- Power Generation, Transmission, & Distribution

- Power Grid Market

Power Grid Market Size, Share, and Growth Forecast, 2026 - 2033

Power Grid Market by Component Type (Power Lines & Cables, Protection & Control Systems, Substations, Switchgear, Transformers, Misc.), Grid Infrastructure Type (Transmission Networks, Distribution Networks, Generation Interconnection, Grid Storage & Reactive Support), Grid Technology (Conventional Grid Infrastructure, Smart Grid Infrastructure, Microgrids), Industry (Residential, Commercial, Industrial, Utilities), and Regional Analysis for 2026 - 2033

Power Grid Market Size and Trends Analysis

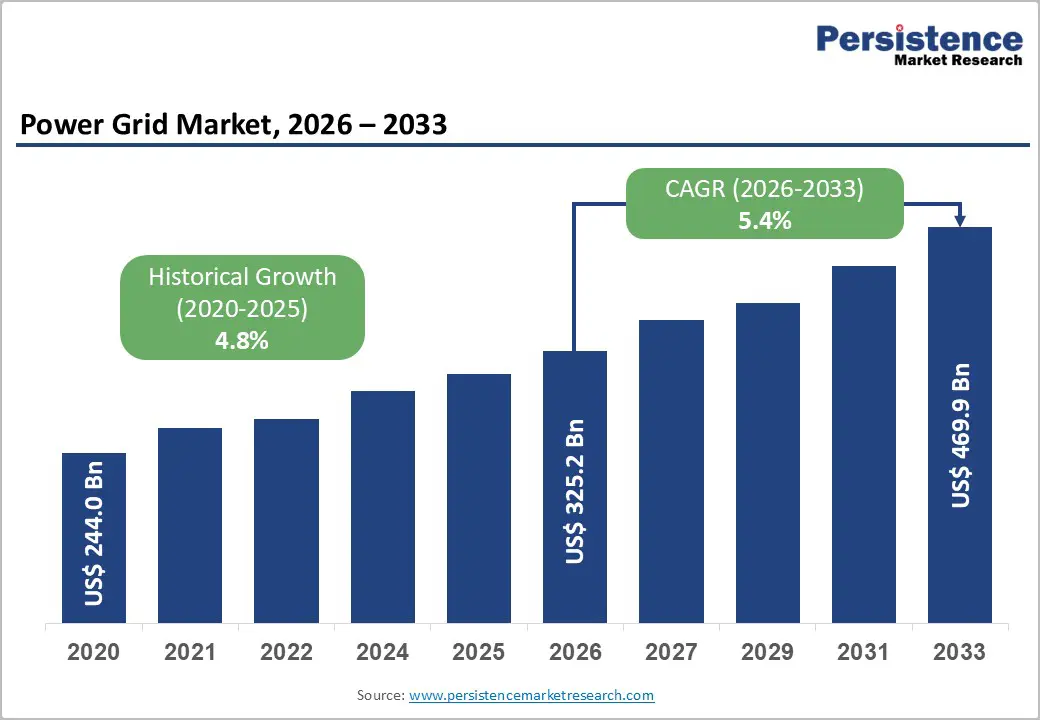

The global power grid market size is likely to be valued at US$ 325.2 billion in 2026 and is projected to reach US$ 469.9 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

This trajectory is underpinned by an accelerating global energy transition, large-scale electrification programs, and the urgent need to modernise ageing transmission and distribution infrastructure across mature and emerging economies alike. Between 2020 and 2026, the market demonstrated a historical CAGR of 4.8%, reflecting sustained structural demand for grid upgrades.

The parallel push to integrate variable renewable energy sources, solar, wind, and hydropower into national grids is amplifying investment in smart grid technologies, high-voltage direct current (HVDC) systems, and advanced protection controls. With electricity consumption climbing globally, including India's 1,694 billion units in FY25, up 33% from FY21, governments and private utilities are channeling unprecedented capital into grid reinforcement, storage deployment, and cross-border transmission linkages.

