- Specialty & Fine Chemicals

- Silicon Impression Material Market

Silicon Impression Material Market Size, Share, and Growth Forecast, 2026 – 2033

Silicon Impression Material Market by Product Type (Additional silicone (A-silicones), Condensation silicone (C-silicones)), Application (Medical application, Industrial application, Consumer products application), and Regional Analysis for 2026 – 2033

Silicon Impression Material Market Size and Trends Analysis

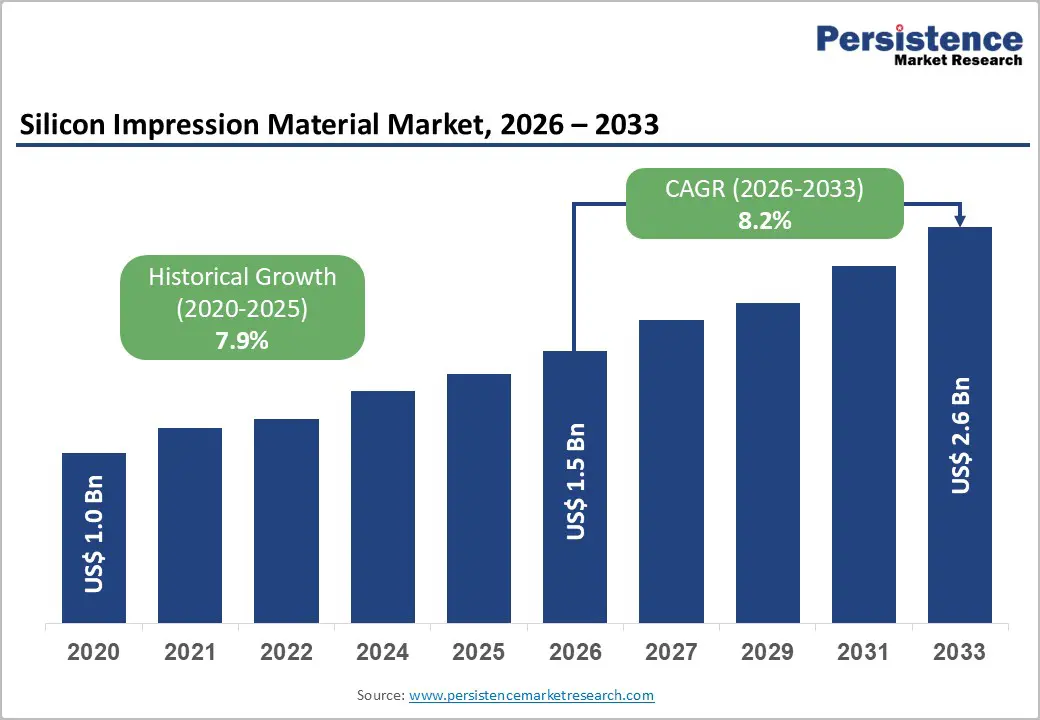

