- Food Ingredients & Additives

- Canola Oil Market

Canola Oil Market Size, Share, and Growth Forecast 2026 - 2033

Canola Oil Market by Product Type (Refined Canola Oil, Cold-Pressed Canola Oil, Organic Canola Oil, Hydrogenated Canola Oil), Nature (Conventional, Organic, Non-GMO), by Packaging Type (Bottles, Cans, Pouches, Bulk Containers), Industry (Food & Beverages, Foodservice & HoReCa, Cosmetics & Personal Care, Biofuels (Biodiesel), Animal Feed), Distribution Channel (Online, Offline), and Regional Analysis, 2026 - 2033

Canola Oil Market Size and Trend Analysis

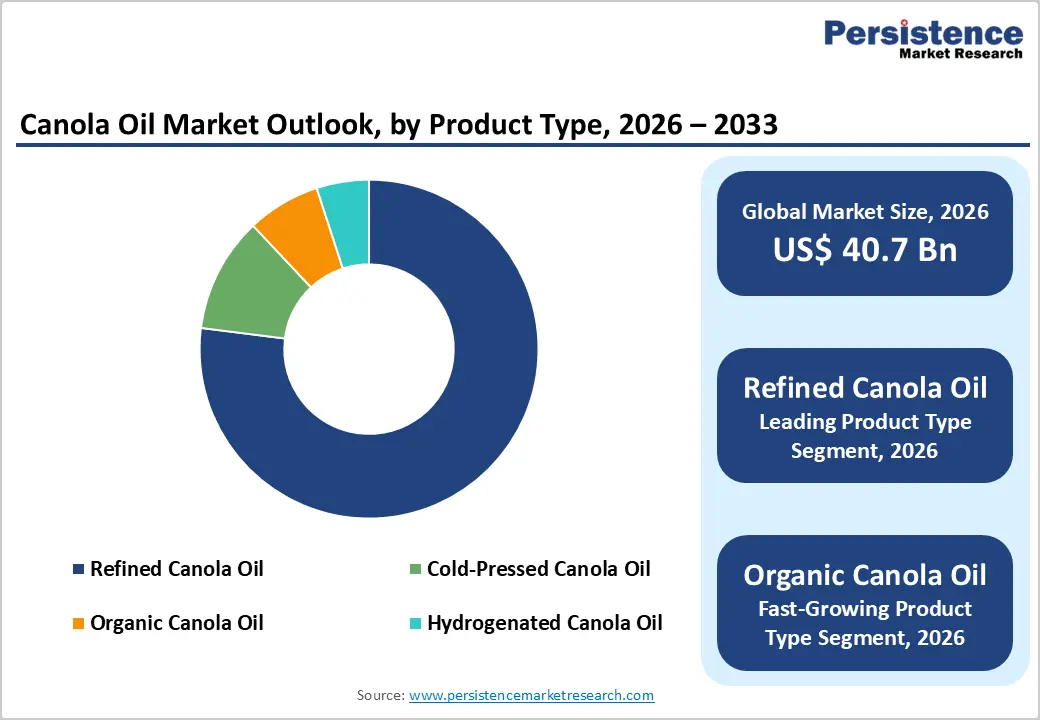

The global canola oil market size is expected to be valued at US$ 40.7 billion in 2026 and projected to reach US$ 55.0 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033. Well-established health credentials, cost-competitive positioning among edible oils, and rapidly growing demand across both food and industrial end-use segments drive the market growth.

Canola oil's heart-healthy fat profile, characterized by the lowest saturated fat content of any common cooking oil and high levels of omega-3 fatty acids, has earned endorsement from the U.S. Food and Drug Administration (FDA), which authorizes a qualified health claim linking canola oil consumption to reduced coronary heart disease risk. Simultaneously, rising global demand for biodiesel as governments advance renewable fuel mandates, and expanding canola cultivation in key producing nations, including Canada, Australia, and the European Union, are collectively reinforcing supply-side scale and downstream market development across all major geographies.

