- Energy Storage Solutions

- Critical Power and Cooling Market

Critical Power and Cooling Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Critical Power and Cooling Market by Solution Type (Critical Power Type, Critical Cooling Type), End-user (IT & Telecommunication, Industrial, Commercial, Transportation, Others), and Regional Analysis for 2026 - 2033

Critical Power and Cooling Market Size and Trends Analysis

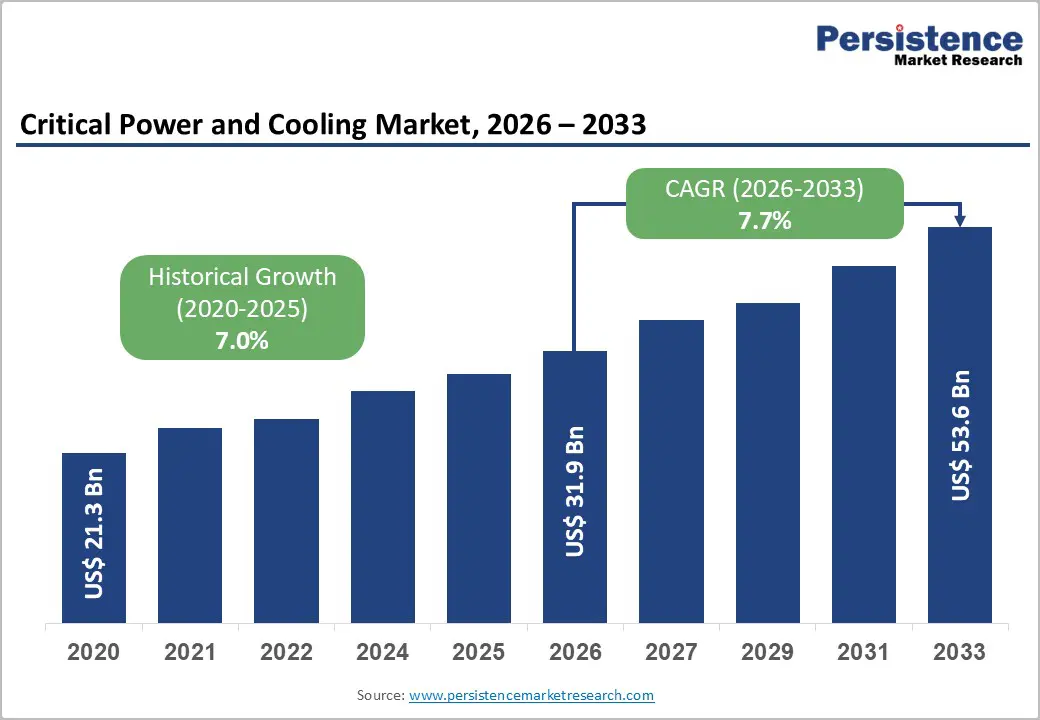

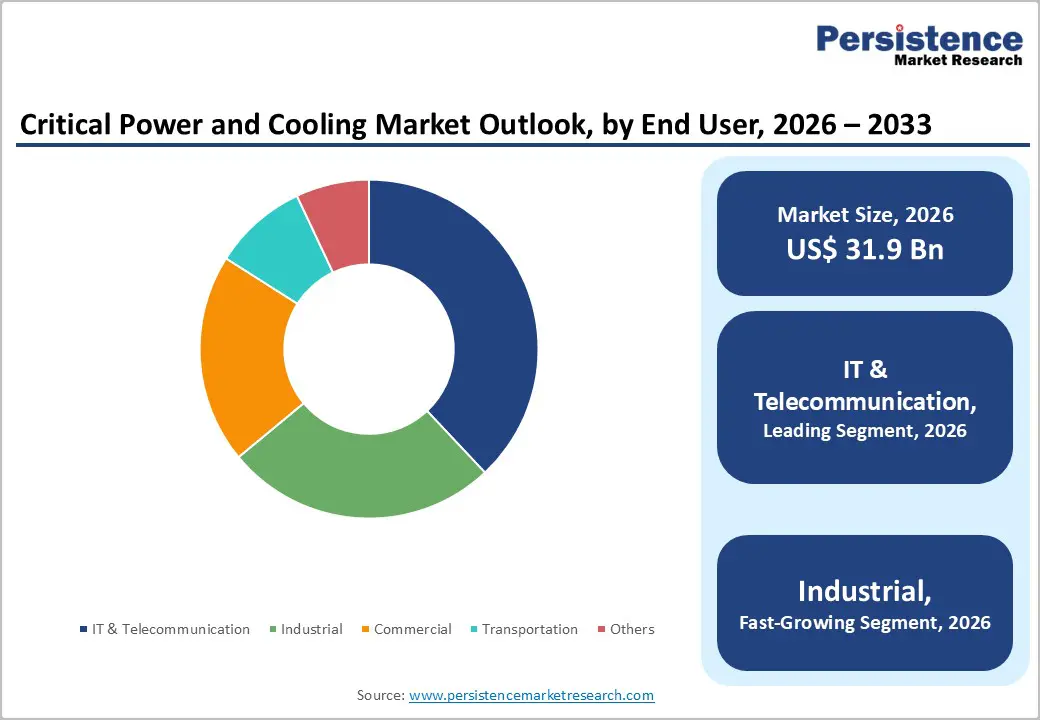

The global critical power and cooling market size is likely to be valued at US$ 31.9 billion in 2026 and is projected to reach US$ 53.6 billion by 2033, growing at a compound annual growth rate of 7.7% during the forecast period.

The market's expansion is primarily driven by the exponential growth of artificial intelligence-powered data centres requiring sophisticated thermal management, the acceleration of cloud computing adoption across enterprises, and increasingly stringent regulatory requirements mandating energy efficiency and sustainable operations.

The proliferation of hyperscale data centre construction, particularly in Asia-Pacific and North America, combined with the electrification of industrial processes and the rollout of 5G telecommunications infrastructure, is creating unprecedented demand for reliable critical power protection and advanced cooling solutions. As organisations globally transition toward digital-first operational models, the criticality of uninterrupted power supply and optimal thermal management has emerged as a fundamental competitive advantage and operational necessity.

Key Industry Highlights:

