- Automotive Components & Materials

- Automotive Powertrain Sensors Market

Automotive Powertrain Sensors Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Powertrain Sensors Market by Sensor Type (Temperature, Current, Position, Exhaust, Voltage, Speed, Torque, Pressure, and Others), Powertrain Subsystem (Engine, Drivetrain, and Exhaust), Vehicle Type (ICE Vehicles, Hybrid Vehicles, Electric Vehicles), and Regional Analysis for 2026 - 2033

Automotive Powertrain Sensors Market Size and Trends Analysis

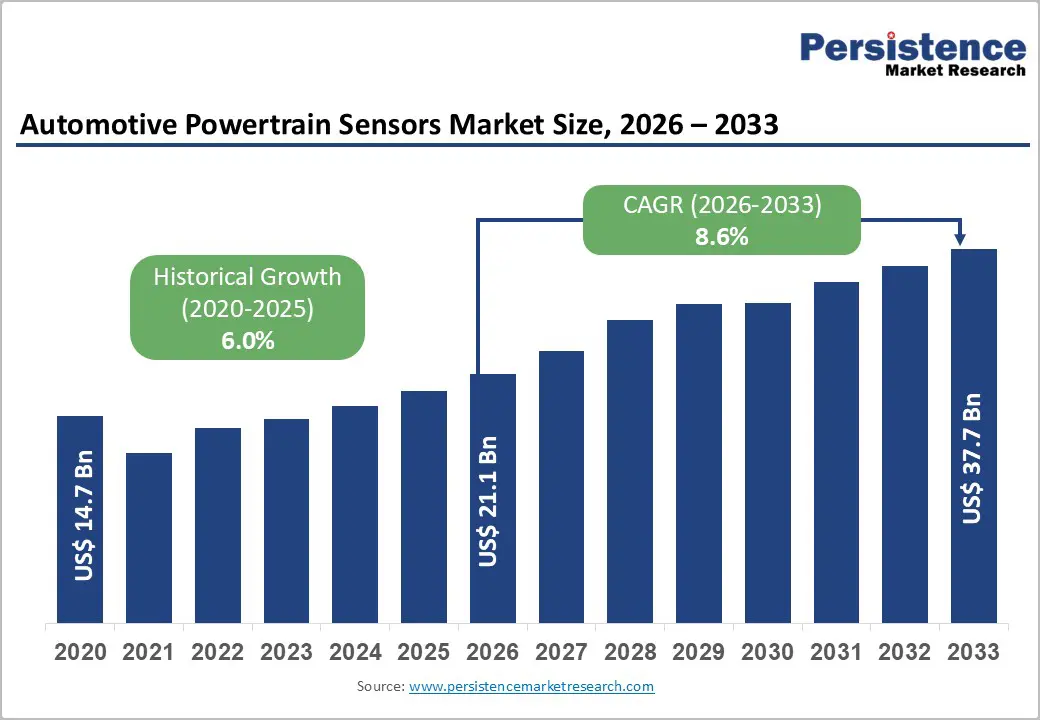

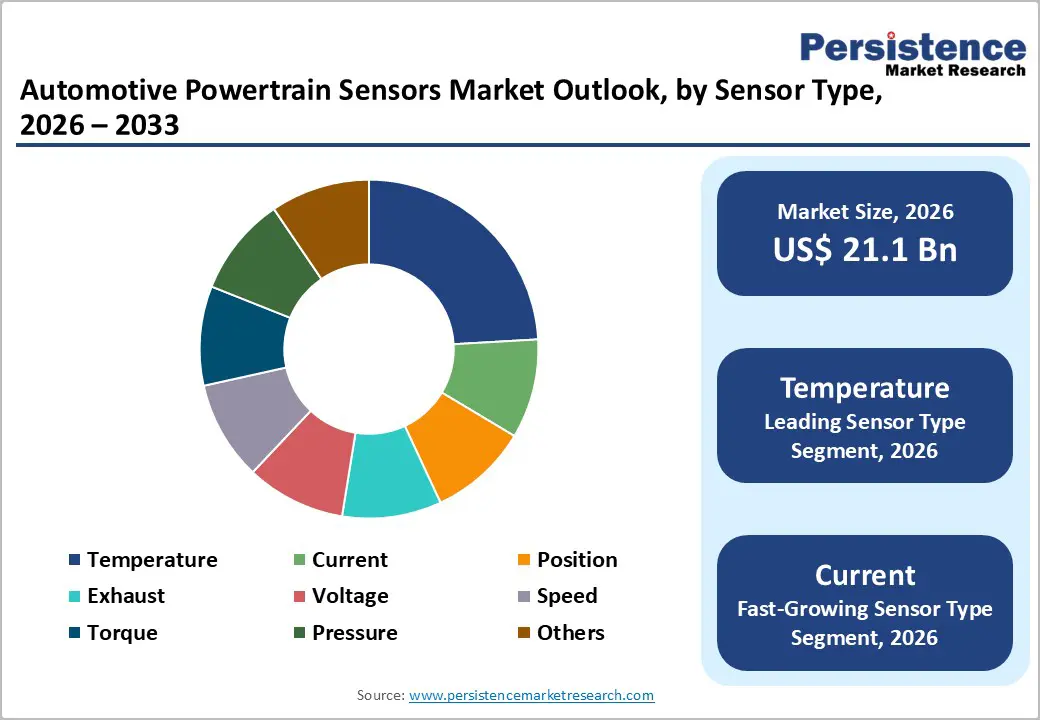

The global automotive powertrain sensors market size is likely to be valued at US$ 21.1 billion by 2026, with further expansion to US$ 37.7 billion by 2033, growing at a CAGR of 8.6% between 2026 and 2033.

The market's robust growth trajectory reflects the automotive industry's fundamental shift toward electrification, stringent emission compliance, and advanced powertrain management systems. Rising vehicle production volumes in developing economies, coupled with mandatory adoption of hybrid and electric powertrains, continue to accelerate sensor deployment across all powertrain subsystems. The convergence of regulatory mandates, technological innovation, and consumer demand for fuel-efficient and eco-friendly vehicles creates a compelling growth narrative for automotive powertrain sensors globally.

Key Industry Highlights:

- Regulatory-Driven Adoption: Stricter emission norms mandate real-time sensing, with regulations targeting 50% NOx reduction and 7.2 billion metric tons CO2 cuts globally.

- Compliance-Led Demand Surge: Regulatory compliance drives the greatest demand, directly linking rising stringency levels with higher sensor penetration across 100% OEM platforms.

- Cybersecurity Cost Pressure: Connected sensors increase data risks, raising compliance costs by 15-20%, particularly impacting small and mid-sized sensor manufacturers worldwide.

- V2X Opportunity Expansion: Smart mobility investments accelerate V2X adoption, boosting demand for high-accuracy sensors supporting autonomous functions, projected double-digit growth through 2033.

