- Food Packaging

- Aluminium Foil Packaging Market

Aluminium Foil Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Aluminium Foil Packaging Market by Thickness (0.007 mm-0.09 mm, 0.09 mm-0.2 mm, 0.2 mm-0.4 mm, Others), Packaging Type (Bags & Pouches, Wraps & Rolls, Laminated Tubes, Aseptic Packaging, Others), End-use (Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics, Others), and Regional Analysis for 2025 - 2032

Aluminium Foil Packaging Market Size and Trend Analysis

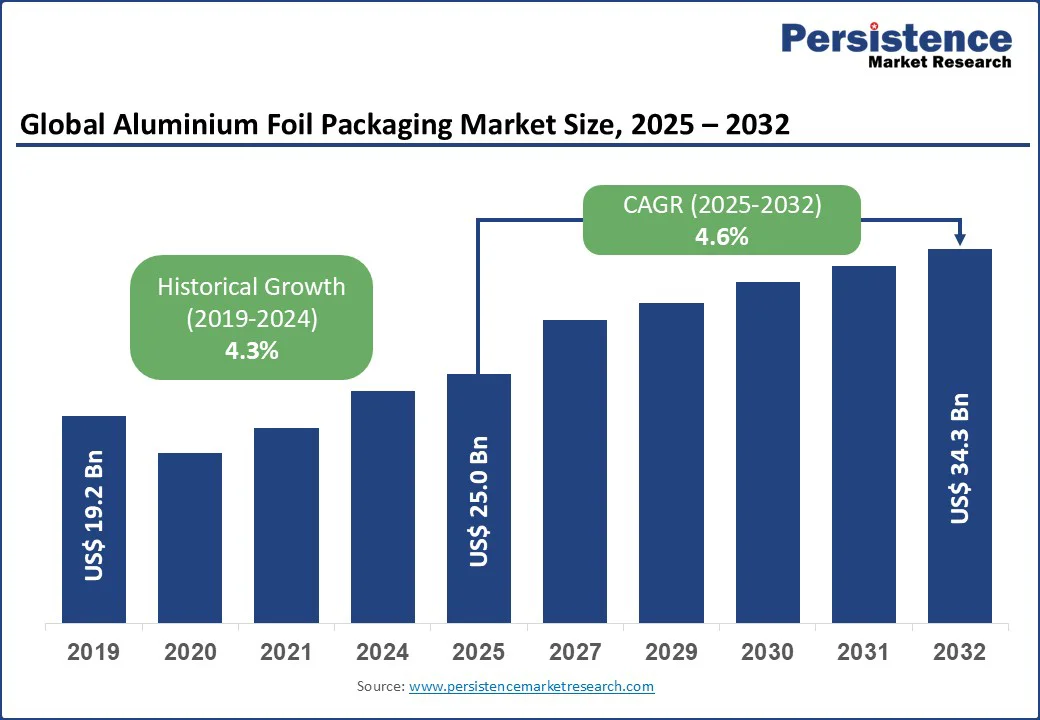

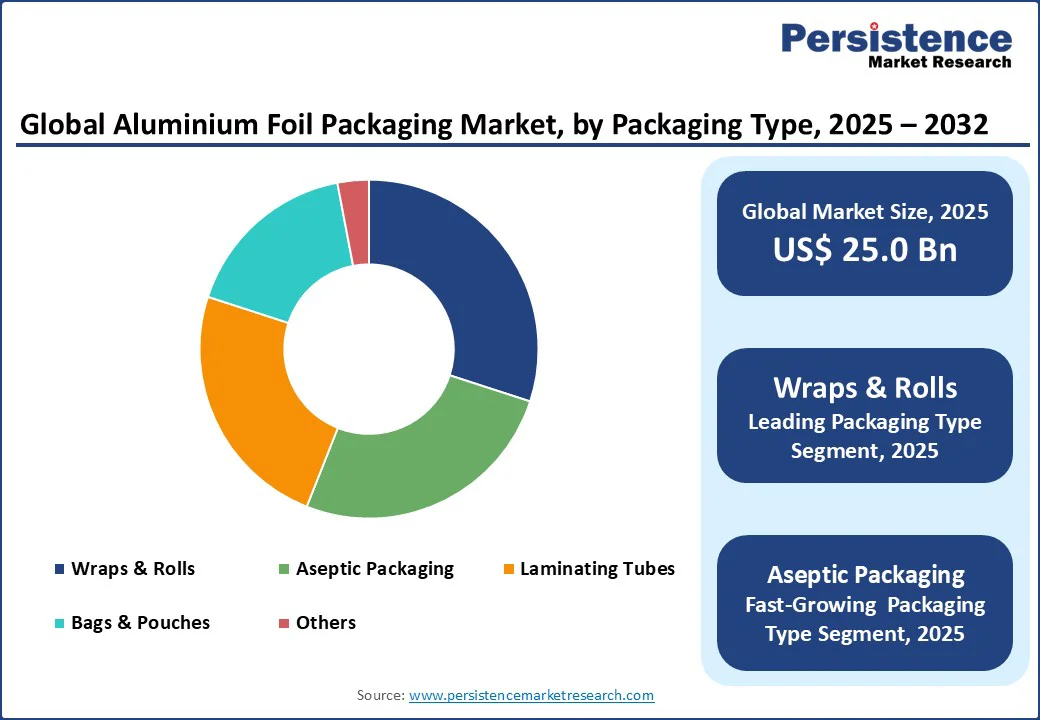

The global aluminium foil packaging market size is likely to be valued at US$25.0 Bn in 2025 and is expected to reach US$34.3 Bn by 2032, growing at a CAGR of 4.6% during the forecast period from 2025 to 2032.

The growing demand for sustainable and recyclable packaging, rising consumption of ready-to-eat meals, and expanding use of aluminium foil in the food, beverage, and pharmaceutical industries fuel the need for aluminum foil packaging. It offers superior barrier properties against moisture, oxygen, and contaminants, ensuring product safety and extended shelf life, fueling adoption. Moreover, government regulations promoting eco-friendly packaging and technological advancements in aluminium foil production are further propelling growth, making it a preferred choice across global consumer and industrial applications.

Key Industry Highlights:

