- Oil & Gas

- Oil and Gas Hose Assemblies Market

Oil and Gas Hose Assemblies Market Size, Share, and Growth Forecast, 2025 - 2032

Oil and Gas Hose Assemblies Market Product (Dock Loading Hose Assemblies, Dump Hose Assemblies, FPSO Water Uptake Hoses, Jumper Hose Assemblies, Bunkering Hose Assemblies, Drilling Mud Hose Assemblies, Frac Hose Assemblies and Other Custom Hose Assemblies), Pressure Intake, and Regional Analysis for 2025 - 2032

Oil and Gas Hose Assemblies Market Size and Trends Analysis

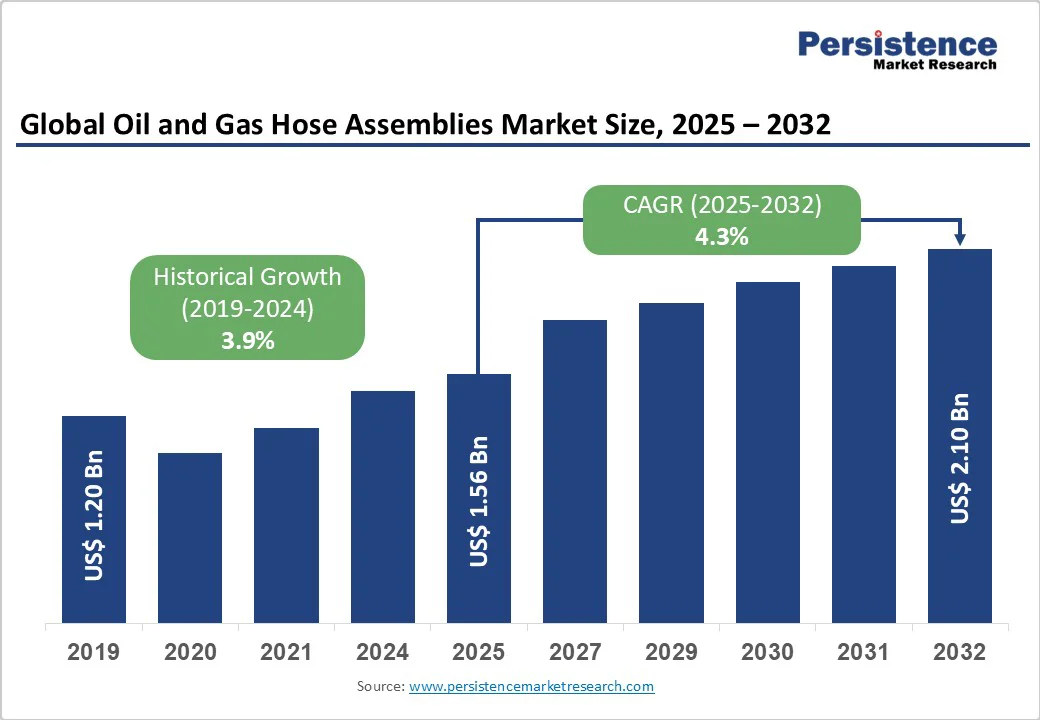

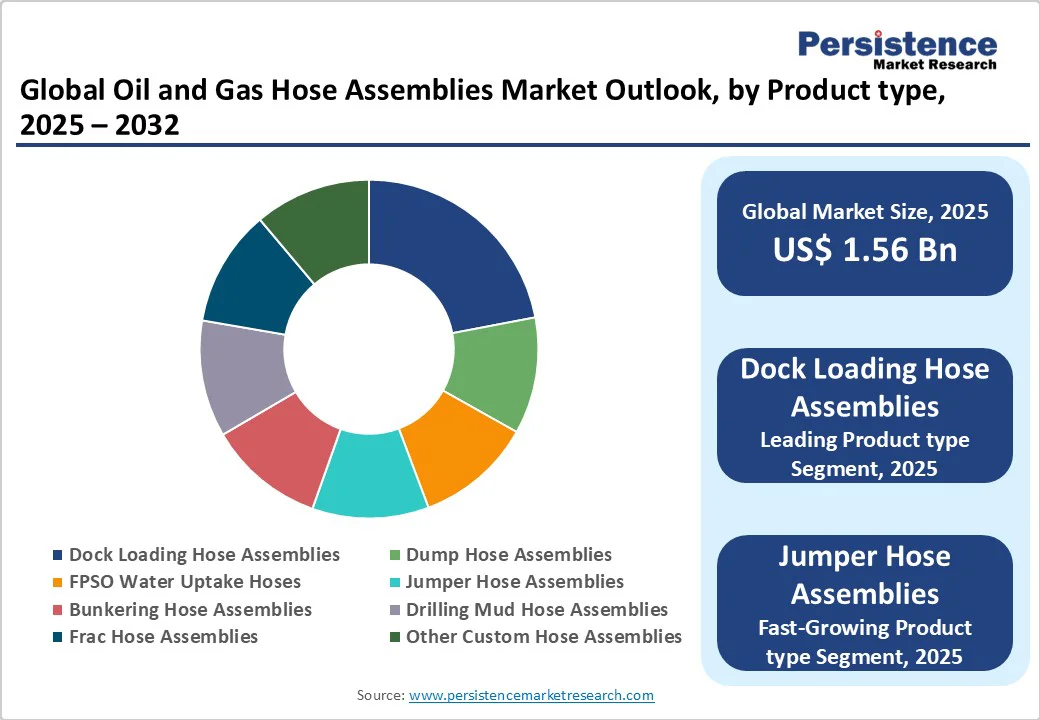