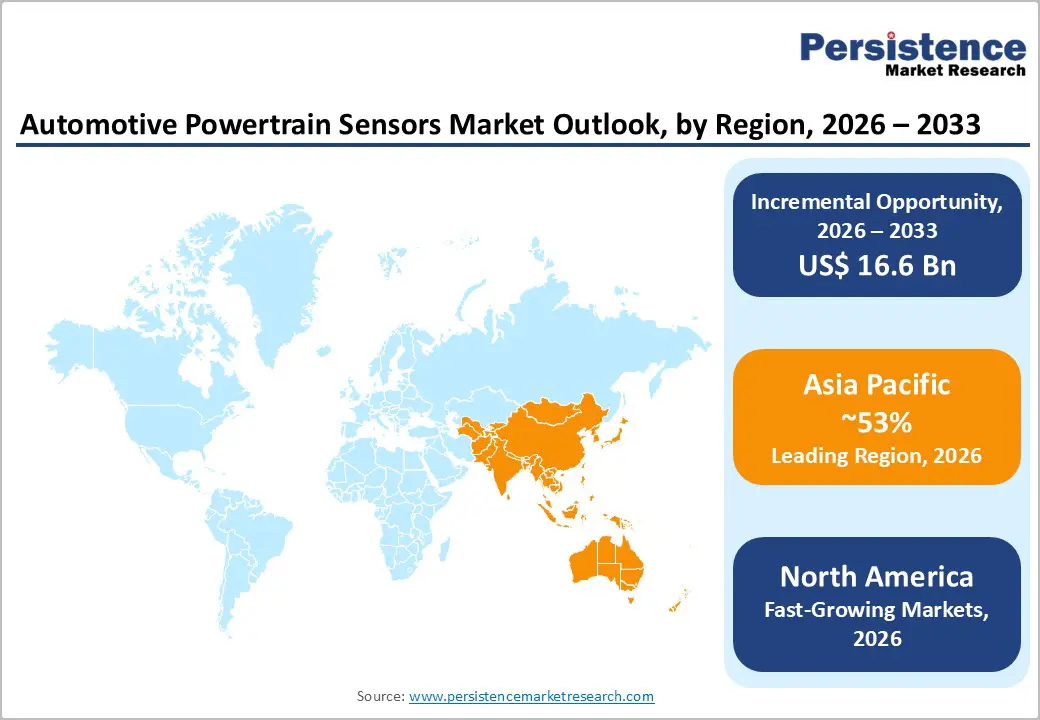

- Leading Region: Asia Pacific dominates with 53% market share, supported by large-scale vehicle production, EV incentives, and localized sensor manufacturing ecosystems.

- Temperature Sensor Leadership: Temperature sensors lead with 25%+ revenue share, driven by universal thermal monitoring needs across ICE, hybrid, and electric powertrains.

- Current Sensors Fastest Growth: Current sensors grow at 9.2% CAGR, fueled by rapid electrification and increasing complexity of EV battery and power management systems.

- Engine Subsystem Dominance: Engine-related sensors account for 40%+ revenue, reflecting continued ICE and hybrid reliance for emission compliance and fuel efficiency optimization.

- Hybrid Vehicles Growth Engine: Hybrid vehicles expand at 9.1% CAGR, requiring intensive sensor integration for dual powertrain coordination and energy management.

- North America Regulatory Boost: North America holds 15-18% share, with new emission standards driving higher sensor density and EV sensor demand growth post-2027.

| Key Insights | Details |

|---|---|

| Automotive Powertrain Sensors Market Size (2026E) | US$ 21.1 Bn |

| Market Value Forecast (2033F) | US$ 37.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.0% |

Market Dynamics

Drivers - Stringent Emission Regulations and Compliance Requirements

Government regulatory bodies worldwide are implementing increasingly strict emission standards that mandate real-time monitoring of vehicle exhaust and powertrain parameters. The EPA's Multi-Pollutant Emissions Standards for Model Years 2027-2032 target a 50% reduction in nitrogen oxides and particulate matter emissions, with cumulative carbon dioxide reductions projected at approximately 7.2 billion metric tons over the program's life. Similarly, the European Union's Regulation (EU) 2024/1257 consolidates and reinforces unified emission standards across member states, while India's Bharat Stage VI standards establish uniform compliance requirements across the subcontinent. These regulatory frameworks necessitate the integration of sophisticated temperature, pressure, and exhaust sensors to monitor combustion efficiency and after-treatment systems in real-time. Compliance-driven sensor adoption represents the single largest market driver, directly correlating regulatory stringency with sensor deployment volumes across original equipment manufacturers (OEMs).