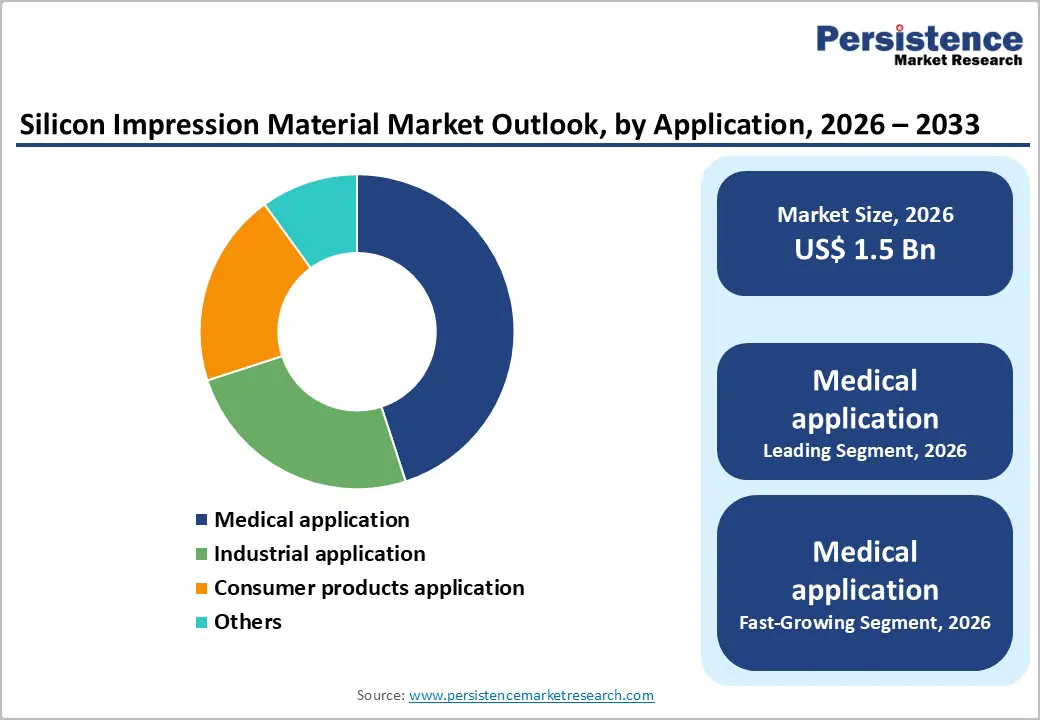

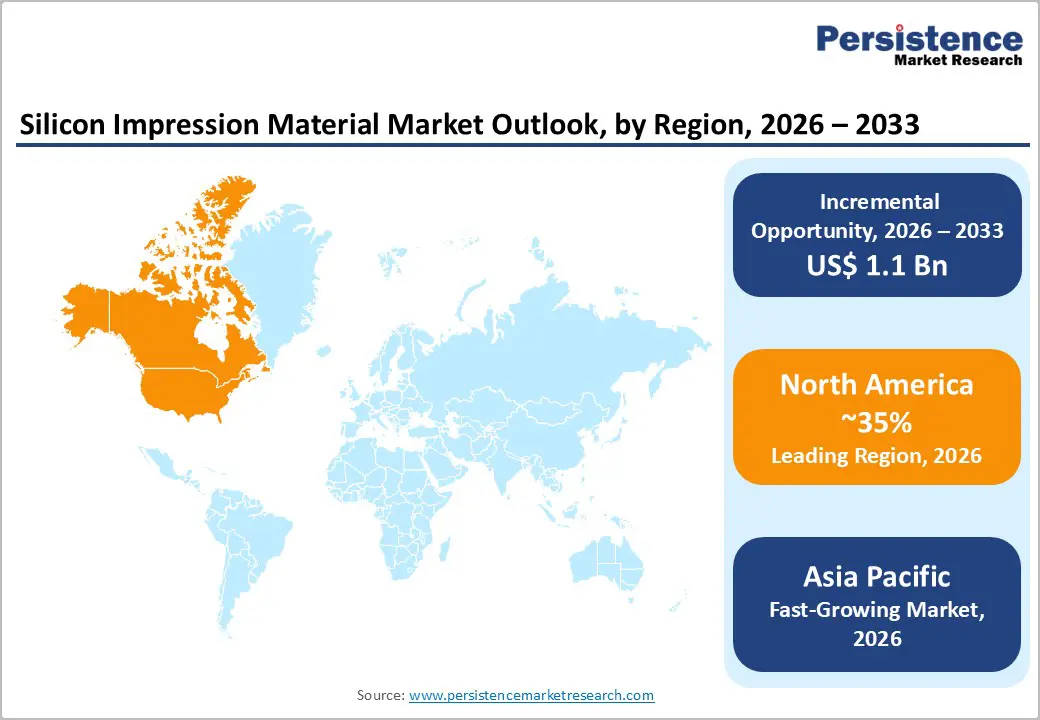

The global silicon impression material market size is likely to be valued at US$1.5 billion in 2026 and is expected to reach US$2.6 billion by 2033, growing at a CAGR of 8.2% during the forecast period from 2026 to 2033, driven by increasing oral health awareness, growing adoption of cosmetic and restorative dentistry procedures, and technological advancements in impression materials.

