- Sporting Goods & Equipment

- Electric Drill Market

Electric Drill Market Size, Share, and Growth Forecast 2026 - 2033

Electric Drill Market by Product Type (Hammer Drills, Impact Drills, Rotary Drills, Others), Power Source (AC Powered, Battery/DC Powered, Others), Price Range (Mass, Premium Range), Application (Residential / DIY, Commercial / Professional, Industrial, Automotive, Mining & Infrastructure), Sales Channel (Supermarkets/Hypermarkets, Specialty Tool Stores, Hardware Stores, E-commerce Marketplaces, Branded Online Stores), and Regional Analysis, 2026 - 2033

Electric Drill Market Size and Trend Analysis

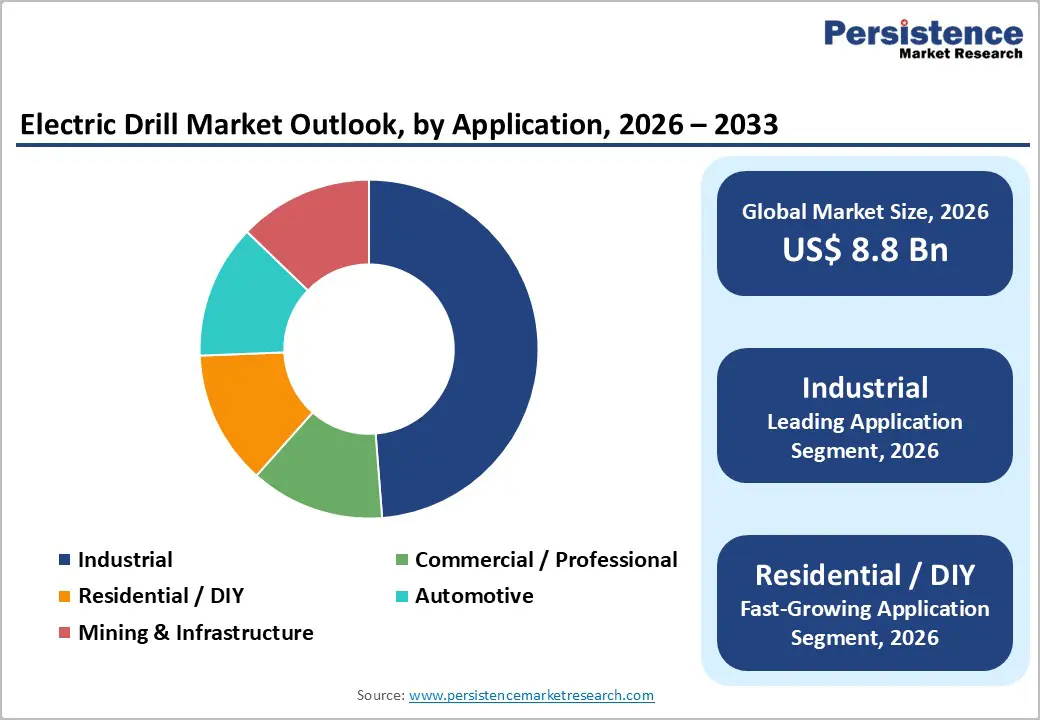

The global electric drill market size is expected to be valued at US$ 8.8 billion in 2026 and projected to reach US$ 11.8 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

The market demonstrates resilient expansion driven by three primary catalysts: the acceleration of do-it-yourself home improvement activities facilitated by digital tutorials and social platforms, the continuous modernization of construction infrastructure globally, with spending expected to exceed US$ 16 trillion by 2030, and breakthrough advancements in battery technology particularly lithium-ion systems that extend operational duration and enhance portability. The convergence of affordable residential projects priced under $5,000 and professional-grade cordless capabilities positions electric drills as indispensable tools across multiple application segments.