The global oil and gas hose assemblies market size is likely to be valued at US$1.56 billion in 2025 and is projected to reach US$2.10 billion by 2032, growing at a CAGR of 4.3% between 2025 and 2032.

The robust growth trajectory is driven by increasing global energy demand, expanding offshore exploration activities, and technological advancements in hose materials.

Key Industry Highlights:

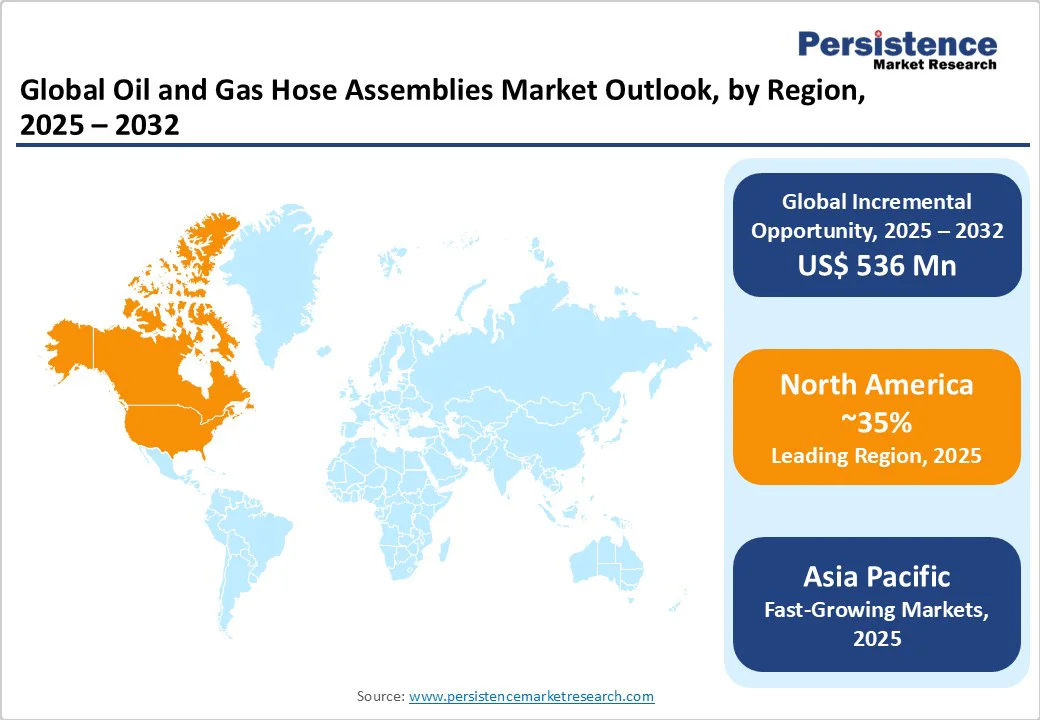

- Regional Growth Leaders: North America leads with 35% global share, supported by mature refining and petrochemical industries, whereas Asia-Pacific demonstrates the strongest growth potential, fueled by industrialization and expanding oil & gas infrastructure.

