- Automotive Components & Materials

- Automotive Anti-Pinch Power Window Systems Market

Automotive Anti-Pinch Power Window Systems Market Size, Share, and Growth Forecast 2026 – 2033

Automotive Anti-Pinch Power Window Systems Market by Offering Type (Automatic and Manual), by Sales Channel (OEM and Aftermarket) and by Vehicle Type (Passenger vehicles, Light Commercial Vehicles (LCV), and Heavy Commercial Vehicles (HCV)) and Regional Analysis for 2026-2033

Automotive Anti-Pinch Power Window Systems Market Size and Trends Analysis

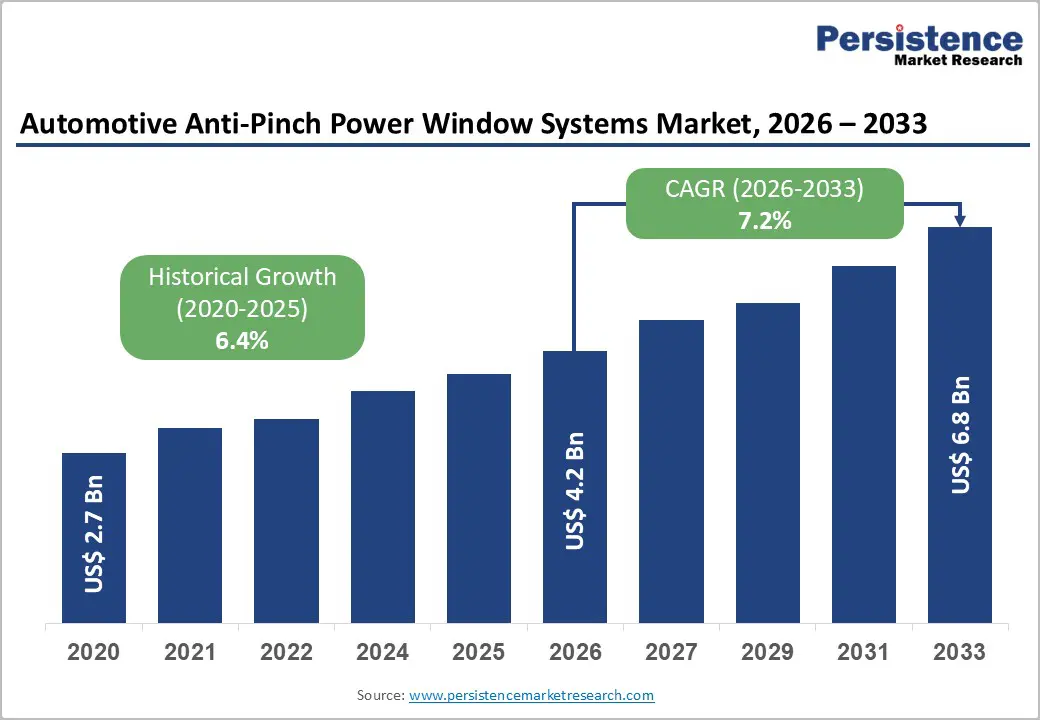

The global Automotive Anti-Pinch Power Window Systems Market size is likely to be valued at US$ 4.2 Billion in 2026 and is projected to reach US$ 6.8 Billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033. The market is experiencing steady expansion driven by stringent safety regulations, increasing vehicle electrification, rising consumer awareness regarding child safety, and the growing adoption of automated window closure systems with automatic obstruction detection capabilities across global automotive markets.

