- Specialty & Fine Chemicals

- Decorative Exterior Materials Market

Decorative Exterior Materials Market Size, Share, Trends, Growth, Regional Forecasts from 2026 to 2033

Decorative Exterior Materials Market by Material Type (Stone & Stone Veneers, Metal Planes & Cladding, Wood & Wood Composites), Application (Exterior Wall Cladding & Facades, Roofing & Exterior Coverings, Decking & Outdoor Flooring), Construction Type, and Regional Analysis 2026 - 2033

Decorative Exterior Materials Market Share and Trends Analysis

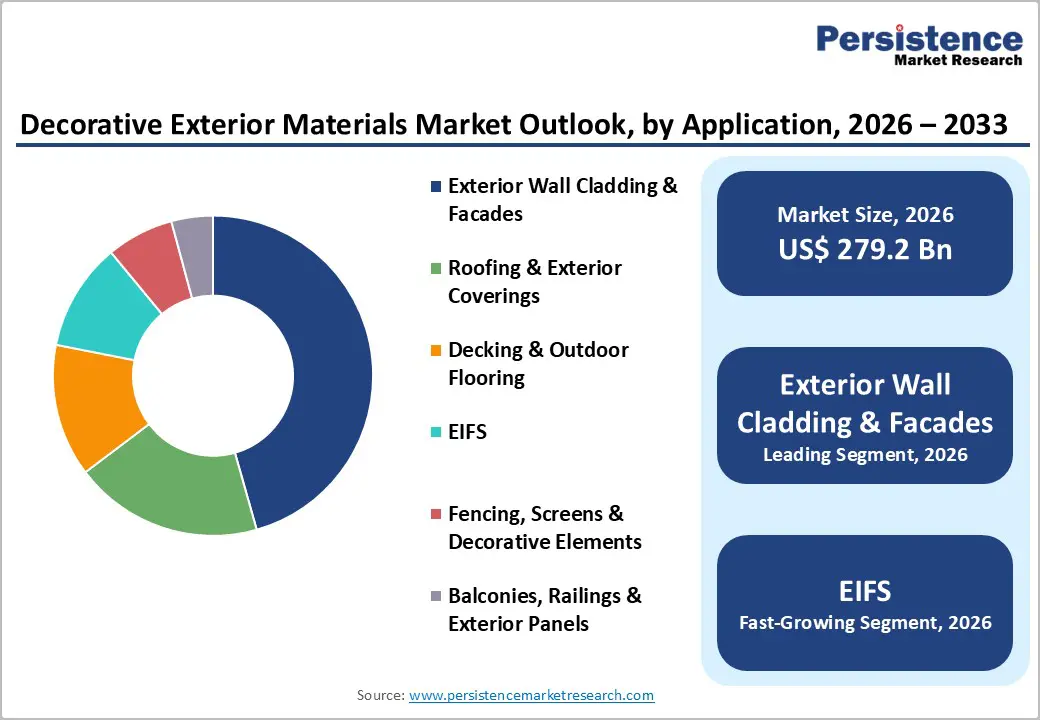

The global decorative exterior materials market size is likely to be valued at US$ 279.2 billion in 2026 and is projected to reach US$ 417.1 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

Market expansion is driven by accelerating residential renovation activity, urbanization across developing economies, regulatory mandates for energy-efficient building envelopes, and growing demand for aesthetically superior facade solutions that combine durability with environmental sustainability.