Key Industry Highlights

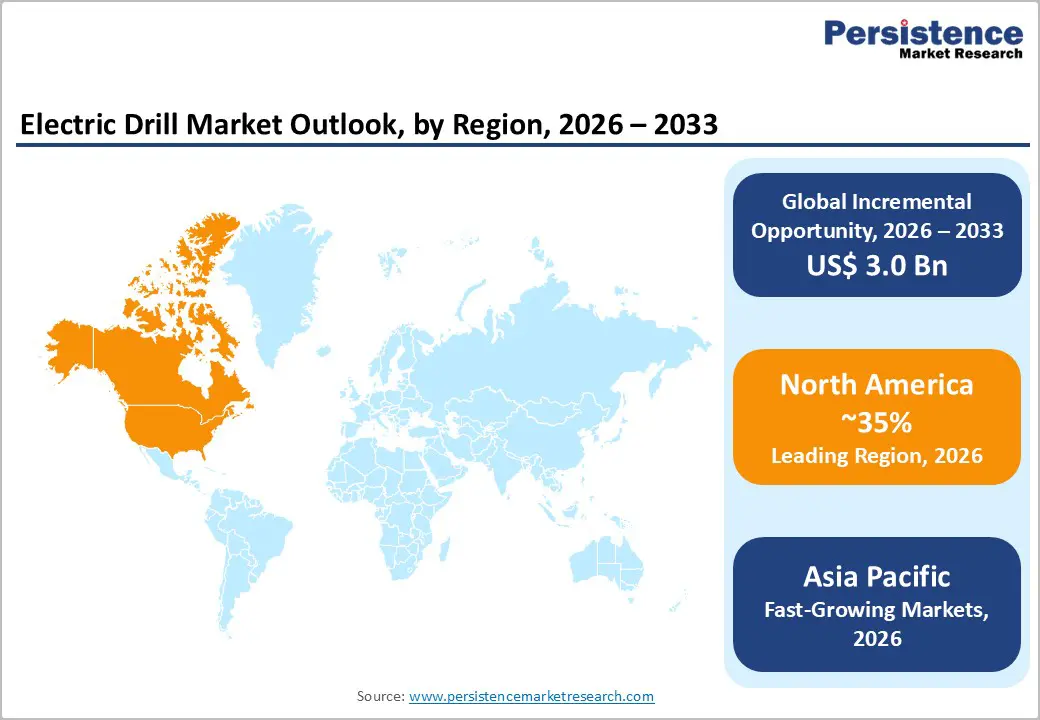

- Leading Region: North America leads the global electric drill market with around 35% share in 2025, supported by strong DIY adoption, high construction spending, extensive retail networks, and infrastructure-led demand concentrated in the United States.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expanding at a projected 6.9% CAGR through 2033, driven by large-scale construction in China, infrastructure modernization in India, rapid urbanization, and rising middle-class tool adoption.

- Dominant Segment: Battery/DC powered drills dominate with nearly 58% market share in 2025, while hammer drills lead by product type due to their versatility in masonry and construction-intensive professional applications.

- Fastest Growing Segment: The residential and DIY segment is projected to grow at 5.8% CAGR through 2033, fueled by increasing home improvement activity, digital learning platforms, and homeowner preference for renovation over relocation.

- Key Market Opportunity: Advancements in battery technology and smart tool integration present major growth opportunities by enabling higher energy efficiency, connected workflows, and platform-based ecosystems that support premium positioning and long-term customer retention.

| Key Insights | Details |

|---|---|

|

Electric Drill Market Size (2026E) |

US$ 8.8 billion |

|

Market Value Forecast (2033F) |

US$ 11.8 billion |

|

Projected Growth CAGR (2026-2033) |

4.3% |

|

Historical Market Growth (2020-2025) |

3.2% |

Market Dynamics

Drivers - Surging DIY Culture and Home Renovation Expenditure

The proliferation of do-it-yourself home improvement culture represents a transformational force propelling electric drill adoption across residential segments. Home improvement spending reached approximately $509 billion in 2025 according to the Joint Center for Housing Studies of Harvard University, with over 60% of homeowners actively undertaking DIY projects to mitigate contractor expenses. Digital platforms, including YouTube and social media channels, democratize technical knowledge, enabling consumers to confidently execute furniture assembly, wall installations, and minor repairs independently.

The median household expenditure on renovations was maintained at $20,000 annually through 2024, with light-duty electric drills operating at voltages below 20 volts experiencing particularly robust demand. This behavioral shift correlates strongly with elevated mortgage rates exceeding 6% that incentivize homeowners to invest in property enhancement rather than relocation, thereby sustaining continuous demand for versatile drilling equipment.

Infrastructure Modernization and Construction Industry Expansion

Global construction market expansion provides substantial momentum for electric drill demand, with industry valuation projected to increase from US$ 11.39 trillion in 2024 to US$ 16.11 trillion by 2030, according to Deloitte. Infrastructure investments focus on transportation networks, renewable energy installations, and urban development projects, particularly in emerging economies undergoing accelerated urbanization. Government initiatives, such as the Infrastructure Investment and Jobs Act in the United States, allocated substantial funding to public works, while construction output in India is projected to grow at 6.2% annually through infrastructure development.