- Leading Product Segments: Dock Loading Hose Assemblies dominate with a 38.4% share in 2025, while Jumper Hose Assemblies represent the fastest-growing product category, driven by rising offshore and midstream adoption.

- Leading Pressure Type: Medium pressure assemblies account for 43.2% of market share, maintaining segment leadership, while High Pressure assemblies exhibit the fastest growth, supported by increasing offshore oil and gas exploration activities.

- End-user Dominance: Downstream operations account for 52.4% of total demand, reflecting their critical role in refining and petrochemical facilities, while the upstream segment records the highest growth rate due to expansion in exploration and drilling.

- Technology Integration: IoT and smart sensor-enabled hose assemblies enhance predictive maintenance and operational efficiency, reducing downtime and improving safety performance across critical End-users.

- Strategic Consolidation: The top five companies control 45-50% market share, with ongoing M&A activity and geographic expansion strategies strengthening competitive positioning.

| Key Insights | Details |

|---|---|

| Oil and Gas Hose Assemblies Market Size (2025E) | US$1.56 Bn |

| Market Value Forecast (2032F) | US$2.10 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.9% |

Market Dynamics

Growth Drivers - Technological Advancements and Material Innovation

Continuous advancements in materials science and the development of high-performance hoses with enhanced resistance to extreme temperatures, chemicals, and pressures are boosting market growth. Manufacturers are investing in high-quality materials, such as thermoplastic elastomers and stainless steel, to improve resistance to abrasion, corrosion, and extreme temperatures.

The growing adoption of advanced materials like polymers and composites for enhanced durability and lightweight designs is creating new opportunities for market expansion. These technological innovations enable hose assemblies to operate effectively in deepwater and ultra-deepwater environments, meeting the stringent performance requirements of modern oil and gas operations.

Stringent Safety and Regulatory Standards

The implementation of stricter safety regulations and environmental compliance requirements is driving demand for certified, high-performance hose assemblies. The American Petroleum Institute (API) has established comprehensive standards, including API 17K for bonded flexible hoses and API 15WT for lay-flat hose operations.

These regulations mandate rigorous testing procedures, pressure ratings, and environmental protection protocols, compelling operators to invest in premium hose assembly solutions that ensure operational safety and regulatory compliance.

Restraint - Oil Price Volatility and Economic Uncertainty

High volatility in oil prices directly affects capital investment in exploration and drilling activities, creating cyclical fluctuations in hose assembly demand. During periods of low oil prices, companies tend to scale back on exploration projects, reducing equipment procurement including hose assemblies. Economic downturns impacting investment in oil and gas projects represent another significant constraint, as operators defer capital expenditures during uncertain market conditions.

Complex Regulatory Landscape and Compliance Costs

The complex regulatory landscape in the oil and gas sector, particularly concerning environmental safety and emissions, poses significant operational constraints. Manufacturers are required to meet stringent standards and certifications, which can increase production costs and extend product development timelines. The necessity for extensive testing, documentation, and compliance verification creates additional cost burdens that can impact market accessibility for smaller operators.

Key Market Opportunities

Smart Technology Integration and Predictive Maintenance

The integration of IoT-enabled hose assemblies equipped with advanced sensors offers a transformative opportunity for the oil and gas sector. By monitoring critical parameters such as pressure, temperature, and wear in real time, these smart systems enable predictive maintenance and operational optimization.

This minimizes downtime, reduces safety risks, and enhances efficiency in high-stakes operations such as offshore drilling, LNG transfer, and hydraulic fracturing, where hose reliability is paramount. The shift toward digitalization positions smart technology as a core enabler of safer, more efficient, and cost-effective hose assembly operations.

Emerging Markets and Offshore Exploration Expansion

China and India lead Asia Pacific, presents strong growth opportunities due to rapid industrialization, infrastructure expansion, and increasing energy demand. Large-scale pipeline installations and oil & gas projects require extensive hose assembly solutions to support new facilities.

