- Industrial Goods & Service

- Power Tools Market

Power Tools Market Size, Share, Trends, and Growth Forecasts 2025 - 2032

Power Tools Market By Product (Drills & Drivers, Fasteners, Wrenches, Power Saws, Grinders & Sanders, Demolition Hammers, Guns, Material Remover, Other), Mode of Operation, Application, Distribution Channel, and Regional Analysis from 2025 - 2032

Market Overview

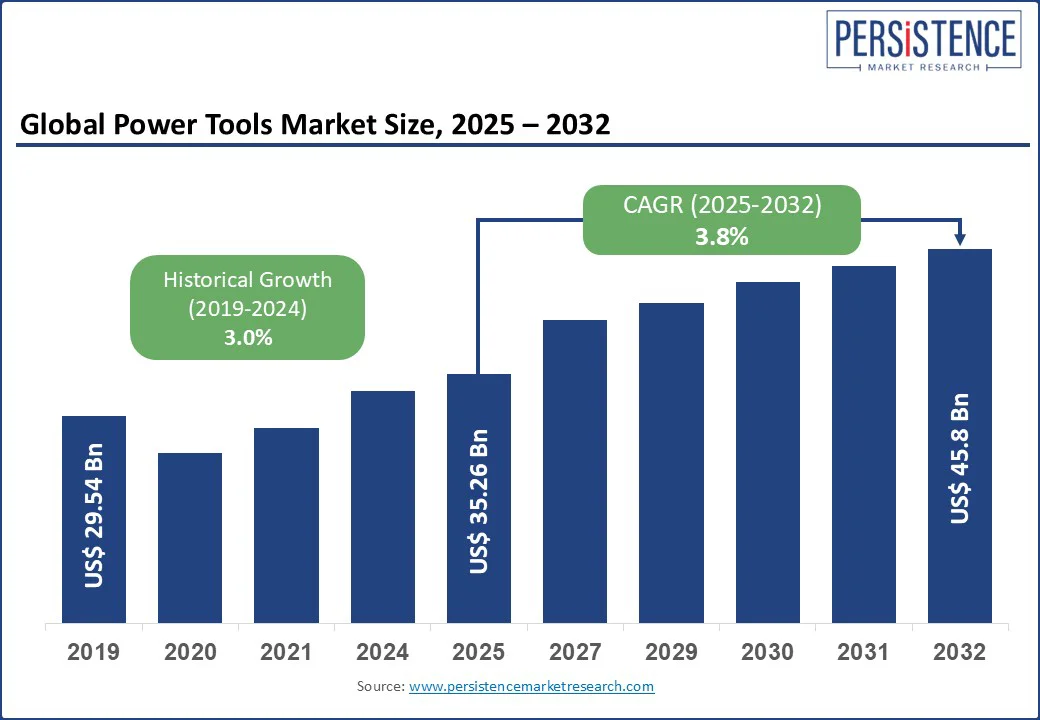

The global power tools market size was valued at US$35.3 Bn in 2025 and is projected to reach US$45.8 Bn by 2032, growing at a CAGR of 3.8% between 2025 and 2032.

The market is demonstrating robust growth, driven by technological advancements in battery technology, the expansion of cordless tool adoption, and a rising DIY culture worldwide.

Key Highlights:

- Drills & drivers are the leading product category with over 25.8% market share in 2025, while fastening tools experience rapid growth driven by manufacturing automation and precision application requirements.