Key Industry Highlights:

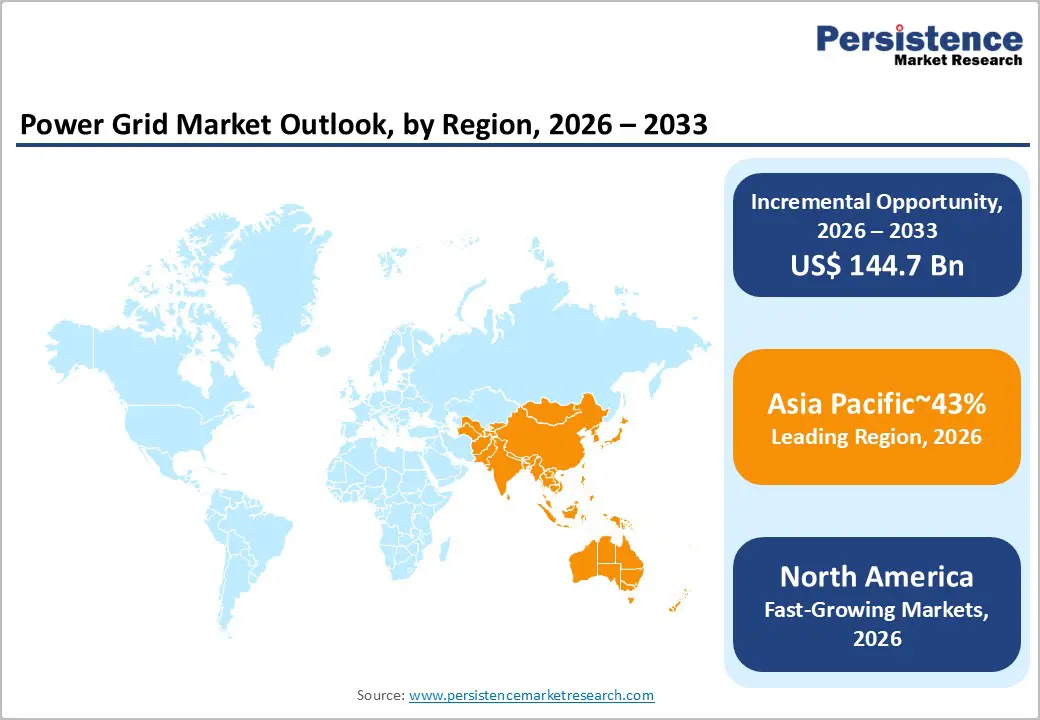

- Dominant Region: Asia Pacific leads the Power Grid Market with approximately 43% share, driven by large-scale transmission expansion in China, India’s Rs. 2 lakh crore grid capex program, and rapid renewable integration across Japan and South Korea.

- Leading Grid Infrastructure: Distribution Networks account for nearly 40% market share, supported by urbanisation, electrification of transport and heating, and the need to modernise ageing last-mile infrastructure.