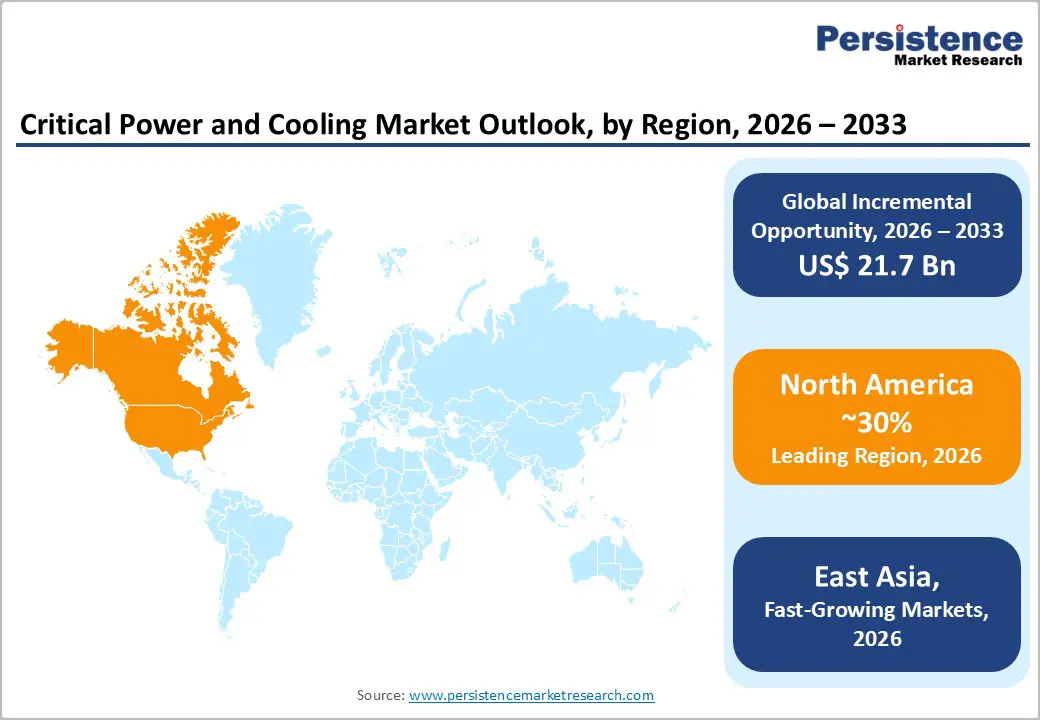

- Regional Leadership: North America dominates the global critical power and cooling market with ~30% share, supported by hyperscale data center concentration, AI infrastructure investments, and strong enterprise cloud adoption in the United States.

- Fastest-Growing Regional Market: East Asia accounts for ~22% share and represents the fastest-growing regional market, driven by large-scale digital infrastructure programs, aggressive AI compute deployment, and expanding cloud ecosystems in China, Japan, and South Korea.

- Solution Type Dominance: Critical Power solutions lead the market with ~70% share, reflecting the essential role of uninterruptible power supply systems, power distribution units, and power conditioning equipment in mission-critical environments.

- Rapidly Growing Solutions: Critical Cooling solutions are the fastest-growing segment, driven by rising rack power densities, regulatory pressure on energy efficiency, and the shift toward liquid and hybrid cooling architectures.

- Leading Industry: IT & Telecommunication remains the largest end-use segment with ~38% share, anchored by cloud computing expansion, AI workload growth, and global 5G network deployment.

| Key Insights | Details |

|---|---|

| Critical Power and Cooling Market Size (2026E) | US$ 31.9 Bn |

| Market Value Forecast (2033F) | US$ 53.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.0% |

Market Dynamics

Artificial Intelligence and High-Density Computing Infrastructure Requirements

The emergence of generative artificial intelligence and machine learning applications has fundamentally transformed data centre power and thermal requirements, creating strong demand within the Critical Power and Cooling Market. AI training and inference workloads consume substantially more electrical power per unit of computing capacity than traditional enterprise applications. Graphics processing units (GPUs) and specialised AI accelerators now operate at thermal densities of 50–100 kilowatts per rack, compared with historical data centre densities of 5–10 kilowatts per rack. AI-driven data centre power demand in the United States is projected to rise from 4 gigawatts in 2024 to 123 gigawatts by 2035, reflecting a more than thirtyfold increase.

Similar acceleration trends are emerging globally, with cloud hyperscalers and new market entrants investing over US$ 200 billion annually in data centre capital expenditure to support AI workloads. The Critical Power and Cooling Market is therefore evolving rapidly to deliver higher-capacity, highly reliable solutions, as even brief power or cooling disruptions can lead to significant computational losses. This shift is accelerating innovation in modular power architectures, liquid cooling technologies, and tightly integrated power–cooling systems tailored for high-density computing environments.

Global Digitalization and Cloud Computing Expansion

The permanent shift toward cloud-first enterprise architecture and digital service delivery across all industry sectors has established continuous, high-reliability power and cooling infrastructure as foundational business requirements.

The European Commission's statistical data indicates that the information and communication services sector comprises approximately 1.4 million enterprises across the European Union alone, employs nearly 7.2 million people, and generated approximately US$667 billion in value added in 2022. Within this ecosystem, hyperscale data centres function as the physical infrastructure supporting cloud services, edge computing, content delivery networks, and digital transformation initiatives. The demand for data centre capacity continues to expand rapidly as enterprises increasingly adopt software-as-a-service applications, migrate on-premises workloads to cloud platforms, and implement big data analytics for a competitive advantage.

