- Power Generation, Transmission, & Distribution

- Nuclear Power Plant Equipment Market

Nuclear Power Plant Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Nuclear Power Plant Equipment Market by Equipment Type (Island Equipment, Auxiliary Equipment / BOP Equipment), Reactor Type (Pressurised Water Reactors (PWR), Boiling Water Reactors (BWR), Pressurised Heavy Water Reactors (PHWR), Advanced Reactor), and Regional Analysis for 2026 - 2033

Nuclear Power Plant Equipment Market Size and Trends Analysis

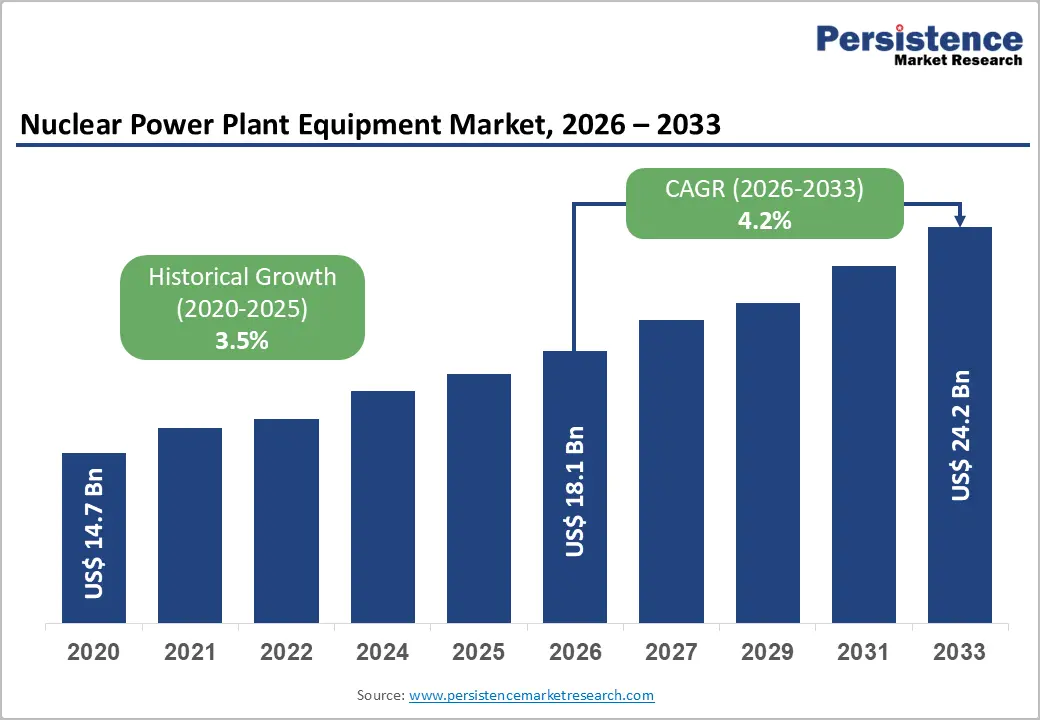

The global nuclear power plant equipment market size is likely to be valued at US$ 18.1 billion in 2026 and is projected to reach US$ 24.2 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

This expansion is driven by accelerating global demand for reliable baseload power to meet rising electricity consumption from digitalisation and industrial growth, aggressive government-mandated decarbonization targets aligned with climate commitments, and substantial policy investments supporting nuclear capacity expansion across the United States, China, and India.