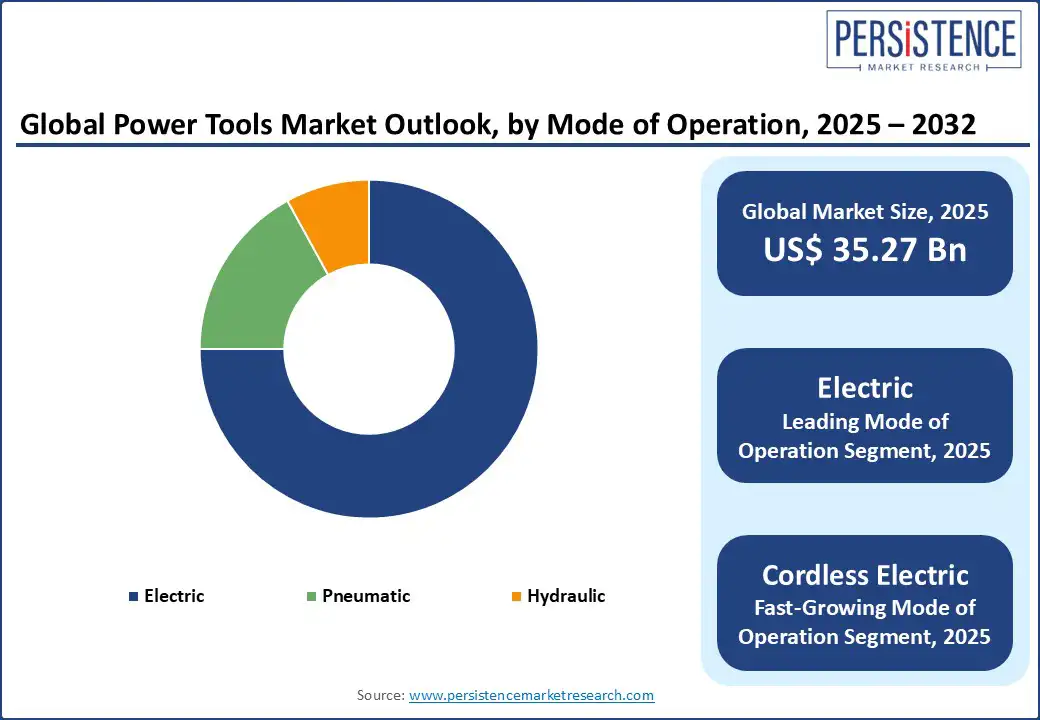

- Electric tools dominate with 75% market share in 2025, with cordless variants showing the strongest growth due to lithium-ion battery improvements and enhanced portability for professional applications.

- Construction & renovation applications account for over 50% of market demand in 2025, supported by global infrastructure investment and urbanization trends across emerging economies.

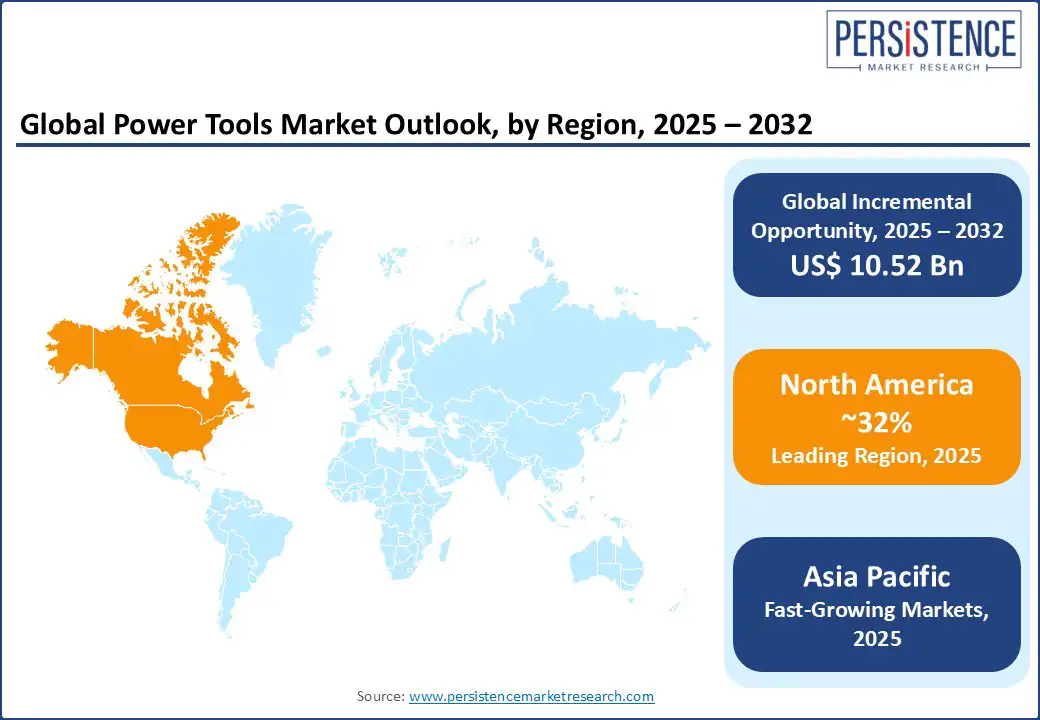

- North America maintains a 32% global market share in 2025, while Asia Pacific emerges as the fast-growing region with a robust CAGR through 2032

- DIY/Home improvement segment demonstrates rapid expansion driven by rising homeowner engagement, e-commerce accessibility, and post-pandemic lifestyle changes emphasizing self-reliance and cost savings

- Smart technology integration and IoT connectivity present significant opportunities for market differentiation and premium positioning among professional contractor segments seeking enhanced productivity and operational insights.