Expanding applications in medical prosthetics, industrial molding, and precision consumer products contribute to market expansion. The superior dimensional stability, accuracy, and biocompatibility of silicone materials continue to encourage adoption. The integration of silicone impression materials with digital dentistry workflows, such as CAD/CAM systems, is enhancing efficiency and precision in clinical practices. Growing investments in R&D by leading manufacturers are also fostering the development of faster-setting, hydrophilic, and environmentally friendly silicone formulations.

Key Industry Highlights:

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by high adoption of advanced dental materials, increasing demand for cosmetic and restorative dentistry, and strong healthcare infrastructure.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the silicon impression material in 2026, supported by rising dental awareness, expanding healthcare infrastructure, and increasing adoption of advanced dental materials.

- Leading Product Type: Additional silicone (A-silicones) is projected to account for 65% of revenue in 2026, driven by increasing demand for precision, hydrophilic, and digitally compatible formulations.

- Leading Application: Medical applications are expected to be the leading application type, accounting for over 60% of revenue in 2026, driven by rising dental procedures, cosmetic dentistry, and prosthetic needs.

| Key Insights | Details |

|---|---|

| Silicon Impression Material Market Size (2026E) | US$1.5 Bn |

| Market Value Forecast (2033F) | US$2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Prevalence of Dental Disorders

Conditions such as tooth decay, periodontal diseases, and missing teeth are on the rise due to changing lifestyles, poor oral hygiene, and aging populations. This trend has led to higher demand for restorative dental procedures, including crowns, bridges, implants, and dentures, which require accurate and high-quality dental impressions. Silicone impression materials, particularly addition-cure silicones, are preferred for their superior dimensional stability, precision, and biocompatibility, thereby ensuring optimal fit and patient comfort in complex dental treatments.

Rising dental disorders also fuel growth in cosmetic and prosthetic dentistry, increasing the adoption of silicone impression materials. As patients increasingly seek aesthetic enhancements and functional restorations, dentists rely on advanced materials for precise impressions. The aging population contributes to higher prosthetic needs, including dentures and implant-supported restorations. This demographic trend, coupled with awareness campaigns on oral health and regular dental check-ups, increases demand for premium silicone materials. The market is growing due to healthcare infrastructure improvements and the shift toward digital-compatible and hydrophilic silicone formulations for modern dental practices.

Demand for Cosmetic Dentistry

With increasing awareness of dental aesthetics and the rising desire for well-aligned, white, and visually appealing teeth, patients are seeking procedures such as veneers, crowns, bridges, and orthodontic treatments. High-precision silicone impression materials are essential in these procedures, providing accurate molds, dimensional stability, and fine detail reproduction, thereby ensuring optimal fit and a natural appearance. Dental clinics and laboratories are increasingly adopting addition-cure silicones due to their compatibility with modern workflows, reinforcing their preference in cosmetic dentistry applications across developed and emerging markets.

This demand is amplified by the influence of social media, celebrity culture, and growing disposable incomes, encouraging more patients to invest in aesthetic dental procedures. Technological advancements, including digital dentistry and (computer-aided design/computer-aided manufacturing) CAD/CAM integration, complement silicone impression materials, allowing faster and more precise outcomes. The rise in dental tourism in regions such as Asia Pacific has expanded access to cosmetic procedures, driving the adoption of premium impression materials. As cosmetic dentistry becomes more mainstream, the market for silicone impression materials continues to grow, supported by innovative formulations that enhance patient comfort and procedural efficiency.