Internet penetration continues to advance globally, with approximately 5.5 billion people using the internet as of 2024, representing 68% of the world's population and projected to exceed 6 billion users by 2025. This expansion directly correlates with increased data traffic, storage requirements, and processing demands, driving corresponding growth in data centre infrastructure. The critical power and cooling market benefits from this structural shift as data centre operators must continually upgrade their electrical and thermal infrastructure to accommodate growing volumes while meeting increasingly rigorous availability targets.

Regulatory Mandates for Energy Efficiency and Sustainability

Government regulatory frameworks globally are imposing increasingly stringent energy-efficiency and environmental-performance requirements on data centre operators, creating strong incentives for investment in advanced critical power and cooling solutions. The European Union's revised Energy Efficiency Directive (EED), which entered into force in October 2023, mandates that data centre operators with total rated power exceeding 500 kilowatts publicly report detailed energy performance metrics, including power utilisation effectiveness (PUE), temperature set points, waste heat utilisation, water consumption, and renewable energy usage.

Data centres exceeding 1 megawatt of total power must implement waste heat utilisation systems or justify technical or economic infrastructure, effectively requiring operators to invest in advanced thermal recovery and integration infrastructure.

Germany's implementation of the EED includes additional requirements mandating 100% renewable energy sourcing by 2027 and a minimum 50% incorporation of renewable energy by 2024, alongside explicit PUE and waste heat reduction targets. In the United States, state-level regulatory bodies and utility companies have begun requiring data center operators to fund infrastructure upgrades necessary to support increased electrical demand, while some states have imposed moratoriums on new data center construction in regions with constrained grid capacity, as occurred in Dublin, Ireland in 2024 when new data center construction was halted due to electricity consumption reaching approximately 20% of regional supply.

These regulatory developments are directly accelerating investment in more efficient cooling technologies, particularly liquid cooling solutions that reduce energy consumption by up to 40% compared to air-based systems, intelligent power distribution and monitoring systems, and integrated facilities management platforms that optimise energy utilisation across critical infrastructure components.

Restraint - Extreme Capital Intensity and Infrastructure Investment Requirements

The deployment of advanced critical power and cooling infrastructure requires substantial capital investment that constrains market penetration, particularly among mid-market enterprises and smaller data centre operators. Enterprise-grade uninterruptible power supply systems, integrated power conditioning equipment, and liquid-cooling distribution systems entail high fixed costs that must be amortised over multi-year operational lifecycles.

The infrastructure modernisation required to support AI-density workloads often necessitates complete facility redesign, including electrical distribution system upgrades, cooling loop reconfiguration, and auxiliary systems modifications. These capital requirements create market barriers for smaller operators and regional data center providers, potentially favouring consolidation toward larger hyperscale operators with access to substantial capital markets and economies of scale in infrastructure deployment.

Opportunity - Liquid Cooling Technology Maturation and Market Penetration

The rapid maturation of liquid cooling technologies, including direct-to-chip cooling, chassis-level immersion, and hybrid air–liquid architectures, presents strong market expansion opportunities within the Critical Power and Cooling Market. Historically, liquid cooling solutions were confined to niche applications such as high-performance computing due to concerns related to complexity, cost, and long-term reliability. Recent technological advancements have repositioned liquid cooling as a viable and increasingly standardized solution for mainstream data centre deployments.

Leading companies such as Schneider Electric, Daikin, and Vertiv, as well as specialized innovators such as Green Revolution Cooling, Iceotope, and CoolIT Systems, have introduced production-ready systems capable of supporting continuous, mission-critical operations. The April 2025 launch of Daikin’s Pro-C Computer Room Air Handler, offering certified cooling capacities ranging from 30 kilowatts to 210 kilowatts, with advanced controls, energy-efficient EC fans, and integrated power-failure protection, reflects this enterprise-grade maturity.