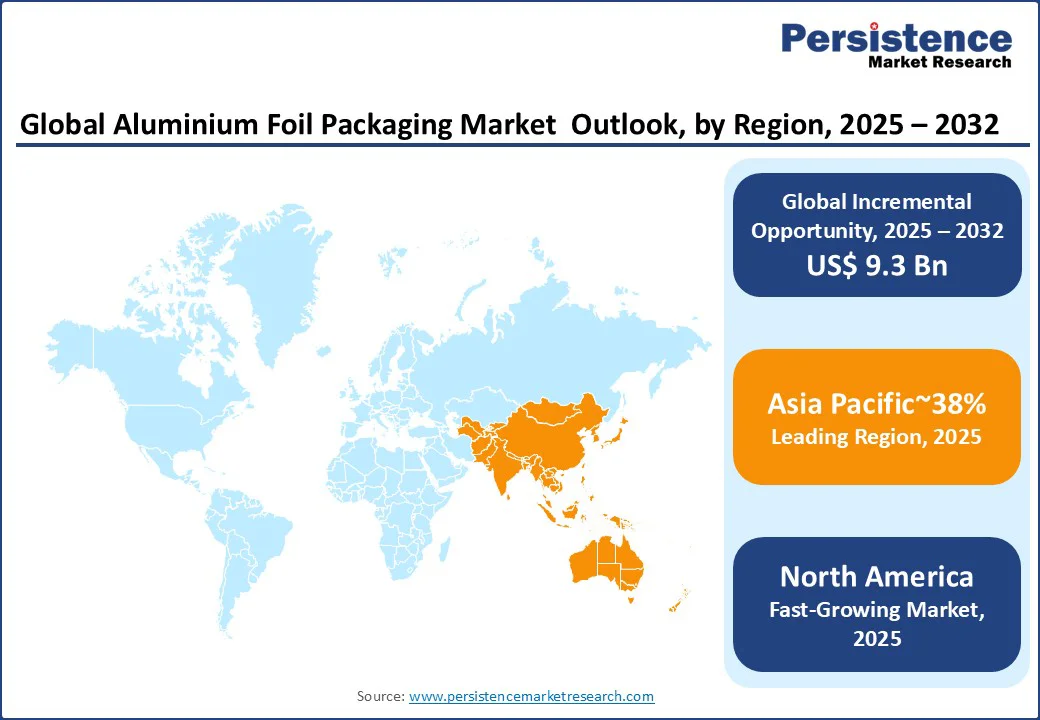

- Dominant Region: Asia Pacific leads the global aluminium foil packaging market with a 38% share in 2025, driven by strong demand from food, beverage, and pharmaceutical sectors in China and India.

- Fastest-growing Region: North America is the fastest-growing market, supported by high adoption in packaged food, ready meals, and pharmaceutical blister packs, along with sustainability-focused initiatives.

- Leading Thickness Type: 0.007 mm–0.09 mm remains the leading thickness segment with a 40% share, favored for its lightweight, flexible, and cost-effective use in food packaging.

- Leading Packaging Type: Wraps & rolls dominate with around 30% share, owing to their widespread application in household and commercial food preservation.

- Prominent End-use: The food & beverages sector accounts for nearly 45% of total demand, driven by rising packaged food consumption and convenience trends.

- Key Developments: In 2024, Amcor introduced recyclable foil solutions, while Hindalco expanded aluminium production capacity in India.

|

Global Market Attribute |

Key Insights |

|

Aluminium Foil Packaging Market Size (2025E) |

US$25.0 Bn |

|

Market Value Forecast (2032F) |

US$34.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.3% |

Market Dynamics

Driver - Growing Demand for Sustainable and Lightweight Packaging Solutions

One of the major drivers of the aluminium foil packaging market is the growing demand for sustainable and lightweight packaging solutions. As industries face mounting pressure to reduce environmental impact, aluminium foil offers a practical alternative due to its recyclability, low weight, and ability to reduce transportation emissions. For instance, the U.S. Environmental Protection Agency (EPA) emphasizes that sustainable packaging conserves resources and helps businesses lower costs and improve waste management efficiency.

Aluminium foil aligns well with these objectives by providing high barrier protection with minimal material use. Its lightweight nature reduces overall packaging volume while ensuring product safety, particularly in food and pharmaceutical applications. Governments and regulators across regions are encouraging a transition towards recyclable packaging, reinforcing the role of aluminium as a preferred choice. This combination of functionality and eco-friendliness continues to make aluminium foil packaging a strong driver of market growth.

Restraint - Volatile Raw Material Prices

One of the major restraints for the aluminium foil packaging market is the volatility of raw material prices. Aluminium, being the core input, is highly-sensitive to fluctuations in global supply and demand, energy costs, and trade dynamics. Since the production process is energy-intensive, changes in electricity and fuel prices directly influence the overall cost of aluminium. This unpredictability often creates challenges for packaging manufacturers, making it difficult to maintain stable pricing structures.

Frequent variations in raw material costs put significant pressure on profit margins, particularly for small and medium enterprises that have limited flexibility in absorbing market shifts. It also hampers long-term planning and investment. For end-use industries such as food, beverage, and pharmaceuticals that depend on consistent packaging solutions, this instability creates additional supply chain risks. As a result, volatile raw material prices continue to be a critical barrier to steady market growth.