Key Industry Highlights:

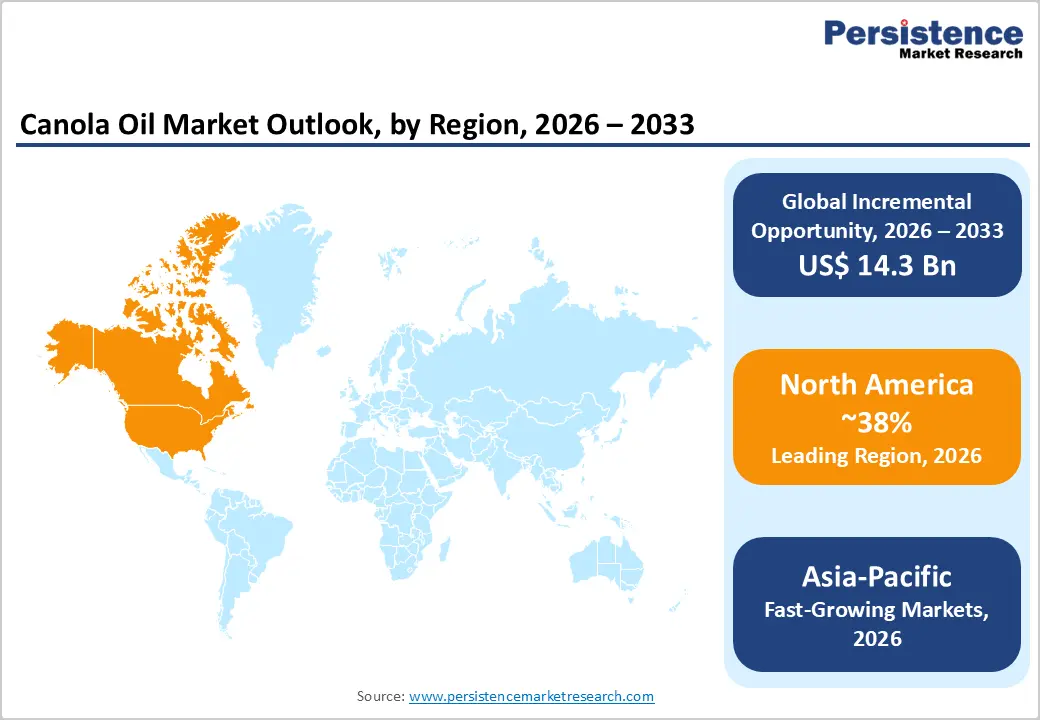

- Regional Leadership: North America holds approximately 38% of global canola oil market share in 2025, anchored by Canada's dominance as the world's largest canola producer, FDA-endorsed health claims, and deep foodservice and biodiesel demand infrastructure.

- Fastest Growing Market: Asia Pacific is the fast-growing market driven by health-conscious cooking oil trade-up in China and India, FSSAI and government dietary guidance endorsing canola oil, and rising modern trade penetration enabling premium product access.

- Dominant Product Segment: Refined canola oil is likely to account for 77% of global product share in 2026, sustained by its high smoke point, neutral flavor, shelf stability, and price competitiveness that make it the default choice across food manufacturing, foodservice, and retail cooking oil segments.

- Fast-Growing Product Segment: Organic canola oil is the fast-growing product type, driven by consumer GMO-free and clean-label preferences, OTA-confirmed organic food market growth, and premium brand positioning by specialty producers commanding 30–50% price premiums over conventional variants.

- Key Opportunity: Canola oil's proven utility as a cosmetics and personal care formulation ingredient is an underpenetrated growth vector its emollient profile, vitamin E content, and clean plant-derived positioning align with the clean beauty trend, offering producers high-margin diversification beyond commodity food and fuel markets.

Market Dynamics

Drivers - Health-Driven Consumer Shift Toward Low-Saturated-Fat Cooking Oils

Growing global consumer and clinical awareness of dietary fat quality as a determinant of cardiovascular health is structurally shifting cooking oil preferences toward canola, directly expanding demand across retail and foodservice channels. The American Heart Association (AHA) recommends canola oil as one of the healthiest cooking oils, citing its 7% saturated fat content lower than olive, coconut, or palm oil and its favorable omega-6 to omega-3 fatty acid ratio.

The FDA's qualified health claim for canola oil and coronary heart disease risk reduction provides manufacturers a powerful, regulator-validated consumer communication tool. This health positioning resonates particularly strongly with aging populations in North America, Europe, and urban Asia Pacific markets, where cardiovascular disease awareness is driving proactive dietary modification, creating sustained retail pull for canola oil at the expense of less healthy alternatives.

Restraints - Volatility in Canola Crop Production Due to Climate and Geopolitical Risks

Canola oil supply is structurally exposed to climate variability and geopolitical disruptions that create price and availability volatility, undermining downstream manufacturer planning and margin stability. The Canola Council of Canada documented significant crop yield reductions in the 2021–2022 growing season due to severe drought conditions in the Canadian prairies, tightening global canola oil supply.

