- Specialty & Fine Chemicals

- Green Building Material Market

Green Building Material Market Size, Share, and Growth Forecast, 2026 - 2033

Green Building Material Market by Product Type (Structural Product, Exterior Product, Interior Product, and Others), By End-user (Commercial, Residential, and Industrial), By (Material Type, Green / Low-Carbon Concrete, Thermal Insulation Materials (Mineral Wool / Glass Wool), Recycled Steel, Fly Ash Bricks / AAC Blocks, Low-VOC Paints & Coatings, and Others), and Regional Analysis for 2026 - 2033

Green Building Material Market Size and Trends Analysis

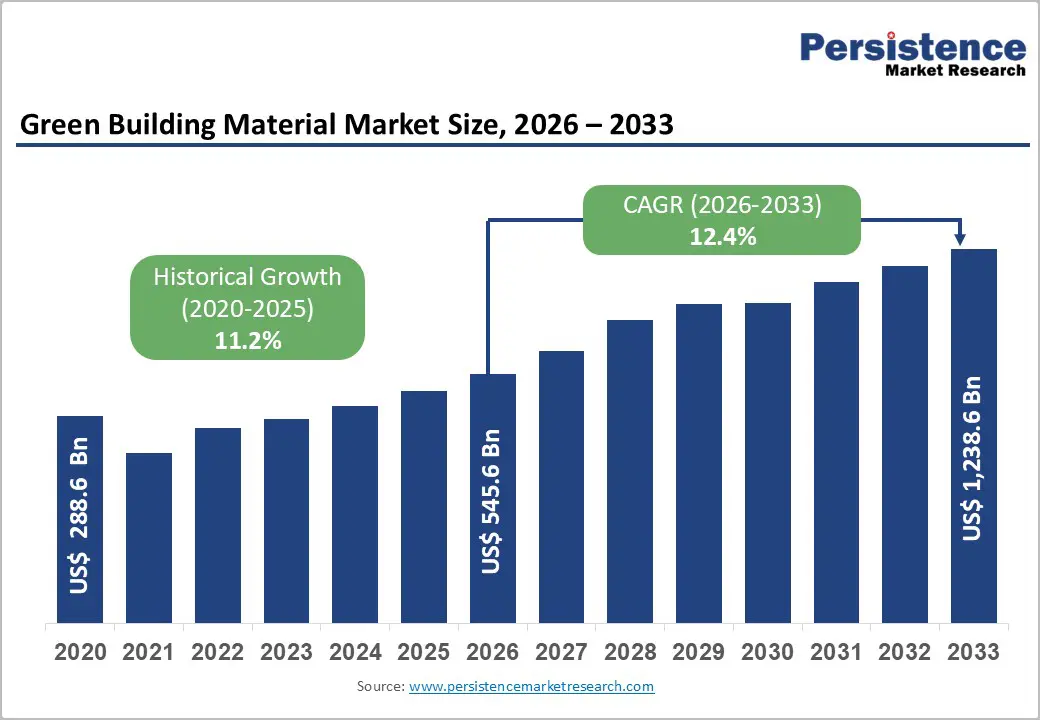

The global green building materials market size is likely to be valued at US$ 545.6 billion in 2026, and is projected to reach US$ 1,238.6 billion by 2033, registering an accelerated CAGR of 12.4% from 2026 to 2033. This robust growth reflects the construction industry’s structural shift toward environmentally responsible practices, driven by tightening regulatory frameworks, rising corporate sustainability commitments, and increasing investor demand for low-carbon, energy-efficient building solutions.

Beyond market expansion, green building materials represent a fundamental transformation in how buildings are designed and evaluated across their lifecycles. These materials are engineered to reduce carbon emissions, improve indoor air quality, lower energy consumption, and extend building longevity, while delivering measurable long-term cost savings. For commercial developers and non-profit organizations alike, adoption enables smarter capital allocation and stronger alignment with sustainability and ESG objectives.