| Key Insights | Details |

|---|---|

|

Power Tools Market Size (2025E) |

US$35.27 Billion |

|

Projected Market Value (2032F) |

US$45.8 Billion |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

3.8% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

3.0% |

Market Dynamics Analysis

Market Drivers

Rapid Advancement of Battery-powered Technologies is Significantly Driving the Demand for Cordless Power Tools

The power tools industry is experiencing a transformational shift driven by advanced lithium-ion battery technology and brushless motor innovations. High-capacity batteries now provide extended runtime, faster charging capabilities, and superior energy density compared to previous generations. This technological advancement has resulted in cordless tools capturing approximately 30% of total power tool sales globally, with the cordless segment projected to grow at a CAGR of 6.0% through 2032.

Brushless motor technology enhances tool efficiency by 25-30% while extending battery life and reducing maintenance requirements, making cordless tools increasingly competitive with corded alternatives for professional applications.

Infrastructure Development and Construction Boom

Global construction activities serve as the primary growth catalyst, with the construction sector accounting for over 50% of the power tools market demand in 2025. Government infrastructure initiatives significantly boost market growth, including the U.S. Infrastructure Investment and Jobs Act, India's National Infrastructure Pipeline worth US$1.4 trillion, and China's Belt and Road Initiative.

The Asian Development Bank projects infrastructure investment needs exceeding US$1.7 trillion annually through 2033 in Asia alone, emphasizing sustained demand for construction tools. Modern construction techniques, including modular construction and smart building technologies, require precision power tools, further driving market expansion.

DIY Culture and Home Improvement Trends

The DIY home improvement market represents a rapidly growing segment, valued at US$800 billion in 2025 and is anticipated to reach US$1.5 trillion by 2032 at a CAGR of 8%. Post-pandemic lifestyle changes have accelerated DIY adoption, with 75% of homeowners attempting DIY projects and 73% citing cost savings as the primary motivation.

The home improvement market in the U.S. is projected to reach US$700 billion by 2030, driven by homeowner confidence and rising disposable income. E-commerce platform expansion facilitates DIY tool accessibility, with DIY e-commerce revenues likely to exceed US$350 billion globally in 2025.

Market Restraints

Geopolitical Tension, Tariff Pressures, and Supply Chain Realignment Triggers Power Tool Costs

The power tools industry faces significant challenges from fluctuating raw material prices, particularly steel and aluminum costs, which have increased substantially. Raw material prices are averaging 10% higher compared to previous periods, with specific materials like steel experiencing 8.2% price increases and aluminum seeing 5.7% price hikes.

International trade policies significantly impact market dynamics, particularly U.S.-China trade relations. The additional 20% tariff imposed on Chinese power tools in March 2025, combined with the existing 18.9% tariff rates, creates a total burden of approximately 38.9% for Chinese imports.

Major manufacturers such as Stanley Black & Decker have implemented price increases and accelerated supply chain reconfiguration, shifting manufacturing from China to Mexico and Southeast Asia to achieve zero China exposure by 2027. These tariffs create operational pressures and pricing challenges, particularly affecting budget-conscious consumers and emerging market buyers.

Market Opportunities

Smart Technology Integration and IoT Connectivity

The integration of Internet of Things (IoT) technology presents substantial growth opportunities, with connected IoT devices growing 13% to 20 billion globally in 2025. Smart power tools equipped with Bluetooth connectivity, performance monitoring, and predictive maintenance capabilities are gaining traction among professional contractors.

Companies such as Hilti and Milwaukee are expanding smart tool portfolios with features including battery health monitoring, usage analytics, and automated inventory management. The industrial IoT market enables predictive maintenance, reducing downtime and optimizing tool performance across construction and manufacturing applications.

Emerging Market Penetration and Infrastructure Investment

Emerging economies present a significant growth potential, particularly in the Asia Pacific region, where the market growth is projected to exceed a CAGR of 6% through 2032. India's power tools market is expected to surpass US$3 billion by 2032, driven by infrastructure development and manufacturing expansion. China's construction sector demonstrates robust growth, with infrastructure investment rising 8.7% in recent reporting periods.

Government initiatives, including India's Smart Cities Mission targeting 100 smart cities and Southeast Asian infrastructure modernization programs, create sustained demand for advanced power tools across professional and industrial segments.

Sustainability and Green Technology Adoption

Environmental regulations and sustainability initiatives drive demand for energy-efficient power tools. The EU Green Deal and India's Make in India campaign encourage cleaner, electrified tools in manufacturing and construction applications.