The construction sector demonstrates consistent demand for professional-grade hammer drills and rotary equipment capable of penetrating masonry, concrete, and hardened materials. Additionally, the automotive manufacturing renaissance, with electric vehicle sales reaching 1.56 million units, representing 10% of light-duty vehicle sales in 2024, generates parallel demand for precision fastening and assembly tools essential for production line operations.

Restraints - Raw Material Price Volatility and Supply Chain Disruptions

The electric drill manufacturing sector confronts persistent challenges from fluctuating raw material costs, particularly for lithium-ion battery components, steel, aluminum, and electronic circuitry essential for modern cordless designs. Global construction cost inflation averaged 4.15% in 2024, with material price escalation directly impacting production economics. Geopolitical tensions, including the U.S.-China trade confrontations introduce tariff uncertainties and export restrictions that elevate procurement expenses and create logistical delays.

Supply chain bottlenecks during economic recoveries reduced component availability, compelling manufacturers to maintain elevated inventory levels or accept margin compression. These cost pressures translate to higher retail prices that potentially constrain purchase decisions among price-sensitive consumer segments and small-scale contractors operating on constrained budgets.

Market Saturation in Developed Economies and Competitive Intensity

Mature markets across North America and Western Europe exhibit high penetration rates where households already possess multiple power tool units, limiting incremental demand to replacement cycles and specialized applications. The market demonstrates extreme fragmentation with numerous established brands, including Stanley Black & Decker, Robert Bosch GmbH, and Makita Corporation, alongside countless regional manufacturers competing aggressively on pricing, features, and distribution access. This competitive saturation compresses profit margins and necessitates substantial research and development investments to differentiate products through incremental innovations.

Furthermore, the extended product lifecycles of quality drills, often exceeding five to seven years, decelerate repurchase frequency. Economic headwinds, including persistent inflation and fluctuations in consumer confidence, lead to project postponements; 80% of homeowners report budget overruns exceeding $500 for renovation activities, prompting more cautious spending.

Opportunities - Battery Technology Innovation and Smart Tool Integration

The evolution of battery technology presents transformative opportunities for market participants to capture premium segments through enhanced value propositions. Lithium-ion batteries currently dominate the market, with over 75% market adoption, yet emerging solid-state battery architectures promise superior energy density, faster charging, and longer service lifetimes. Leading manufacturers, including Robert Bosch GmbH invested approximately USD 8.89 billion in research and development during 2024, advancing features such as Bluetooth connectivity, artificial intelligence-driven adaptive speed control that automatically modulates torque based on material resistance, and integration with Internet of Things ecosystems for inventory tracking and predictive maintenance alerts.

Techtronic Industries recorded USD 14.6 billion in sales during 2024, leveraging smart tool ecosystems that consolidate multiple devices under unified battery platforms. Companies pioneering sustainable manufacturing approaches, with Stanley Black & Decker targeting 50% recycled stainless steel content by 2025 and Bosch utilizing 56% recycled steel and 35% recycled aluminum, position themselves favorably as environmental consciousness influences purchasing criteria across demographic segments.

Emerging Market Penetration and E-commerce Channel Expansion

Developing economies across the Asia Pacific, Latin America, and Middle East & Africa regions represent substantial untapped demand reservoirs characterized by expanding middle classes, accelerating urbanization trajectories, and nascent DIY adoption patterns. The Asia-Pacific power tools market is projected to grow at a 7.61% CAGR, driven by China’s manufacturing modernization initiatives and India’s Make in India incentive programs, which are attracting domestic and foreign original equipment manufacturers. Rising disposable incomes, coupled with increasing awareness of power tool benefits through digital media exposure, catalyze initial purchase occasions among first-time buyers.

Simultaneously, e-commerce platforms exhibit explosive growth with online channels demonstrating 10.1% CAGR as manufacturers implement direct-to-consumer strategies that reduce intermediary costs and enable personalized customer engagement. Amazon commands approximately 13% of the marketplace share in the power drill category, while branded online stores offer subscription services, extended warranties, and educational content that enhance customer lifetime value. The convergence of affordable entry-level products targeting the mass price segment with sophisticated digital marketing capabilities enables market leaders to establish early brand loyalty in high-growth geographies experiencing infrastructure boom cycles.

