established petrochemical base and industrial clusters. The presence of leading refineries and chemical complexes in Jamnagar, Dahej, and Hazira ensures abundant feedstock for hydrocarbon and petrochemical-based solvents.

Companies such as Deepak Nitrite, Aarti Industries, and Reliance Industries have expanded production capacities to meet the rising demand from paints, coatings, and pharmaceutical manufacturers in the zone. The Gujarat Industrial Development Corporation (GIDC) estates have also promoted solvent recovery and recycling units to improve sustainability. With the western region housing India’s largest paint and pharma plants, it remains the dominant zone for both production and consumption of solvents.

South India Solvents Market Trends

South India’s market is primarily boosted by the growth of the pharmaceutical and agrochemical sectors in Telangana, Andhra Pradesh, and Tamil Nadu. Hyderabad’s pharma corridor, one of Asia Pacific’s largest API hubs, heavily relies on high-purity solvents such as acetone, methanol, and IPA for drug manufacturing.

Several companies, including Laurus Labs and Divi’s Laboratories, have extended capacity and established solvent recovery systems to ensure regulatory compliance and cost efficiency. The region’s proximity to ports such as Chennai and Visakhapatnam also aids in the easy import of specialty solvents. Rising demand from the electronics and coatings industries in Karnataka and Tamil Nadu is also contributing to solvent consumption growth.

North India Solvents Market Trends

In North India, solvent demand is mainly influenced by the thriving paint, coatings, and printing industries across Delhi NCR, Haryana, and Punjab. The construction boom and surging automotive component manufacturing in this belt have boosted the use of solvent-based coatings and adhesives.

Prominent paint companies, including Kansai Nerolac and Nippon Paint, have strengthened their presence in this region to cater to rising urban and industrial demand. However, solvent production is relatively limited here compared to western and southern India, making the region more dependent on supplies from Gujarat and Maharashtra. The push for low-VOC paints and sustainable inks is also gradually influencing solvent preferences in this market.

Competitive Landscape

The India solvents market is influenced by both domestic giants and multinational players. Local companies such as Reliance Industries, Deepak Nitrite, and Aarti Industries dominate bulk solvents due to their superior backward integration in petrochemicals and cost efficiency.

Multinational firms, including BASF, Shell Chemicals, and Eastman, focus more on specialty and eco-friendly solvents, catering to high-value sectors such as pharmaceuticals, coatings, and adhesives. The presence of both segments creates a highly competitive market where pricing and quality consistency play key roles.

Key Industry Developments

- In June 2025, DCM Shriram Ltd approved the acquisition of Hindusthan Specialty Chemicals Ltd (HSCL) for ?375 crore, marking its entry into the epoxy and advanced-materials field. HSCL’s plant in Jhagadia produces liquid epoxy resins, solvent cuts, and related resins for sectors such as aerospace and EVs.

- In April 2025, Deepak Chem Tech (a Deepak Nitrite subsidiary) announced its plans to invest heavily in a new phenol and solvent manufacturing hub to produce phenol, acetone, and isopropyl alcohol domestically, aiming to reduce import dependence.

Companies Covered in India Solvents Market

- BASF SE

- Exxon Mobil Corporation

- Royal Dutch Shell plc.

- Total S.A.

- Idemitsu Kosan Co., Ltd.

- The Dow Chemical Company

- Solvay S.A.

- Ashland Inc.

- Bharat Petroleum Corporation Limited

- India Glycols Limited.

- Hindustan Petroleum Corporation Limited

- Eastman Chemical Company

Frequently Asked Questions

The India solvents market is projected to reach US$5.4 Billion in 2025.

Expanding pharmaceutical and coatings industries are the key market drivers.

The India solvents market is poised to witness a CAGR of 4.0% from 2025 to 2032.

Government support for green chemistry and rising investments in bio-refinery projects are the key market opportunities.

BASF SE, Exxon Mobil Corporation, and Royal Dutch Shell plc. are a few key market players.