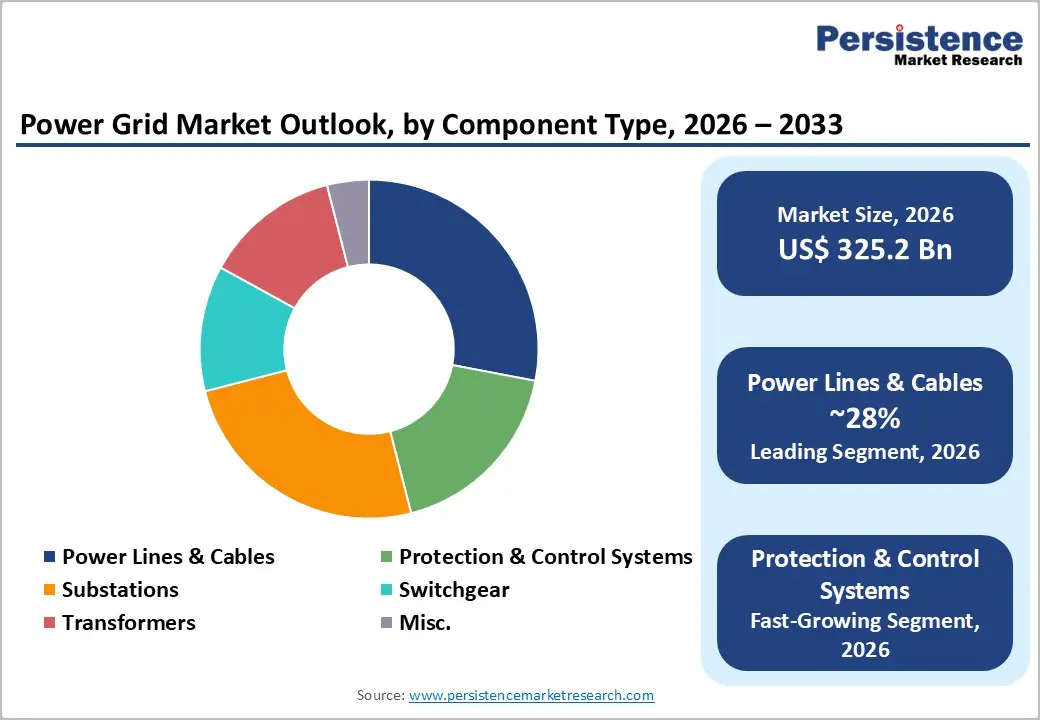

- Leading Component: Power Lines & Cables hold around 28% share, reflecting their foundational role in transmission and distribution expansion, reinforced by multi-year procurement agreements across Europe and Asia.

- Fast-growing Grid Infrastructure: Generation Interconnection Fastest-Growing: Generation Interconnection is the fastest-growing infrastructure segment, propelled by record renewable additions and large-scale solar and wind grid connectivity requirements globally.

- Growth Indicator: Accelerated renewable capacity additions, including India’s 500 GW 2030 target and Europe’s rapid solar expansion, are structurally increasing demand for transmission, substations, and grid stability solutions.

- HVDC & Ultra-High Voltage Opportunity: Ultra-High Voltage and HVDC transmission projects are emerging as major investment avenues, enabling efficient long-distance renewable power transfer with lower losses and reduced land footprint.

- North America Strategic Investment Hub: North America holds approximately 21% share, supported by multi-billion-dollar DOE transmission programs, rising AI-driven data center load growth, and expanding domestic transformer and switchgear manufacturing capacity.

| Key Insights | Details |

|---|---|

| Power Grid Market Size (2026E) | US$ 325.2 Bn |

| Market Value Forecast (2033F) | US$ 469.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Dynamics

Drivers - Accelerated Renewable Energy Integration and Grid Modernisation Imperatives

The rapid deployment of utility-scale solar and wind capacity worldwide is fundamentally reshaping grid architecture, necessitating significant investment in transmission, protection systems, and energy storage. As intermittent generation sources displace conventional base-load plants, grid operators face increased complexity in maintaining frequency, voltage stability, and load balance across national networks.

India's renewable capacity reached 250.64 GW by October 2025, with solar contributing 129.9 GW and wind 53.6 GW, while the country aims for 500 GW of renewable capacity by 2030, a target that demands extensive transmission infrastructure buildout, including Power Grid Corporation of India's Rs. 2 lakh crore (US$ 23.1 billion) capital expenditure plan. In Europe, between 2022 and 2024, the EU added 168 GW of solar capacity and 44 GW of wind capacity, with renewables accounting for 46.9% of the EU's energy production mix in 2024, placing immense pressure on transmission networks to absorb and redistribute variable output. For the power grid market, this structural shift is one of the most consequential long-term demand drivers, necessitating grid-scale investments across both transmission and distribution tiers globally.

Surging Electricity Demand Driven by Industrialisation, Electrification, and Emerging Digital Infrastructure

Global electricity demand has entered an era of structurally elevated growth, fueled by industrial expansion, urbanisation, the electrification of transport, and the explosive proliferation of data centres and artificial intelligence infrastructure.