Category-wise Analysis

Product Type Insights

Hammer drills represent the most dominant product type, accounting for around 42% of the market in 2025 and expected to sustain leadership through the forecast period. Their strong position is driven by unmatched versatility in drilling into hard substrates such as concrete, brick, and stone across residential, commercial, and industrial settings. The combined rotary and percussive action enables faster penetration and consistent performance, making hammer drills indispensable for construction professionals, electricians, plumbers, and HVAC technicians. Growing reliance on rental equipment for short-term projects further supports demand, as hammer drills remain a core rental category. Continuous innovations such as brushless motors, improved vibration control, and ergonomic designs enhance durability, energy efficiency, and operator comfort, reinforcing their sustained market dominance.

Power Source Insights

Battery/DC powered drills hold a commanding share of approximately 58% in 2025, reflecting a structural shift toward cordless, flexible working environments. Their popularity stems from superior mobility, elimination of power cord constraints, and enhanced safety on job sites with limited or unstable electricity access. Advancements in lithium-ion battery technology have significantly improved runtime, charging speed, and overall energy density, enabling cordless drills to rival corded alternatives in performance. Professionals benefit from uninterrupted workflows, while DIY users value ease of storage and instant usability. Ecosystem-based platforms offering battery compatibility across multiple tools further increase adoption. Ongoing innovation in smart battery management systems and rapid charging infrastructure continues to strengthen this segment’s long-term growth outlook.

Price Range Insights

The mass price segment dominates the electric drill market with nearly 67% share in 2025, catering to a broad base of homeowners and cost-conscious professionals. Priced typically between USD 50 and USD 150 for cordless models, these products balance affordability with dependable performance, meeting the needs of routine maintenance, light construction, and small-scale contracting work. The segment benefits from high retail penetration, frequent promotional campaigns, and wide availability through large home improvement stores and local hardware outlets. Manufacturers emphasize functional reliability, standard torque capabilities, and basic ergonomic features rather than advanced customization. The mass segment’s dominance underscores the widespread democratization of power tool usage across emerging and developed markets alike.

Application Insights

Industrial applications account for approximately 45% of electric drill demand in 2025, driven by extensive usage in manufacturing, automotive assembly, aerospace production, and heavy equipment fabrication. These environments require drills capable of continuous operation, consistent torque delivery, and resistance to mechanical stress. Industrial buyers prioritize durability, compliance with occupational safety standards, and minimal downtime, often investing in standardized tool fleets for efficiency. Regular replacement cycles supported by capital expenditure budgets further sustain demand. Integration of advanced electric systems and precision controls enhances productivity in repetitive fastening and drilling operations. As industrial automation and manufacturing output expand globally, electric drills remain a foundational tool supporting operational efficiency and production reliability.

Sales Channel Insights

Hardware stores remain the leading sales channel, capturing around 38% of market share in 2025 due to strong consumer trust and hands-on purchasing experiences. These stores allow customers to physically evaluate drills, assessing weight, balance, grip comfort, and feature accessibility before purchase. Personalized guidance from trained staff plays a crucial role, particularly for first-time buyers and DIY users seeking application-specific recommendations. Immediate product availability and bundled accessory options further strengthen this channel’s appeal. Established chains and independent retailers maintain deep local presence, reinforcing customer loyalty. Despite rising digital competition, hardware stores continue to anchor electric drill sales by combining expert support with tangible product interaction.

Regional Insights

North America Electric Drill Market Trends and Insights

North America holds a leading position in the global electric drill market, accounting for nearly 35% share in 2025, with the United States contributing over three-fourths of regional revenues. Market strength is underpinned by a deeply ingrained DIY culture, high household power tool penetration, and a well-developed retail ecosystem spanning big-box stores, specialty distributors, and digital channels. Strong construction activity, particularly across major metropolitan hubs, continues to generate steady professional demand.

Federal infrastructure spending programs focused on transportation, energy grids, and broadband expansion further stimulate commercial and industrial drill consumption. Despite elevated interest rates, residential renovation remains resilient as homeowners prioritize upgrades over relocation, sustaining cordless drill demand. Innovation leadership from domestic manufacturers ensures continuous advancements in brushless motors, extended battery platforms, and smart tool integration, reinforcing North America’s position as a technologically mature and high-value market.

