- Automotive Components & Materials

- Electric Vehicle Power Inverter Market

Electric Vehicle Power Inverter Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Electric Vehicle Power Inverter Market by Propulsion Type (Battery Electric Vehicles – BEV, Fuel Cell Electric Vehicles – FCEV, Plug-in Hybrid Electric Vehicles – PHEV), Power Output (Up to 100 kW, 101–300 kW, 301–600 kW, Above 600 kW), Vehicle Type (Passenger Cars, Commercial Vehicles – LCV, HCV), and Region Analysis for 2026 - 2033

Electric Vehicle Power Inverter Market Trends & Analysis

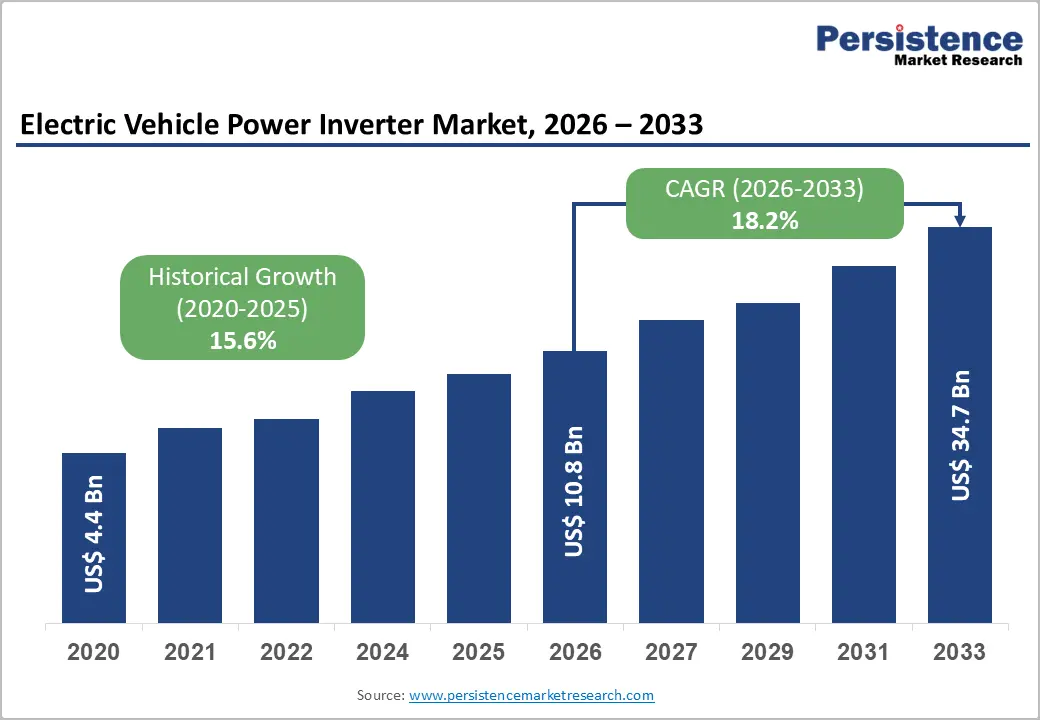

The global Electric Vehicle Power Inverter Market size is projected at US$ 10.76 Bn in 2026 and is projected to reach US$ 34.69 Bn by 2033, growing at a CAGR of 18.2% between 2026 and 2033. IEA's Global EV Outlook 2025 confirmed over one in four cars sold globally in 2025 are electric; BEV propulsion inverter share stands at 58.4%; Asia Pacific commands 51.3% growth driven by China's 4.1 Bn market; and SiC-based inverter adoption, enabling 25–30% efficiency gains is accelerating commercial vehicle and FCEV powertrain investment globally.

Accelerating global EV adoption, mandatory zero-emission vehicle regulatory frameworks across North America, Europe, and China, and the transition to silicon carbide semiconductor inverter technology, driving efficiency gains, are the primary structural growth drivers. The historical 15.6% CAGR from 2020 to 2026 confirms technology-driven rapid market formation sustained by OEM electrification investment programs and government EV incentive policies globally.

Key Industry Highlights:

- Leading Propulsion Type: BEV leads at 58.4% share (~US$ 6.28 Bn); FCEV grows fastest at 21.1% CAGR, driven by Japan NEDO US$ 18 Bn hydrogen fund and EU REPowerEU FCEV commercial vehicle deployment programs globally through 2033.

