- Renewable Energy

- Wind Power Equipment Market

Wind Power Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Wind Power Equipment Market by Location (Offshore, Onshore), by Equipment (Blades, Control Systems, Gearboxes, Generators, Towers, Turbines, Others), by Regional Analysis, 2026 - 2033

Wind Power Equipment Market Size and Trend Analysis

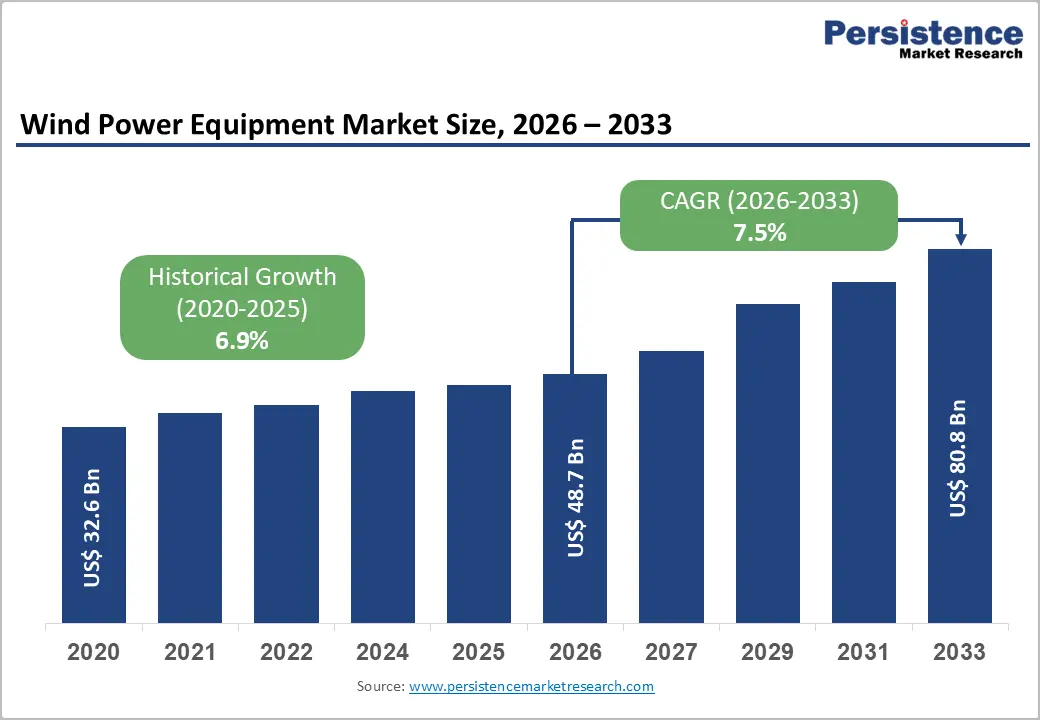

The global wind power equipment market size is expected to be valued at US$ 48.7 billion in 2026 and projected to reach US$ 80.8 billion by 2033, growing at a CAGR of 7.5% between 2026 and 2033. This sustained growth is anchored by national net-zero commitments driving unprecedented renewable energy capacity expansion, with the International Energy Agency (IEA) projecting wind power to supply over 35% of global electricity by 2050.

Surging offshore wind investment, next-generation turbine technology advancements, and government-mandated renewable energy targets across Europe, North America, and Asia Pacific are collectively creating the largest pipeline of wind equipment orders in history, underpinning robust market expansion through 2033.

