- Pharmaceuticals

- Oral Antidiabetic Treatment Market

Oral Antidiabetic Treatment Market Size, Share, and Growth Forecast, 2026 – 2033

Oral Antidiabetic Treatment Market by Drug Class (Biguanides, Sodium-glucose Co-Transporter-2 (SGLT-2) Inhibitors, Dipeptidyl Peptidase-4 (DPP-4) Inhibitors, Sulfonylureas, Thiazolidinediones, Meglitinides, Alpha-glucosidase Inhibitors, Others), Route of Administration (Oral, Sublingual, Buccal), End-User (Hospitals, Drug Stores, Pharmacy Stores, Diabetes Treatment Centers, Others), and Regional Analysis for 2026-2033

Oral Antidiabetic Treatment Market Share and Trends Analysis

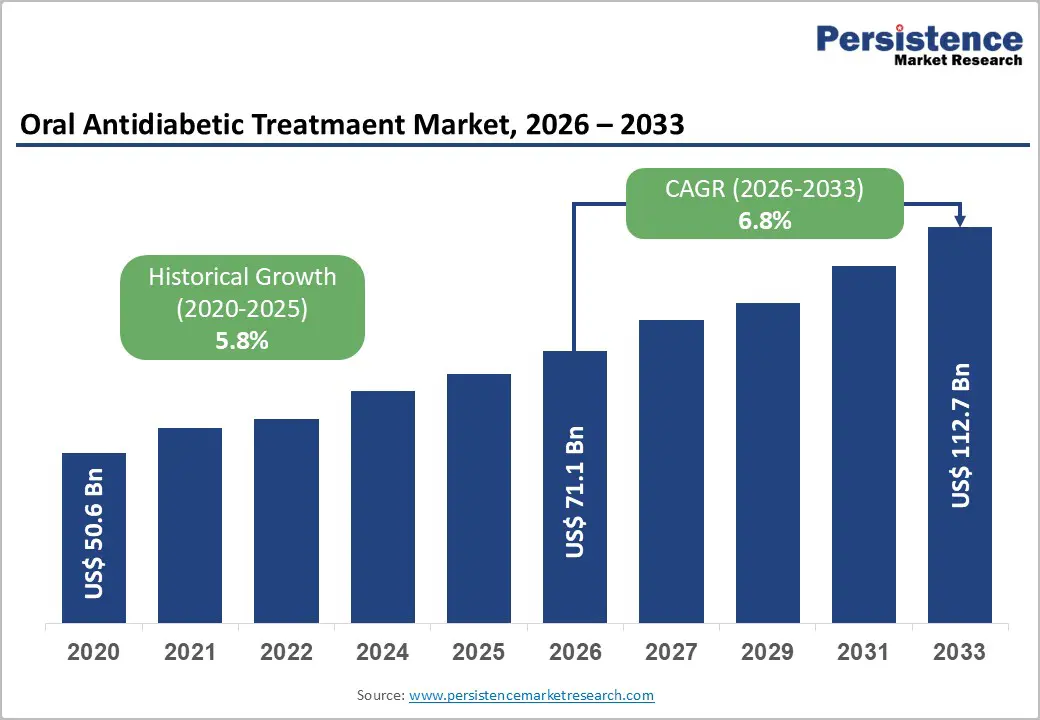

The global oral antidiabetic treatment market size is likely to be valued at US$ 71.1 billion in 2026, and is projected to reach US$ 112.7 billion by 2033, growing at a CAGR of 6.8% during the forecast period 2026−2033.

Demand for diabetes management solutions is increasing as aging populations and sedentary urban lifestyles are contributing to a higher incidence of type 2 diabetes. Health authorities are expanding awareness initiatives and structured screening programs to promote early diagnosis and timely pharmacological intervention. Physicians are prescribing oral glucose lowering agents as first line therapy to manage glycemic control and delay disease progression. Pharmaceutical companies are advancing combination regimens and patient centric dosage formulations to improve adherence and optimize therapeutic efficacy. Healthcare systems are strengthening primary care networks and retail pharmacy distribution channels to ensure consistent access to medication. Digital health platforms and telemedicine services are supporting remote monitoring, patient counseling, and compliance tracking. Regulatory agencies are streamlining approval pathways for innovative antidiabetic molecules, which is accelerating product commercialization.