Key Industry Highlights:

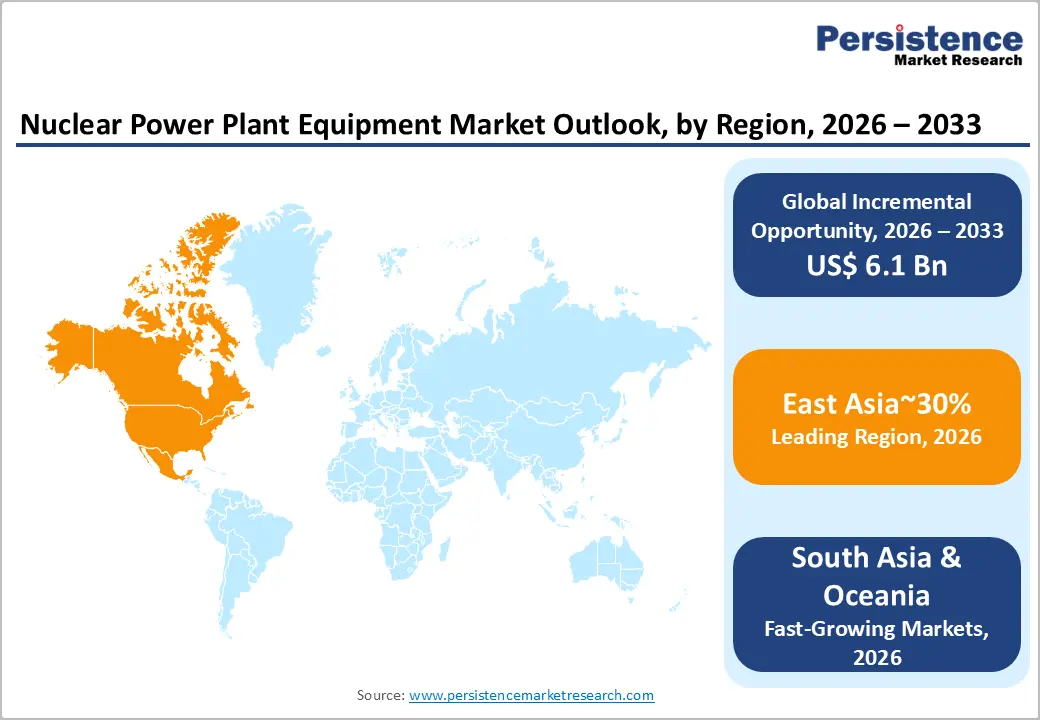

- Leading Region: East Asia commands 34% market share, driven by China’s large-scale reactor approvals, indigenous reactor programs, and sustained island equipment procurement.

- High-Growth Region: South Asia & Oceania is the fastest-growing region, fueled by India’s 100 GW nuclear mission, PHWR expansion, and aggressive localization of nuclear equipment manufacturing.

- Dominant Equipment: Island Equipment holds 63% market share, reflecting the capital-intensive nature of reactor vessels, steam generators, turbines, and NSSS systems.

- Fastest-Growing Equipment: Auxiliary Equipment / Balance-of-Plant (BOP) is expanding rapidly, supported by SMR standardization, modular builds, and distributed nuclear deployments.