Key Industry Highlights

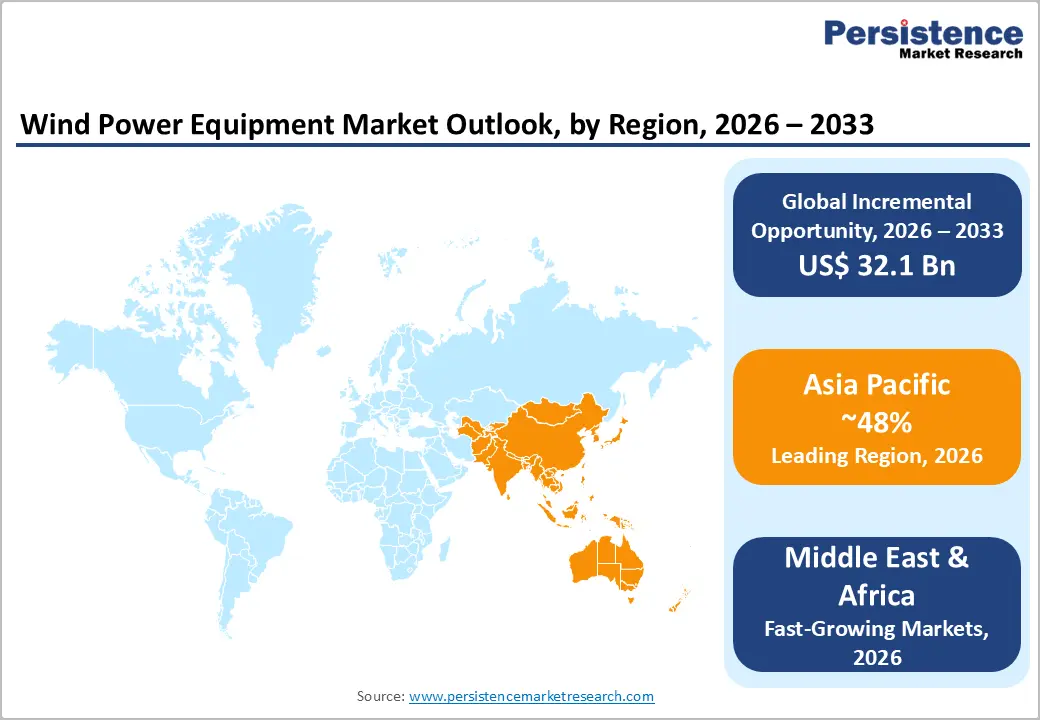

- Leading Region: Asia Pacific holds 48% of the global Wind Power Equipment market in 2025, dominated by China's 440+ GW installed fleet and 70-80 GW annual additions, supported by Indian and Southeast Asian market expansion driving sustained record-level equipment procurement volumes.

- Fastest Growing Region: Middle East & Africa is the fastest-growing region with 10.2% CAGR through 2026 - 2033, driven by ambitious renewable energy diversification programs in Saudi Arabia, UAE, South Africa, and Morocco, creating rapidly expanding wind equipment demand across the region.