Key Industry Highlights

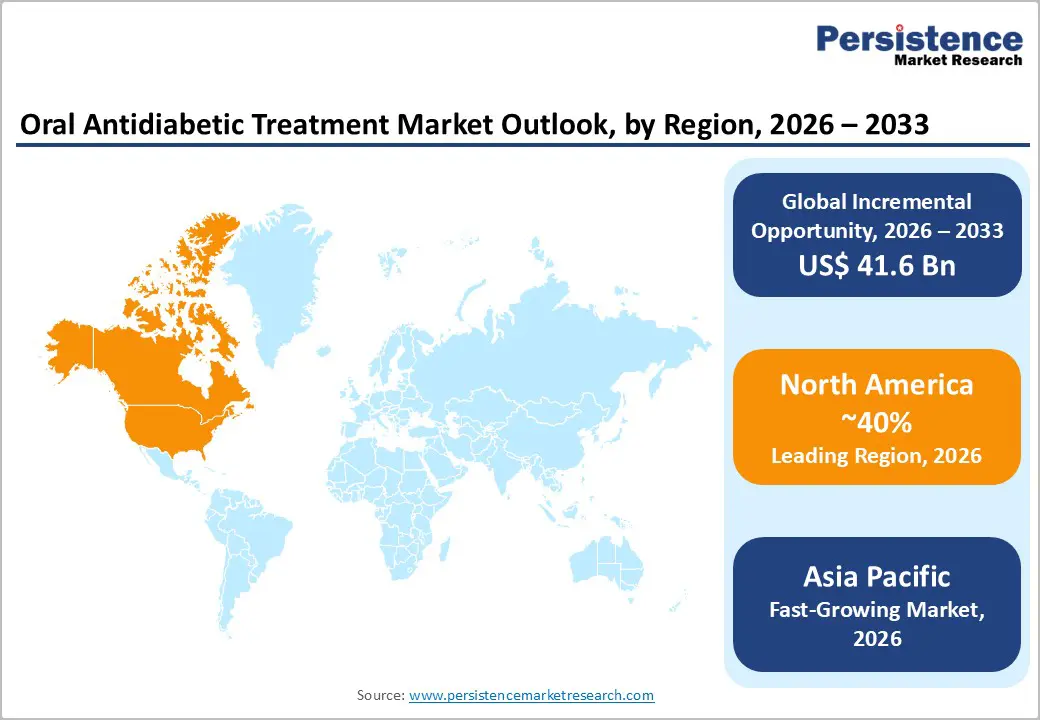

- Dominant Region: North America is projected to lead with a 40% market share by 2026, driven by strong reimbursement alignment and robust outpatient infrastructure.

- Fastest-growing Regional Market: Asia Pacific is projected as the fastest-growing market through 2033, supported by high diabetes prevalence and wide availability of cost-efficient oral therapies.