Simultaneously, rising investment in offshore and ultra-deepwater exploration is driving demand for high-performance, corrosion-resistant hoses that can withstand extreme marine environments. Together, these trends create significant long-term opportunities in both emerging onshore markets and advanced offshore developments.

Category-wise Analysis

Product Type Insights

Dock Loading Hoses Dominate While Jumper Hoses Emerge as Fastest-Growing Offshore Segment

Dock loading hose assemblies dominate the product segment with 38.4% share, serving as essential components for transferring petroleum and chemical products between marine vessels and onshore storage during import and export operations. These assemblies are critical for maritime trade in crude oil and LNG, with global expansion driving sustained demand. The segment benefits from established infrastructure and proven end-users across major ports worldwide.

Jumper Hose Assemblies represent the fastest-growing product segment, driven by increasing demand for flexible connection solutions in offshore platforms and subsea End-users. These assemblies provide critical connectivity between production equipment and pipeline systems, particularly in FPSO (Floating Production Storage and Offloading) operations and offshore drilling platforms. Their growth reflects the industry's shift toward more complex offshore installations requiring versatile fluid transfer solutions.

Pressure Type Insights

Medium Pressure Leads While High Pressure Assemblies Drive Fastest Growth

Medium-pressure hose assemblies command the largest market share at 43.2%, offering an optimal balance of cost-effectiveness, flexibility, and performance for standard oil and gas End-users. These assemblies serve the majority of pipeline transportation, storage facility connections, and refinery operations where moderate pressure requirements align with operational needs.

High-pressure assemblies constitute the fastest-growing segment, driven by increasing demands from hydraulic fracturing, deep-water drilling, and enhanced oil recovery operations. The expansion of unconventional oil extraction techniques and offshore exploration in challenging environments necessitates hose assemblies capable of withstanding extreme pressure conditions exceeding standard operational parameters.

End-use Insights

Downstream Dominance and Upstream Growth Define End-user Trends

Downstream operations represent the dominant End-user segment with 52.4% market share, encompassing refineries, petrochemical plants, and distribution terminals where hose assemblies facilitate product transfer and processing operations. The mature infrastructure and continuous operational requirements in downstream facilities ensure steady demand for replacement and upgrade cycles.

Upstream End-users show the fastest growth rate, driven by expanding exploration and production activities, particularly in offshore and unconventional resource developments. The segment benefits from increased investment in shale oil production, deep-water drilling, and enhanced recovery techniques that require specialized hose assembly solutions capable of handling harsh operating conditions.

Regional Insights and Trends

North America Leads Global Hose Assemblies Market with Strong Shale Oil, Refining, and Petrochemical Growth

North America maintains market leadership with an estimated 35% global market share, driven by extensive shale oil production, ongoing offshore exploration in the Gulf of Mexico, and robust refining and petrochemical sectors. The U.S. market is projected to reach approximately $950 million by 2028, growing at a CAGR of 4.2%. Key growth drivers include the resurgence of shale oil production, technological innovations in hose manufacturing, and increasing safety regulations requiring high-performance, corrosion-resistant hoses.

According to the U.S. Energy Information Administration (EIA), global oil consumption in 2024 is projected to increase by 1.1 million barrels per day, underscoring the critical importance of reliable hose assemblies in supporting these operations.

The region's mature industrial base and extensive infrastructure support both domestic consumption and export activities. Canada's market is projected to reach approximately $410 million by 2028, driven by its vast oil sands reserves, extensive pipeline networks, and active offshore drilling in both Atlantic and Pacific waters.

Europe’s Oil & Gas Hose Assemblies Market Advances with LNG, Refinery Upgrades, and Sustainability Focus

The European oil and gas hose assemblies market is experiencing steady growth, driven by strict EU green regulations, increased LNG adoption as a transition fuel, and significant investments in refinery modernization. Regulatory bodies such as the European Chemicals Agency (ECHA) and the European Maritime Safety Agency (EMSA) enforce safety and compliance standards, ensuring reliability in offshore and onshore End-users. Germany, France, and Italy lead in LNG operations, with growing demand for cryogenic hoses and specialized solutions for refining and emerging green hydrogen projects.