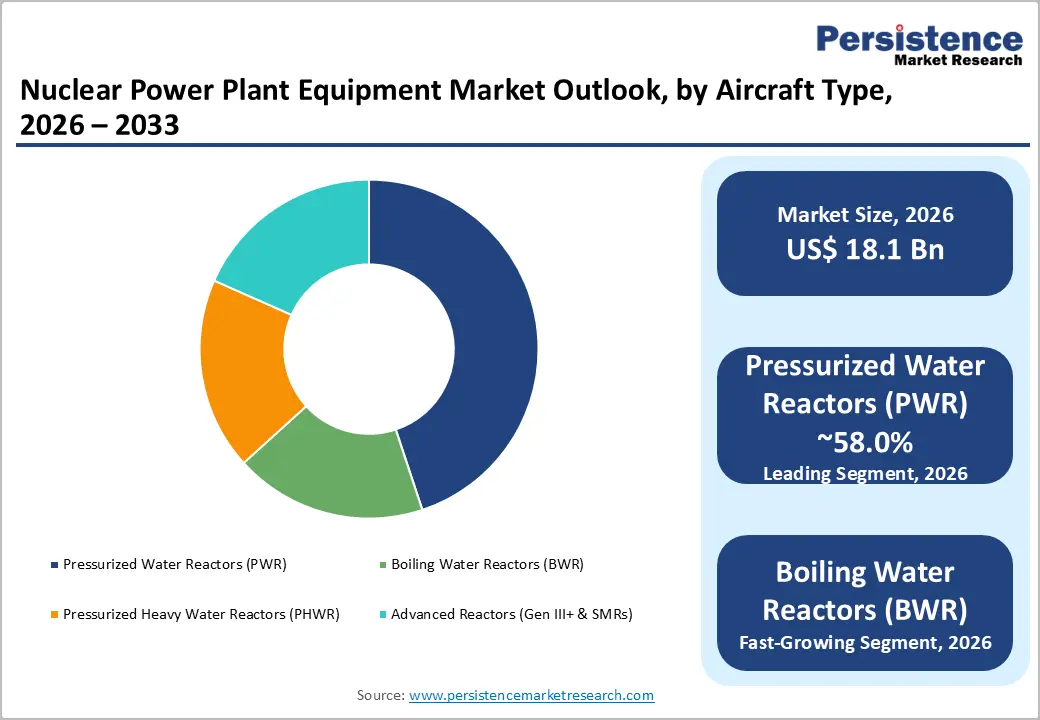

- Leading Reactor Type: Pressurised Water Reactors (PWRs) account for 58% of equipment demand, underpinned by global new-build pipelines and life-extension retrofit programs.

| Key Insights | Details |

|---|---|

| Nuclear Power Plant Equipment Market Size (2026E) | US$ 18.1 Bn |

| Market Value Forecast (2033F) | US$ 24.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Dynamics

Drivers - Energy security and decarbonization mandates are propelling nuclear modernisation and new builds in the Nuclear Power Plant Equipment Market.

Governments are increasingly embracing nuclear energy as a cornerstone of long-term energy independence and climate commitments, fundamentally reshaping demand for nuclear power plant equipment. Driver reflects how rising geopolitical tensions, renewable intermittency challenges, and net-zero pledges have converted nuclear from a marginal technology into a strategic priority for energy-intensive economies in the nuclear power plant equipment market.

In December 2025, India launched a Nuclear Energy Mission targeting 100 GW of capacity by 2047, a tenfold increase from the current 8.18 GW, with NPCIL expected to contribute 54 GW through indigenous pressurised heavy water reactors (PHWRs) and light water reactors, while BARC develops small modular reactors (BSMR-200 and SMR-55) for industrial and remote deployment.

China approved 10 new reactor projects in April 2025 with over USD 27.45 billion in investment, targeting a capacity of 110 GW by 2030 and 200 GW by 2035 to achieve carbon neutrality by 2060. South Korea's updated 15-year energy plan mandates construction of two large reactors and 700 MW of SMR capacity by 2038 to meet rising electricity demand and climate goals. For the nuclear power plant equipment market, these strategic pivots translate into multi-decade procurement pipelines for reactor island systems, control instrumentation, and balance-of-plant (BOP) equipment across PWR, BWR, and PHWR technologies.

Supply-chain localisation and indigenous manufacturing policies in major nuclear markets

Governments and operators are mandating domestic sourcing and value-added local production of nuclear equipment to build industrial self-reliance and reduce supply-chain vulnerabilities, creating new opportunities in the Nuclear Power Plant Equipment Market for regional manufacturers and OEMs establishing in-country operations.

In October 2024, India's Nuclear Power Corporation (NPCIL) received Design Organisation Approval (DOA) under CAR 21 from the Directorate General of Civil Aviation, enabling in-house design and implementation of interior and structural modifications to accelerate fleet modernisation. Supported by collaboration with Tata Technologies, this approval strengthens India's domestic engineering and modification capabilities.