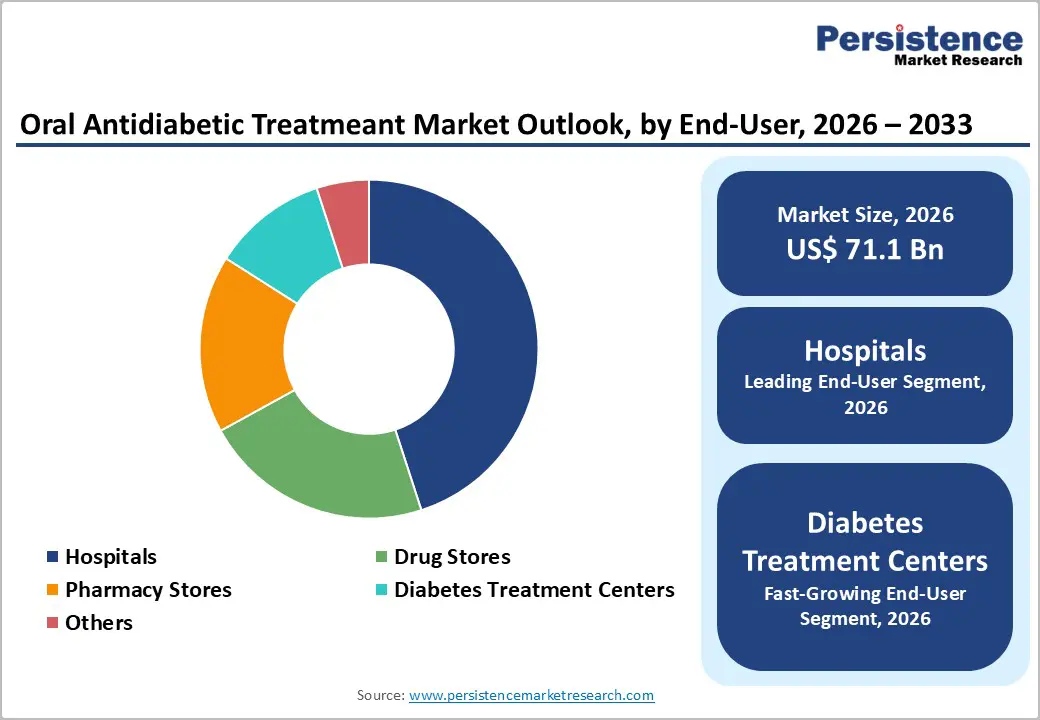

- Leading End-User: Hospitals are set to hold nearly 45% revenue share in 2026, owing to specialist-led prescribing, integrated care, and advanced infrastructure.

- Fastest-growing End-User: Diabetes treatment centers are expected to be the fastest-growing between 2026 and 2033, propelled by specialized care models, patient education, and digital monitoring.

- January 2026: Novo Nordisk’s Wegovy pill was launched across the U.S. as the first oral glucagon-like peptide-1 (GLP-1) weight-loss therapy, expanding treatment options for adults seeking effective, non-injectable obesity management.

| Key Insights | Details |

|---|---|

| Oral Antidiabetic Treatment Market Size (2026E) | US$ 71.1 Bn |

| Market Value Forecast (2033F) | US$ 112.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Diabetes Burden and Early Diagnosis Expansion

The expanding prevalence of diabetes reshapes therapeutic demand by enlarging the treated population across age groups, income levels, and care settings. Lifestyle transitions marked by sedentary behavior, calorie-dense diets, and urban stress patterns elevate incidence rates in both developed and developing economies. This epidemiological shift increases the proportion of patients requiring long-term glycemic control through convenient, scalable, and cost-effective solutions. Oral therapies align with these structural needs by supporting outpatient management, reducing dependency on injectable interventions, and fitting within primary care pathways. Health systems under budgetary pressure favor treatments that enable chronic disease control without intensive infrastructure requirements. The World Health Organization (WHO) estimates that diabetes affected around 537 million adults globally in 2021, reinforcing the scale-driven demand expansion supported by public health evidence. This rising patient base creates sustained volume growth rather than episodic demand cycles, strengthening long-term commercial visibility.

Early diagnosis expansion further accelerates uptake by shifting treatment initiation to earlier disease stages. Screening programs, employer-led health checks, and improved access to diagnostics identify prediabetes and early-stage type 2 diabetes with greater precision. Earlier detection translates into longer treatment duration and broader therapeutic coverage, as clinicians prioritize oral regimens for initial disease management to delay complications. Payers and policymakers promote early intervention frameworks to limit downstream costs linked to cardiovascular, renal, and neurological outcomes. Clinical guidelines increasingly emphasize stepwise treatment escalation, positioning oral options as first-line or combination foundations. This diagnostic and policy environment converts latent disease prevalence into active treatment demand, reinforcing predictable prescription growth.

High Costs of Advanced Therapies

High development and manufacturing costs for advanced therapies restrict market expansion by limiting affordability and uptake among patients and payers. Innovation in drug classes such as GLP-1 receptor agonists, sodium-glucose cotransporter-2 (SGLT2) inhibitors, and combination therapies requires significant investment in clinical research, regulatory processes, and complex production capabilities. These expenses are reflected in premium pricing structures that private insurers and government health programs must absorb or pass on to patients. In cost-sensitive healthcare environments, higher copayments and stricter coverage criteria reduce prescription fulfillment and long-term adherence, particularly among populations with limited disposable income. In the United States, overall prescription drug spending reached US$ 805.9 billion in 2024, driven in large part by high-cost therapy segments such as GLP-1 treatments, demonstrating the scale of economic pressure advanced medications exert on system budgets and patient access.