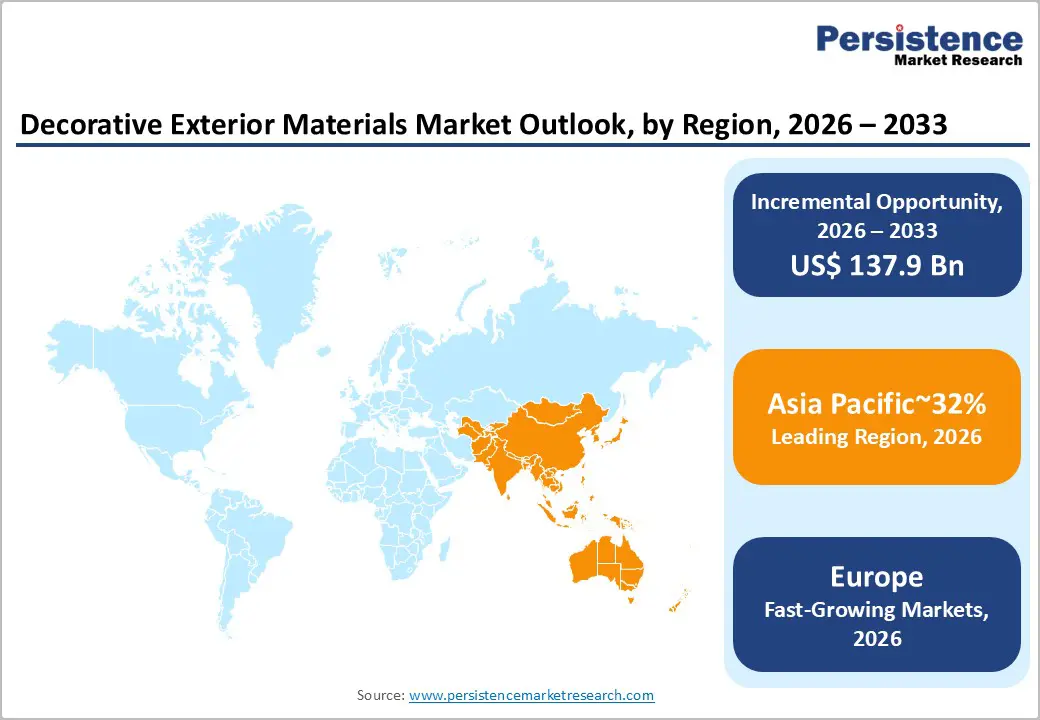

Asia Pacific dominates the global market with a 32% regional share expanding at 6.3% CAGR, supported by rapid urbanization and residential construction in China and India, while North America and Europe collectively represent 53% market value, driven by home renovation cycles and strict energy efficiency building codes.

Key Industry Highlights:

- Exterior wall cladding and facades lead applications with a 46% market share, while EIFS is the fastest-growing segment at 6.6% CAGR, driven by building code mandates for thermal efficiency and sustainability across residential and commercial construction.

- Stone and stone veneers dominate material types with a 23.5% share, whereas fiber cement boards grow fastest at 6.8% CAGR due to superior durability, fire resistance, and rising adoption in residential siding and commercial cladding.

- New construction accounts for 62.7% of market share, while renovation and remodeling expand at a 6.3% CAGR, reflecting demand for modernizing the aging housing stock and enhancing property values globally.

- Asia-Pacific leads with 32% market share and 6.3% CAGR, supported by urbanization and residential construction in China and India, while North America and Europe together hold 53%, driven by renovation cycles and efficiency regulations.

- Key players, including Owens Corning, Saint-Gobain, Kingspan, and James Hardie, maintain advantages through integrated solutions, geographic expansion, and sustainability strategies, with 2024 - 2025 investments in India highlighting confidence in Asia-Pacific growth.

| Key Insights | Details |

|---|---|

| Decorative Exterior Materials Market Size (2026E) | US$ 279.2 million |

| Market Value Forecast (2033F) | US$ 417.1 million |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 5.0% |

Market Dynamics Analysis

Drivers

Accelerating Residential Renovation and Remodeling Activities

The global residential renovation and remodeling market, closely linked to demand for decorative exterior materials, is growing at a 4.6% CAGR, driving sustained demand for exterior cladding, facade systems, and decorative finishing materials. North America shows particularly strong renovation momentum, with aging housing stock over 30 years driving systematic replacement cycles as homeowners invest in kitchen upgrades, bathroom renovations, and exterior facade improvements to enhance property values and energy efficiency.

The U.S. residential remodeling market alone grows at a 4.8% CAGR through 2032, fueled by the adoption of work-from-home, which demands improved living spaces. Asia-Pacific markets, led by China and India, are demonstrating accelerated growth, driven by expanding middle-class populations prioritizing home modernization and aesthetics. Government incentives for energy-efficient retrofits, favorable financing, and consumer preference for sustainable materials are broadening renovation project scopes to include exterior wall cladding, roofing, and decorative facades, thereby boosting consumption of decorative exterior materials across residential portfolios.

Energy Efficiency Regulations and Green Building Standards Driving EIFS Adoption

Governments worldwide are implementing strict energy-efficiency regulations, building codes, and environmental compliance frameworks that mandate thermal insulation performance, favoring exterior insulation and finishing systems (EIFS) and complementary cladding and facade materials to enhance comprehensive building envelope performance. The EIFS market is projected to grow significantly, driven by regulatory mandates, building codes, and commercial demand for high-performance thermal solutions that reduce operational energy costs. European Union energy directives require renovations to meet progressive efficiency standards, incorporating EIFS with complementary facade materials.