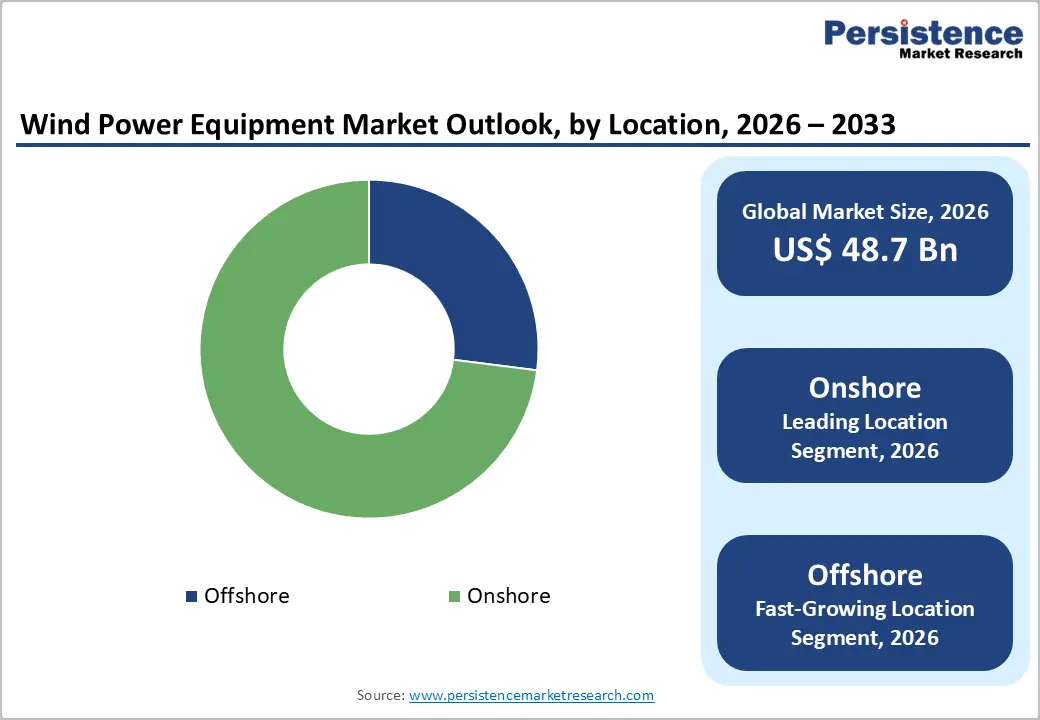

- Dominant Location Segment: Onshore holds 73% market share in 2025, reflecting its cost-competitiveness with LCOE as low as US$ 25-50/MWh per IEA data, making it the world's cheapest new power generation source and sustaining the highest volume of equipment deployments globally.

- Fastest Growing Location Segment: Offshore is the fastest-growing location segment (2026 - 2033), driven by GWEC-projected growth to 380 GW by 2032, next-generation 12-20 MW turbine platforms requiring premium high-value equipment, and floating offshore wind technology unlocking deep-water markets globally.

- Key Market Opportunity: WindEurope-estimated 15 GW European repowering need through 2030, DOE-identified 10+ GW U.S. repowering pipeline, and India's MNRE 140 GW wind target collectively represent the highest-certainty, near-term equipment demand growth opportunities for wind OEMs and component suppliers through 2033.

Market Dynamics

Drivers - Global Net-Zero Commitments and Renewable Energy Targets Driving Record Wind Capacity Additions

National and regional net-zero carbon commitments represent the most powerful structural driver of the global Wind Power Equipment market, creating policy-backed, multi-decade demand certainty for turbine manufacturers, component suppliers, and developers. As of 2024, over 140 countries have submitted nationally determined contributions (NDCs) under the Paris Agreement that explicitly include wind energy expansion targets.

The International Energy Agency (IEA) in its World Energy Outlook 2023 projects that wind capacity must grow to over 8,000 GW by 2050 to achieve net-zero scenarios, requiring annual capacity additions of over 300 GW from 2030 onward. In 2023, global wind installations reached a record 117 GW per Global Wind Energy Council (GWEC) data, the highest single-year addition in history. This policy-backed volume demand translates directly into equipment orders for turbines, blades, towers, generators, and control systems across both onshore and offshore segments, creating the largest and most sustained equipment procurement cycle in the industry's history.

Off-shore Wind Expansion and Next-Generation Turbine Scaling Driving Premium Equipment Demand

The rapid global expansion of offshore wind, driven by superior wind resources, reduced land-use conflict, and increasingly cost-competitive project economics, is generating high-value equipment demand as turbines scale to unprecedented sizes. According to the Global Wind Energy Council (GWEC), offshore wind installations reached approximately 10.8 GW in 2023, with Europe and China leading global deployment.

Next-generation offshore turbine platforms, including Siemens Gamesa's SG 14-236 DD and GE Vernova's Haliade-X 14 MW, feature rotor diameters exceeding 200 meters, requiring correspondingly advanced blades, towers, generators, and drivetrain systems that command substantially higher per-unit equipment revenues. The European Union has set an offshore wind target of 300 GW by 2050 under the EU Offshore Renewable Energy Strategy, while the U.S. Bureau of Ocean Energy Management (BOEM) has leased substantial offshore areas targeting 30 GW by 2030, both creating enormous pipeline demand for high-value offshore wind equipment through the forecast period.

Restraints - Supply Chain Bottlenecks and Critical Material Constraints

The wind power equipment market faces significant supply chain challenges, including shortages of key raw materials, notably rare earth elements for permanent magnet generators, high-grade steel for towers, and specialized composites for blades. The IEA has flagged that demand for rare earth elements could increase by over 4x by 2040 in net-zero scenarios, creating potential supply bottlenecks.