Key Industry Highlights:

- Structural Products Leadership: Structural products maintain a dominant 45%+ market share through low-carbon concrete, recycled steel, and engineered timber applications, while exterior products emerge as the fastest-growing segment at 13.2% CAGR, driven by green roofing systems and advanced façade technologies.

- Thermal Insulation Market Expansion: Thermal insulation materials represent the fastest-growing material type at 13.8% CAGR, driven by building energy code stringency, net-zero building requirements, and lifecycle cost advantages delivering 20-30% operational energy reductions in building systems.

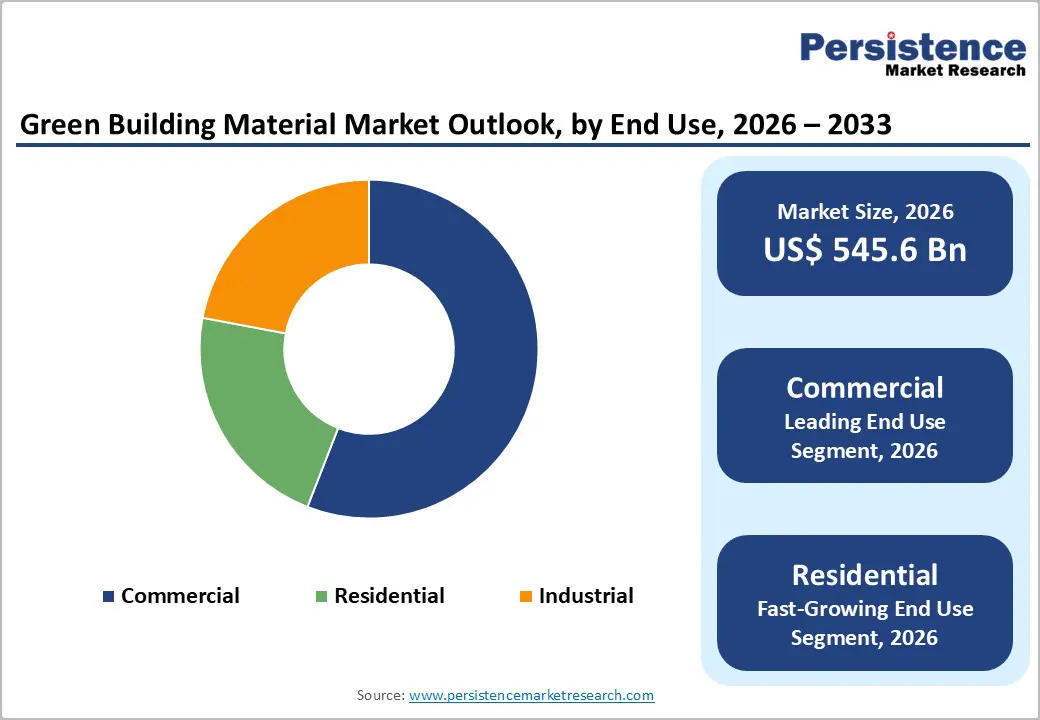

- Commercial Sector Dominance: Commercial construction maintains 45%+ market share through institutional investor ESG mandates and corporate decarbonization commitments, while residential construction emerges as the fastest-growing end-use at 13.6% CAGR, driven by emerging market urbanization and residential retrofit expansion.