U.K. regulations emphasizing thermal performance and combustibility are driving the adoption of advanced EIFS in residential construction. France’s carbon-neutral objectives mandate EIFS capable of achieving Passivhaus and ultra-low-energy standards, with a 9.5% CAGR through 2035. U.S. energy codes and state efficiency mandates are accelerating EIFS use in residential and commercial construction, also growing at a 9.5% CAGR. Green building certifications (LEED, BREEAM, Living Building Challenge) reinforce high-performance facade specifications, supporting premium positioning and sustainable market share.

Restraints

Raw Material Cost Volatility and Supply Chain Disruptions

Decorative exterior materials manufacturing, including stone, metal, ceramic, fiber cement, and architectural glazing, remains sensitive to commodity price volatility, logistics disruptions, and supply chain constraints that limit production flexibility and extend delivery timelines. Stone and veneer rely on quarrying costs and the availability of transport. Metal panels track commodity cycles for aluminum and steel and energy inputs. Ceramic and porcelain tiles depend on energy-intensive firing, exposing producers to swings in electricity prices. Fragmented supply chains amplify disruptions, raise project costs, extend schedules, and suppress.

Regulatory Compliance Complexity and Fire Safety Standards

Decorative exterior materials face complex regulations covering fire safety, moisture resistance, installation protocols, and environmental compliance, varying by region and application. Stone veneers require fire ratings and combustibility testing. Metal claddings must meet fire, corrosion, and thermal standards. Fiber-cement boards require fire classification, moisture control, and structural certification. EIFS demand validated installation and weather barrier procedures. Divergent EU and North American standards increase compliance costs, restrict market access, complicate multi-regional operations, and slow expansion for manufacturers serving construction markets.

Opportunity

Emerging Market Penetration and Infrastructure Development in ASEAN and South Asia

Growing consumer and corporate demand for sustainable building materials is driving expansion opportunities for decorative exterior products featuring recycled content, renewable materials, low-impact manufacturing, and extended lifecycle performance that reduces replacement frequency. Thin stone veneer innovations, which use up to 95% less CO2 during transport than conventional slabs, offer environmental differentiation and premium positioning, attracting sustainability-focused designers and architects. Fiber cement boards increasingly emphasize recycled content, low-embodied carbon production, and fire-resistant durability, enhancing operational lifespan and reducing long-term environmental costs. Metal cladding solutions now highlight fully recyclable aluminum and steel, supporting circular economy objectives. Ceramic and porcelain tile manufacturers integrate recycled materials and low-emission production technologies to meet eco-friendly standards. Green building certification programs reinforce material transparency, lifecycle assessment, and environmental disclosure, strengthening sustainability-focused positioning across supply chains and expanding market share among eco-conscious segments.

Sustainability-Driven Material Innovation and Circular Economy Positioning

Rising consumer and corporate demand for sustainable building materials is driving growth opportunities for decorative exterior products featuring recycled content, renewable materials in construction, low-impact manufacturing, and longer lifecycle performance to reduce replacement needs. Thin stone veneer innovations, which use up to 95% less CO2 during transport than conventional slabs, offer environmental differentiation and premium positioning, appealing to sustainability-focused designers and architects. Fiber cement boards emphasize recycled content, low-embodied carbon production, and fire-resistant durability, extending operational lifespan and lowering environmental costs. Metal claddings promote the use of fully recyclable aluminum and steel, supporting circular economy goals. Ceramic and porcelain tile manufacturers integrate recycled materials and low-emission production techniques. Major construction companies, developers, and building owners increasingly embed environmental criteria into specifications and procurement, fostering favorable market conditions for sustainable products. Green building certifications emphasizing material transparency, lifecycle assessment, and disclosure reinforce sustainability positioning, enabling premium pricing and market share growth among eco-conscious segments.

Category-wise Analysis

Material Type Insights

Stone and stone veneer products dominate the decorative exterior materials market, with a 23.5% share, driven by aesthetics, durability, and premium positioning in luxury residential and high-end commercial projects. Natural stone cladding, granite, limestone, slate, and marble offer timeless appeal, weathering patina, and premium specification. Thin engineered veneers reduce weight and installation complexity, expanding use in renovations and residential applications. Demand is supported by fire resistance, minimal maintenance, and heritage architectural appeal.

Regional sourcing in Europe, Asia, and North America enables supply efficiency and local specification advantages. Emerging competition from engineered and alternative cladding materials may limit share growth compared to faster-growing segments.