Blade manufacturing capacity constraints, port infrastructure limitations for offshore equipment handling, and specialized installation vessel shortages have caused project delays and cost overruns for several major offshore wind programs in Europe and North America, constraining the pace of market expansion relative to stated policy ambitions.

Permitting Delays and Grid Integration Challenges Slowing Installation Timelines

Complex and lengthy permitting processes, particularly for offshore wind and large onshore wind projects, represent a structural restraint on wind equipment market growth, creating pipeline delays that defer equipment demand. In the United States, the American Clean Power Association (ACP) has repeatedly identified permitting reform as the single most critical enabler of clean energy deployment, with average onshore wind project permitting timelines extending to 4-7 years in several states.

Concurrently, grid transmission capacity constraints in key markets, including Germany, the U.S. Midwest, and parts of India, limit the operational commissioning of completed wind projects, dampening realized equipment installation rates relative to capacity targets.

Opportunities - Offshore Wind as the Fastest-Growing Segment Offering Highest Revenue per Installation

Offshore wind represents the fastest-growing location segment within the Wind Power Equipment market, offering the highest per-unit equipment revenue opportunity as turbine sizes scale to 12-20 MW rated capacities in next-generation platforms. The GWEC projects that offshore wind capacity will reach approximately 380 GW globally by 2032, with particularly high growth rates in Europe, the U.S., and Asia Pacific. Emerging offshore wind markets, including Japan, South Korea, India, Brazil, and Southeast Asia, are establishing regulatory frameworks and auction pipelines that are beginning to translate into equipment procurement demand.

Floating offshore wind (FOW) technology is a critical emerging frontier, enabling wind energy deployment in deep-water sites far exceeding the reach of fixed-foundation technology. The European Commission's Offshore Renewable Energy Strategy explicitly targets 7 GW of floating offshore wind by 2030, with Scotland, Norway, and Portugal leading early commercial development. Equipment suppliers investing in FOW-specific component design, including purpose-built floating foundations, dynamic cable systems, and specialized turbine platforms, are positioned to capture significant first-mover advantages in this technically demanding, high-margin emerging segment.

Emerging Market Wind Energy Expansion and Repowering of Aging Onshore Fleet

Two structurally distinct but complementary opportunity streams are expanding the Wind Power Equipment market beyond its traditional base: the rapid acceleration of wind energy deployment in emerging markets, and the beginning of a multi-decade onshore repowering cycle in mature markets. In emerging markets, India's National Wind-Solar Hybrid Policy and Ministry of New and Renewable Energy (MNRE) targets of 500 GW of renewable capacity by 2030 are creating a large and rapidly growing equipment procurement market, with annual onshore wind tenders exceeding 10 GW.

In mature markets, thousands of first-generation wind turbines installed in the 1990s and 2000s are approaching end-of-life, creating an enormous repowering opportunity. WindEurope estimates that approximately 15 GW of European wind capacity will require repowering through 2030, while the U.S. Department of Energy (DOE) identifies over 10 GW of U.S. installed capacity requiring near-term repowering. Each repowering project requires entirely new turbine, blade, tower, and drivetrain equipment, generating revenues comparable to new-build installations while leveraging existing grid connections and site permits.

Category-wise Analysis

Location Insights

Onshore leads the Location category with an estimated 73% market share in 2025, reflecting its status as the mature, cost-established, and volume-dominant wind energy deployment pathway globally. Onshore wind has achieved cost parity, and in many markets, cost leadership, among all power generation technologies. The IEA reports that onshore wind delivered levelized costs of electricity (LCOE) as low as US$ 25-50/MWh in best-resource markets in 2023, making it the cheapest new electricity generation source in most of the world.

China, the world's largest wind market, continues to install onshore capacity at multi-gigawatt annual rates, while India, the U.S., and parts of Latin America and Africa are scaling rapidly. Offshore is the fastest-growing location segment, driven by policy mandates in Europe, the U.S., and Asia Pacific, and by next-generation turbine platforms enabling higher capacity factors that increasingly justify the higher capital costs of offshore installation and operations.