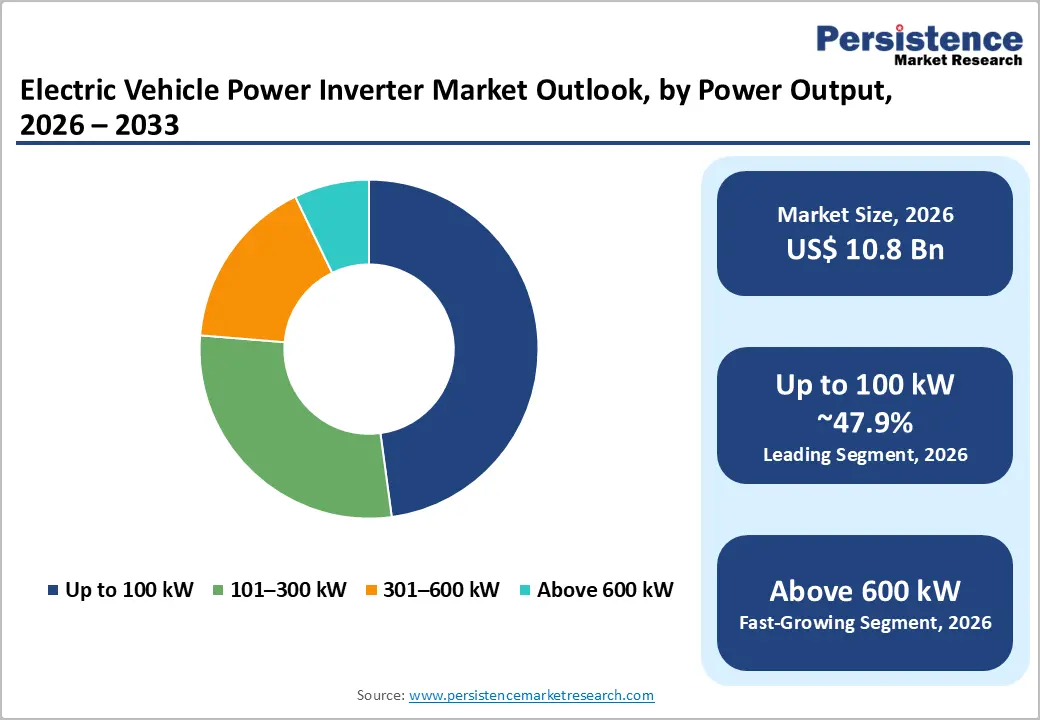

- Leading Power Output: Up to 100 kW leads at 47.9% share (~US$ 5.15 Bn); Above 600 kW grows fastest at 21.9% CAGR driven by EU 2040 zero-emission HCV mandate and commercial fleet electrification at Daimler Truck and Volvo Group.

- Leading Vehicle Type: Passenger Cars lead at 66.8% share (~US$ 7.19 Bn); Commercial Vehicles grow fastest at 20.1% CAGR from California CARB Advanced Clean Trucks and Amazon and DHL 100,000+ unit electric LCV fleet procurement.