In September 2025, Framatome inaugurated its India operations base in Navi Mumbai to support long-term operations, life extension, new nuclear builds, and SMR programs, positioning the company to serve India's 100 GW nuclear target through localised engineering and execution. India's defence industrial corridors (Uttar Pradesh and Tamil Nadu) have attracted significant investment in nuclear component manufacturing, with NPCIL, Bhel, L&T, and private partners expanding capacity for reactor equipment, heat exchangers, and balance-of-plant systems.

Localisation reshapes regional competitive dynamics, enabling indigenous suppliers to capture higher margins on commodity components while global OEMs increasingly serve as technology and certification partners. This trend, coupled with India's requirement to domestically manufacture most reactor equipment by 2047, fundamentally expands the equipment production footprint and creates multi-billion-dollar opportunities in India, China, and Southeast Asia.

Small modular reactor (SMR) design maturation and first-of-a-kind deployments are reshaping equipment demand

The nuclear power plant equipment market is experiencing a structural shift as advanced reactor designs transition from demonstration to commercial deployment, creating demand for factory-built, standardised equipment modules. This driver centres on how SMRs' smaller unit capacity, passive safety features, and off-grid deployment flexibility expands the addressable market beyond traditional utility-scale nuclear to data centres, industrial heat users, and remote regions in the nuclear power plant equipment market.

SMR deployment accelerates the procurement of integrated pressurizer-steam generator assemblies, compact reactor vessels, modular structural systems, and factory-certified balance-of-plant packages. Equipment suppliers such as Holtec, BWXT, and Mitsubishi Electric are scaling production capacity and developing standardised designs to support fleet-wide deployment, fundamentally altering equipment supply-chain structure and supporting margins for factory-built systems over site-assembled components.

Restraint - Capital Intensiveness and Extended Project Development Timelines

Nuclear power plant projects require substantial upfront capital investments, with conventional large reactors demanding USD 10-20 billion in total lifecycle costs, whilst SMR projects typically require USD 4,000-6,000 per kilowatt of installed capacity, creating barriers to deployment acceleration within the Market.

Extended regulatory licensing timelines, typically requiring 7-10 years for design certification and construction permits in Western jurisdictions, delay equipment procurement cycles and constrain equipment manufacturer capacity planning. Supply chain bottlenecks in specialised nuclear-grade components (heavy forgings, pressure vessels, instrumentation systems) have extended lead times by 6-12 months, increasing procurement costs by 15-25 percent and creating scheduling constraints within the Nuclear Power Plant Equipment Market.

Opportunity - Advanced reactor architectures and fourth-generation technologies are creating retrofit and new equipment platforms.

High-temperature gas-cooled reactors (HTGRs), fast breeder reactors (FBRs), and molten salt reactors represent technology convergence that will drive demand for specialised equipment in industrial applications, hydrogen production, and distributed heating, expanding the serviceable addressable market of the Nuclear Power Plant Equipment Market beyond conventional electricity generation.

China commissioned the world's first commercial high-temperature gas-cooled reactor at Huaneng Shidaowan in 2023, while the Linglong One SMR is scheduled for completion by 2026, positioning China as a leader in next-generation reactor technology. India's nuclear roadmap includes the development of fast breeder reactors (FBRs) and high-temperature gas-cooled reactors (HTGCRs) for long-term capacity expansion and industrial heat applications, with BARC advancing multiple technology pathways to meet the 100 GW target by 2047.

Advanced reactor deployments create demand for novel heat exchangers, specialised coolant pumps, high-performance I&C systems, and modular balance-of-plant architectures. Equipment suppliers investing in R&D for hydrogen production integration, industrial process heat, and district heating applications will unlock new revenue streams. As utilities and industrial operators recognize the dual-use potential of nuclear heat, retrofit and equipment modification contracts will expand, driving the market beyond traditional generation-only models.

Strategic partnerships and joint ventures between OEMs and international technology providers are accelerating equipment localisation

Global nuclear equipment OEMs are forming alliances with regional partners to achieve localised manufacturing, technology transfer, and design approval in high-growth markets, structurally reshaping competitive positioning and equipment sourcing in the nuclear power plant equipment market.