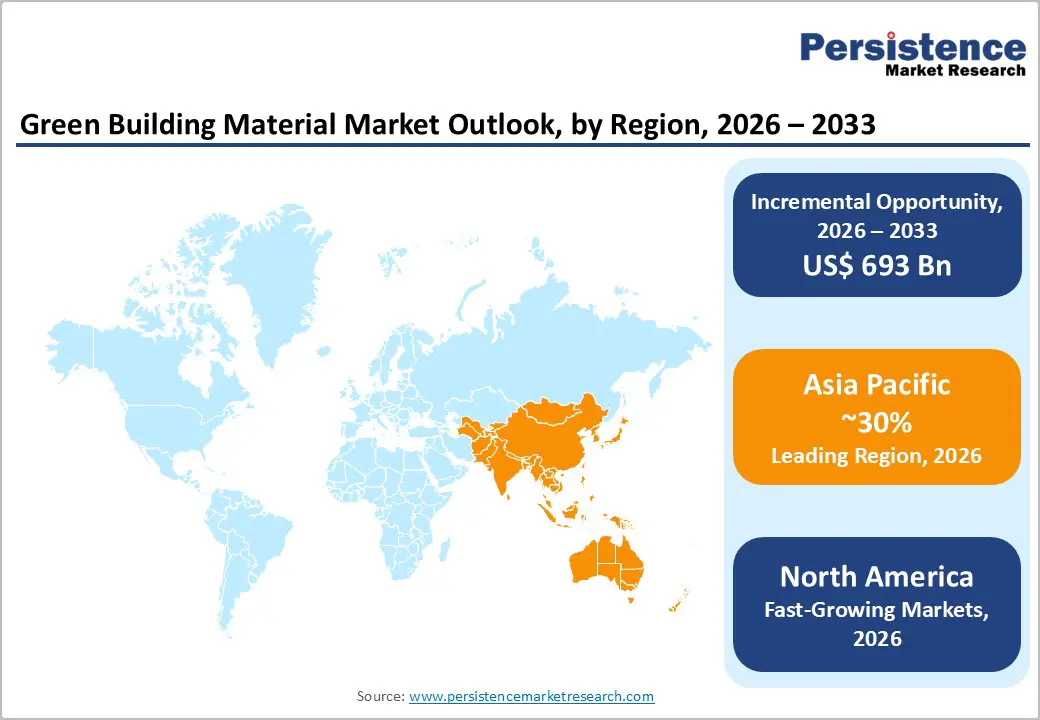

- Asia Pacific Regional Leadership: Asia Pacific commands 30%+ global market share with China, India, and Southeast Asia collectively generating 45-48% of global construction demand, while North America experiences 13.5% CAGR growth driven by federal procurement requirements and state-level building performance mandates.

- Regulatory Structural Drivers: Mandatory green building certifications (LEED, BREEAM, IGBC), building energy code stringency escalation, low-carbon procurement mandates, and circular economy compliance requirements are creating systematic market demand expansion independent of cyclical economic factors.

| Key Insights | Details |

|---|---|

|

Green Building Material Market Size (2026E) |

US$ 545.6 Bn |

|

Market Value Forecast (2033F) |

US$ 1,238.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.2% |

Market Dynamics

Drivers - Stringent Regulatory Frameworks and Green Building Certifications

Regulatory mandates and building performance standards represent the primary structural driver of green building materials adoption across developed and emerging markets. Government agencies and international organizations have established mandatory sustainability requirements that obligate construction stakeholders to specify environmentally certified materials in building projects.

The U.S. Environmental Protection Agency (EPA) promotes sustainable construction through ENERGY STAR certification programs and Smart Growth initiatives, while Australia's Low-Carbon Concrete Requirements specify minimum embodied carbon reductions of 40% for general concrete and 45% for structural applications, creating measurable compliance pathways for builders and concrete suppliers.

Green building certification systems, including LEED (Leadership in Energy and Environmental Design), BREEAM (Building Research Establishment Environmental Assessment Method), and IGBC (Indian Green Building Council) have transitioned from voluntary market differentiators to competitive necessities in commercial real estate portfolios, driving material specification decisions across institutional property development. In North America, bipartisan legislative initiatives have mandated the use of low-carbon construction materials in federally funded infrastructure projects, effectively creating procurement preferences that accelerate market adoption.

The European Union's Energy Performance of Buildings Directive (EPBD) requires substantial energy efficiency improvements in building renovations, generating significant demand for advanced thermal insulation materials and low-VOC interior finishes. These regulatory frameworks directly correlate to material cost tolerance and create market expansion opportunities valued at approximately US$ 180-200 billion through 2033, with regulatory compliance costs representing 12-15% of material specification budgets in developed markets.