Pricing pressures also impede strategic investment and competitive dynamics across markets. Healthcare providers may prefer established, lower-cost therapies to meet institutional budget targets, slowing adoption rates for newer options. Payers tighten formulary access and negotiate rebates to contain expenditure, which can compress margins for innovators and deter product launches in price-sensitive regions. In emerging economies with high out-of-pocket spending and limited insurance penetration, these dynamics contribute to inequitable access and suppressed demand, weakening revenue forecasts and disincentivizing local market commitments.

Innovation in Combination Therapies and Digital Integration

Therapeutic innovation increasingly centers on combination regimens that address glycemic control, cardiovascular risk, and metabolic balance within a single treatment framework. Monotherapy pathways face structural limits when disease progression involves multiple physiological dysfunctions. Fixed-dose and mechanism-diverse combinations improve treatment durability, simplify prescribing decisions, and support faster clinical intensification without increasing pill burden. Clinical development strategies prioritize synergistic efficacy profiles aligned with long-term disease management rather than short-term glucose reduction. This approach reflects clinical practice realities where treatment inertia and complexity weaken outcomes. Integrated combinations support standardized care pathways, reduce variability in prescribing behavior, and strengthen confidence among healthcare professionals managing heterogeneous patient profiles.

Digital integration elevates therapeutic value by shifting treatment from episodic intervention to continuous management. Connected devices, data-driven decision support, and therapy-linked platforms translate real-world patient behavior into actionable clinical insight. These capabilities improve adherence monitoring, enable early risk identification, and support outcome-driven care models favored by healthcare systems. Pharmaceutical stakeholders benefit through lifecycle extension, differentiated value propositions, and data assets that inform pipeline optimization. Healthcare providers gain operational efficiency through proactive management and reduced complication intensity.

Category-wise Analysis

Drug Class Insights

Biguanides are likely to be the leading segment with an estimated 35% of the oral antidiabetic treatment market revenue share in 2026, due to established first-line clinical positioning, broad physician acceptance, and long-term safety validation. Biguanides remain the preferred initial therapy in type 2 diabetes management guidelines issued by major public health authorities. Widespread inclusion in national essential medicines lists supports consistent procurement and reimbursement across public and private healthcare systems. Strong cost-effectiveness profiles improve accessibility across income segments, reinforcing sustained prescription volumes. Generic availability further enhances penetration through primary care and community pharmacy channels. High treatment adherence, familiarity among clinicians, and compatibility with combination regimens strengthen long-term utilization. Manufacturing scalability and stable supply chains support uninterrupted availability, reinforcing leadership positioning within oral antidiabetic treatment portfolios.

SGLT-2 inhibitors are expected to witness the fastest growth between 2026 and 2033, as clinical evidence supports broader metabolic and cardiovascular benefits. Expanding physician confidence in multi-organ outcome improvement drives increased adoption beyond glycemic control. Regulatory endorsements for risk reduction in comorbid populations enhance prescribing scope. Improved safety monitoring frameworks and real-world evidence strengthen payer confidence. Ongoing formulation innovation and pipeline expansion improve differentiation within the oral therapy category.

Route of Administration Insights

Oral administration is poised to lead with a forecasted 95% revenue share in 2026, owing to patient familiarity, ease of use, and strong integration into outpatient care models. Oral dosing aligns with long-term chronic disease management requirements, supporting high adherence rates through routine incorporation into daily treatment schedules. Established prescribing confidence among clinicians reinforces continuity across therapy lines. Extensive retail pharmacy penetration and mail-order distribution enhance accessibility across urban and semi-urban settings. Cultural acceptance across diverse healthcare systems reinforces sustained utilization over extended treatment horizons. Digital prescription platforms further streamline refills, therapy tracking, and continuity of care, strengthening alignment with structured follow-up models and cost-efficient healthcare delivery frameworks.

Sublingual administration is anticipated to be the fastest-growing segment between 2026 and 2033, driven by innovation in rapid-absorption formulations and patient-centric delivery technologies. This route addresses unmet needs linked to delayed onset and gastrointestinal limitations associated with conventional dosing. Enhanced bioavailability and faster onset profiles support targeted use cases requiring prompt therapeutic action. Advances in formulation science improve stability, dosing accuracy, and patient convenience. Adoption within digitally enabled care pathways and specialty prescribing expands awareness among clinicians managing complex profiles. Integration with remote monitoring tools supports precision dosing strategies, reinforcing the role of sublingual delivery within differentiated treatment algorithms.