In the United States, the Edison Electric Institute reported that nearly 80% of US$ 186.4 billion spent by investor-owned utilities in 2024 was directed to infrastructure, driven by a five-year load growth forecast that rose over five times from 23 GW in 2023 to 120 GW in 2024. In California alone, PG&E announced plans to invest US$ 73 billion in transmission enhancements by 2030 to accommodate a projected 10 GW demand increase from new data centers, while CAISO is directing US$ 4.8 billion between 2024 and 2025 to relieve grid congestion and enable the electrification of buildings and transport.

India's peak power demand reached 250 GW in June 2025 and is projected to reach 277 GW in FY26, highlighting the urgency of grid capacity expansion. These demand pressures are directly channelled into the Power Grid Market, requiring higher volumes of transmission infrastructure, substation upgrades, switchgear, and digital grid management solutions.

Government Policy Mandates and Public Investment in Grid Resilience and Security

Regulatory frameworks and government-backed financing programs have emerged as foundational pillars sustaining capital deployment in grid infrastructure. The U.S. Department of Energy announced an investment of US$ 1.5 billion across four transmission projects and additionally awarded US$ 2.2 billion to eight transmission projects across 18 states, with the potential to expand grid capacity by approximately 13 GW, supported by the National Transmission Planning Study, which identifies 54,500 GW-miles of new transmission required by 2035.

In India, the central government's power investment plan totalling Rs. 9.15 lakh crore (US$ 109.5 billion) aims to strengthen the national grid and achieve near-universal electricity access, with an additional Rs. 4.79 lakh crore (US$ 56.07 billion) earmarked for energy storage deployment by 2032. In Europe, grid investment frameworks are being structured to clear growing queues of renewables projects waiting for grid connections, queues that are more than three times the capacity needed for the EU to meet its 2030 energy and climate targets. For the Power Grid Market, these policy-driven mandates translate into durable, multi-year procurement cycles for grid components and systems across all geographies.

Restraint - High Capital Expenditure and Long Project Gestation Periods

Grid infrastructure projects are capital-intensive endeavours with multi-year development cycles, complex permitting requirements, and significant upfront procurement costs. A report issued in May 2025 projected that investments of up to US$ 600 billion per year by 2030 would be required globally to modernize aging grids, integrate renewables, and support electric mobility.

Many grids across Europe and North America are over 40 years old, and replacement costs are formidable. In the United States, customer electricity prices rose 4.5% nationally, nearly twice the 2.4% national inflation rate, reflecting the pass-through burden of infrastructure investment to end consumers and creating political friction around utility rate approvals. These cost dynamics constrain the pace at which capital can be deployed without triggering regulatory pushback or affordability concerns.

Supply Chain Constraints and Manufacturing Capacity Limitations

The demand surge for critical grid components, including transformers, switchgear, and cables, has exposed significant bottlenecks in global manufacturing capacity. Lead times for large power transformers have extended considerably across major markets, limiting the pace of grid expansion and modernisation.

In response, Siemens Energy announced a US$ 2.3 billion investment to expand its global transformer and switchgear manufacturing capacity by 2028, while separately committing US$ 1 billion to scale up U.S. production facilities and create over 1,500 skilled jobs. These supply constraints, combined with raw material sourcing challenges for copper, aluminium, and speciality steels, represent a structural brake on the Power Grid Market's capacity to meet accelerating demand from utilities and governments worldwide.

Key Opportunities - Ultra-High Voltage and HVDC Transmission for Long-Distance Renewable Energy Delivery

The need to transmit large volumes of renewable electricity across vast distances from generation-rich regions to load centers positions ultra-high voltage direct current (HVDC) technology as one of the most strategically significant opportunities in the Power Grid Market. HVDC systems enable efficient, low-loss power transmission over thousands of kilometres, making them essential for integrating offshore wind farms, large-scale solar parks, and remote hydropower resources into national grids.

A landmark demonstration of this technology was the energisation of the Raigarh-Pugalur 6,000 MW plus or minus 800 kV UHVDC transmission link in India, spanning approximately 1,800 kilometres to connect central and southern India, enabling large-scale renewable energy transmission to high-demand centres while providing reliable electricity to over 80 million people. The project also demonstrated that HVDC technology occupies approximately one-third the land space of a conventional AC substation, making it particularly attractive in land-constrained corridors.