The market is further supported by the development of recyclable and bio-based hoses that reduce environmental impact. In the UK, growth is reinforced by North Sea investments, stringent offshore safety standards enforced by the Health and Safety Executive (HSE) and the Oil and Gas Authority (OGA), and emission reduction initiatives. Industry trends highlight rising adoption of lightweight, flexible hydraulic hoses for FPSOs, along with fireproof, anti-static solutions and AI-enabled predictive maintenance technologies.

Asia Pacific Represents the Fastest-Growing Market for Oil And Gas Hose Assemblies

Asia Pacific represents the fastest-growing market for oil and gas hose assemblies, holding about 30% global market share, fueled by rapid industrialization, surging energy demand, and large-scale infrastructure development across China, India, Japan, and ASEAN countries.

The region benefits from cost-effective manufacturing, skilled labor, and government-backed investments in pipeline networks and offshore exploration projects, reinforcing its position as a global supply hub. Emerging economies further boost growth as rising energy consumption drives strong demand for durable and efficient hose solutions.

Japan stands out with growing LNG demand and increasing investments in hydrogen fuel infrastructure, supported by policies from the Ministry of Economy, Trade, and Industry (METI) and JOGMEC. Japanese firms are innovating flexible cryogenic hoses, corrosion-resistant solutions for offshore platforms, and advanced hoses for hydrogen and ammonia transport. Additionally, the development of wear-resistant and earthquake-resilient hoses highlights Japan’s focus on safety, sustainability, and advanced energy End-users.

Competitive Landscape

The oil and gas hose assemblies market is fragmented. The growth comes from the need for tough, high-pressure hoses in upstream, midstream, and downstream work. In addition, due to more oil and gas searches, strict safety rules, and better hose materials and tech adds more growth.

Firms aim for top-notch, rust-proof, heat-resistant hoses to boost safety, work quality, and life in tough spots. The market has top hose makers, oil field tool sellers, and fluid transfer tech teams. Each group helps with new ideas in flexible hoses, cold transfer hoses, and hydraulic hose systems.

Key Industry Developments

- In October 2024, Penflex Corporation, a leading provider of flexible piping solutions, secured Canadian Registration Number (CRN) approval from the Alberta Boilers Safety Association for its made-to-stock metal hose assemblies. CRN is granted by an authorized safety authority in each Canadian province or territory for boilers, pressure vessels, or fittings operating above 15 psig (1 barg). This certification confirms that the design meets regulatory standards and is approved for use within the respective jurisdiction.

- In November 2024, EnerMech secured a multi-million-dollar contract as the preferred provider of Flexible Hose Assembly (FHA) and Small Bore Tubing (SBT) management services for a leading E&P organization’s UK assets. The minimum five-year agreement encompasses the management, maintenance, and inspection of FHA and SBT systems, ensuring asset integrity, production continuity, and operational efficiency. EnerMech’s scope includes condition monitoring of hoses and small bore tubing, adhering to stringent safety and operational standards.

Companies Covered in Oil and Gas Hose Assemblies Market

- Alfa Gomma S.p.A.

- Abcon Industrial Products Ltd

- Continental AG

- Eaton Corporation Plc

- EMSTEC GmbH

- Gates Industrial Corporation plc

- Kuriyama Holdings Corporation

- Parker Hannifin Corporation

- LGG Industrial, Inc.

- Trelleborg AB

- Other Market Players

Frequently Asked Questions

The Oil and Gas Hose Assemblies market is estimated to be valued at US$ 1.56 Bn in 2025.

The key demand driver for the Oil and Gas Hose Assemblies market is the increasing exploration and production (E&P) activities across onshore and offshore operations.

In 2025, the North America region will dominate the market with an exceeding 35% revenue share in the global Oil and Gas Hose Assemblies market.

Among the Product Type, Dock Loading Hose Assemblies holds the highest preference, capturing beyond 38.5% of the market revenue share in 2025, surpassing other parts.

The key players in Oil and Gas Hose Assemblies are Alfa Gomma S.p.A., Abcon Industrial Products Ltd, Continental AG and Eaton Corporation Plc.