Barrier Analysis - Dimensional Instability Issues

Dimensional instability can compromise the accuracy of dental and medical impressions. While silicone materials are preferred for their precision, factors such as improper mixing, extended setting times, and temperature or humidity variations can cause shrinkage or warping. This affects the fit of prostheses, crowns, or implants, thereby reducing clinical effectiveness and patient satisfaction. Despite advancements in addition-cure silicones with better stability and hydrophilic properties, dimensional changes remain a challenge in complex applications. In industrial and consumer sectors, minor deviations in silicone impressions can lead to defective components, increased rework, and higher costs. As digital dentistry grows, the need for stable, distortion-free impressions is critical for compatibility with scanning and CAD/CAM workflows, pushing innovation to overcome these material limitations.

Supply Chain Constraints and Raw Material Volatility

Key ingredients, including high-purity silicone polymers, catalysts, and additives, are sourced from specialized suppliers, making the market vulnerable to disruptions. Delays in procurement, fluctuations in availability, or geopolitical factors can affect production timelines, increase costs, and disrupt deliveries to dental clinics, laboratories, and industrial users. Manufacturers must manage these uncertainties while maintaining product quality and meeting regulatory standards.

Raw material price volatility further complicates matters, as fluctuations in silicone polymer costs directly affect the pricing of impression materials. Rising input costs can limit adoption in price-sensitive markets and reduce profitability for manufacturers and distributors. Transportation disruptions, trade restrictions, and increased competition for quality silicone feedstock can worsen the situation. To mitigate these risks, companies are diversifying sourcing strategies, securing long-term supplier contracts, and optimizing inventory, but the market remains sensitive to raw material and logistical uncertainties.

Opportunity Analysis - Expansion in Emerging Markets and Dental Tourism

Countries in Asia Pacific, Latin America, and the Middle East are experiencing rising disposable incomes, improved healthcare infrastructure, and increasing awareness of oral health. These factors are driving demand for restorative and cosmetic dental procedures, which rely heavily on high-quality silicone impression materials. Local dental clinics and laboratories are adopting premium silicones to ensure precision and patient satisfaction. Governments are supporting oral healthcare initiatives, creating a favorable environment for market penetration and the introduction of technologically advanced impression materials in these regions.

Dental tourism enhances market opportunities in emerging economies, particularly in countries such as India, Thailand, and Mexico, which offer high-quality dental treatments at lower costs. Patients from developed countries often travel to these regions for cosmetic and restorative procedures, increasing demand for reliable impression materials that ensure accurate prosthetic outcomes. Manufacturers can leverage this trend by supplying premium silicone products to clinics catering to international patients, emphasizing dimensional stability, biocompatibility, and compatibility with digital workflows.

Hybrid Digital-Compatible Materials

These advanced materials combine the traditional advantages of silicone, such as dimensional stability, tear resistance, and biocompatibility, with properties that enhance compatibility with digital dentistry workflows, including CAD/CAM scanning and 3D printing. Dental professionals increasingly prefer materials that integrate seamlessly with digital systems, allowing for faster, more accurate, and more efficient treatment planning. Manufacturers are focusing on hydrophilic, fast-setting, and high-precision formulations that reduce errors in impression-taking and improve prosthetic fit, supporting adoption in both premium and technologically advanced dental practices.

The adoption of hybrid materials also aligns with the growing trend of digital dentistry, in which dental clinics and laboratories use scanners, milling machines, and 3D printers for restorations and implants. Digital-compatible silicones enable accurate digital capture of oral structures, reducing the need for repeated impressions and enhancing patient comfort. This technological integration creates opportunities for product innovation, premium pricing, and differentiation in competitive markets. As more clinics adopt digital workflows, the demand for hybrid silicone materials that bridge traditional and digital methods is rising.

Category-wise Analysis

Product Type Insights

Additional silicone (A-silicones) is expected to lead the silicon impression material market, accounting for approximately 65% of revenue in 2026, driven by its superior dimensional stability, minimal shrinkage, and excellent accuracy in reproducing fine details, which are critical for dental and medical impressions. A-silicones are widely preferred for final impressions in restorative dentistry and prosthodontics, where precision directly impacts treatment outcomes. Their resistance to deformation during storage and transportation strengthens adoption across dental clinics and laboratories. For example, their extensive use in crown and bridge procedures, where clinicians rely on A-silicones to achieve accurate marginal fit and long-term prosthetic success.