Restraint - Cost Differential and Material Price Volatility

Premium pricing of green building materials relative to conventional alternatives creates persistent adoption barriers, particularly in price-sensitive emerging markets and residential construction segments. Green concrete formulations incorporating supplementary cementitious materials (fly ash, slag, silica fume) or low-carbon cement technologies command cost premiums of 15-25% compared to conventional concrete, creating capital budget pressures for project developers, particularly in markets with thin profit margins.

Thermal insulation materials manufactured from bio-based polymers (aerogels, vacuum insulation panels) display cost differentials of 40-60% relative to conventional mineral wool or fiberglass products, limiting adoption in cost-constrained residential and light commercial applications. Raw material cost volatility—driven by fluctuating energy prices, polymer feedstock markets, and iron ore commodities—creates procurement uncertainty that discourages long-term material specifications.

Recycled content materials, while environmentally advantageous, face supply chain inconsistencies and quality standardization challenges that require additional verification and testing protocols, increasing project delivery timelines by 2-4 weeks and adding 3-5% to material costs through third-party certification requirements. Developing economies in South Asia and Southeast Asia experience particular sensitivity to material cost differentials, as residential construction budgets remain constrained despite rapid urbanization, limiting green building material penetration below 8-12% of total construction materials procurement in these regions.

Opportunity - Emerging Markets Urbanization and Infrastructure Modernization

Rapid urbanization in Asia Pacific, Africa, and Latin America presents substantial material demand expansion, particularly for cost-effective green building solutions adapted to emerging market economic conditions. China, India, and Southeast Asian nations collectively account for approximately 45% of global construction investment, with urbanization rates accelerating at 2.5-3.2% annually through 2033. India's Housing for All initiative targets the construction of 20 million residential units by 2030, creating demand for thermal insulation materials, recycled brick alternatives, and low-cost green concrete formulations. These emerging market opportunities are estimated at US$ 180-220 billion through 2033, with particular strength in affordable housing segments where cost-effective green material innovations offer environmental benefits without premium pricing.

Infrastructure modernization programs—including transportation networks, water treatment facilities, and industrial manufacturing expansion—create specification opportunities for recycled steel, fly ash bricks, and low-carbon concrete. Local manufacturing expansion in emerging markets, supported by government industrial policy incentives and reduced logistics costs, is expected to compress cost differentials between green and conventional materials from the current 15-25% premiums to 5-10% premiums by 2030, substantially improving market adoption economics.

Category-wise Analysis

Product Type Insights - Structural Materials Dominate Green Building Market While Exterior Solutions Accelerate Growth

Structural products continue to hold a dominant position in the green building material market, accounting for approximately 45% of total revenue. This leadership is driven by their project-critical role, higher per-unit material costs, and strict building code and certification requirements. Structural components such as low-carbon concrete, recycled steel reinforcement, engineered timber, and composite systems represent the largest value segment, as building structures contribute nearly 60–65% of total embodied carbon in construction projects. This makes structural materials a primary focus area for cost-effective decarbonization efforts.

Within this category, low-carbon concrete is the leading sub-segment, contributing around 30–35% of structural material value. The use of supplementary cementitious materials, alternative cement chemistries, and carbon-capture-enabled concrete solutions is expanding rapidly while preserving performance standards. Recycled steel adoption is also increasing, supported by cost parity and circular supply chain benefits. Additionally, engineered wood products such as CLT and LVL are gaining traction in mid-rise commercial and institutional buildings, supported by expanding code acceptance and manufacturing capacity.

In contrast, exterior products represent the fastest-growing segment, expanding at a 13.2% CAGR. Growth is driven by stricter energy codes, urban heat mitigation needs, and renewable energy integration. Green roofing systems, advanced façades, and low-carbon insulation solutions are gaining momentum, with solar roofing and smart façade technologies delivering measurable energy savings and strong long-term value propositions.