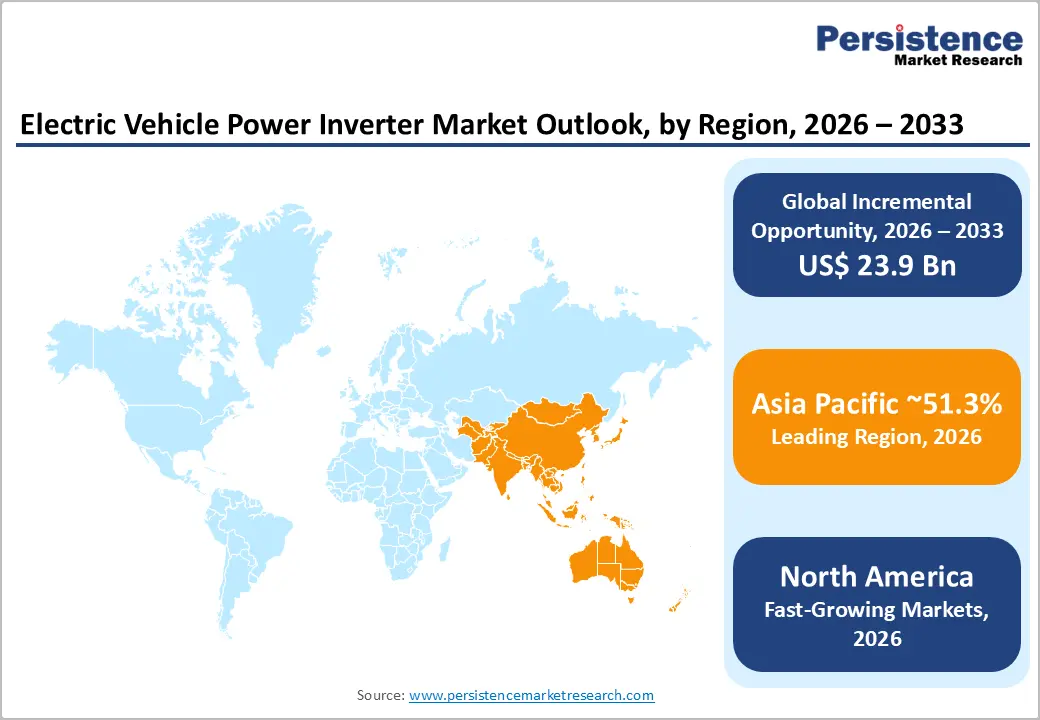

- Regional Leader: Asia Pacific leads at ~51.3% share (China US$ 4.1 Bn, India US$ 442.7 Mn) at 19.4% CAGR; Europe holds 23.7% share (Germany US$ 1.4 Bn); North America grows at 17.7% CAGR (U.S. US$ 2.0 Bn).

- Strategic Milestone: Vitesco-Schaeffler's €4.8 Bn EV powertrain merger (April 2025) and Bosch-Wolfspeed's 2 million EV inverter SiC supply agreement (September 2024) confirm vertical SiC integration and OEM consolidation as the defining competitive investment themes through 2033.

Market Dynamics Analysis

Drivers - Accelerating Global EV Adoption Backed by Government ZEV Mandates and OEM Electrification Commitments Generating Structural Inverter Demand

The IEA's Global EV Outlook 2025 confirmed over 17 million electric vehicles sold globally in 2024, a 25% YoY increase, with China accounting for 10.5 million units, Europe for 3.2 million units, and the United States for 1.7 million units (IEA, Global EV Tracker 2025), each EV unit requiring at minimum one traction inverter per driven axle, establishing a direct unit-to-inverter procurement multiplier that generates compounding demand as global EV fleet scale doubles.

The EU's binding zero-emission vehicle mandate for 2035 (EU Regulation 2023/851), requiring 100% of new car sales to be zero-emission, and California's Advanced Clean Cars II rule covering 17 U.S. states representing 40% of total U.S. new vehicle sales, collectively create a regulatory procurement floor ensuring sustained EV inverter demand growth independent of consumer preference cycles through 2033.

China's NEV credit mandate requiring automakers to maintain a minimum NEV credit ratio (MIIT, China NEV Credit Policy), combined with SAIC, BYD, and Geely's combined production of 8.7 million NEVs in 2024, is generating domestic inverter procurement at the world's largest single EV manufacturing base, where local inverter suppliers Innopower, BYD Semiconductor, and SVOLT are establishing vertically integrated power electronics supply chains at scale. The IEA projects the global EV fleet reaching 250 million units by 2030, representing an estimated US$ 85–100 Bn cumulative traction inverter procurement opportunity through 2030, demonstrating the structural market size trajectory underpinning the 18.2% CAGR forecast through 2033.

Silicon Carbide (SiC) Semiconductor Adoption in EV Inverters Driving Premium Performance Inverter Market Expansion

Silicon carbide-based EV power inverters, delivering switching frequencies 5–10x higher than IGBT silicon alternatives, enabling 10–15% extended driving range per charge cycle and 25–30% reduction in inverter heat generation at equivalent power output (Yole Intelligence, SiC Power Electronics in Automotive Report 2024), are transitioning from premium BEV-exclusive applications toward mainstream mass-market EV inverter architecture, with Tesla's Model 3 SiC inverter, BYD's Han EV SiC platform, and Toyota's next-generation FCEV SiC inverter establishing commercial adoption benchmarks.