Additional silicone (A-silicones) is also likely to represent the fastest-growing segment in 2026, supported by increasing preference for advanced, high-performance impression materials in modern dental practices. Growth is supported by rising demand for hydrophilic formulations that perform reliably in moist oral environments and integrate well with contemporary clinical techniques. The shift away from condensation silicones is accelerating as clinicians prioritize precision, efficiency, and consistency in outcomes. For example, their growing adoption in implant-supported restorations, where A-silicones enable accurate transfer of implant positions to dental laboratories.

Application Insights

Medical applications are projected to lead the market, accounting for approximately 60% of revenue in 2026, supported by extensive use in dental procedures, including impressions for crowns, dentures, bridges, and orthodontic appliances. Silicone impression materials are valued in medical settings for their biocompatibility, patient comfort, and ability to capture precise anatomical details. High procedural volumes in dental clinics and hospitals sustain consistent demand, particularly in restorative and prosthetic dentistry. For example, the widespread use of silicone impression materials in full and partial denture fabrication is where accuracy is essential for comfort, function, and long-term wear.

Medical applications are also likely to be the fastest-growing in 2026, driven by the increasing prevalence of dental disorders, rising demand for cosmetic dentistry, and an aging population requiring prosthetic solutions. Growth is particularly strong in implant dentistry and aesthetic restorations, where precision impressions are critical for successful outcomes. Expanding access to dental care in emerging markets and growth in dental tourism accelerate the adoption of silicone impression materials in medical settings. For example, the increasing use of silicone impressions in orthodontic treatment requires accurate modeling of tooth alignment to fabricate customized appliances.

Regional Insights

North America Silicon Impression Material Market Trends

North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by advanced dental care infrastructure, high procedural volumes, and rapid adoption of premium impression technologies. The region remains a leading contributor to revenue, supported by significant demand for restorative, prosthetic, and cosmetic dental treatments. Increasing awareness of oral health and robust insurance coverage enhances patient access to sophisticated procedures that rely on high-precision silicone materials for accurate molds. For example, 3M Company’s continued innovation and expansion of its vinyl polysiloxane silicone impression portfolio, which reinforces its competitive position in North America through enhanced clinical performance and clinician preference.

Integration with digital dentistry and hybrid workflows, where physical silicone impressions are increasingly paired with intraoral scanners and CAD/CAM systems to optimize precision and efficiency. This hybrid adoption improves turnaround times for prosthetics, reduces remakes, and satisfies the growing expectations of both clinicians and patients for seamless technology use. Technological advancements, such as hydrophilic silicones that perform reliably in the oral environment, are elevating North America’s market potential by expanding use cases beyond traditional applications.

Europe Silicon Impression Material Market Trends

Europe is likely to be a significant market for silicon impression material in 2026, due to established dental care systems, increasing patient awareness, and strong regulatory frameworks that uphold quality and safety standards. European countries such as Germany, the U.K., France, Italy, and Spain are key contributors, driven by the high prevalence of dental disorders and increasing demand for restorative, cosmetic, and implant dentistry procedures that rely on precision impression materials. The region’s market benefits from a mature healthcare infrastructure and widespread adoption of advanced dental practices.

European market is the focus of product innovation and competitive differentiation among leading dental materials companies. For example, Ivoclar Vivadent AG has advanced its presence by introducing eco-friendly and high-accuracy silicone impression products tailored to meet stringent European quality standards and clinician preferences. Ivoclar’s efforts to combine biocompatibility with enhanced clinical performance reflect broader market demands for materials that improve patient comfort and procedural outcomes. Partnerships and R&D investments across the region are enabling manufacturers to develop customized silicone formulations that satisfy specific clinical needs, such as hydrophilic properties for better moisture control and fast-setting options that reduce chair time.