End-user Insights - Commercial Construction Dominates, Residential Segment Emerges as Fastest-Growing Demand Driver

Commercial construction remains the dominant end-use segment in the green building material market, accounting for approximately 45% of total market value. This leadership is primarily driven by institutional investor demand for ESG-compliant assets, corporate net-zero commitments, and growing tenant preference for sustainability-certified workspaces. Office, retail, and hospitality developers increasingly use green building materials as competitive differentiation tools, with investors and occupiers favoring LEED- or BREEAM-certified properties. In addition to new construction, commercial renovations represent a significant demand driver.

Around 35–40% of existing commercial building stock is expected to undergo energy-efficiency upgrades by 2033, supporting sustained demand for thermal insulation systems, façade refurbishment materials, and low-VOC interior products. Corporate headquarters, research facilities, and institutional campuses have largely standardized green material specifications, particularly across life sciences, technology, and financial services sectors, where nearly 70–75% of new projects target recognized sustainability certifications.

Residential construction, while smaller in current value share, represents the fastest-growing end-use segment, expanding at a projected CAGR of 13.6%. Growth is supported by strong new housing demand in emerging markets and expanding retrofit activity in developed regions. Large-scale housing programs in India, continued urbanization in China, and middle-class expansion across Southeast Asia are generating robust demand for cost-effective green materials, including thermal insulation and green concrete. In North America and Europe, residential retrofitting is accelerating as 20–25% of housing stock requires deep energy-efficiency renovations to meet climate targets. Homeowners are increasingly prioritizing insulation upgrades and low-VOC paints, driven by energy cost savings, stricter building codes, and rising awareness of indoor air quality.

Material Type Insights - Low Carbon Concrete Dominates While Thermal Insulation Drives Fastest Growth

Green and low-carbon concrete continue to hold a dominant position in the green building material market, accounting for over 30% of total material-type revenue. This leadership reflects the central role of structural concrete in buildings and its significant potential for carbon reduction. The widespread use of supplementary cementitious materials (SCMs) such as fly ash, blast furnace slag, and silica fume enables embodied carbon reductions of 25–35% compared to ordinary Portland cement, while preserving required structural performance. Emerging innovations, including carbon-capture integrated concrete and geopolymer formulations, further enhance decarbonization potential, offering 35–50% and 40–45% carbon reductions respectively. Recycled concrete aggregates are also gaining traction, particularly in non-structural applications, with penetration expected to rise from 5–7% today to 12–15% by 2033. However, adoption in price-sensitive markets remains constrained by cost premiums of 12–18%.

In contrast, thermal insulation materials represent the fastest-growing segment, expanding at a robust 13.8% CAGR. Growth is driven by tightening energy efficiency regulations, rising energy costs, and net-zero building mandates. Mineral wool and glass wool dominate due to cost efficiency, fire resistance, and compatibility with standard construction systems. Advanced insulation solutions such as aerogels, vacuum insulation panels, and phase-change materials are expanding rapidly in high-performance applications, while bio-based insulation materials are gaining momentum in regions prioritizing circular economy principles.

Regional Insights and Trends

Asia Pacific Leads Global Green Building Materials Market Through Regulation-Driven Construction Growth

Asia Pacific holds a dominant position with over 30% of global green building materials market share and is expected to retain leadership through 2033. The region includes the world’s largest and fastest-growing construction markets-China, India, Japan, and Southeast Asia-collectively accounting for US$ 2.3–2.5 trillion in annual construction spending, or nearly 45–48% of global investment. Green material adoption is accelerating from historical levels of 8–10% to an estimated 18–22% by 2033, driven by stricter energy regulations, carbon reduction targets, and ESG-focused investments.

China, representing 45–50% of regional market value, leads adoption through stringent Building Energy Codes, carbon peak commitments, and the Three-Star Green Building Certification system. These frameworks are driving strong demand for thermal insulation, low-carbon concrete, and energy-efficient façade materials. Cement industry decarbonization initiatives, including clinker reduction and alternative fuels, are expanding domestic low-carbon concrete availability, while large-scale insulation manufacturing supports cost competitiveness.