End-User Insights

Hospitals are positioned dominate with nearly 45% of the oral antidiabetic treatment market share in 2026, supported by high diagnostic throughput, specialist-driven prescribing, and integrated care delivery systems. Hospital-based endocrinology departments influence treatment initiation and regimen selection through standardized clinical protocols and evidence-based pathways. Advanced diagnostic infrastructure enables early detection, risk stratification, and therapy escalation within controlled environments. Institutional procurement contracts ensure steady supply volumes, pricing stability, and formulary consistency. Clinical credibility and multidisciplinary care models reinforce prescribing authority across referral networks. Strong linkage with inpatient, outpatient, and emergency services sustains patient flow, supporting long-term therapy continuity and reinforcing hospitals as primary decision-making hubs.

Diabetes treatment centers are expected to emerge as the fastest-growing segment between 2026 and 2033, driven by specialized care models, patient education programs, and digital monitoring integration. Focused disease management improves treatment adherence and therapy optimization through structured follow-up and individualized care plans. Dedicated clinical teams enhance patient engagement, lifestyle counseling, and outcome tracking. Expansion of standalone centers and telehealth-supported services increases accessibility across underserved and urban markets. Cost-efficient outpatient delivery strengthens referral inflows from primary care providers. Integration with remote data platforms supports proactive intervention, positioning specialized centers as scalable and performance-oriented care settings.

Regional Insights

North America Oral Antidiabetic Treatment Market Trends

By 2026, North America is expected to lead with an estimated 40% of the oral antidiabetic treatment market share, supported by early disease identification, rapid therapy initiation, and strong alignment between clinical protocols and reimbursement structures. High screening intensity within primary care drives earlier treatment starts, extending therapy duration per patient and increasing cumulative treatment value. Prescribing practices emphasize combination regimens and timely intensification, which elevates per-patient revenue rather than relying on population expansion. Broad insurance coverage and structured formulary access reduce therapy discontinuity, while acceptance of branded oral therapies sustains pricing strength. Advanced outpatient infrastructure ensures seamless transitions from diagnosis to long-term management, reinforcing consistent demand generation.

Leadership is further reinforced by a highly efficient commercialization and distribution ecosystem that accelerates adoption of new formulations. Integrated pharmacy benefit management, mail-order fulfillment, and digital prescribing platforms improve refill adherence and persistence, strengthening lifetime treatment economics. Concentration of clinical research activity accelerates physician familiarity with novel mechanisms prior to wider global adoption. Regulatory clarity and predictable approval timelines support faster market entry and lifecycle extension strategies. Corporate investment prioritization favors this geography for innovation launches, digital integration, and fixed-dose combinations, creating sustained competitive advantage.

Europe Oral Antidiabetic Treatment Market Trends

Europe is expected to maintain a significant position in the market for oral antidiabetic treatments through 2033 due to strong healthcare infrastructure, well-established treatment guidelines, and high patient awareness of chronic disease management. Early diagnosis supported by national screening programs enables timely therapy initiation, while structured outpatient care ensures long-term adherence. Prescribing behavior emphasizes individualized treatment and rapid adoption of combination regimens addressing both glycemic control and comorbid conditions. Extensive retail pharmacy networks, hospital outpatient clinics, and digital prescription systems facilitate consistent access to therapies, reducing interruptions in care. Value-based reimbursement frameworks and chronic disease monitoring programs further reinforce predictable demand and stable treatment outcomes.

Significant growth is driven by investment in innovation, integration of digital health solutions, and patient-centric support initiatives. Telemedicine and remote monitoring platforms enhance adherence tracking and enable proactive therapy adjustments, supporting outcome-focused care models. Regulatory clarity and streamlined approval processes accelerate adoption of novel formulations and fixed-dose combinations across specialty and primary care settings. Educational programs, lifestyle management initiatives, and multidisciplinary care pathways strengthen patient engagement and reduce discontinuation rates. Pharmaceutical strategies focusing on lifecycle management, combination therapies, and digital adherence tools enhance competitiveness.