As countries accelerate their renewable deployment targets, with India alone targeting 500 GW of renewable capacity by 2030, and China leading global solar and wind expansion demand for HVDC infrastructure and associated grid interconnection equipment, is set to intensify substantially across multiple continents

Grid Digitalisation, AI-Enabled Operations, and Smart Grid Platforms

The convergence of artificial intelligence, the Internet of Things, and advanced grid sensors is creating a new paradigm for grid management, enabling utilities to optimise asset performance, predict failures, improve outage response times, and integrate distributed energy resources more effectively. This digital transformation represents a significant commercial opportunity across planning, operations, and asset management software, as well as intelligent hardware at the grid edge.

In November 2025, Schneider Electric launched its AI-enabled One Digital Grid Platform, designed to help utilities modernise operations, strengthen grid resilience, and reduce energy costs without requiring full infrastructure overhauls, while providing real-time outage restoration estimates. Mitsubishi Electric and Landis and Gyr formalised a Memorandum of Understanding in January 2026 to advance grid edge intelligence, leveraging intelligent edge devices and analytics to enhance grid stability and integrate distributed energy resources.

The digitalisation of the Power Grid Market is further reinforced by the growing recognition that junction failures are responsible for over 70% of distribution grid outages, underscoring the commercial case for advanced monitoring, inspection, and condition-based maintenance platforms across ageing network assets.

Grid Storage, Reactive Support, and Energy Flexibility Infrastructure

As variable renewable penetration deepens, the need for grid-scale energy storage and reactive power support is becoming a critical infrastructure priority, creating a distinct and rapidly expanding investment class within the Power Grid Market. Grid storage assets ranging from large battery energy storage systems to pumped hydro and synchronous condensers are essential to maintaining grid stability and ensuring a reliable supply during periods of low renewable generation.

In Germany, Siemens Energy was commissioned by TenneT to supply three grid stabilisation systems, including synchronous condensers, to address the challenges of replacing conventional power plants with decentralised renewable energy, enabling kinetic energy storage and active power feed-in to maintain grid stability.

India has identified energy storage deployment as an investment priority, with the segment expected to attract Rs. 4.79 lakh crore (US$ 56.07 billion) by 2032, reflecting the scale of the storage buildout required to support renewable integration and grid reliability. These developments collectively signal a structural shift toward multifunctional grid infrastructure that combines generation interconnection, storage, and reactive support within unified investment frameworks.

Category-wise Analysis

Component Type Insights

Power Lines and Cables account for approximately 28% of the Global Power Grid Market in 2026, reflecting their fundamental role as the physical backbone of every transmission and distribution network. This segment encompasses overhead transmission lines, underground cables, and subsea interconnectors, all of which are witnessing sustained procurement activity as utilities expand grid footprints, replace ageing conductors, and construct new renewable energy evacuation corridors.

The scale of this demand is evidenced by Prysmian's framework agreement with Enedis to supply medium-voltage cables for the modernisation of the French power grid over seven years, valued at up to EUR 550 million, and its three-year agreement with Terna worth up to EUR 382.5 million for HVAC cables for Italy's high-voltage transmission network. Additionally, Prysmian and EON signed a long-term agreement to supply low and medium-voltage cables for Germany's grid modernisation as part of a EUR 6 billion procurement program, with an emphasis on sustainable materials including recycled aluminium and copper. These contracts underscore the large procurement volumes being directed to this segment globally.

Protection and Control Systems represent the fastest-growing component category, driven by the imperative to manage complex, bidirectional power flows across grids integrating high shares of variable renewables. This segment includes digital relays, SCADA systems, grid automation platforms, and power flow controllers, all of which are essential for maintaining stability, preventing cascades, and enabling real-time grid management.

Grid Infrastructure Type Insights

Distribution Networks hold approximately 40% of the Global Power Grid Market in 2026, reflecting the density and capital intensity of the last-mile infrastructure that connects transmission systems to end-user industrial facilities, commercial establishments, and residential consumers.