Equipment Insights

Turbines lead the Equipment category with approximately 52% market share in 2025, as turbines represent the highest-value single component in any wind power installation, encompassing the nacelle assembly, drivetrain, and electrical systems that collectively convert wind energy into grid-ready electricity. Turbine prices for onshore wind in Europe averaged approximately EUR 0.8-1.0 million per MW in recent years, with offshore turbine platforms commanding substantially higher per-unit values.

Turbine supply is dominated by a concentrated group of global original equipment manufacturers (OEMs), including Vestas, Siemens Gamesa, GE Vernova, Enercon, Nordex, and Goldwind, which maintain competitive advantage through proprietary technology platforms, global service networks, and long-term service agreements. Blades are the fastest-growing equipment segment, driven by the escalating length requirements of next-generation turbines, with offshore blades now exceeding 100 meters, creating significant incremental material and manufacturing investment requirements for the supply chain.

Regional Insights

Asia Pacific leads the global Wind Power Equipment market with approximately 48% of total market share in 2025 while Middle East & Africa is the fastest-growing region, expanding at an estimated CAGR of approximately 10.2% through 2033.

North America Wind Power Equipment Market Trends and Insights

North America is a large and rapidly growing wind equipment market, driven by the U.S. Inflation Reduction Act (IRA)'s expanded production tax credits and investment tax credits for wind energy. The IRA has catalyzed a wave of new domestic wind equipment manufacturing investment, reshaping supply chain dynamics. Canada's offshore wind ambitions on the Atlantic coast are emerging as a meaningful new demand driver.

U.S. Wind Power Equipment Market Size

The U.S. accounts for approximately 88% of North American wind equipment demand, with an estimated regional market share of 12% of global total in 2025. The American Clean Power Association (ACP) reports over 147 GW of installed U.S. wind capacity as of 2024, with the IRA targeting 300 GW by 2030, creating one of the world's largest active equipment procurement pipelines.

Europe Wind Power Equipment Market Trends and Insights

Europe is the global leader in offshore wind development and remains a dominant onshore market, driven by the EU REPowerEU plan targeting 510 GW of wind capacity by 2030. WindEurope reports record European wind installations in 2023 and growing momentum in Germany, the U.K., France, and Scandinavia. Supply chain scaling and grid investment remain critical enablers for achieving stated targets.

Germany Wind Power Equipment Market Size

Germany holds approximately 22% of European wind equipment demand, with over 66 GW of installed capacity as of 2024 per Bundesnetzagentur. Germany's Renewable Energy Sources Act (EEG 2023) sets a target of 115 GW of onshore wind by 2030, requiring sustained equipment procurement investment throughout the forecast period.

U.K. Wind Power Equipment Market Size

The U.K. is Europe's offshore wind leader, with approximately 16% of European share driven by over 14 GW of installed offshore capacity. The Crown Estate's ScotWind and Round 4 leasing rounds have allocated over 35 GW of new offshore capacity, creating a generation-defining equipment procurement pipeline extending well beyond 2033.

France Wind Power Equipment Market Size

France represents approximately 10% of European wind equipment demand, with installed capacity exceeding 22 GW onshore. France's multi-annual energy plan targets significant acceleration of both onshore and offshore wind deployment, with its first commercial offshore wind farm commissioned in 2022. Growing floating offshore wind ambitions in the Mediterranean and Atlantic are creating new equipment demand horizons.

Asia Pacific Wind Power Equipment Market Trends and Insights

Asia Pacific dominates the global wind power equipment market, led by China with over 440 GW of installed capacity and annual additions consistently exceeding 70-80 GW. China's domestic turbine manufacturers, including Goldwind, Ming Yang, Envision, and Guodian United Power, supply the majority of domestic demand. India, Japan, and Southeast Asia are rapidly expanding their wind equipment markets.

India Wind Power Equipment Market Size

India accounts for approximately 14% of Asia Pacific wind equipment demand (excluding China) in 2025, with over 45 GW of installed capacity. India's MNRE targets 140 GW of wind capacity by 2030, with annual tenders exceeding 10 GW creating sustained equipment procurement demand. Vestas, Siemens Gamesa, and domestic suppliers compete actively in the Indian market.