Battery technology improvements support sustainability goals through longer tool lifecycles and reduced environmental impact. Companies are increasingly focusing on circular economy principles, incorporating recycled materials and developing rechargeable battery platforms that reduce waste generation across tool categories.

Segmentation Analysis

Product Type Analysis

Drills & Drivers Leading Market Share

Drills & drivers dominate the power tools market with over 25.8% market share in 2025, attributed to their versatility across construction, renovation, metal fabrication, and woodworking applications. Their compatibility with both electric and cordless platforms enhances user convenience and operational efficiency.

Market leadership is reinforced by increasing infrastructure development and expanding the DIY user base, which in turn requires precision drilling and fastening capabilities. The segment benefits from continuous technological improvements, including brushless motors, variable speed controls, and enhanced ergonomic designs.

Fastening Tools Experiencing Rapid Growth

Fastening tools represent the fastest-growing product segment, driven by automation in assembly lines within high-precision industries, including automotive and aerospace manufacturing.

Professional contractors increasingly adopt advanced fastening solutions for efficiency improvements and consistent quality outcomes. The segment growth is supported by technological innovations, including smart fastening systems with torque control and digital connectivity features enabling precise application monitoring and documentation.

Mode of Operation Analysis

Electric Tools Maintain Dominant Position

Electric power tools command 75% market share in 2025, driven by reliability, ease of use, and broad application suitability across construction, industrial, and residential segments. The dominance reflects improved battery technology, making cordless electric tools increasingly preferred over corded alternatives.

Enhanced battery capacity, faster charging, and lightweight designs contribute to operational convenience without compromising power output. Government initiatives promoting electric tool adoption for noise reduction and environmental compliance further strengthen the market position.

Cordless Technology Driving Innovation

Within the electric segment, cordless tools demonstrate the highest growth path, supported by lithium-ion battery improvements providing longer runtime and faster recharge cycles. Professional users increasingly adopt cordless solutions for enhanced mobility and reduced setup time. The technology evolution includes platform compatibility across tool ranges, enabling users to utilize single battery systems across multiple tools, improving cost-effectiveness and operational efficiency.

End-use Application Analysis

Construction & Renovation Sector Leadership

Construction and renovation applications accounted for over 50% of the power tools market demand in 2025, driven by robust infrastructure expansion, housing upgrades, and commercial development projects. The segment benefits from government infrastructure initiatives and urbanization trends across emerging economies.

Power tools serve as essential equipment for precision tasks, including cutting, drilling, grinding, and fastening operations across residential, commercial, and industrial construction projects.

DIY/Home Improvement Rapid Expansion

The DIY/Home improvement segment represents the fastest-growing application category, fueled by rising homeowner engagement in renovation projects and the accessibility of user-friendly tools.

Post-pandemic lifestyle changes have accelerated DIY adoption, with homeowners undertaking projects ranging from simple repairs to complex renovations. E-commerce platform growth and online tutorial availability further support segment expansion by reducing barriers to DIY tool adoption among non-professional users.

Regional Market Insights

North America Power Tools Market

North America maintains market leadership with 32% global market share in 2025. The region demonstrates a preference for cordless electric tools driven by stringent noise pollution regulations and the integration of Industry 4.0 practices. Government initiatives, including the Infrastructure Investment and Jobs Act, drive demand for efficient precision tools across construction and manufacturing sectors.

The region's focus on premium quality tools with advanced features commands higher price points while maintaining strong brand loyalty among professional contractors. In January 2025, Hilti North America launched the DD 150-U-22 Cordless diamond core rig, two DSH 600/700 cut-off saws, and PR 4/40/40G-22 Rotating Lasers to enhance the all-in-one Nuron battery platform, addressing the needs of contractors in the commercial construction industry.

U.S. Power Tools Market – 2025 Snapshot & Beyond

The U.S. power tools market size in 2025 is expected to surpass US$10 billion, benefiting from growing repair & renovation activities in the residential sector, new construction projects in the commercial segment, and a resounding echo of DIY culture.

The U.S. power tools market primarily benefits from strong residential and commercial renovation demand, supported by high disposable incomes and aging infrastructure.

Product development and IoT integration from the major manufacturers, including Stanley Black & Decker, Techtronic Industries, and regional innovation centers, further reinforce the region’s leadership. Distribution channels remain predominantly offline due to consumer preference for tangible product experience, though e-commerce adoption is accelerating among younger demographics.

Europe

Europe represents a significant market segment driven by active renovation and maintenance activities, infrastructure development, and a strong DIY culture. The region's pioneers’ adoption of eco-friendly power tools also aligns with environmental sustainability goals.