Distribution network investment is driven by urbanisation, the electrification of heating and transport, and the need to accommodate distributed energy resources such as solar rooftop, battery storage, and electric vehicle charging. The vulnerability of distribution infrastructure is significant, with failures at junctions responsible for over 70% of distribution grid outagesmaking investment in network modernisation a high-priority agenda for utilities globally. Nexans' introduction of the first range of low-carbon power grid cables in France, reducing greenhouse gas emissions by 35 to 50% compared to standard cables, exemplifies innovation being embedded at the distribution infrastructure level to meet both reliability and sustainability objectives.

Generation Interconnection is the fastest-growing infrastructure type, driven by the massive pipeline of renewable energy projects requiring new transmission connections to national grids. As solar and wind capacity additions accelerate, India added a record 20.1 GW of renewable capacity during April through August of FY26, a 123% increase year-on-year. The need for dedicated generation interconnection infrastructure is creating substantial demand for new substations, connection lines, and protection systems.

Regional Insights and Trends

Asia Pacific Power Grid Market Trends

Asia Pacific is the dominant regional contributor to the Global Power Grid Market, commanding approximately 43% of global market share, driven by China, India, Japan, and South Korea as the primary investment centres.

China's electricity system is the world's largest, with the country accounting for a significant portion of global new solar, onshore wind, and distributed energy additions between 2019 and 2024, while managing an energy-related CO2 emissions profile of 11,130 million tonnes representing 32% of global emissions, which creates sustained policy pressure to modernise and decarbonise grid infrastructure.

India presents among the most dynamic investment environments globally: with an installed capacity of 505 GW as of October 2025, electricity consumption of 1,694 BU in FY25, and peak demand projected to reach 277 GW in FY26, the country's power investment opportunity is estimated at INR 40 lakh crore (US$ 461.95 billion) over the next decade. India's grid expansion is led by Power Grid Corporation of India's Rs. 2 lakh crore capex plans, with thermal power expected to attract INR. 2.3 lakh crore (US$ 26.71 billion) by 2028 for 80 GW of additional capacity.

South Korea's total electricity production was approximately 607,349 GWh in 2024, more than doubling since 2000, while Japan's high import-dependence at 87.4% of energy supply underscores the strategic importance of domestic grid reliability and resilience for both countries. In India, the private sector represents 50.7% of total installed capacity, while the central sector contributes 24% a diversified ownership structure that channels both public and private capital into grid infrastructure procurement

North America Power Grid Market Trends

North America accounts for approximately 21% of the global market, with the United States as the primary demand centre. In 2023, the U.S. generated approximately 4,178 billion kWh from utility-scale facilities, with fossil fuels accounting for roughly 60%, nuclear contributing 18.6%, and renewables providing 21.4%. The structural shift in the U.S. energy mix with coal declining significantly and natural gas and renewables expanding, is driving extensive grid reconfiguration investment.

The U.S. Department of Energy's National Transmission Planning Study identified the need for 54,500 GW-miles of new transmission by 2035, anchoring a multi-decade investment pipeline. Edison Electric Institute data confirmed that nearly 80% of US$ 186.4 billion spent by investor-owned utilities in 2024 was directed to infrastructure, while CAISO is directing US$ 4.8 billion to accommodate data centers, electrification of transport, and grid congestion relief. Siemens Energy's US$ one billion investment announced in February 2026 to scale up U.S. production of grid and gas turbine equipment, including a new switchgear plant in Mississippi and expanded transformer production, reflects the growing domestic manufacturing footprint being established to serve this demand. The Grid Modernisation Initiative of the U.S. Department of Energy continues to direct resources toward innovative technologies that enhance grid security, sustainability, and resilience.