Adoption is accelerating most rapidly in the Asia-Pacific region, where operators are deploying high-density AI-focused infrastructure across both new builds and retrofitted facilities. Liquid cooling addresses a critical limitation of traditional air-based systems, which can consume up to 40% of total data centre power and struggle to support rack densities beyond 50 kilowatts without extensive redesign. As a result, the shift toward proven and standardized liquid cooling technologies is creating sustained opportunities for equipment manufacturers, system integrators, and service providers supporting next-generation thermal infrastructure.

Edge Computing and Distributed Data Centre Infrastructure at 5G Micro-Regions

The deployment of 5G wireless networks and the architectural shift toward distributed edge computing create substantial new market opportunities for compact, modular critical power and cooling solutions optimised for smaller-scale, geographically dispersed infrastructure. Traditional data centre design concentrates computing resources in hyperscale facilities, but 5G infrastructure architecture requires computational capacity distributed across thousands of small cell sites, macro cell sites, and edge computing nodes positioned throughout metropolitan areas and rural regions. This distributed architecture necessitates ruggedised, compact critical power protection and thermal management solutions designed for space-constrained environments.

India's telecommunications sector provides an instructive example of this opportunity scale: as of June 2025, India recorded 1.21 billion mobile subscribers with 86.09% tele-density and 979 million internet subscribers, with 5G networks already contributing nearly 25% of total wireless data usage in FY25 after accelerated deployment over the previous two years. The expansion of 5G infrastructure, combined with cloud-native application architectures that require computational resources at network edges to minimise latency, is driving demand for specialised, critical power and cooling systems designed for distributed deployment across telecommunications networks, mobile edge computing facilities, and remote locations.

Category-wise Analysis

Solution Type Insights

The Critical Power Type segment commands 70% of the global critical power and cooling market as of 2026, reflecting the fundamental criticality of uninterruptible power supply and power conditioning systems for data centre and mission-critical facility operations. This segment encompasses uninterruptible power supplies (UPS) systems, automatic transfer switches, power distribution units (PDUs), surge protection equipment, and integrated power conditioning solutions that protect sensitive IT equipment from electrical anomalies, including voltage sags, surges, frequency variations, and complete power outages.

The dominance of the critical power type segment reflects several structural factors: first, power reliability remains a non-negotiable operational requirement, with severe financial consequences for interruptions, providing a strong justification for investment in redundant, high-reliability power protection systems. Second, regulatory and compliance requirements across regulated industries, including financial services, healthcare, telecommunications, and government operations, mandate specific standards for power availability and reliability. Third, the proliferation of AI-dense data centre configurations has intensified power quality requirements, as power disturbances can corrupt computational operations and compromise system stability.

The Critical Cooling Type segment, while accounting for a smaller current market share, is experiencing the fastest growth trajectory in the Critical Power and Cooling Market in response to rising thermal density requirements and escalating energy efficiency mandates. Advanced cooling technologies, including liquid cooling systems, high-efficiency, precision air conditioning units, immersion cooling solutions, and integrated thermal management platforms, are the fastest-growing subcategory as data center operators transition from legacy air-based cooling approaches to next-generation thermal management solutions.

Industry Insights

The IT & Telecommunication sector dominates the Global Critical Power and Cooling Market, with approximately 38% market share in 2026, reflecting the sector's structural reliance on highly available, continuously operating computing infrastructure and network systems. This segment encompasses cloud service providers (hyperscalers), telecommunications carriers, internet service providers, software-as-a-service platforms, and enterprise data center operations that require mission-critical power protection and thermal management for revenue-generating infrastructure.

The IT & Telecommunication sector's dominance reflects both its scale, which is telecommunications infrastructure that comprises approximately 1.4 million enterprises and 7.2 million employees across the European Union alone, and the catastrophic business impact of power interruptions or thermal failures.