Opportunity - Demand for Recyclable and Customizable Foil Packaging

A major opportunity in the aluminium foil packaging market lies in the development of recyclable and customizable packaging solutions. With increasing consumer awareness about sustainability and stricter regulations on single-use plastics, companies are focusing on creating aluminium foil products that are easier to recycle while maintaining performance standards. The inherent recyclability of aluminium, combined with innovations in coating and lamination technologies, is enabling manufacturers to design packaging that meets both environmental requirements and functional needs.

Customization further adds value by allowing brands to differentiate their products through unique designs, printing options, and sizes tailored to diverse applications in the food, beverage, and pharmaceutical industries. This not only improves brand visibility but also caters to changing consumer preferences for personalized and eco-friendly packaging. By investing in recyclable and customizable foil packaging, companies can enhance their market position, capitalize on emerging demand trends, and align with global sustainability goals, thereby driving long-term growth opportunities.

Category-wise Insights

Thickness Insights

The 0.007 mm–0.09 mm thickness segment is expected to accounts for 40% share in 2025. This ultra-thin foil is widely used in food packaging applications, including wraps, pouches, and laminates, due to its lightweight, flexible, and cost-effective nature. Its superior barrier properties against moisture, oxygen, and light make it essential for preserving the freshness and portability of snacks, dairy products, and ready-to-eat meals. In 2024, nearly half of global food packaging relied on this thickness range, underlining its dominance in everyday packaging solutions.

The 0.09 mm–0.2 mm segment represents the fastest-growing category, supported by its rising adoption in pharmaceutical blister packs, laminated tubes, and premium food packaging. This thickness offers enhanced durability and reliable protection, ensuring product safety and extended shelf life. Increasing demand for blister packs in healthcare and flexible, high-strength solutions in food packaging is accelerating its growth. With strong application potential across multiple industries, this segment is set to play a significant role in shaping the future.

Packaging Type Insights

In the aluminium foil packaging market, wraps and rolls hold the leading position with nearly 30% market share in 2025. Their dominance is attributed to widespread use in both household and commercial food preservation, where they provide excellent convenience, flexibility, and reliable protection. In 2024, approximately 60% of household foil consumption was attributed to wraps and rolls, underscoring their importance in everyday storage and cooking. Valued for their versatility, ease of use, and recyclability, this segment continues to drive consistent demand across developed and emerging markets.

On the other hand, aseptic packaging is recognized as the fastest-growing segment, supported by rising demand for long-shelf-life beverages and dairy products. Its adoption in milk and juice cartons has surged, with a notable 15% increase in 2024, particularly in the Asia Pacific region, where packaged beverage consumption is expanding rapidly. Offering superior barrier protection and extended shelf stability, aseptic packaging is reshaping product distribution and storage, positioning it as a critical growth driver.

End-use Insights

The food and beverages sector dominates and accounts for nearly 45% share in 2025. Growth in this segment is strongly driven by the rising consumption of packaged food, ready meals, and e-commerce grocery deliveries, which require reliable and lightweight packaging. In 2024, approximately 70% of aluminium foil packaging was utilized for food applications, including trays, pouches, wraps, and laminates. These formats play a crucial role in ensuring product safety, freshness, and extended shelf life, making them indispensable in modern food distribution and retail channels.

The pharmaceutical industry represents the fastest-growing segment, fueled by the increasing need for secure, tamper-evident, and high-barrier packaging. Aluminium foil is a preferred material for blister packs, strip packs, and laminated tubes, as it provides strong protection against moisture, oxygen, and contaminants. In 2024, the use of blister packs for tablets and capsules increased by 10%, highlighting their growing adoption. With rising global healthcare demand and strict regulatory standards, pharmaceuticals are expected to drive significant future growth.