Asia Pacific Oral Antidiabetic Treatment Market Trends

Asia Pacific is forecasted to be the fastest-growing market for oral antidiabetic treatment during the 2026-2033 forecast period, reflecting rapid expansion in disease detection, treatment initiation, and long-term therapy management. Rising prevalence driven by urbanization, sedentary lifestyles, and dietary shifts increases the pool of newly diagnosed patients requiring pharmacological intervention. Integration of chronic disease screening into primary care networks accelerates early treatment uptake, while oral therapies align with cost-efficient outpatient models that support widespread accessibility. Local production of generics and competitively priced branded options reduces financial barriers, enabling higher penetration across both public and private healthcare channels. Digital health platforms embedded in care delivery enhance adherence tracking, refill continuity, and patient engagement, converting initial treatment adoption into sustained long-term therapy compliance.

Growth acceleration is supported by modernization of healthcare infrastructure and policy initiatives that expand access to treatment. Government-backed insurance schemes and reimbursement reforms lower out-of-pocket costs, facilitating broader adoption across income segments. Expansion of specialty clinics, teleconsultation services, and digitally enabled care pathways shortens the time from diagnosis to therapy initiation. Prescribing patterns increasingly favor early intervention and combination regimens, extending treatment duration and improving outcomes. Technology-driven distribution, including e-pharmacies and app-based prescription fulfillment, reaches semi-urban and rural populations efficiently. Pharmaceutical strategies focused on fixed-dose combinations, localized formulations, and scalable manufacturing further reinforce market penetration, creating a high-velocity growth environment anchored in structural demand expansion and accessible outpatient care delivery.

Competitive Landscape

The global oral antidiabetic treatment market landscape exhibits a moderately consolidated structure, with leading pharmaceutical companies accounting for a significant portion of total revenue. Market concentration is highest among multinational innovators such as Novo Nordisk A/S, Sanofi, AstraZeneca, Merck KGaA, Eli Lilly, and Pfizer Inc., whose diversified portfolios span biguanides, SGLT-2 inhibitors, and DPP-4 inhibitors. These companies leverage patent-protected formulations to secure revenue streams and maintain therapeutic differentiation. Established distribution networks, including hospital partnerships, retail pharmacies, and digital prescription platforms, ensure broad accessibility and therapy continuity. Long-standing relationships with healthcare providers reinforce prescribing confidence, while strategic marketing and medical education programs enhance brand recognition.

Complementing multinational innovators, companies such as Cipla and Johnson & Johnson operate in more fragmented generic and specialty segments, introducing competitive dynamics across pricing and volume-driven channels. Generic producers expand accessibility, particularly in cost-sensitive markets, while stimulating efficiency in manufacturing and supply chain management. This combination of established global players and agile generic manufacturers supports targeted investment strategies, enabling innovation in combination therapies, fixed-dose formulations, and patient-centric delivery methods. Competitive pressures encourage clinical differentiation, lifecycle management, and integration of digital adherence tools.

Key Industry Developments

- In July 2025, Sanofi and Emcure Pharmaceuticals signed an exclusive distribution and promotion agreement to broaden the reach of Sanofi’s oral anti-diabetic drugs, including Amaryl and Cetapin, across India through Emcure’s extensive network.

- In June 2025, Abbott and MSD Pharmaceuticals entered a strategic distribution partnership to expand access to MSD’s oral anti-diabetic medicines, including sitagliptin and its combinations marketed as Januvia, Janumet, and Janumet XR, across India through Abbott’s nationwide network.

- In May 2025, Cadila Pharmaceuticals launched Empadon (empagliflozin), its SGLT-2 inhibitor oral antidiabetic therapy in India, expanding access to this treatment class with fixed-dose combinations and broader affordability.

Companies Covered in Oral Antidiabetic Treatment Market

- Novo Nordisk A/S

- Sanofi

- AstraZeneca

- Merck KGaA

- Eli Lilly

- Pfizer Inc.

- Cipla.

- Johnson & Johnson

- Sun Pharmaceutical Industries Ltd.

Frequently Asked Questions

The global oral antidiabetic treatment market is projected to reach US$ 71.1 billion in 2026.

Rising diabetes prevalence, demand for improved glycemic control, and adoption of combination therapies are driving the market.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Innovation in combination therapies, digital integration, and expansion into emerging outpatient care channels present key market opportunities.

Some of the key market players include Novo Nordisk A/S, Sanofi, AstraZeneca, Merck KGaA, Eli Lilly, Pfizer Inc., Cipla, Johnson & Johnson, and Sun Pharmaceutical Industries Ltd.