Key Market Highlights

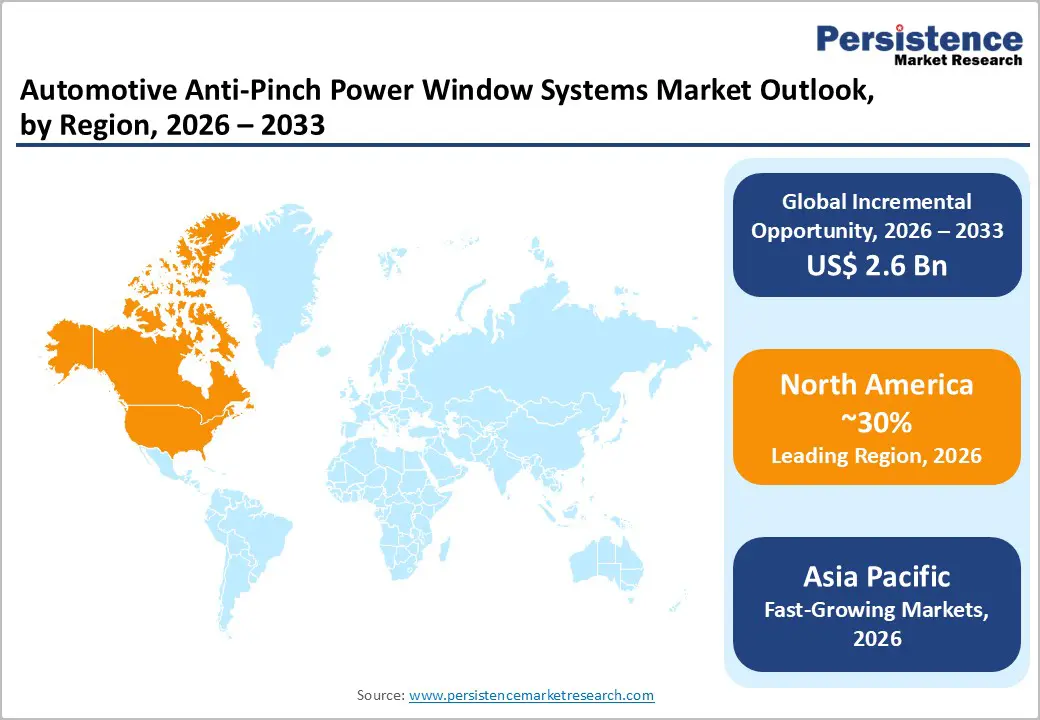

- Leading Region: North America commands approximately 30% of global anti-pinch power window systems market revenue, driven by stringent safety regulations, strong consumer safety consciousness, and established OEM manufacturing networks supporting regulatory compliance and technology leadership across premium and mainstream vehicle segments.

- Fastest Growing Region: Asia-Pacific exhibits fastest market growth trajectory at 8% CAGR through 2033, propelled by exceptional vehicle production growth in China and India, rapid electric vehicle electrification, and progressive adoption of international safety standards across developing automotive markets.

- Dominant Segment: Automatic anti-pinch power window systems command approximately 65% of market revenue, driven by regulatory mandates, technological maturity, and universal adoption across vehicle manufacturing, establishing automatic functionality as standard market offering across OEM and aftermarket channels.

- Fastest Growing Segment: Electric vehicle anti-pinch window systems represent fastest-expanding segment at 9% CAGR, reflecting accelerating EV adoption globally with EVs comprising 22% of new passenger vehicle sales in 2024, creating integrated demand for sophisticated electronic window control systems within advanced vehicle platforms.

- Key Market Opportunity: Commercial vehicle safety expansion represents high-potential growth opportunity through regulatory mandates enhancing driver safety in Heavy Commercial Vehicle segments, fleet operator demands for advanced safety features, and emerging vehicle electrification creating integrated demand for automated window control systems in commercial vehicle platforms.

| Key Insights | Details |

|---|---|

| Automotive Anti-Pinch Power Window Systems Market Size (2026E) | US$ 4.2 Bn |

| Market Value Forecast (2033F) | US$ 6.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.2% |

| Historical Market Growth (CAGR 2020 to 2024) | 6.4% |

Market Dynamics

Drivers - Stringent Regulatory Requirements and Child Safety Mandates

Regulatory frameworks including the Federal Motor Vehicle Safety Standard (FMVSS-118) and the Cameron Gulbransen Kids Transportation Safety Act of 2007 have established mandatory requirements for automatic reversal systems and obstruction detection in power window mechanisms, particularly for express-up windows that operate through single-press actuation. The NHTSA has progressively strengthened safety standards, requiring automatic reversal when window systems detect obstruction resistance exceeding 100 Newtons, with emerging regulatory proposals recommending reduction to 40 Newtons to enhance child protection. European regulatory frameworks and international safety organizations including Euro NCAP have similarly emphasized anti-pinch safety features as critical components of vehicle occupant protection.

Rising Global Vehicle Production and Electric Vehicle Electrification Trends

Global automotive production reached approximately 92 million vehicles in 2024, with passenger car production accounting for 75.5 million units, creating substantial baseline demand for power window systems and safety components. China leads global automotive production with 31 million vehicles in 2024, representing more than 33% of worldwide output, while India and Mexico are emerging as high-growth production hubs, with India's automotive sector growing at robust rates driven by expanding middle-class consumers and increased vehicle ownership. The accelerating transition toward electric vehicles (EVs) globally, with EVs comprising 22% of new passenger vehicle sales in 2024 compared to just 2.7% in 2019, represents a significant growth in driver as electric vehicle manufacturers prioritize advanced safety systems and convenient automated features.