Restraint - Data Privacy, Security, and Cybersecurity Concerns

The proliferation of connected sensors and vehicle-to-infrastructure communication systems generates massive volumes of sensitive operational and personal data. Automakers must prioritize cybersecurity protocols and data privacy compliance with evolving global regulations, including GDPR and emerging EV-specific cybersecurity standards, adding substantial compliance costs to sensor systems. Security breaches in sensor networks could compromise vehicle safety and operational integrity, creating liability exposure and regulatory penalties. These data protection requirements increase development timelines and manufacturing costs, particularly for small and mid-sized sensor manufacturers lacking dedicated cybersecurity infrastructure.

Opportunity - Connected, Localized, Data-Driven Automotive Sensor Growth Opportunities

The convergence of connected vehicle technologies, expanding automotive production in emerging economies, and the rise of data-driven services is creating a strong multi-dimensional opportunity for the automotive sensor market. The rapid development of Vehicle-to-Everything (V2X) communication ecosystems is increasing demand for real-time, high-accuracy sensor data to support traffic optimization, collision avoidance, and autonomous driving functions. As governments and municipalities invest in smart transportation infrastructure, OEMs are prioritizing sensor platforms capable of seamless communication with vehicles, infrastructure, and cloud systems, enabling suppliers to access premium, long-term contracts.

Simultaneously, accelerating vehicle manufacturing across the Asia Pacific-particularly in China, India, and Southeast Asia-is driving large-scale demand for powertrain, safety, and connectivity sensors. Localized manufacturing of sensors in these regions offers cost advantages, reduced supply-chain exposure, and faster OEM integration, supported by government incentives for EV and advanced mobility production. Emerging domestic suppliers are increasingly competitive, reshaping global sourcing strategies.

In parallel, the integration of sensors with cloud-based analytics is unlocking predictive maintenance and connected vehicle services. Continuous sensor data streams enable proactive fault detection, performance optimization, and lifecycle management, shifting value creation from one-time hardware sales to recurring digital service revenues while strengthening OEM-supplier partnerships.

Category-wise Analysis

Sensor Type Insights - Temperature Leadership and Electrification Driving Automotive Sensor Market Growth

Temperature sensors continue to dominate the automotive sensor landscape, accounting for more than 25% of total revenue across powertrain applications. Their leadership position is driven by their indispensable role in monitoring engine block temperatures, exhaust gas levels, and battery thermal conditions. Accurate temperature measurement is fundamental to optimizing fuel efficiency, ensuring emissions compliance, and maintaining operational safety across internal combustion engine (ICE), hybrid, and electric vehicle architectures. The universal requirement for thermal monitoring across virtually all vehicle subsystems ensures sustained demand, even as newer sensing technologies emerge. Their broad applicability, proven reliability, and cost-effectiveness reinforce temperature sensors as a foundational component of modern automotive systems.

In contrast, current sensors represent the fastest-growing segment, projected to expand at a robust CAGR of 9.2% through 2033. This rapid growth is closely linked to the accelerating shift toward vehicle electrification. Hybrid and electric vehicles require precise current measurement to support battery management systems, inverter performance optimization, and electric motor control. Current sensors enable real-time monitoring of power flow, early detection of thermal stress, and effective fault isolation within charging and propulsion systems. As EV and HEV platforms proliferate and powertrain architectures become more complex, demand for advanced current sensing solutions is expected to rise sharply, positioning this segment as a key growth driver for sensor manufacturers over the forecast period.

Powertrain Subsystem Insights - Engine Dominance and Rapid Drivetrain Growth

Within the powertrain subsystem landscape, engine-related sensing technologies continue to command market leadership, accounting for over 40% of total revenue. This dominance is closely tied to the sustained global presence of internal combustion engine (ICE) and hybrid vehicles, which depend heavily on advanced engine management systems for optimal performance. Engine subsystems deploy a combination of temperature, pressure, oxygen, and position sensors to precisely control fuel injection timing, air-fuel ratios, ignition, and exhaust gas recirculation. These sensors play a direct role in meeting stringent emission regulations, improving fuel efficiency, and ensuring consistent drivability, making them indispensable to OEMs even as electrification advances. Their ability to deliver immediate, measurable gains in efficiency and compliance continues to justify strong investment.