Trade restrictions and geopolitical tensions including export controls by major producing nations have demonstrated the fragility of canola oil supply chains, creating procurement risk for industrial users and food manufacturers dependent on stable canola oil input costs.

Opportunities - Rising Demand for Organic and Non-GMO Canola Oil in Premium Retail and Health Channels

The Organic Canola Oil segment is the fastest-growing product category within the market, representing a compelling high-margin opportunity for producers and brands capable of securing certified organic supply chains and premium retail distribution. Consumer distrust of conventional genetically modified canola varieties is converting a segment of health-conscious buyers toward certified organic and Non-GMO Project Verified canola oil products, which command price premiums of 30–50% over conventional equivalents. The Organic Trade Association (OTA) confirmed U.S. organic food retail sales exceeding US$ 67 billion in 2023, with organic oils among the fastest-growing categories. Brands like La Tourangelle and Jivo Wellness Pvt. Ltd. have demonstrated viable premium positioning, while the growth of health specialty retailers and e-commerce channels provides scalable distribution infrastructure for organic canola oil brands targeting ingredient-aware consumers.

Category-wise Analysis

Product Type Insights

Refined canola oil dominates the product category with an overwhelming market share of approximately 77% in 2025, entrenched by its superior suitability for high-heat cooking applications with a smoke point of approximately 200–230°C (400–450°F) light neutral flavor that does not compete with food flavors, long shelf life, and the most competitive price point among canola oil variants. These functional properties make refined canola oil the preferred choice for commercial food manufacturers, foodservice operators, and mass-market retail consumers globally.

The Canola Council of Canada documents refined canola oil's dominant position in both domestic and export markets. Organic Canola Oil is the fastest-growing segment, driven by clean-label demand and GMO-free positioning, though it remains a premium niche relative to the refined mainstream volume.

Nature Insights

Conventional canola oil holds the dominant nature segment position with approximately 80% of market share in 2025, reflecting the entrenched cost advantage of conventional genetically modified canola varieties that deliver higher per-acre yields documented by the Canola Council of Canada as yielding 20–30% more per hectare than conventional non-GM varieties enabling competitive retail pricing that sustains high-volume household and industrial penetration.

Conventional canola oil underpins the bulk biodiesel feedstock market and the dominant foodservice channel. Non-GMO and Organic segments are the fastest-growing nature categories, as consumer clean-label awareness and retailer certification requirements drive premium portfolio expansion among major brands investing in traceable, verified supply chain infrastructure.

Regional Insights

North America Canola Oil Market Trends and Insights

North America dominates due to strong upstream integration, especially in Canada, which is the world’s largest canola producer and exporter. Canada produced ~21.8 million tonnes of canola in 2025 with exports valued at CAD $12.6 billion, indicating a highly export-oriented value chain . Over 50% of production is processed domestically, supporting large-scale oil output . The U.S. complements this with strong consumption and biofuel demand. Advanced crushing infrastructure, government-backed agriculture, and global trade networks ensure North America’s leadership in both supply and value realization.

Canada Canola Oil Market Trends and Insights

Canada remained the global backbone of the canola oil market, producing 21.8 MMT in 2025 and exporting oil worth over CAD $5.4 billion . Saskatchewan alone contributed 56% of production, highlighting geographic concentration and efficiency . Strong domestic crushing (11.6 MMT) ensured value addition and export competitiveness. The country’s integrated supply chain and dominance in global trade positioned it as the largest revenue contributor, expected to reach US$15–17 Bn by 2026.

United States Canola Oil Market Trends and Insights

The U.S. emerged as the fastest-growing market due to increasing use of canola oil in biofuels and processed foods. It is the largest importer of Canadian canola oil, accounting for CAD $5.7 billion exports . Rising renewable diesel capacity and health-driven edible oil consumption are accelerating demand. Expansion of domestic crushing facilities and policy support for clean fuels are expected to drive growth at ~5.5% CAGR, making it the fastest-growing country in the region.

Europe Canola Oil Market Trends and Insights

Europe plays a critical role due to its strong biodiesel industry and sustainability regulations. The EU is one of the largest consumers of rapeseed oil (canola equivalent), driven by renewable energy mandates and food applications. Countries like Germany and France rely heavily on rapeseed oil for biodiesel blending. Europe also imports significant volumes from Canada, with the EU among top export destinations . The region’s focus on low-carbon fuels, circular economy, and plant-based oils ensures stable demand and makes it a strategically important market despite slower growth compared to Asia.