In December 2025, the Government of India and Russia's Rosatom agreed to accelerate discussions on setting up a second Russian-designed nuclear power plant in India, including deeper cooperation on VVER reactors, localization, and joint manufacturing of nuclear equipment and fuel assemblies. The X-energy/Amazon/KHNP/Doosan partnership announced in August 2025 explicitly covers reactor engineering, equipment supply chains, and construction planning, with Doosan positioned as a key equipment supplier for the global Xe-100 deployment. GE Vernova's May 2024 sale of its Steam Power business to EDF, now operating as Arabelle Solutions, reinforces the trend of consolidation around specialized equipment platforms, enabling EDF to strengthen its nuclear equipment portfolio for new builds and life extensions in Europe and globally.

These partnerships accelerate technology transfer to emerging markets and create supply agreements that lock in multi-decade demand. Joint ventures reduce time-to-market for localised manufacturing and lower the cost of capital through risk-sharing, ultimately expanding equipment production capacity and creating competitive pricing pressure that benefits operators while maintaining quality and safety standards across the nuclear power plant equipment market.

Category-wise Analysis

Aircraft Type Insights

Island equipment represents approximately 63% of the Nuclear Power Plant Equipment Market in 2026, establishing this category as the dominant revenue contributor. Island equipment encompasses the nuclear steam supply system (NSSS), including reactor pressure vessels, steam generators, pressurizers, primary coolant pumps, and associated piping and controls, plus conventional island equipment such as turbine-generator sets and condenser systems. These components are the most capital-intensive and technology-critical, with single units often commanding USD 100-300 million+ per reactor.

Large-scale projects such as India's 100 GW nuclear mission and China's 10-reactor approval in April 2025 drive substantial island equipment orders, with Framatome, Westinghouse, GE Hitachi, and Mitsubishi Heavy Industries competing for major contracts. The concentration of capex in island equipment reflects the non-modular, site-integrated nature of conventional nuclear plants, where turbines, generators, and primary system components are fabricated centrally and shipped as modules.

Auxiliary Equipment and Balance-of-Plant (BOP) segment is identified as the fastest-advanced category within equipment type, driven by SMR standardization and distributed deployment patterns. Auxiliary equipment includes cooling systems, electrical distribution, I&C cabinets, water treatment, fire protection, and auxiliary building systems.

Service Model Insights

Pressurized Water Reactors (PWRs) accounted for approximately 58% of the Nuclear Power Plant Equipment Market in 2026, making them the dominant reactor type by equipment demand. PWRs remain the largest-deployed technology globally, with over 300 units operational across the United States, Europe, Asia, and Russia. Major PWR programs include India's planned light water reactors as part of the 100 GW mission with international cooperation, China's CAP1000 domestically adapted design, and life-extension projects across the U.S. and France. Equipment demand for PWRs centres on Westinghouse AP1000 components such as pressure vessels, steam generators, Framatome EPR systems, and Russian VVER technology.

The PWR market share reflects both large-scale new-built pipelines and mature retrofit and life-extension work, where control system upgrades, replacement steam generators, and structural reinforcements sustain recurring equipment orders. Boiling Water Reactors (BWRs) are identified as the fastest-growing reactor type segment, despite commanding a smaller overall market share than PWRs. BWR demand is being driven by SMR development, which is attracting investment from utilities, private companies, and energy-intensive industrial operators seeking lower-capex, off-grid nuclear solutions.

Regional Insights and Trends

North America Nuclear Power Plant Equipment Market Trends

North America represents 28% of the global Nuclear Power Plant Equipment Market, supported by the United States' 94 operational reactors producing 778 TWh annually i.e., 18.6% of national electricity generation in 2023, and Canada's 15 operational reactors generating approximately 15 percent of national electricity.