Asia Pacific Silicon Impression Material Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by rising healthcare access, increasing oral health awareness, and expanding dental care infrastructure across major economies such as China, and India Rapid urbanization and growing disposable incomes have empowered patients to seek both restorative and aesthetic dental procedures, fueling demand for high-precision silicone impression materials that deliver superior dimensional stability and accurate detail reproduction. For example, GC Corporation’s strategic expansion of manufacturing capabilities in Southeast Asia, aimed at meeting rising local demand and reducing lead times for silicone impression products, helps improve regional supply responsiveness and cost competitiveness.

Another prominent trend shaping the Asia Pacific market is the rapid integration of technology and digital dentistry, underscored by increased uptake of intraoral scanners, CAD/CAM systems, and digital design workflows. Dental clinics and laboratories are keen to adopt materials that not only deliver traditional clinical precision but also integrate seamlessly with digital tools to improve accuracy, reduce remakes, and shorten turnaround times. This demand has encouraged manufacturers to innovate silicone formulations with enhanced hydrophilic properties and optimized scanning characteristics tailored for hybrid procedures.

Competitive Landscape

The global silicon impression material market exhibits a moderately fragmented structure, driven by the presence of several established multinational dental materials companies alongside regional and specialized players competing for share through innovation, distribution strength, and technology integration. Competition in this market revolves around product performance, formulation advancements, and alignment with evolving dental practices such as hybrid digital workflows.

With key leaders including 3M Company, Dentsply Sirona Inc., GC Corporation, Kerr Corporation, and Heraeus Kulzer GmbH, the competitive landscape is shaped by diverse strategic approaches to differentiate offerings and expand market influence. These players compete through innovative product portfolios, strategic collaborations, and regional expansions, often tailoring solutions to meet the specific needs of dental professionals in key regions such as North America, Europe, and Asia Pacific.

Key Industry Developments:

- In October 2025, Prusa Research, in collaboration with Filament2, announced that the Prusa XL 3D printer would support a dedicated silicone printhead. This new toolhead enabled multi-material 3D printing, combining silicone with rigid plastics in a single build. The solution, demonstrated with Polytek FS-20 silicone, was scheduled for commercial release in 2026, with details to be showcased at Formnext.

- In April 2025, Dentsply Sirona and Formlabs launched the Lucitone Digital Print Denture™ workflow, validated on Formlabs Form 4B dental 3D printers. This collaboration enabled dental labs to produce high-quality, single-arch, and complex dentures more efficiently, reducing processing time and improving consistency. The workflow supported the full range of Lucitone Digital Print materials, enhancing accessibility to advanced denture solutions.

- In February 2025, 3D Systems unveiled its new dental 3D printing solutions for silicone workflows at LMT Lab Day 2025. The NextDent 300 MultiJet 3D printer allowed direct printing of fully cured, multi-material dentures, eliminating post-curing steps and improving lab efficiency. The system also introduced FDA-cleared NextDent Jet Teeth and NextDent Jet Base materials, ensuring durability, aesthetics, and impact resistance.

Companies Covered in Silicon Impression Material Market

- 3M Company

- Dentsply Sirona Inc.

- Kerr Corporation

- Kulzer GmbH

- GC Corporation

- Ivoclar Vivadent AG

- Shofu Dental Corporation

- Zhermack SpA

- Septodont Holding

- Kettenbach GmbH & Co. KG

- DenMat Holdings, LLC

- Henry Schein, Inc.

- Patterson Companies, Inc.

- Ultradent Products, Inc.

- Parkell, Inc.

- DMG America, LLC

Frequently Asked Questions

The global silicon impression material market is projected to reach US$1.5 billion in 2026.

The silicon impression material market is driven by rising demand for accurate dental and medical impressions, fueled by growing cosmetic dentistry, increasing dental disorders, and advancements in high-precision, biocompatible materials.

The silicon impression material market is expected to grow at a CAGR of 8.2% from 2026 to 2033.

Key market opportunities include expansion in emerging markets and dental tourism, along with growing adoption of digital-compatible and hybrid silicone impression materials integrated with modern dental workflows.

3M Company, Dentsply Sirona Inc., Kerr Corporation, Kulzer GmbH, and GC Corporation are the leading players.