Germany Canola Oil Market Trends and Insights

Germany leads due to its dominant biodiesel production capacity, where rapeseed oil is a primary feedstock. The country is one of Europe’s largest processors and consumers of oilseeds, supported by strong renewable energy policies. High domestic crushing capacity and consistent demand from transport fuels and food industries position Germany as the regional leader, expected to reach US$6–7 Bn by 2026.

France Canola Oil Market Trends and Insights

France is emerging as the fastest-growing market due to expanding biofuel mandates and increasing domestic rapeseed cultivation. Government policies supporting renewable diesel and sustainable agriculture are accelerating demand. Growth in food-grade oil consumption and local processing capacity is expected to drive a CAGR of ~5%, making France a key growth engine within Europe.

Asia Pacific Canola Oil Market Trends and Insights

Asia Pacific is the fastest-growing region due to rising population, urbanization, and increasing edible oil consumption. Countries like China and India are major importers of canola oil to meet domestic demand. The region benefits from dietary shifts toward healthier oils and rapid expansion in food processing industries. Limited domestic production compared to consumption drives imports, especially from Canada. Rising income levels and health awareness are accelerating adoption, making Asia Pacific the fastest-growing region with demand expanding faster than global average CAGR (4.4%).

China Canola Oil Market Trends and Insights

China is the largest consumer in the region, driven by massive population and food processing demand. It is a major importer of Canadian canola oil and meal, ensuring steady supply. Growing urbanization and increasing consumption of packaged foods are boosting demand. Despite trade fluctuations, China remains the dominant revenue contributor, expected to reach US$10 billion by 2026.

India Canola Oil Market Trends and Insights

India is the fastest-growing market due to rising edible oil consumption and increasing health awareness. The country imports significant volumes of vegetable oils to meet demand-supply gaps. Government initiatives to promote oilseed production and reduce import dependency are supporting growth. Expanding middle-class population and food industry demand are expected to drive ~5–6% CAGR, making India the fastest-growing country in Asia Pacific.

Competitive Landscape

The global canola oil market is moderately consolidated at the upstream (seed crushing and refining) level, with agricultural commodity giants Cargill, Incorporated, ADM, Bunge, Louis Dreyfus Company, and Wilmar International Limited collectively controlling a significant portion of global crush capacity. Key competitive differentiators include integrated supply chain control from farm to refinery, sustainability certification capabilities, and brand equity in retail and foodservice channels. Emerging competitive trends include investments in non-GMO and organic certified processing lines, biodiesel co-product integration, and premium specialty brand development targeting clean-label and organic retail segments.

Key Developments:

- April, 2026: Cargill opened a new canola processing facility in Regina, significantly expanding market access for Canadian farmers. The facility was designed to increase crushing capacity and improve supply chain efficiency, enabling farmers to deliver larger volumes of canola locally. This development strengthened Canada’s position as a leading global exporter of canola oil and related products.

- March, 2025: Louis Dreyfus Company maintained its oilseed expansion strategy in North America despite ongoing tariff uncertainties. The company continued to invest in processing and supply chain operations, signaling confidence in long-term demand for oilseeds such as canola and soybeans.

Global Canola Oil Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 33.1 Billion |

|

Projected Market Value (2026) |

US$ 40.7 Billion |

|

Projected Market Value (2033) |

US$ 55.0 Billion |

|

CAGR (2026-2033) |

4.4% |

|

Leading Region |

North America, 38% share |

|

Dominant Product |

Refined Canola Oil, 77% share |

|

Top-ranking Application |

Conventional, 63% share |

|

Incremental Opportunity |

US$ 14.3 billion |

Companies Covered in Canola Oil Market

- Louis Dreyfus Company

- ADM

- Cargill, Incorporated

- Wilmar International Limited

- Richardson International Limited

- Viterra

- CHS Inc.

- Associated British Foods plc

- Jivo Wellness Pvt. Ltd.

- La Tourangelle

- Bunge

- Sunora Foods

- Others

Frequently Asked Questions

The global canola oil market is valued at US$ 40.7 billion in 2026.

Health awareness, low saturated fat preference, rising food processing demand, biodiesel use, and growing global population.

North America leads the global canola oil market with approximately 38% of global share in 2025.

Expansion in emerging markets, rising organic demand, biodiesel growth, food processing innovation, and health-conscious consumers.

Louis Dreyfus Company, ADM, Cargill, Incorporated, Wilmar International Limited, Richardson International Limited, Viterra.