The sector's growth trajectory is primarily driven by the expansion of cloud computing, the buildout of AI infrastructure, 5G network deployment, and the accelerating adoption of data-intensive applications. The International Telecommunication Union estimates global 5G subscribers will grow from 290 million in 2024 to 770 million by 2028, with 5G data traffic expanding rapidly in India specifically. 5G data traffic increased threefold year-over-year in 2024, reaching 35.5% of total mobile data traffic and projected to surpass 4G by mid-2026.

The Industrial segment is positioned as the fastest-growing Industry within the Critical Power and Cooling Market, driven by increasing adoption of IoT (Internet of Things) devices, automation systems, and digital twin technologies that require reliable computational infrastructure and controlled environmental conditions.

Regional Insights and Trends

North America Critical Power and Cooling Market Trends

North America commands approximately 30% of the global critical power and cooling market, driven by concentrated cloud hyperscaler investment, advanced technology adoption, and substantial enterprise digital infrastructure spending. The United States accounts for the majority of regional market activity, characterized by aggressive data center expansion, particularly in Virginia, which hosts the highest concentration of critical infrastructure in the United States.

The regulatory environment in North America is increasingly favorable for investment in critical power and cooling infrastructure, though nuances vary by state and utility jurisdiction. The U.S. Infrastructure Investment and Jobs Act (IIJA), enacted in 2021, allocated substantial funding for electrical grid modernization and power generation capacity expansion, indirectly supporting data center infrastructure development by improving underlying grid reliability. However, specific states, including Virginia and Wisconsin, have begun implementing tariff structures requiring hyperscale data centre operators to fund infrastructure upgrades necessary to support their power demand, shifting costs toward large consumers and creating incentives for more efficient thermal management

East Asia Critical Power and Cooling Market Trends

East Asia, comprising China, Japan, and South Korea, accounts for approximately 22% of the Global Critical Power and Cooling Market and represents the fastest-growing regional market in the forecast period. China is the dominant force in the region, driven by massive government investment in digital infrastructure, aggressive adoption of cloud computing, and rapid AI infrastructure buildout. According to the China Internet Network Information Center, China reached 1.108 billion internet users by December 2024, with 1.105 billion mobile internet users representing 99.7% of netizens, reflecting near-universal digital connectivity.

The diversification of access devices, including desktops, laptops, tablets, smart TVs, wearables, smart home devices, and connected vehicles, signals rising demand for resilient, high-bandwidth optical networking infrastructure and supporting power/cooling systems.

Japan and South Korea are significant but secondary markets in East Asia. Japan's advanced technology sector, including robotics, automotive, and semiconductor manufacturing, drives substantial critical power and cooling infrastructure requirements. South Korea's competitive strength in semiconductor manufacturing and advanced telecommunications has established it as a technology leader in power and cooling solutions, with companies including Mitsubishi Electric and Samsung developing and deploying sophisticated critical infrastructure technologies.

Advanced landscape in East Asia is evolving rapidly, with traditional Japanese manufacturers (Mitsubishi Electric, Daikin) competing against emerging Chinese domestic suppliers and international players such as Schneider Electric, Vertiv, and ABB. Government policy initiatives, including China's Green Data Center promotion programs and Korea's advanced manufacturing initiatives, are accelerating technology adoption and creating strong demand for high-efficiency critical power and cooling solutions.

Europe Critical Power and Cooling Market Trends

Europe accounts for approximately 18% of the Global Critical Power and Cooling Market, characterized by highly developed digital infrastructure, stringent energy-efficiency regulations, and a strong emphasis on sustainability. The European Union's information and communication services sector comprises 1.4 million enterprises generating US$ 667 billion in value added, with Internet penetration reaching 94% as of 2025. Germany is the largest single contributor to EU sectoral value added at 22.8%, followed by France, with the five largest EU economies collectively generating nearly two-thirds of total EU value added in information and communication services.