The U.S. nuclear fleet's average operational age of 40+ years necessitates sustained equipment replacement and modernization, with major refurbishment initiatives targeting extended plant life beyond original 40-year licenses to 60-80 years, generating recurring equipment demand cycles within the Nuclear Power Plant Equipment Market. BWX Technologies' C$80 million expansion of its Cambridge, Ontario, manufacturing facility to scale production of nuclear power plant equipment for SMRs, large reactors, and advanced reactor programs strengthens North American supply chain resilience and validates growing domestic equipment procurement demand within the market.

Natural Resources Canada's 2018 SMR Roadmap and subsequent federal government commitments to SMR commercialisation established policy frameworks enabling private-sector equipment innovation and regional manufacturing capability development, with Ontario Power Generation's Darlington New Nuclear Project hosting BWRX-300 deployment, creating anchor customer demand for standardised SMR equipment production.

East Asia Nuclear Power Plant Equipment Market Trends

East Asia represents approximately 34% of the global Nuclear Power Plant Equipment Market, making it the largest regional market and the primary growth engine for the sector. China dominates this region, with 59 operational reactors (58.1 GWe) and 35 reactors under construction i.e. 40.4 GWe gross capacity, representing roughly 50 percent of all global reactor construction. In April 2025, China's State Council approved 10 new reactor projects with over USD 27.45 billion in investment, targeting capacity expansion to 110 GW by 2030 and 200 GW by 2035. China's electricity generation mix is dominated by coal (60.9%), but nuclear deployment is accelerating as a strategic pillar of decarbonization and energy independence; nuclear accounted for 444.7 TWh in 2024.

China's equipment market is shaped by indigenous reactor designs Hualong One (HPR1000) and CAP1000, which reduce dependence on foreign vendors while creating supply contracts for Chinese manufacturers such as SNPEMC, Dongfang Electric, and Mitsubishi-JSW partnerships for reactor vessels. The Linglong One SMR scheduled for 2026 will further localise SMR equipment production within China's supply base.

South Korea and Japan contribute a steady demand through fleet modernisation and selective new builds. South Korea's updated energy plan mandates 2 large reactors plus 700 MW SMR capacity by 2038, adding to the existing fleet of 26 reactors. Japan is cautiously restarting reactors post-Fukushima, with emphasis on seismic reinforcements, cyber-hardened I&C, and safety system upgrades, sustaining equipment retrofit demand for Mitsubishi Heavy Industries and Japanese suppliers.

Europe Nuclear Power Plant Equipment Market Trends

Europe accounts for approximately 20% of the nuclear power plant equipment market, anchored by France's large fleet, substantial German, UK, and Eastern European assets, and active government-backed new-build programs. European electricity generation in 2023 totaled 2,637 TWh, with nuclear contributing 22.3 percent (588 TWh), reflecting nuclear's centrality to Europe's decarbonization strategy, particularly post-Russia energy crisis. EU policy frameworks such as Clean Energy Directive, REPowerEU are supporting the life extension of existing reactors and selective new-build projects, most notably France's Flamanville EPR and the UK's Hinkley Point C and Sizewell C programs.

The regulatory environment is stringent (EASA, national nuclear regulators) with multi-year design approval cycles, creating higher engineering and certification costs but ensuring global acceptability of equipment designs. Competitive positioning reflects a mix of Framatome dominance in PWR/EPR segments, Westinghouse strength in AP1000 contracts, and emerging SMR vendors.

Supply-chain vulnerabilities identified during the Russia-Ukraine conflict are prompting Europe to diversify equipment sourcing and nearshore manufacturing; this is expanding opportunities for non-Russian suppliers while creating cost pressures on traditional supply arrangements. Investment opportunities in Europe concentrate on life-extension equipment for ageing fleets, SMR supply-chain development, and localised manufacturing of BOP components to reduce dependence on non-EU suppliers.