Regional Insights

North America Aluminium Foil Packaging Market Trends

North America is the fastest-growing market in the aluminium foil packaging industry, driven by strong demand in food and pharmaceutical applications. In the United States, nearly 40% of packaged food sales in 2024 used foil-based wraps, trays, and pouches, underscoring their importance in ready-to-eat meals and snacks. Canada is also experiencing growth, supported by sustainable packaging initiatives, with around 20% of dairy products adopting aseptic foil cartons backed by government recycling programs. Rising focus on eco-friendly solutions and high adoption across sectors continue to accelerate market growth in the region.

Europe Aluminium Foil Packaging Market Trends

Europe represents a significant market for aluminium foil packaging, supported by strong demand in food, beverage, and pharmaceutical applications. The region’s emphasis on sustainability and circular economy initiatives has accelerated the shift toward recyclable and lightweight packaging solutions. High adoption of aluminium foil in ready meals, dairy products, and pharmaceutical blister packs underlines its importance across industries. With stringent EU regulations promoting eco-friendly packaging and rising consumer awareness of recyclable materials, Europe continues to hold a substantial share, reinforcing its position as a key market in the aluminium foil packaging industry.

Asia Pacific Aluminium Foil Packaging Market Trends

Asia Pacific dominates the aluminium foil packaging market with around 38% share in 2025, driven by rapid growth in the food, beverage, and pharmaceutical industries. Rising urbanization, expanding e-commerce grocery sales, and increasing consumption of ready-to-eat meals have boosted demand for foil-based trays, pouches, and wraps. The region also leads in pharmaceutical blister pack adoption, supported by large-scale generic drug production. With strong manufacturing capabilities, cost advantages, and growing sustainability initiatives, the Asia Pacific region remains the leading region, setting the pace for global expansion.

Competitive Landscape

The global aluminium foil packaging market is characterized by innovation, sustainability initiatives, and expanding production capacities. Companies are focusing on lightweight, recyclable, and customizable solutions to meet rising demand in food, beverages, and pharmaceuticals. Advancements in barrier coatings, laminates, and eco-friendly technologies are shaping product development, while regional players emphasize cost efficiency and localized supply. Strategic partnerships, R&D investments, and compliance with packaging regulations further intensify competition, positioning sustainability and performance as core differentiators.

Key Developments:

- October 2024: Amcor announced the launch of ESSENTIELLE, a plastic-free aluminium and paper foil designed for premium beverage packaging, supporting sustainability goals and reducing reliance on plastic.

- July 2024: Hindalco committed to a major capacity expansion in aluminium and copper smelting operations in India, strengthening its position in sustainable metal production and supporting packaging industry demand.

- March 2023: Novelis unveiled plans to expand its aluminium recycling and rolling capacity in the U.S., enhancing the supply of high-performance foil products for food and beverage packaging.

Companies Covered in Aluminium Foil Packaging Market

- Amcor plc (U.S.)

- Constantia Flexibles (Austria)

- Qingdao Kingchuan Packaging (China)

- Henan Tendeli Metallurgical Materials Co., Ltd (China)

- Henan Huawei Aluminium Co., Ltd (China)

- Hindalco Industries Ltd. (India)

- Novelis (U.S.)

- ProAmpac (U.S.)

- RusAL (Russia)

- Pactiv Evergreen Inc. (U.S.)

- Hong Kong Daching Enterprises Limited (China)

- CAFCO (China)

- ALUFO (India)

- Others

Frequently Asked Questions

The aluminium foil packaging market is projected to reach US$25.0 Bn in 2025, driven by demand for sustainable packaging solutions.

Key drivers include rising demand for recyclable packaging, growth in the food and pharmaceutical industries, and technological advancements.

The aluminium foil packaging market will grow from US$25.0 Bn in 2025 to US$34.3 Bn by 2032, with a CAGR of 4.6%.

Opportunities include aseptic packaging innovations, expansion in emerging markets, and demand for pharmaceutical packaging.

Leading players include Amcor plc, Constantia Flexibles, Hindalco Industries Ltd., Novelis, ProAmpac, and Pactiv Evergreen Inc.