SiC EV inverter penetration rate, estimated at 18% of global EV inverter shipments in 2024, is projected to reach 45–55% by 2030 (IDTechEx, Power Electronics Market Report) as SiC wafer production scaling at Wolfspeed, STMicroelectronics, and Infineon reduces SiC inverter module manufacturing cost by an estimated 40–50% between 2024 and 2028.

Toyota's investment of US$ 8 Bn in SiC semiconductor fabrication capacity and General Motors' SiC inverter collaboration with Wolfspeed for Ultium platform vehicles demonstrate the strategic capital commitment driving SiC inverter mainstream adoption, with SiC-based inverters commanding 20–35% premium ASP over IGBT equivalents while delivering system-level cost savings in thermal management, cooling system complexity, and battery capacity requirements that justify OEM specification upgrades across passenger car and commercial vehicle EV platforms globally.

Restraints - SiC Semiconductor Supply Chain Constraints and Substrate Wafer Availability Limiting High-Performance Inverter Production Scaling

Global SiC substrate wafer production capacity, concentrated at Wolfspeed (50%), Coherent (formerly II-VI, 20%), and STMicroelectronics (15%), faces structural supply tightness as automotive-grade SiC demand grows at 35–40% CAGR, with EV inverter OEM qualification lead times of 18–36 months from design-in to production ramp constraining high-performance inverter production capacity expansion velocity at automotive supply tiers globally. Wolfspeed's Q2 2025 production ramp delays and reported 12–18-month SiC wafer allocation backlogs at tier-1 automotive inverter suppliers demonstrate active supply-constraint risk, quantified at approximately 2–3 million EV-equivalent inverter production units affected through 2026.

EV Inverter Thermal Management Complexity and Automotive-Grade Certification Cycles Creating Competitive Entry Barriers and Program Delay Risks

EV traction inverter automotive-grade qualification under AEC-Q101 component standards and ISO 26262 functional safety certification requires 24–36 month development validation cycles, constraining new entrant time-to-revenue at automotive OEM qualification programs where incumbent inverter suppliers, including Bosch, Denso, and Mitsubishi Electric, maintain entrenched design-win positions. Thermal management failure, the most common EV inverter field failure mode, creates warranty claim exposure and recall risk quantified at US$ 800–US$ 2,500 per vehicle warranty incident at insufficient thermal interface material and liquid cooling system design, creating development program cost escalation risk at new inverter platform launch programs globally.

Opportunities - Commercial Vehicle EV Inverter Market Expansion Driven by Fleet Electrification Mandates and High-Power Above 600 kW Inverter Demand

Global electric commercial vehicle production, led by BYD eBus, Volvo Trucks, and Daimler Truck electric platforms, reached 2.1 million units in 2024 (International Energy Agency, Global EV Outlook 2025), with heavy commercial vehicle traction inverters requiring 301–600+ kW power output configurations at ASPs 3–8x higher than passenger car inverter equivalents, creating a premium high-power inverter market segment growing at 20.1% CAGR through 2033 with significant ASP leverage per vehicle. EU fleet decarbonization regulations, requiring 90% CO2 reduction for new heavy trucks by 2040 (EU Regulation 2024/1610), and California's CARB Advanced Clean Trucks rule covering 9 states, are generating structured fleet operator procurement commitments for electric HCV platforms that incorporate high-power SiC inverter systems valued at US$ 15,000–US$ 45,000 per truck inverter installation.

The commercial vehicle EV inverter addressable market is estimated at US$ 6.8–9.2 Bn by 2030, concentrated at BYD Commercial, Daimler Truck, Volvo Group, Navistar International, and Yutong-supplied fleet electrification programs in China, Europe, and North America, where high-power above 600 kW and 301–600 kW inverter segments represent the fastest ASP-growth tier of the global EV power inverter market.