The regulatory environment in Europe is the most stringent globally, with the revised Energy Efficiency Directive mandating comprehensive reporting of data centre energy performance metrics and requiring the implementation of waste heat utilisation systems in facilities with power consumption exceeding 1 megawatt. These regulatory requirements are driving substantial investment in advanced critical cooling technologies, particularly liquid-cooling solutions that reduce energy consumption and support waste-heat recovery. Germany's accelerated implementation of the EED, with 100% renewable energy requirements by 2027, is creating particularly strong incentives for efficient critical infrastructure solutions.

Competitive Landscape

The global critical power and cooling market exhibits an oligopolistic structure, characterised by the strong presence of a limited number of multinational companies with extensive global footprints and integrated solution portfolios. Leading players compete on the basis of technological reliability, energy efficiency, scalability, and long-term service capabilities, particularly for data centres, healthcare facilities, and industrial infrastructure.

Schneider Electric, Vertiv Group, Eaton Corporation, ABB, Siemens, and Delta Electronics dominate the competitive landscape, benefiting from strong brand recognition, broad distribution networks, and recurring service revenues. These companies continue to strengthen their positions through investments in intelligent power management, liquid and hybrid cooling technologies, and modular infrastructure solutions. While regional and niche players remain active, high capital requirements, stringent uptime standards, and long customer replacement cycles create substantial entry barriers.

Key Industry Developments

- On Oct 15, 2025, Daikin Applied - Daikin Applied strengthened its leadership in the Critical Power and Cooling market by advancing its mission-critical data centre cooling portfolio through innovative product launches, strategic acquisitions, and a dedicated data centre business unit. Key developments include the introduction of the Magnitude® WME-C Quad Chiller with magnetic-bearing technology for high-capacity, high-uptime data centres, expansion of next-generation chiller and air-handling solutions, acquisition of DDC Solutions to add modular and rack-level cooling capabilities, and expansion of testing and manufacturing capacity to support scalable, reliable cooling for AI- and cloud-driven data centre infrastructure.

- On Oct 08, 2025, Delta Electronics showcased its integrated critical power and cooling solutions for high-density, AI-driven data centres at Data Centre World Asia 2025, highlighting containerised data centre architectures, liquid-cooling technologies, and modular power infrastructure. Key developments included a 20-foot Containerised Data Centre with a liquid-to-air CDU delivering up to 80 kW of cooling, in-rack liquid-cooling CDUs supporting up to 200 kW per rack, and scalable power distribution platforms, such as power skids and HVDC-enabled systems. The portfolio strengthens energy efficiency, reliability, and sustainability for next-generation data centre power and cooling infrastructure.

Companies Covered in Critical Power and Cooling Market

- ABB

- Asetek A/S

- Cyber Power Systems

- Daikin Industries Ltd.

- Delta Electronic, Inc.

- Eaton Corporation

- General Electric

- Johnson Controls, Inc.

- Rittal GmbH & Co. Kg

- Schneider Electric

- Siemens

- Socomec

- Stulz GmbH

- Vertiv Co.

Frequently Asked Questions

The global critical power and cooling market is projected to be valued at US$ 31.9 Bn in 2026.

The Critical Power Type is expected to account for approximately 70.0% of the global Critical Power and Cooling Market by Solution Type in 2026.

The market is expected to witness a CAGR of 7.7% from 2026 to 2033.

The Critical Power and Cooling Market is driven by AI-led high-density computing, rapid cloud and digital infrastructure expansion, and increasingly stringent global energy-efficiency and sustainability regulations.

Key opportunities in the Critical Power and Cooling Market include the rapid adoption of liquid cooling technologies for high-density AI workloads and the expansion of modular power and cooling solutions for 5G-enabled edge and distributed data centre infrastructure.

The key players in the Critical Power and Cooling Market include Schneider Electric, Vertiv Group, Eaton Corporation, ABB, Siemens, and Delta Electronics.