Fiber cement products, the fastest-growing decorative exterior category, with a 6.8% CAGR, offer fire resistance, moisture and mold resistance, dimensional stability, and design versatility for residential siding, commercial cladding, and architectural applications. Adoption in renovations is rising due to durability, low maintenance, and cost-efficiency. Market growth is supported by North American leadership, expanded Asia-Pacific production, and sustainable, recycled-content manufacturing practices.

Application Insights

Exterior wall cladding and facade applications account for ~46% of the global decorative exterior materials market, integrating aesthetics, weather protection, thermal insulation, and maintenance performance across residential and commercial buildings. Facade cladding provides both weather barrier protection and architectural distinction through material, color, texture, and design innovation. Solutions include metal composite panels, ventilated and rainscreen cladding, and prefabricated cassette systems.

High-rise commercial projects specify advanced facades with integrated insulation, smart materials, and innovative attachment methods to meet energy compliance requirements. Residential renovations and commercial upgrades drive sustained demand, while regional economic conditions influence project timing. Long-term urbanization and population growth ensure resilient structural demand.

Exterior insulation and finishing systems (EIFS), growing at a 6.6% CAGR, are driven by energy-efficiency regulations, building codes, and commercial recognition of their superior thermal performance, which reduces operational energy costs. EIFS combines continuous insulation with reinforced finish coats, minimizing thermal bridging. Regulatory mandates, installation automation, prefabrication, and validated fire safety performance are accelerating adoption across residential, commercial, and renovation projects globally.

Construction Type Insights

New construction dominates decorative exterior materials, representing ~63% of market value, driven by envelope optimization in greenfield projects where architects and developers specify premium facades, advanced cladding, and integrated finishing systems without retrofit constraints. Residential construction enables a comprehensive selection optimizing aesthetics, durability, maintenance, and cost efficiency. Commercial projects, including high-rise office, hospitality, and institutional buildings, demand premium facades, glazing, and specialty cladding for distinctive architectural and sustainability performance.

Asia Pacific infrastructure expansion, with projected 1.5-2 billion new homes by 2050, systematically increases materials demand. Economic growth, investment cycles, interest rates, and demographics influence demand, while urbanization and infrastructure backlogs in emerging economies sustain structural growth and favorable market fundamentals.

Renovation and remodeling, growing at a 6.3% CAGR, drive demand for decorative exterior materials due to aging buildings, aesthetic upgrades, energy efficiency, and lifestyle adaptations. North America, Europe, and the Asia Pacific regions' renovations replace outdated facades with premium, durable materials that offer superior performance and visual appeal. Innovation in easier installation, reduced timelines, and lower costs expands market accessibility and supports extended service life with reduced maintenance.

Regional Market Insights

North America Decorative Exterior Materials Market Trends

North America maintains a prominent market share of approximately 27% of the global decorative exterior materials market, with mature infrastructure markets, substantial residential renovation activity, sophisticated building code frameworks, and high-performance material specification standards supporting premium product positioning and sustained demand growth. The United States dominates North American market dynamics, with the residential remodeling market driven by an aging housing stock (average age 37 years), an established renovation culture prioritizing kitchen, bathroom, and exterior envelope improvements, and homeowner investment in property value enhancement and energy efficiency upgrades.

Government incentive programs, favorable financing options, and tax credits for renovation investments are systematically expanding project scopes to include exterior wall cladding, roofing system upgrades, and facade modernization alongside interior improvements.

North America’s building codes, including International Building Code adoption, drive high-performance cladding, EIFS, and advanced facade specification for fire safety, structural integrity, and energy efficiency. Manufacturers focus on modular systems, prefabrication, and improved installation methods to reduce costs and timelines. Commercial renovations across offices, retail, and hospitality create sustained demand, while innovation and automation support premium pricing and performance differentiation.

Europe Decorative Exterior Materials Market Trends

Europe commands a considerable market share of 26% of the decorative exterior materials market, growing at a CAGR of 5.9%, supported by stringent environmental regulations, ambitious decarbonization objectives, sophisticated architectural heritage preservation requirements, and systematic building envelope modernization supporting sustainable urban development. Western European nations, particularly Germany, France, the United Kingdom, and Spain, exhibit mature renovation markets with established consumer preferences for sustainable materials, energy-efficient building upgrades, and contemporary design aesthetics.

German construction markets, incorporating stringent building efficiency standards (KfW Efficiency House classification), building rehabilitation, and energy performance mandates, are systematically incorporating EIFS, advanced cladding systems, and high-performance facade solutions into renovation projects targeting net-zero energy performance.