Government initiatives, including the EU Renovation Wave Strategy, aiming to double building renovations by 2030, create sustained demand for cordless tools across residential and commercial sectors. Germany's Climate Neutral Building Plan further drives electric tool adoption for reduced environmental impact.

DIY (do-it-yourself) projects are a significant factor driving the demand for power tools in the region. Countries like Germany, France, and the U.K. have a strong DIY culture, with homeowners actively engaging in home improvement activities. In contrast, countries such as Spain, Italy, Poland, and Portugal tend to favor the "do-it-for-me" (DIFM) approach, where home improvement tasks are often entrusted to professional services rather than being handled by the homeowners themselves.

The European market demonstrates a preference for premium quality tools with advanced safety features and compliance with stringent regulatory standards. Professional contractors prioritize durability and precision, while DIY enthusiasts increasingly adopt cordless solutions for convenience and portability.

Regional manufacturers focus on innovation in battery technology and smart connectivity features to maintain competitive positioning against global players. The European Power Tool Association (EPTA) also acknowledges cordless electric power tools as the fast-growing category in the power tools segment, reflecting greater portability and safety of these devices.

Asia Pacific

Asia Pacific emerges as the fastest-growing regional market with a 24% global share in 2025. The region's growth is driven by rapid urbanization, infrastructure development, and an expanding middle-class population with increased disposable income. China's infrastructure investment growth of 8.7% and India's Smart Cities Mission create substantial demand for construction and industrial power tools.

India's power tools market is projected to exhibit robust growth during the forecast period, supported by government initiatives and manufacturing sector expansion. The region demonstrates increasing adoption of cordless tools driven by affordability improvements and e-commerce accessibility. Rising DIY culture in urban areas and growing awareness of power tool benefits contribute to market expansion across professional and consumer segments.

Competitive Landscape

The global power tools market demonstrates moderate concentration with leading players collectively holding approximately 40% market share. Stanley Black & Decker, Robert Bosch, Techtronic Industries, Makita Corporation, and Hilti Corporation comprise the top-tier manufacturers with significant global presence and diversified product portfolios. The competitive landscape includes established multinational corporations alongside regional manufacturers focusing on specific market segments and price-competitive solutions.

Market dynamics emphasize technological innovation, brand strength, and distribution network effectiveness as primary competitive differentiators. Leading companies invest heavily in R&D for battery technology advancement, smart connectivity features, and ergonomic design improvements to maintain market leadership and command premium pricing.

Business Strategies Adopted by Leading Companies

Innovation Leadership and Technology Differentiation

Market leaders prioritize continuous R&D investment in battery technology, brushless motors, and smart connectivity features to maintain competitive advantages. Companies focus on developing integrated tool ecosystems with compatible battery platforms across product ranges, enhancing customer value proposition and encouraging brand loyalty through platform lock-in effects.

Market Expansion and Distribution Enhancement

Strategic emphasis on emerging market penetration through local partnerships, affordable product development, and e-commerce platform expansion. Companies balance premium positioning in developed markets with cost-competitive offerings in price-sensitive emerging economies to capture broader market opportunities while maintaining profit margins.

Recent Industry Developments

- In May 2025, Milwaukee Tool introduced the latest advancement to their circular saw blade lineup. Designed for professional framers, carpenters, remodelers, roofers, and general contractors, the 7-1/4 inches 24T NITRUS™ Carbide Framing & Demolition Circular Saw Blade delivers the best-in-class cutting solution for framing and demolition applications, offering the fastest cuts and longest life.

- In June 2025, Bosch Power Tools announced a new round of product additions to its growing 18V cordless and accessory portfolio with latest tools and solutions engineered for power, versatility, and efficiency across a wide range of jobsite tasks. From nailing and drilling to grinding and layout work, these toolbox essentials are designed for tradespeople who demand performance and reliability in every application.

Companies Covered in Power Tools Market

- Atlas Copco AB

- Emerson Electric Co.

- Enerpac Tool Group

- Hilti Corporation

- Ingersoll Rand

- Stanley Black & Decker Inc.

- Robert Bosch GmbH

- Makita Corporation

- Apex Tool Group

- Techtronic Industries Co., Ltd.

Frequently Asked Questions

Yes, the market is set to reach US$ 45.8 Bn by 2032.

Rising construction activities in the emerging economies and industrial automation drives the demand for the power tool market.

Increasing home renovation and DIY culture, with the growing penetration of online channels, is creating the opportunity for the market.

India is estimated to witness a CAGR of 4.1% in the forecast period.

Robert Bosch GmbH is considered the leading player in the Power Tools market.