Restraints - High Implementation Costs and Complexity in Integration

Anti-pinch power window systems require integration of multiple sophisticated components including infrared sensors, force-sensing mechanisms, electronic control units, motor drivers, and communication interfaces that substantially increase system costs compared to conventional manual or basic power window mechanisms. Automatic Reversal Systems (ARS) utilizing non-contact infrared detection, contact-based force measurement, or speed-monitoring technologies add $200-400 per vehicle depending on technology sophistication and sensor complexity, creating significant cost burdens particularly for cost-sensitive segments including budget passenger vehicles and commercial vehicle applications. Original Equipment Manufacturers (OEMs) operating in competitive markets with tight margin structures face challenges justifying anti-pinch system expenditures when consumer price sensitivity remains elevated, particularly in emerging markets where cost-conscious buyers prioritize basic functionality over advanced safety features.

Supply Chain Vulnerabilities and Semiconductor Component Availability

The automotive anti-pinch power window systems market is highly dependent on semiconductor components, microcontrollers, and integrated circuits supplied by specialized manufacturers including NXP Semiconductors, Microchip Technology, and Infineon Technologies, whose supply chains have experienced periodic disruptions affecting system availability and production schedules. Raw material price volatility, particularly for copper used in motors and wiring harnesses, aluminum in mechanical components, and rare-earth metals in advanced sensors, creates unpredictable cost structures that complicate pricing strategies and margin management for system manufacturers. Geopolitical supply chain disruptions, trade tensions, and regional manufacturing relocations have impacted on consistent component availability, with semiconductor shortages in 2021-2023 demonstrating vulnerability of concentrated supplier bases to external disruptions affecting automotive production schedules globally.

Opportunities - Autonomous Vehicle Development and Advanced Driver Assistance Systems (ADAS) Integration

The rapid development of autonomous vehicles and advanced driver assistance systems represents a significant growth opportunity as self-driving vehicle platforms require comprehensive sensor networks and automated safety systems including sophisticated window control mechanisms that can operate independently or be manually overridden. Level 2 and Level 3 autonomous vehicles emerging in markets including North America, Europe, and Asia-Pacific incorporate enhanced sensor arrays, automated climate control, and intelligent cabin management systems that necessitate advanced anti-pinch window technology capable of operating seamlessly within broader vehicle automation ecosystems. Integration of anti-pinch power windows with vehicle-to-everything (V2X) communication systems, weather-sensing capabilities, and predictive safety algorithms create opportunities for manufacturers to develop next-generation window control systems offering enhanced functionality beyond basic safety features.

Growth in Premium Vehicle Segment and Connected Vehicle Technologies

The expanding premium and luxury vehicle segment, particularly in emerging markets including China and India where increasing affluent consumer populations demand sophisticated vehicle features, represents a high-potential market opportunity for advanced anti-pinch window systems with enhanced functionality. Premium vehicle manufacturers emphasize differentiated customer experiences through integration of smart window technologies offering gesture control, rain sensing, automatic opening and closing, and integration with vehicle climate management systems that create compelling value propositions justifying premium pricing. Connected vehicle platforms incorporating Internet of Things (IoT) capabilities, cloud-based vehicle management systems, and mobile device integration are increasingly incorporating intelligent window control features enabling remote operation, scheduling, and diagnostic monitoring of window systems.

Category-wise Analysis

Offering Type Insights

Automatic anti-pinch power window systems commanding approximately 65% of total market revenue represent the dominant segment driven by regulatory mandates requiring automatic reversal functionality, rising consumer safety consciousness, and technological maturity of automatic detection mechanisms. Automatic reversal systems utilizing infrared proximity detection, contact-based force sensing, or speed-monitoring technologies automatically detect obstructions and reverse window direction without manual intervention, providing superior safety protection particularly for unattended vehicle operations and unsupervised child occupants. FMVSS-118 S5 compliance requirements explicitly mandate automatic reversal on express-up windows, creating regulatory imperative for OEM adoption across North American vehicles and increasingly across international markets adopting harmonized safety standards.

Manual override segments accounting for approximately 30% of market revenue represent supplementary functionality integrated with automatic systems to provide user control options and address edge-case scenarios where automatic functionality may be inadvertently inhibited.