In contrast, the drivetrain subsystem represents the fastest-growing powertrain segment, projected to expand at a robust 9.4% CAGR. This growth reflects the rapid evolution of transmission and power delivery architectures, particularly in hybrid and electric vehicles. Modern drivetrains incorporate CVTs, dual-clutch transmissions, multi-speed automatics, and regenerative braking systems, all of which rely on high-precision torque, speed, and position sensors. As drivetrain complexity increases, sensor demand is rising faster than in the relatively mature engine segment, positioning drivetrain systems as a key future growth engine for the market.

Vehicle Type Insights - ICE Dominance and Hybrid Growth Reshape Automotive Powertrain Sensor Demand

Vehicle type dynamics continue to shape demand patterns within the automotive powertrain sensors market. Internal combustion engine (ICE) vehicles remain the dominant revenue contributor, accounting for more than 75% of market share. This leadership is supported by the vast global installed base, sustained production of conventional powertrains, and the slower pace of electrification in cost-sensitive emerging economies. Even as long-term growth moderates, ongoing platform refreshes, emission-compliance upgrades, and efficiency improvements sustain consistent sensor demand across fuel, exhaust, temperature, pressure, and engine management applications. As a result, ICE vehicles provide a stable baseline of volumes and predictable revenues for sensor suppliers.

In contrast, hybrid vehicles represent the fastest-growing segment, expanding at a projected CAGR of 9.1%. Hybrid architectures are inherently sensor-intensive, requiring precise coordination between internal combustion engines and electric motors. Advanced sensors are critical for battery state-of-charge monitoring, power split optimization, thermal management across dual power sources, and regenerative braking control. Positioned as a practical transition technology between ICE and full electrification, hybrids are increasingly offered across passenger cars, SUVs, and commercial vehicles. This broad applicability, combined with regulatory pressure to reduce emissions without full EV dependence, makes hybrids the primary growth driver for automotive sensor manufacturers.

Regional Insights and Trends

Asia Pacific Dominates Global Automotive Sensors Through Production Scale and Electrification

Asia Pacific holds a commanding position in the global automotive sensor market, accounting for over 53% of total revenue and representing the world’s largest automotive production hub. This leadership is underpinned by China’s scale as the largest vehicle and electric vehicle producer globally, Japan’s advanced automotive engineering and hybrid technology base, and India’s rapidly expanding vehicle manufacturing ecosystem. The region is expected to retain its dominant position through 2033, supported by sustained vehicle output growth and accelerating electrification across passenger and commercial segments.

China remains the cornerstone of regional performance, producing more than 26 million vehicles annually and capturing nearly 35% of Asia Pacific sensor demand. Its EV output reached approximately 9.5 million units in 2024, reinforcing its role as the global EV manufacturing leader. Japan contributes close to 20% of regional sensor demand through technologically advanced OEM platforms and strong hybrid vehicle penetration, while India is emerging as a high-growth market with annual vehicle production exceeding 4 million units and rapidly scaling EV capabilities.

Market expansion is driven by converging factors including strict government-led electrification timelines, cost-competitive and localized manufacturing ecosystems, and rising vehicle demand from growing middle-class populations in India and Southeast Asia. Regulatory clarity, emission norms, and targeted incentives continue to attract investment, positioning Asia Pacific as the global hub for cost-efficient, innovation-led automotive sensor development.

North America Sensor Market Reshaped by Emissions Regulations and EV Acceleration

North America represents approximately 15-18% of the global automotive sensor market, with the United States accounting for nearly 85% of regional demand. The region has long been characterized by advanced sensor specifications aligned with stringent emissions and vehicle safety requirements. A major inflection point is the introduction of the Environmental Protection Agency’s finalized Multi-Pollutant Emissions Standards for Model Years 2027-2032, the most significant regulatory shift in over two decades. These regulations directly mandate higher sensor penetration across all new vehicle platforms.