India’s green building material demand is supported by rapid residential construction under Housing for All and expanding commercial development in IT parks and institutional buildings. While price sensitivity limits premium material penetration in mass housing, tightening Energy Conservation Building Code (ECBC) norms are increasing adoption of insulation and low-carbon materials in commercial projects.

Japan demonstrates high market maturity, with 75–80% of new buildings meeting green material standards, supported by the Japan Sustainable Building Consortium (JSBC) and its CASBEE assessment system. Southeast Asia is an emerging growth region, where infrastructure investment, foreign capital inflows, and ASEAN regulatory harmonization are steadily expanding green material specifications.

North America’s Green Building Growth Driven by Regulation, ESG, and Decarbonization

North America accounts for approximately 20–22% of the global green building market value and is witnessing accelerated growth driven by regulatory innovation, corporate decarbonization commitments, and ESG-focused institutional investment. According to the U.S. Environmental Protection Agency and USGBC policy tracking, state legislatures in 2025 are increasingly aligning climate action, resilience, and building performance objectives. States such as California, Florida, and Nevada are advancing wildfire resilience, climate adaptation, and tax incentives using LEED and its resilience pathway as compliance benchmarks, while New York’s proposed Healthy and Green Procurement Act mandates LEED Silver standards for large public projects. Building decarbonization remains central, with California and Colorado introducing performance standards, electrification incentives, and energy reporting requirements, even as states like Texas reflect divergent policy approaches. Code modernization efforts, K–12 and higher education infrastructure upgrades, and public-sector investments further reinforce sustainable construction demand.

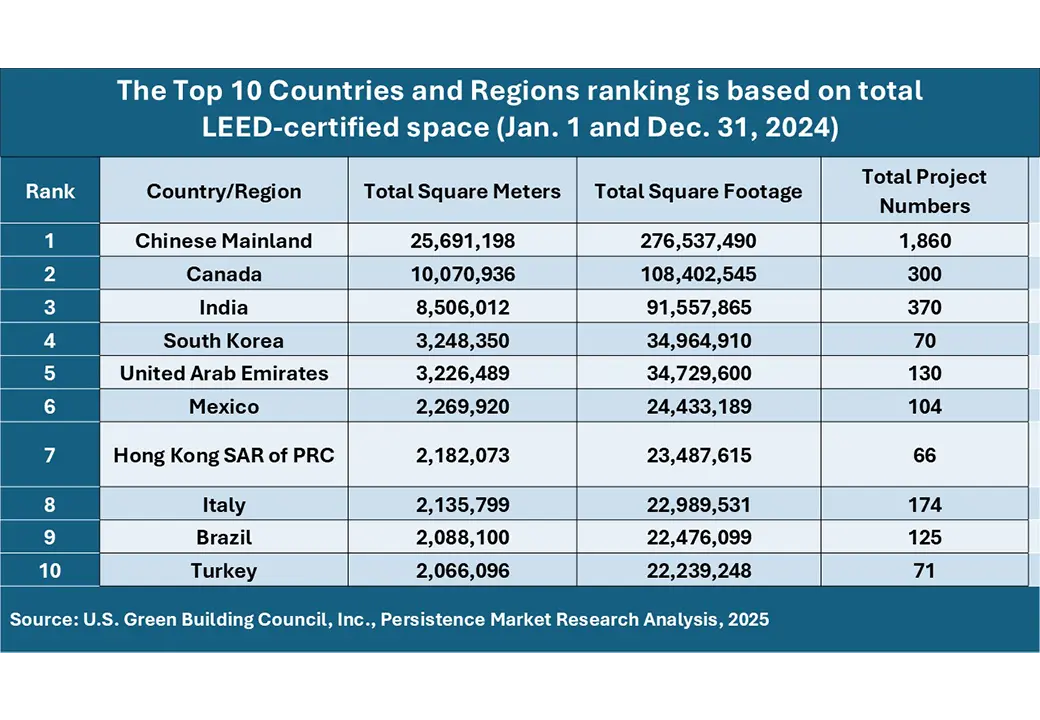

At the federal level, low-carbon material procurement policies are driving adoption of recycled steel, low-carbon concrete, and advanced insulation. The U.S. dominates the region with 85–90% share, supported by widespread LEED penetration and premium commercial valuations. Canada complements regional growth, recording over 10 million square meters of LEED-certified space in 2024, underpinned by net-zero building mandates, while Mexico shows emerging adoption in institutional and corporate projects.