Vehicle Type Insights

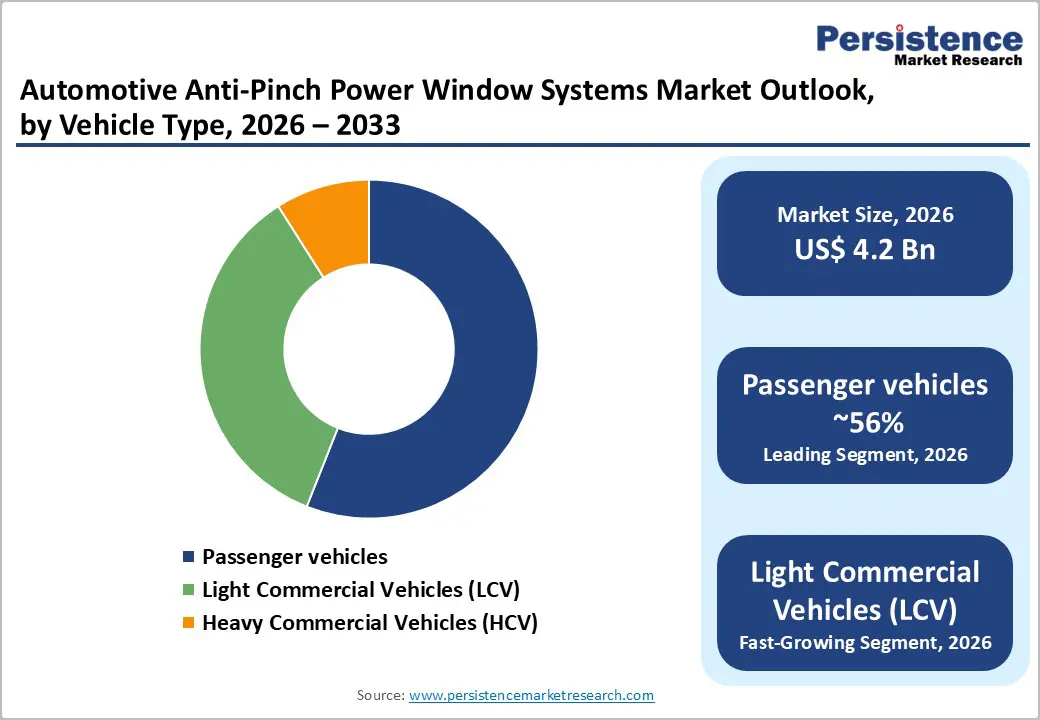

Passenger vehicles representing sedans, hatchbacks, crossovers, and utility vehicles command approximately 58% of anti-pinch power window systems market revenue, driven by global passenger vehicle production of 75.5 million units in 2024 and accelerating EV adoption targeting passenger vehicle segment. Premium passenger vehicle segments emphasizing advanced safety and convenience features have achieved near-universal adoption of anti-pinch systems, while mainstream passenger vehicles increasingly incorporate anti-pinch functionality as cost-competitiveness improves and regulatory requirements expand globally.

Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs) collectively represent approximately 32% of market revenue, with LCVs including compact trucks and vans commanding larger share than HCVs including full-size trucks and buses. Commercial vehicle manufacturers are increasingly adopting anti-pinch power window systems driven by driver safety regulations, insurance requirements, and fleet operator demands for advanced safety features that reduce accident liability and occupational injury risks.

Sales Channel Insights

Original Equipment Manufacturer (OEM) sales channel commanding approximately 72% of anti-pinch power window systems market revenue represents the primary distribution pathway through which anti-pinch systems are integrated into vehicles during manufacturing processes. OEM adoption is driven by regulatory mandates, competitive differentiation strategies, and consumer safety expectations that compel vehicle manufacturers to incorporate anti-pinch functionality as standard or premium feature offerings. Major automotive manufacturers including Volkswagen, General Motors, Toyota, Honda, Ford, BMW, Mercedes-Benz, Volvo, SAIC, and NIO are standardizing anti-pinch systems across vehicle platforms in response to regulatory requirements and consumer preference for integrated safety features.

Aftermarket sales channel representing approximately 28% of market revenue encompasses retrofit installations, replacement components, and upgrade packages for existing vehicles lacking integrated anti-pinch functionality. Aftermarket adoption is driven by vehicle owners seeking enhanced safety features, insurance incentives for safety upgrades, and fleet operators retrofitting commercial vehicle fleets with anti-pinch systems to reduce occupational injury risks and liability exposures.

Regional Insights

North America Anti-pinch Power Window Systems Market Trends

North America commands approximately 30% of global anti-pinch power window systems market revenue, with the United States representing the dominant regional market supported by stringent FMVSS-118 regulations requiring automatic reversal systems on express-up windows. The NHTSA regulatory framework has established clear mandate for automatic reversal functionality, driving universal adoption among OEMs and creating established market infrastructure supporting suppliers, installers, and aftermarket providers. The U.S. automotive market produced 11.4 million vehicles in 2024, comprising approximately 13% of global output, with North American vehicle production remaining stable supporting consistent demand for anti-pinch window systems.