Fuel Cell Electric Vehicle Inverter Market Emerging as Long-Range Zero-Emission Platform for Commercial and Infrastructure Applications

Hydrogen FCEV adoption, led by Toyota Mirai, Hyundai NEXO passenger platforms and Hyundai Xcient, Nikola, and IVECO hydrogen truck programs, is generating demand for specialized high-efficiency bidirectional inverters managing fuel cell stack power conditioning, regenerative braking energy recovery, and high-voltage DC bus management at power topologies distinct from battery-only BEV inverter architectures. Japan's "Green Innovation Fund" allocating US$ 18 Bn to hydrogen economy development (NEDO, 2024 Hydrogen Policy Report) and the EU's REPowerEU hydrogen strategy targeting 10 million tonnes of domestic green hydrogen production by 2030 are generating FCEV inverter technology investment at Toyota, Hyundai, Honda, and BMW FCEV platform development programs where FCEV-specific power inverter design-in contracts are estimated to reach US$ 1.8–2.6 Bn annually by 2030.

Category-wise Insights

Propulsion Type Analysis

Battery Electric Vehicles (BEV) lead the propulsion type segment with a 58.4% market share in 2026, estimated at approximately US$ 6.28 Bn, driven by BEV's dominant position as the highest-volume EV architecture globally, where each BEV requires a dedicated traction inverter per driven axle, with dual-motor AWD configurations requiring two inverters per vehicle, generating proportionally higher inverter procurement volume per unit above PHEV or FCEV alternatives that share electrical drive components with combustion or hydrogen fuel cell systems. BEV propulsion dominance reflects the technology and policy convergence around pure battery electric architecture, with IEA confirming BEV at approximately 75% of global EV sales mix in 2024, sustaining inverter market segment leadership. FCEV grows faster from a smaller base due to hydrogen policy investments, but BEV's scale advantage in global EV OEM production volumes sustains propulsion-type segment revenue leadership through 2033.

FCEV is the fastest-growing propulsion type, with a 21.1% CAGR through 2033. Japan NEDO Green Innovation Fund hydrogen investment, EU REPowerEU hydrogen strategy, commercial vehicle FCEV deployment targets, Toyota Mirai and Hyundai NEXO second-generation platform volume expansion, and hydrogen truck programs at Hyundai Xcient and Nikola collectively drive FCEV inverter market acceleration from a low base globally through 2033.

Power Output Analysis

Up to 100 kW inverters lead the power output segment with a 47.9% market share in 2026, estimated at approximately US$ 5.15 Bn, anchored by their volume dominance at mass-market passenger car BEV and PHEV applications where 80–100 kW single-motor front-wheel-drive configurations represent the most-deployed EV powertrain architecture globally, covering entry-level BEVs including Wuling Hongguang Mini EV, Renault Zoe, and Tata Nexon EV models that collectively represent the highest unit-volume EV production tiers across China, Europe, and India markets. Up to 100 kW segment leadership reflects the fundamental structure of global EV production mix, dominated by affordable compact urban BEVs where sub-100 kW inverter configurations satisfy application requirements at competitive manufacturing cost. Above 600 kW is growing fastest, but volume leadership at mass-market BEV configurations sustains up to 100 kW segment market revenue dominance through 2033.

Above 600 kW is the fastest-growing power output segment at 21.9% CAGR through 2033. Heavy commercial vehicle electrification mandates requiring 600 kW+ high-power SiC inverters across Daimler Truck, Volvo, BYD Commercial, and Nikola hydrogen HCV platforms, combined with high-performance BEV sports and hypercar 800V architecture adoption, drive rapid expansion of the above-600 kW inverter market at premium ASP tiers globally through 2033.

Vehicle Type Analysis

Passenger Cars lead the vehicle type segment with a 66.8% market share in 2026, estimated at approximately US$ 7.19 Bn, driven by the global EV market's structural concentration at passenger car platforms where China's 10.5 million EV sales, European passenger BEV volume, and U.S. Tesla, GM, and Ford EV production collectively generate the largest absolute inverter unit procurement pool globally at OEM production volumes exceeding 15 million passenger EV units annually in 2025 across all BEV, PHEV, and FCEV architectures. Passenger car dominance reflects the maturity of consumer BEV market formation in China and Europe, where established model lines and customer adoption cycles sustain high-volume inverter OEM procurement. Commercial vehicle EV inverter growth accelerates amid fleet mandate momentum, but passenger car's 15+ million-unit production scale sustains vehicle type segment revenue leadership through 2033.