EU energy performance directives and 2023 revisions mandate improved thermal insulation and airtightness, accelerating the adoption of EIFS and advanced cladding. French carbon-neutral targets and UK thermal and combustibility regulations drive premium insulation and fire-resistant cladding specifications. Green certifications emphasizing sustainability, transparency, and lifecycle assessment support premium materials. Regional manufacturing in metal, ceramic, and fiber cement enables rapid delivery and local specification advantages across Europe.

Asia Pacific Decorative Exterior Materials Market Trends

Asia Pacific emerges as the leading regional market, with a market share of 32%, expanding at approximately 6.3% CAGR, driven by accelerated urbanization, rapid new construction expansion, a growing middle-class population prioritizing residential quality improvement, and emerging manufacturing capabilities supporting cost-competitive supply for regional and global markets. China represents the dominant market driver, with urbanization exceeding 60%, unprecedented residential construction volumes, and consumer demand for aesthetic residential improvements, supporting massive consumption of decorative exterior materials.

Chinese new construction incorporates contemporary facade systems, advanced cladding materials, and integrated finishing solutions as developers compete for consumer preference through architectural differentiation. Fiber cement product manufacturing in China is expanding to support both domestic and export demand, leveraging cost-competitive labor and advanced manufacturing technology.

India is the fastest-growing Asia Pacific market, driven by affordable housing targeting 20 million units, infrastructure investment, and rising middle-class property spending. Smart city and urban development programs generate commercial demand for premium facades and decorative cladding. Fiber cement production grows at 8.2% CAGR, supported by cost-competitive labor, natural material supply chains, technical expertise, and export opportunities, fueling regional and global market growth.

Competitive Landscape

The global decorative exterior materials market is moderately fragmented, with consolidation among multinationals like Owens Corning, Saint-Gobain, Kingspan, and James Hardie. Market entry barriers include specialized manufacturing, certifications, technical expertise, and capital-intensive infrastructure. Independent specialists such as Nichiha, Arconic, and CertainTeed compete through product focus, engineering customization, and regional expertise. Integrated solution providers offering complementary insulation, cladding, and facade systems gain competitive advantages.

Strategic Developments (Post-2023)

- In June 2024, Saint-Gobain announced plans to double mineral wool capacity in India, targeting USD 4.3 billion in revenue by 2032, backed by USD 719-959 million in capex and acquisitions to accelerate consolidation and expand its presence in the decorative exterior and insulation market.

- In August 2024, Rockwool announced a USD 65.5 million mineral wool facility in Cheyyar, Tamil Nadu, India, with commissioning in 2026 and a 50,000-tonne capacity, reinforcing confidence in residential construction growth, building envelope modernization, and localized supply efficiency.

- In June 2024, James Hardie maintained its number-one North American siding position, with products on over 10 million homes, supported by continued fiber-cement innovation, expanded design options, and installation simplification, driving contractor specification across renovation and new-construction markets.

Business Strategies

Market leaders pursue innovation, geographic expansion, sustainability leadership, and integrated solutions to sustain advantages. Strategies focus on next-generation materials with fire resistance, thermal efficiency, moisture control, modular prefabrication for installation, and digital design tools. Expansion targets the Asia-Pacific region via localized manufacturing and technical support. Sustainability differentiates through low-carbon processes, recycled content, lifecycle transparency, and certification alignment. Integrated portfolios enable system value.

Companies Covered in Decorative Exterior Materials Market

- Owens Corning

- Saint-Gobain S.A.

- Kingspan Group

- James Hardie Industries

- Boral Limited

- Rockwool International A/S

- Knauf Group

- Nichiha Corporation

- Arconic Corporation

- CertainTeed Corporation

- BASF SE

- Knauf Insulation

- ArcelorMittal Construction

- Hunter Douglas Architectural

- Metadecor

Frequently Asked Questions

The global decorative exterior materials market is likely to be valued at US$ 279.2 billion in 2026 and is projected to reach US$ 417.1 billion by 2033.

Market growth is driven by accelerating residential renovation spending, rapid Asia Pacific urbanization and housing expansion, and stringent energy efficiency and green building regulations promoting EIFS and advanced facade material adoption.

The decorative exterior materials market is expected to grow at a 5.9% CAGR from 2026 to 2033.

Key opportunities include emerging market penetration in ASEAN and South Asia, sustainability-led material innovation commanding premium pricing, and expanding EIFS adoption in renovation-driven thermal efficiency upgrades.

Major players include Owens Corning, Saint-Gobain, Kingspan, James Hardie, Boral, Rockwool, and Knauf, alongside regional specialists such as Nichiha, Arconic, CertainTeed, BASF, and Hunter Douglas, with recent investments underscoring strong Asia Pacific growth commitment.