Europe Power Grid Market Trends

Europe represents approximately 18% of the global market, characterised by some of the most ambitious clean energy policy mandates globally and corresponding levels of grid investment. The EU generated 2,637 TWh of net electricity in 2023, with renewable energy sources accounting for 40.8% of total generation, while fossil fuels made up 36.4%. Between 2022 and 2024, the EU added 168 GW of solar capacity and 44 GW of wind capacity, with solar PV overtaking coal in the EU's electricity mix for the first time, a milestone in Europe's clean energy transition. This pace of renewable buildout is creating urgent demand for grid reinforcement: a May 2025 joint report flagged that renewables stuck in grid connection queues represent more than three times the capacity needed for the EU to reach its 2030 targets, highlighting critical under-investment in interconnection and distribution infrastructure. TenneT's commissioning of Siemens Energy grid stabilisation systems in Germany and Prysmian's EUR 550 million medium-voltage cable supply agreement for France's Enedis reflect the breadth of procurement activity across the European market.

Competitive Landscape

The global power grid market is largely consolidated, dominated by a few major players that control high-value segments, including transmission networks, substations, and smart grid solutions. Leading companies, including Siemens AG, General Electric (GE) Grid Solutions, Schneider Electric, ABB Group, Hitachi Energy, and Eaton Corporation, hold significant market share and leverage advanced technologies and global project experience to secure key contracts. These firms focus on strategic partnerships, mergers, and acquisitions to expand their presence across developed and emerging regions, particularly in renewable integration and digital grid modernisation.

While transmission and smart grid segments are highly consolidated due to capital intensity and regulatory barriers, distribution and component markets remain somewhat fragmented, providing opportunities for regional players. Competition is intensifying as demand for smart metering, digital substations, and grid automation grows, pushing companies to differentiate through innovation, software solutions, and after-sales services.

Key Industry Developments:

- In February 2026, Siemens Energy announced a $1 billion investment to expand U.S. production of power grid and gas turbine equipment, creating over 1,500 skilled jobs. The investment aims to strengthen grid infrastructure and meet rising electricity demand driven by data centres, AI, and industrial electrification, enhancing resilience and supporting the rapid growth of the U.S. energy market.

- In February 2026, Prysmian signed a framework agreement with Enedis to supply the full range of medium-voltage cables for the modernisation of the French power grid over seven years (2026–2032), in a contract worth up to €550 million. The initiative supports low-carbon and renewable energy integration, incorporates recycled materials in cable production, and strengthens France’s grid infrastructure while advancing sustainable and circular energy solutions.

- In January 2026, Mitsubishi Electric joined Landis+Gyr’s Application Ecosystem through a Memorandum of Understanding to advance grid edge intelligence and accelerate the energy transition. The collaboration leverages intelligent edge devices and analytics to enhance grid stability, integrate distributed energy resources, and improve utility operations, enabling consumers to optimize energy use while supporting a smarter, more flexible, and sustainable power grid.

Companies Covered in Power Grid Market

- ABB Ltd.

- Siemens Energy AG

- General Electric Company

- Prysmian S.p.A.

- Nexans S.A.

- Schneider Electric SE

- Mitsubishi Electric Corporation

- Eaton Corporation plc

- Hitachi Energy Ltd.

- Powell Industries, Inc.

- Hubbell Incorporated

- Toshiba Energy Systems & Solutions Corporation

- Sécheron SA

Frequently Asked Questions

The global Power Grid Market is projected to be valued at US$ 325.2 Bn in 2026.

The Distribution Networks segment is expected to account for approximately 40% of the Global Power Grid Market by Grid Infrastructure Type in 2026.

The market is expected to witness a CAGR of 5.4% from 2026 to 2033.

The Power Grid Market growth is driven by accelerated renewable energy integration, surging electricity demand from industrialisation and digital infrastructure, and large-scale government-backed investments in transmission expansion, grid modernisation, and energy storage deployment.

Key market opportunities in the global Power Grid Market lie in Ultra-High Voltage and HVDC transmission expansion, AI-enabled grid digitalisation and smart grid platforms, and large-scale grid storage and reactive power infrastructure to support renewable integration and energy flexibility.

Key players in the Power Grid Market include Siemens AG, General Electric (GE) Grid Solutions, Schneider Electric, ABB Group, Hitachi Energy, and Eaton Corporation.