Europe Electric Drill Market Trends and Insights

Europe represents a mature yet stable electric drill market, capturing around 28% of global share in 2025. Demand is shaped by stringent quality standards, sustainability regulations, and a strong focus on energy efficiency across construction and renovation activities. Germany anchors regional consumption through its large construction and industrial base, supported by ongoing investments in green buildings and infrastructure modernization. The United Kingdom and France contribute significantly through professional contracting and residential refurbishment, while Southern European countries benefit from tourism-driven infrastructure upgrades.

Regulatory frameworks promoting circular economy principles encourage manufacturers to adopt recycled materials and lower-emission production processes. Although market growth remains moderate due to saturation and economic pressures, consistent renovation spending and government-backed energy efficiency incentives sustain baseline demand. Europe’s emphasis on durability, compliance, and environmental performance continues to define purchasing behavior across both residential and professional segments.

Asia Pacific Electric Drill Market Trends and Insights

Asia Pacific is the fastest-growing electric drill market globally, holding approximately 37% share in 2025 and projected to expand at a robust pace through the forecast period. China dominates regional demand, driven by large-scale construction activity, manufacturing expansion, and infrastructure modernization. Competitive domestic pricing combined with premium offerings from international brands supports broad market penetration. India stands out as a high-growth market, supported by infrastructure investments, urban development initiatives, and rising middle-class consumption, enabling first-time tool adoption.

Southeast Asian economies benefit from rapid urbanization and foreign manufacturing investments, boosting industrial demand. Japan and South Korea emphasize precision, quality, and smart tool integration, while Australia reflects strong DIY adoption and preference for cordless platforms. Localized battery production and expanding supply chains further enhance cost competitiveness, positioning the Asia Pacific as the primary growth engine for the global electric drill market.

Competitive Landscape

The global electric drill market is characterized by a moderately fragmented competitive structure, with a mix of multinational manufacturers, regional players, and numerous local producers competing across price tiers and end-use segments. While a limited group of large participants together account for a sizable share of global revenues, a long tail of smaller firms serves application-specific and regionally focused demand, particularly in emerging markets. Competition is shaped less by price alone and more by differentiation strategies centered on technology, distribution reach, and customer lock-in.

Leading players increasingly adopt platform-based business models, offering standardized battery and accessory ecosystems that span multiple power tool categories to enhance repeat purchases and switching costs. Strategic priorities also include continuous product innovation, operational efficiency, and sustainability-oriented manufacturing. In parallel, mergers, acquisitions, and strategic partnerships remain active, enabling participants to expand geographic presence, access advanced technologies, and strengthen competitive positioning in both mature and high-growth markets.

Key Developments:

- February 2024: Bosch introduced two new 18V Power for All System cordless drill drivers with interchangeable attachments featuring QuickSnap interfaces for enhanced drilling and screwing flexibility.

- February 2025: Bohle launched the Aqua Drill Pro AS cordless wet drilling machine offering high-torque, water-cooled drilling performance for professionals working on hard materials like tiles and granite at efficient speeds.

- September 2025: Milwaukee expanded its compact drilling and driving tool range with new lightweight M12 brushless percussion drill, drill driver, and impact driver models designed for enhanced performance in tight or overhead workspaces.

Companies Covered in Electric Drill Market

- Stanley Black & Decker, Inc.

- Robert Bosch GmbH

- Panasonic Corporation

- Makita Corporation

- Hilti Corporation

- Apex Tool Group

- Emerson Electric Company

- Koki Holdings Company

- Ingersoll-Rand Plc

- Techtronic Industries Company, Ltd.

- Milwaukee Electric Tool Company

- DeWalt Industrial Power Tool Company, Ltd.

- Meterk, Inc.

- Ryobi Limited

- Atlas Copco AB

- Snap-on Incorporated

- Festool GmbH

- Positec Tool Corporation

- Chervon Holdings Limited

- Craftsman

- Bohle GmbH

- Milwaukee Tool

Frequently Asked Questions

The global electric drill market is projected to reach approximately US$ 8.8 billion in 2026.

Demand is driven by rising DIY activity, expanding construction and infrastructure projects, and continuous improvements in cordless battery technology.

North America leads the market, supported by strong DIY culture, high construction spending, and well-developed retail networks.

Advancements in battery technology and smart, connected tool ecosystems represent the most significant growth opportunity.

Leading companies include Stanley Black & Decker, Inc., Robert Bosch GmbH, Techtronic Industries Company, Ltd., Makita Corporation, Hilti Corporation, Milwaukee Electric Tool Company, and DeWalt Industrial Power Tool Company, Ltd.