Competitive Landscape

The global green building materials market is moderately consolidated, with large, established manufacturers holding strong competitive positions while specialized and regional players gain traction in innovation-led segments. Market dynamics vary across sub-segments such as low-carbon concrete, thermal insulation, recycled steel, and low-VOC coatings, each characterized by distinct cost structures, technical requirements, and entry barriers.

Major integrated players—including BASF, Lafarge-Holcim, Sika, and Heidelberg Materials—account for approximately 30–35% of total market value, supported by diversified product portfolios, extensive distribution networks, and long-standing institutional relationships. These companies continue to expand their green offerings through sustained R&D investment, strategic acquisitions, and in-house product development.

Mid-sized specialized manufacturers represent roughly 15–20% of the market, focusing on niche categories where technical expertise and customized solutions provide competitive advantage. Regional manufacturers, accounting for about 25–30%, compete effectively in localized markets by leveraging cost efficiencies and regulatory familiarity. Competitive intensity is increasing as conventional material suppliers transition capacity toward sustainable products, intensifying price competition, accelerating innovation, and strengthening demand for suppliers with comprehensive green portfolios and integrated sustainability credentials.

Key Industry Developments:

- On December 12, 2025, BASF strengthened its position in sustainable construction materials by expanding its spray polyurethane foam (SPF) portfolio with the launch of WALLTITE® RSB, a next-generation closed-cell insulation solution. Designed to address rising demand for low-carbon building materials, WALLTITE® RSB integrates recycled and renewable content while maintaining high thermal and air-sealing performance. The product supports improved building energy efficiency and reduced lifecycle emissions, aligning with stricter green building standards and decarbonization goals in the construction sector.

- On January 17, 2025, Canon Inc. announced the adoption of scrap-recycled electric furnace steel in selected printing and office equipment products launching in 2025. While primarily a manufacturing initiative, the move contributes to the broader green building materials ecosystem by increasing demand for recycled steel and strengthening circular supply chains. Canon will also supply steel scrap from used multifunction devices to steel producers, supporting material recycling and reduced dependence on virgin steel.

- On November 27, 2024, STARK Group advanced circular construction practices in Europe by introducing recycled bricks across all its Danish branches. This initiative aims to lower embodied carbon in building projects, reduce construction waste, and support Denmark’s green transition objectives, reinforcing recycled masonry as a viable low-carbon building material.

- On April 18, 2023, Holcim launched ECOCycle®, a proprietary circular construction platform enabling the recycling of 100% of construction and demolition waste into new building materials. The technology supports low-carbon cement production, recycled aggregates for concrete, and fillers for road construction, significantly accelerating circularity and decarbonization in the global building materials industry.

Companies Covered in Green Building Material Market

- PPG Industries

- BASF SE

- Dupont de Nemours

- Sika AG

- Forbo International SA

- Owens Corning

- REDBUILT

- HOLCIM

- CERTAINTEED

- Kingspan Group

- Other Market Players

Frequently Asked Questions

The Green Building Material market is estimated to be valued at US$ 545.6 Bn in 2026.

The key demand driver for the Green Building Materials market is the tightening of building energy efficiency and carbon reduction regulations, combined with rising lifecycle cost awareness among developers and asset owners.

In 2026, the Asia Pacific region will dominate the market with an exceeding 30% revenue share in the global Green Building Material market.

Among end-user, construction has the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other end-users.

PPG Industries, BASF SE, DuPont de Nemours, Sika AG, Forbo International SA, Owens Corning, and REDBUILT. There are a few leading players in the Green Building Material market.