Japan Wind Power Equipment Market Size

Japan represents approximately 6% of regional market share, with installed capacity of approximately 5.2 GW. Japan's ambitious offshore wind pipeline, targeting 45 GW by 2040 under its Act on Promoting Utilization of Sea Areas, is creating large forward equipment demand, particularly for offshore turbines, foundations, and specialized installation systems in the world's most challenging marine environment.

Southeast Asia Wind Power Equipment Market Size

Southeast Asia accounts for approximately 5% of Asia Pacific market share but is one of the fastest-growing sub-regions, with Vietnam, the Philippines, Thailand, and Indonesia all developing wind energy pipelines. Vietnam leads regional deployment with approximately 4.6 GW of installed capacity, and new offshore wind auction frameworks are expected to unlock significant incremental equipment demand at an estimated CAGR of approximately 12% through 2033.

Competitive Landscape

The global wind power equipment market is moderately consolidated at the turbine OEM level, with a small group of large manufacturers accounting for the majority of global supply. In contrast, the upstream component segment, including blades, towers, and gearboxes, remains relatively fragmented with numerous regional suppliers.

Competitive positioning is primarily driven by technological advancement, turbine efficiency, and the ability to deliver large-scale offshore and onshore solutions. Scale of operations, global service networks, and strong after-sales maintenance capabilities are critical for securing long-term contracts with utilities and independent power producers. Manufacturers are increasingly focusing on next-generation high-capacity turbines exceeding 15 MW, particularly for offshore applications, while also investing in floating wind technologies to unlock deeper water installations.

Localization of supply chains and cost optimization strategies are gaining importance amid rising raw material and logistics pressures. Long-term operations and maintenance contracts are also becoming a key revenue stabilizer, enhancing lifecycle value creation for OEMs.

Key Developments

- April 2026: Suzlon Energy launched its new “Blue Sky” wind turbine platform in Europe, introducing high-capacity 5 MW and 6.3 MW models to strengthen its presence in the region’s repowering and new wind energy project market.

- February 2026: Vayona Energy secured its first India order to supply 64.8 MW of wind turbines to Oyster Renewable Energy for a project in Kadapa, Andhra Pradesh, marking its entry into the Indian wind equipment market following its Siemens Gamesa acquisition.

- April 2025: Vestas Wind Systems A/S secured a 1.4 GW order for its V172-7.2 MW onshore turbines across multiple European markets, representing one of the company's largest single-year order tranches and reflecting accelerating demand driven by EU REPowerEU renewable energy targets.

Wind Power Equipment Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 32.6 Billion |

| Current Market Value (2026) | US$ 48.7 Billion |

| Projected Market Value (2033) | US$ 80.8 Billion |

| CAGR (2026 - 2033) | 7.5% |

| Leading Region | Asia Pacific, 48% market share (2025) |

| Dominant Location | Onshore, 73% market share (2025) |

| Top-ranking Equipment | Turbines, 52% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 32.1 Billion |

Companies Covered in Wind Power Equipment Market

- Vestas Wind Systems A/S

- Siemens Gamesa Renewable Energy

- Enercon GmbH

- Envision Energy

- GE Vernova (General Electric Renewable Energy)

- Guodian United Power Technology Company Limited

- Ming Yang Wind Power Group Limited

- Senvion S.A.

- Nordex SE

- Xinjiang Goldwind Science & Technology Co., Ltd.

- Suzlon Energy Limited

- Windworld A/S

- CSSC Haizhuang Wind Power (China Shipbuilding)

Frequently Asked Questions

The global wind power equipment market is estimated at US$ 48.7 billion in 2026, with strong growth projected to reach US$ 80.8 billion by 2033.

Key drivers include global net-zero targets, rising renewable capacity additions, and large-scale offshore wind expansion projects.

Asia Pacific leads with around 48% share, driven by large installations in China and strong growth in India’s wind capacity.

Major opportunities lie in offshore wind expansion and large-scale turbine repowering projects across mature markets.

Key players include Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy, GE Vernova, Enercon GmbH, Nordex SE, Xinjiang Goldwind Science & Technology Co. Ltd., Ming Yang Wind Power Group, Envision Energy, Guodian United Power Technology, and Suzlon Energy Limited.