The requirement to achieve up to a 50% reduction in NOx emissions, alongside tighter particulate matter controls, compels OEMs to deploy advanced exhaust sensor arrays capable of real-time monitoring of catalyst efficiency, particulate filter regeneration, and aftertreatment system performance. This not only increases the number of sensors per vehicle but also drives replacement demand as existing platforms are re-engineered for compliance. The phased rollout between 2027 and 2032 provides suppliers with predictable timelines, enabling gradual capacity expansion and technology upgrades.

Simultaneously, EV adoption is accelerating, with North American production reaching around 1.3 million units in 2024. Market leadership from Tesla, alongside competitive responses from Ford Motor Company, General Motors, and Stellantis, is sustaining strong demand for EV-specific powertrain and thermal management sensors, reinforcing long-term regional growth.

Competitive Landscape

The automotive powertrain sensors market demonstrates a moderately consolidated competitive structure, with approximately 8-10 leading global manufacturers accounting for nearly 65-70% of total market share. This concentration is driven by high entry barriers, including stringent OEM qualification processes, long validation cycles, heavy capital investment in precision manufacturing, and strong intellectual property protection around advanced sensing technologies. Established players benefit from long-standing OEM relationships, economies of scale, and the ability to offer integrated, multi-sensor powertrain platforms covering engine, transmission, thermal, and emission control systems.

The market is broadly segmented into three competitive tiers. The first tier consists of global Tier-1 suppliers such as Bosch, Continental, Denso, Delphi, and Aptiv, which collectively command around 50-55% of global revenue through diversified portfolios and deep system-level integration capabilities.

The second tier comprises specialized technology leaders such as Sensata, TE Connectivity, and Amphenol Sensors, focusing on high-performance pressure, temperature, and position sensors. The third tier includes regional and emerging manufacturers, particularly from China and India, capturing 15-20% share through cost competitiveness and rising localization across high-volume vehicle programs.

Key Industry Developments

- July 29, 2025 - Magna Development: Magna expanded interior sensing adoption, securing or launching five OEM programs globally over 18 months, driven by ADAS regulations, as S&P Global projects 3.5× growth through 2032.

- June 2025 - Kistler Development: Kistler introduced the 4012A absolute pressure sensor for hydrogen applications, enabling reliable combustion engine and fuel-cell pressure monitoring, validated for high hydrogen resilience and optimized performance in hydrogen-powered powertrains.

- June 2025 - LEM Development: LEM launched a hybrid supervising unit integrating shunt and open-loop Hall technologies, delivering compact, cost-efficient, and high-safety current sensing solutions tailored for next-generation EV battery management systems.

Companies Covered in Automotive Powertrain Sensors Market

- Continental AG

- DENSO CORPORATION

- Infineon Technologies AG

- Mitsubishi Electric Mobility Corporation

- NXP Semiconductors

- Renesas Electronics Corporation

- Robert Bosch GmbH

- TE Connectivity

- Texas Instruments Incorporated

- Valeo SA

- Other Market Players

Frequently Asked Questions

The Automotive Powertrain Sensors market is estimated to be valued at US$ 21.1 Bn in 2026.

The primary demand driver for the automotive powertrain sensors market is the tightening of global emission and fuel-efficiency regulations, combined with the rapid shift toward electrified and hybrid powertrains. Governments across Europe, North America, China, and India are enforcing stricter standards such as Euro 6/7, China VI, and BS-VI, compelling OEMs to precisely monitor combustion efficiency, exhaust emissions, and energy consumption.

In 2026, the Europe region will dominate the market with an exceeding 35% revenue share in the global Automotive Powertrain Sensors market.

Among Powertrain Subsystem, the engine has the highest preference, capturing beyond 40% of the market revenue share in 2026, surpassing other powertrain subsystems.

Continental AG, DENSO CORPORATION, Infineon Technologies AG, Mitsubishi Electric Mobility Corporation, NXP Semiconductors, Renesas Electronics Corporation, and Robert Bosch GmbH. are a few leading players in the Automotive Powertrain Sensors market.