Commercial Vehicles (LCV, HCV) are the fastest-growing vehicle type at 20.1% CAGR through 2033. EU 2040 zero-emission truck mandate, California CARB Advanced Clean Trucks regulation, Amazon and DHL last-mile electric LCV fleet procurement at 100,000+ unit scale, and China's NEV credit extension to commercial platforms collectively drive the commercial vehicle EV inverter market's rapid acceleration at high-power, premium ASP configurations globally through 2033.

Regional Market Insights

North America

North America is growing at a prominent 17.7% CAGR through 2033, holding approximately 19.8% of global Electric Vehicle Power Inverter Market share in 2026, estimated at approximately US$ 2.13 Bn, driven by the United States' IRA (Inflation Reduction Act) EV tax credit framework generating structurally supported EV demand, Tesla's vertically integrated SiC inverter production leadership, GM Ultium platform inverter procurement, and Ford Pro commercial EV fleet program expansion at North American OEM manufacturing operations.

U.S. Electric Vehicle Power Inverter Market: IRA-Supported BEV Demand, Tesla SiC Leadership, and Commercial Fleet Electrification

The United States holds approximately US$ 2.0 Bn in 2026, driven by IRA Section 30D EV consumer tax credits generating 1.7 million annual EV sales (IEA 2024), Tesla's 1.8 million global unit production requiring in-house SiC inverters, and GM Ultium Drives LLC inverter manufacturing at Ramos Arizpe, Mexico. NHTSA FMVSS safety standards and EPA Phase 3 GHG regulations sustain certified EV powertrain procurement requirements. Canada contributes through Stellantis Windsor and Honda Alliston EV production transitions and Volkswagen PowerCo battery facility supporting Ontario EV manufacturing.

North America's growth is sustained by IRA EV tax credit-driven BEV sales expansion, U.S. domestic SiC inverter manufacturing investment at Wolfspeed and onsemi, and commercial EV fleet electrification at Amazon, FedEx, and UPS, driving structured LCV inverter procurement through 2033.

Europe

Europe holds a 23.7% share of the global Electric Vehicle Power Inverter Market in 2026, estimated at approximately US$ 2.55 Bn, driven by the EU 2035 ICE ban regulatory mandate sustaining OEM electrification capex, premium EV platforms at BMW, Mercedes-Benz, and Audi specifying high-efficiency SiC inverter architectures, and Volkswagen Group's MEB platform inverter procurement across ID.3, ID.4, and Audi Q4 e-tron production volumes.

Germany Electric Vehicle Power Inverter Market: Premium OEM SiC Inverter Leadership, EU ZEV Mandate Compliance, and FCEV Investment

Germany holds approximately US$ 1.4 Bn in 2026, anchored by Bosch's EV inverter development at Reutlingen, Continental/Vitesco Technologies' traction inverter supply to VW Group and BMW, and ZF Friedrichshafen's EV drive systems. The U.K. sustains Jaguar Land Rover EV transition inverter procurement and Arrival commercial EV platform demand. France drives Valeo SiC inverter R&D for Stellantis and Renault. Spain expands through SEAT Cupra Born and SEAT MEB inverter supply chain investment. EU Ecodesign and functional safety standards shape inverter certification procurement.

Europe's EU 2035 ZEV mandate-driven OEM inverter capex, German Tier-1 SiC inverter manufacturing leadership at Bosch and Continental/Vitesco, and growing FCEV hydrogen truck inverter investment sustain above-average ASP inverter market revenue growth through 2033.

Asia Pacific

Asia Pacific is the fastest-growing and leading region, commanding approximately 51.3% of global Electric Vehicle Power Inverter Market share in 2025, driven by China's world-leading 10.5 million annual EV production generating the highest absolute inverter procurement volume, India's accelerating BEV adoption under FAME III policy, Japan's SiC and FCEV technology innovation at Toyota and Denso, and South Korea's Hyundai-Kia EV export platform inverter manufacturing at scale.