North American aftermarket distribution networks are well-established, supporting robust retrofit installation capacity and replacement component availability for vehicle owners seeking safety upgrades. The region is expected to grow at 6% CAGR through 2033, with growth moderating relative to Asia-Pacific reflecting higher baseline adoption rates and market maturity in established vehicle segments.

Europe Automotive Anti-pinch Power Window Systems Market Trends

Europe represents approximately 25% of global anti-pinch power window systems market revenue, driven by stringent vehicle safety regulations, strong consumer safety consciousness, and regulatory harmonization initiatives advancing standardized safety requirements across member states. European Union vehicle safety directives and Euro NCAP protocols emphasize advanced safety features including anti-pinch window systems as critical occupant protection mechanisms, establishing regulatory expectations and driving widespread adoption across European vehicle manufacturers.

Germany leads European automotive manufacturing with approximately 2.5 million vehicles in 2024, establishing technology standards and innovation benchmarks influencing broader European market adoption patterns. European electric vehicle adoption is progressing rapidly, with BEVs comprising 17.8% of new registrations in 2024 and growth accelerating through 2026, supporting demand for integrated anti-pinch systems in advanced vehicle platforms. Regulatory harmonization initiatives across EU member states are facilitating standardized safety requirements and component specifications, enabling manufacturers to achieve economies of scale through cross-border production and distribution networks.

Asia Pacific Anti-pinch Power Window Systems Market Trends

Asia Pacific represents the fastest-growing regional market, commanding approximately 28% of global anti-pinch power window systems revenue with projected growth at 8-9% CAGR, driven by exceptional vehicle production growth and rapid electric vehicle adoption. China dominates Asia-Pacific automotive production with 31 million vehicles in 2024 and emerging EV leadership with 48% of passenger vehicles being electric, establishing the region as critical growth engine for anti-pinch system manufacturers.

China's advanced manufacturing capabilities, technology innovation ecosystem, and domestic consumer demand for safety-enhanced vehicles are driving rapid adoption of anti-pinch systems across domestic and export-oriented vehicle production. India's automotive sector is experiencing accelerating growth with 26.9 million vehicles produced in 2026, driven by expanding middle-class consumer base and rising vehicle ownership rates, creating substantial untapped market opportunities for anti-pinch system penetration.

Competitive Landscape

The Automotive Anti-Pinch Power Window Systems Market exhibits a moderately consolidated competitive structure with specialized automotive component suppliers and integrated systems manufacturers controlling approximately 55% of aggregate market revenue. Tier 1 suppliers including Bosch, Continental, Denso, Valeo, Aisin Seiki, and ZF Friedrichshafen leverage extensive automotive supply relationships, manufacturing capabilities, and technological expertise to dominate market competition. These established suppliers differentiate through advanced sensor technologies, integrated control systems, and comprehensive solutions addressing regulatory compliance and manufacturer requirements.

Key Market Developments

- In July 2024, Valeo SA introduced integrated smart-window control platform combining window lift, lighting, and sunroof functions into single software-defined interface, improving OEM integration flexibility and enabling advanced vehicle automation features.

- In February 2024, Continental activated a new competitive R&D strategy which focuses attention towards enhancing the specific characteristics of automotive R&D networks globally.

Companies Covered in Automotive Anti-Pinch Power Window Systems Market

- Aisin Seiki

- Bosch

- Continental

- Denso

- Hella GmbH

- Infineon

- Microchip

- NXP Semiconductors

- Valeo

- ZF Friedrichshafen

- Others Key Players

Frequently Asked Questions

The Global Automotive Anti-Pinch Power Window Systems Market is projected to reach US$ 6.8 Billion by 2033, expanding from US$ 4.2 Billion in 2026 at a CAGR of 7.2%.

The market is primarily driven by stringent FMVSS-118 and international safety regulations mandating automatic reversal systems; rising global vehicle production exceeding 92 million units in 2024; rapid electric vehicle electrification with EVs comprising 22% of new passenger vehicle sales globally.

Automatic anti-pinch power window systems dominate approximately 65-70% of market revenue, driven by regulatory mandates requiring automatic reversal functionality on express-up windows.

North America commands approximately 30% of global market revenue as leading region.

The key players in Backhoe Loader are Bosch, Denso Corporation; Valeo, Continental, Aisin Seiki, and ZF Friedrichshafen.