Competitive Landscape

The global nuclear power plant equipment market is largely oligopolistic with consolidated tendencies, dominated by a handful of highly experienced multinational corporations that possess advanced technologies, long-term service capabilities, and deep regulatory know how. Major players such as GE Vernova, Framatome, BWX Technologies, Inc. (BWXT), Rosatom / Atomstroyexport, Mitsubishi Heavy Industries, Ltd. (MHI), and Doosan Enerbility lead the market with extensive portfolios spanning reactor components, steam generators, pressure vessels, and balance-of-plant equipment. These companies benefit from long project lifecycles, high entry barriers, and strategic partnerships with national utilities, which limit the competitive influence of smaller suppliers.

The market’s high capital intensity and stringent safety and compliance requirements further reinforce the dominance of established players, creating substantial barriers for new entrants. Collaborative ventures and technology sharing among the leading firms are common, particularly in advanced reactor designs and modular construction techniques. Meanwhile, regional champions like Korea Electric Power Corporation (KEPCO/KHNP) and Holtec International strengthen competitive dynamics by securing sizeable contracts in Asia and the Americas.

Key Industry Developments:

- In May 2024 - GE Vernova / EDF: GE Vernova completed the sale of a portion of its Steam Power business to EDF, covering nuclear conventional island equipment, including Arabelle steam turbines, and related maintenance and upgrade activities outside the Americas. The transferred business now operates as Arabelle Solutions under EDF, strengthening EDF’s nuclear equipment portfolio while allowing GE Vernova to sharpen its focus on nuclear services in the Americas and SMR technologies such as the BWRX-300.

- In August, 2025 - X-energy, Amazon, KHNP & Doosan Enerbility: X-energy, Amazon, Korea Hydro & Nuclear Power, and Doosan Enerbility announced a strategic partnership to accelerate deployment of Xe-100 advanced SMRs in the U.S., targeting over 5 GW of new nuclear capacity by 2039. The collaboration covers reactor engineering, equipment supply chains, construction planning, and fuel (TRISO-X), with plans to mobilise up to USD 50 billion in public and private investment, strengthening the global nuclear power plant equipment and advanced reactor ecosystem.

Companies Covered in Nuclear Power Plant Equipment Market

- GE Vernova

- Framatome

- BWX Technologies, Inc. (BWXT)

- Holtec International

- Rosatom / Atomstroyexport

- Mitsubishi Heavy Industries, Ltd. (MHI)

- Doosan (Doosan Enerbility / Doosan Škoda Power)

- Toshiba Energy Systems & Solutions (TAES)

- Korea Electric Power Corporation (KEPCO / KHNP)

- Shanghai Electric Group

- Toshiba Corporation

- Orano

- EDF (Électricité de France)

- NuScale Power

- X‑Energy

Frequently Asked Questions

The global nuclear power plant equipment market is projected to be valued at US$ 18.1 Bn in 2026.

The Pressurized Water Reactors (PWR) segment is expected to account for approximately 58% of the Global Nuclear Power Plant Equipment Market by Service Model in 2026.

The market is expected to witness a CAGR of 4.2% from 2026 to 2033.

The Nuclear Power Plant Equipment Market is driven by government-led energy security and decarbonization mandates, accelerating large-scale reactor builds, localisation and indigenous manufacturing policies expanding domestic equipment supply chains, and the maturation of SMR technologies, shifting demand toward standardised, factory-built reactor island and balance-of-plant equipment across PWR, BWR, PHWR, and advanced reactor platforms.

Key opportunities in the Nuclear Power Plant Equipment Market arise from advanced and fourth-generation reactor deployments expanding demand for specialized and retrofit equipment, alongside strategic OEM partnerships and joint ventures that accelerate localisation, technology transfer, and long-term equipment supply across high-growth nuclear markets.

Key players in the Nuclear Power Plant Equipment Market include GE Vernova, Framatome, BWX Technologies, Inc. (BWXT), Rosatom / Atomstroyexport, Mitsubishi Heavy Industries, Ltd. (MHI), and Doosan Enerbility.