China Electric Vehicle Power Inverter Market: BEV Production Volume, FCEV Technology, and SiC Manufacturing Investment

China holds US$ 4.1 Bn in 2026, driven by BYD's 1.76 million NEV units produced in Q1 2025, CATL and BYD Semiconductor's SiC inverter vertical integration, and MIIT NEV mandate-driven OEM inverter procurement at SAIC, Geely, NIO, and Li Auto. India, at US$ 442.7 Mn, expands through Tata Motors Nexon EV and Punch EV production, FAME III subsidy, and Maruti Suzuki EV launch inverter procurement. Japan sustains Toyota Denso SiC FCEV inverter global leadership. South Korea contributes through the Hyundai-Kia Ioniq and EV9 platform inverter scale.

Asia Pacific's China BEV production volume inverter dominance, India FAME III-supported EV market acceleration, and Japan and South Korea SiC and FCEV inverter technology export leadership collectively sustain the region's leading market position through 2033.

Competitive Landscape

The global EV Power Inverter Market is moderately consolidated, with Robert Bosch, Denso, Mitsubishi Electric, Continental/Vitesco, and BorgWarner collectively holding approximately 45–52% of global EV inverter revenue, while Tesla's vertically integrated in-house inverter production, BYD Semiconductor's captive supply, and emerging SiC-specialized entrants are reshaping the competitive structure toward vertical integration and semiconductor technology differentiation. SiC topology expertise, automotive AEC-Q101 qualification pedigree, and OEM design-win platform exclusivity are primary competitive moats.

SiC inverter architecture development at 800V EV platforms, commercial vehicle high-power inverter qualification at HCV fleet electrification programs, FCEV-specific bidirectional inverter technology investment, and Asia Pacific OEM design-win expansion define the dominant strategic investment themes across global EV Power Inverter market participants through 2033.

Strategic Developments

- In February 2025, Denso Corporation launched its third-generation SiC traction inverter, achieving power density of 50 kW/L through advanced direct liquid cooling architecture, enabling 12% driving range extension versus second-generation units across Toyota and Lexus BEV and FCEV platforms scheduled for 2026–2027 model year production programs globally.

- In November 2024, BorgWarner Inc. announced a US$ 120 Mn capacity expansion at its Suzhou, China EV inverter manufacturing facility, adding SiC power module assembly and testing lines targeting BYD, NIO, and SAIC OEM supply programs, aligning with China's annual 10+ million NEV production volume growth trajectory through 2027.

- In September 2024, Bosch announced a technology partnership with Wolfspeed, securing a multi-year SiC wafer supply agreement for Bosch's EV power inverter SiC module production at Reutlingen, covering an estimated annual 2 million EV inverter SiC module equivalents targeting European OEM Tier-1 supply programs through 2030.

Companies Covered in Electric Vehicle Power Inverter Market

- Robert Bosch GmbH

- Denso Corporation

- Mitsubishi Electric Corporation

- Continental AG / Vitesco Technologies

- BorgWarner Inc.

- ZF Friedrichshafen AG

- Valeo SA

- Toyota Industries Corporation

- Hitachi Astemo Ltd.

- Marelli Corporation

- BYD Semiconductor Co., Ltd.

- Lear Corporation

- Tesla, Inc.

- Meidensha Corporation

- Eaton Corporation

Frequently Asked Questions

The market is valued at US$ 10.76 Bn in 2026, projected to reach US$ 34.69 Bn by 2033, delivering an incremental opportunity of US$ 23.93 Bn through 2033.

IEA-confirmed 17 million global EV sales in 2024 growing 25% YoY, EU 2035 ICE ban mandate, SiC-based inverter technology delivering 25–30% efficiency gains, and Asia Pacific's 51.3% dominant share led by China's 10.5 million annual NEV production are the primary structural growth drivers.

The market grows at a CAGR of 18.2% from 2026 to 2033, building on a historical CAGR of 15.6% from 2020 to 2026, reflecting compounding EV adoption and SiC inverter premiumization momentum.

The market grows at a CAGR of 18.2% from 2026 to 2033, building on a historical CAGR of 15.6% from 2020 to 2026, reflecting compounding EV adoption and SiC inverter premiumization momentum.

Commercial vehicle EV inverter addressable market of US$ 6.8–9.2 Bn by 2030 driven by EU HCV zero-emission mandates and FCEV-specific bidirectional inverter contracts estimated at US$ 1.8–2.6 Bn annually by 2030 through Japan and EU hydrogen vehicle programs represent the highest-value strategic opportunities.