- Specialty & Fine Chemicals

- Electronic Board Level Underfill and Encapsulation Material Market

Electronic Board Level Underfill and Encapsulation Material Market Size, Share, and Growth Forecast 2026 - 2033

Electronic Board Level Underfill and Encapsulation Material Market by Product Type (Underfills (Capillary, Edge Bonds, No-Flow Underfill), Gob Top Encapsulations), Material Type, Board Type, Industry, and Regional Analysis, 2026 - 2033

Electronic Board Level Underfill and Encapsulation Material Market Size and Trend Analysis

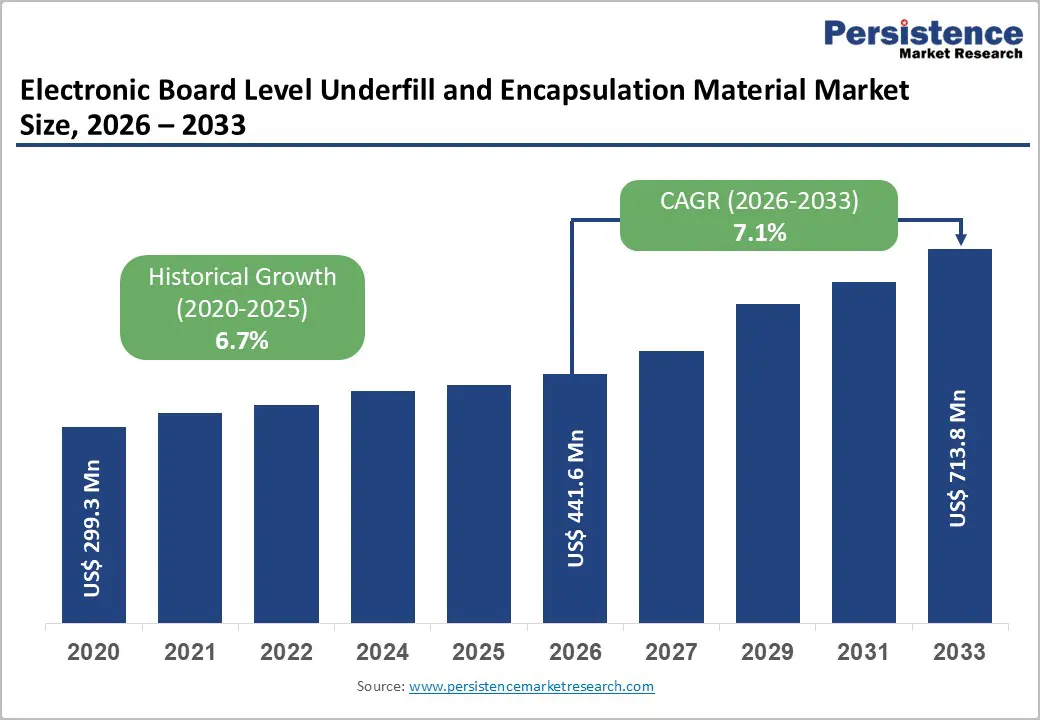

The global electronic board level underfill and encapsulation material market size is expected to be valued at US$ 441.6 million in 2026 and projected to reach US$ 713.8 million by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

This growth is fueled by the rising demand for miniaturized electronics and high-reliability packaging solutions across consumer, automotive, and industrial sectors. Advances in semiconductor technologies, including 5G, AI, and electric vehicles, require robust underfill and encapsulation materials to protect solder joints from thermal and mechanical stresses. Strong chip sales, totaling $574 billion in 2024, further drive the need for high-performance materials, supporting sustained market expansion.

Key Industry Highlights:

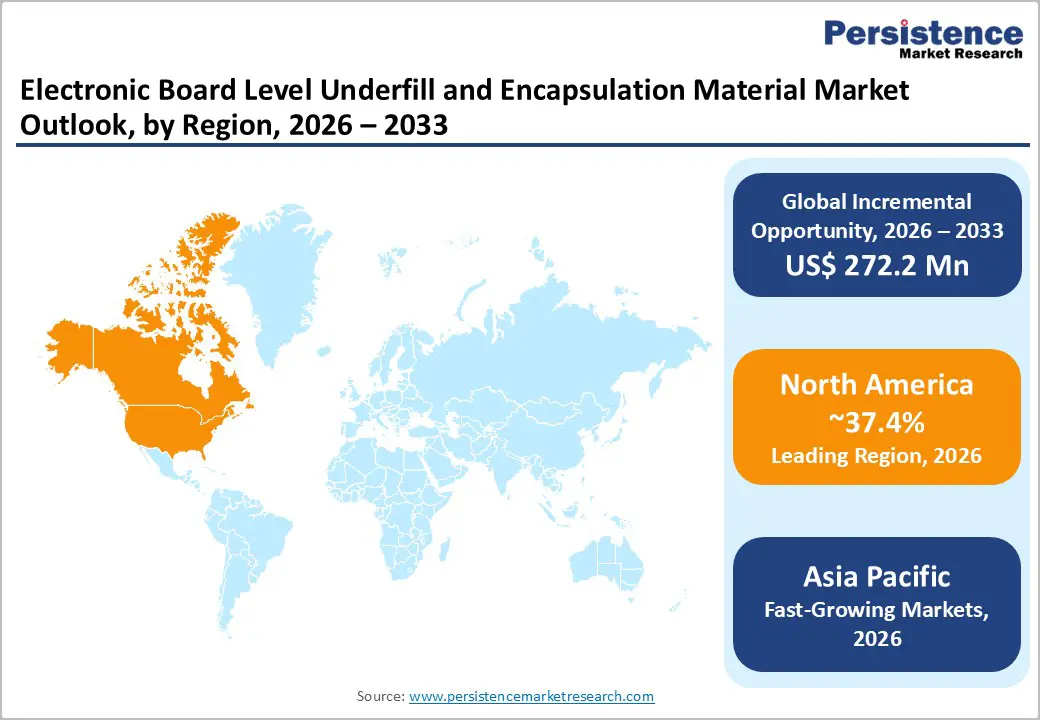

- Leading Region: North America leads the market with a 37.4% share in 2025, driven by U.S. innovation, CHIPS Act investments, and adoption in AI, EV, and 5G electronics.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with a 32.8% share in 2025, supported by China and Taiwan hubs, high-volume manufacturing, and technological innovation.

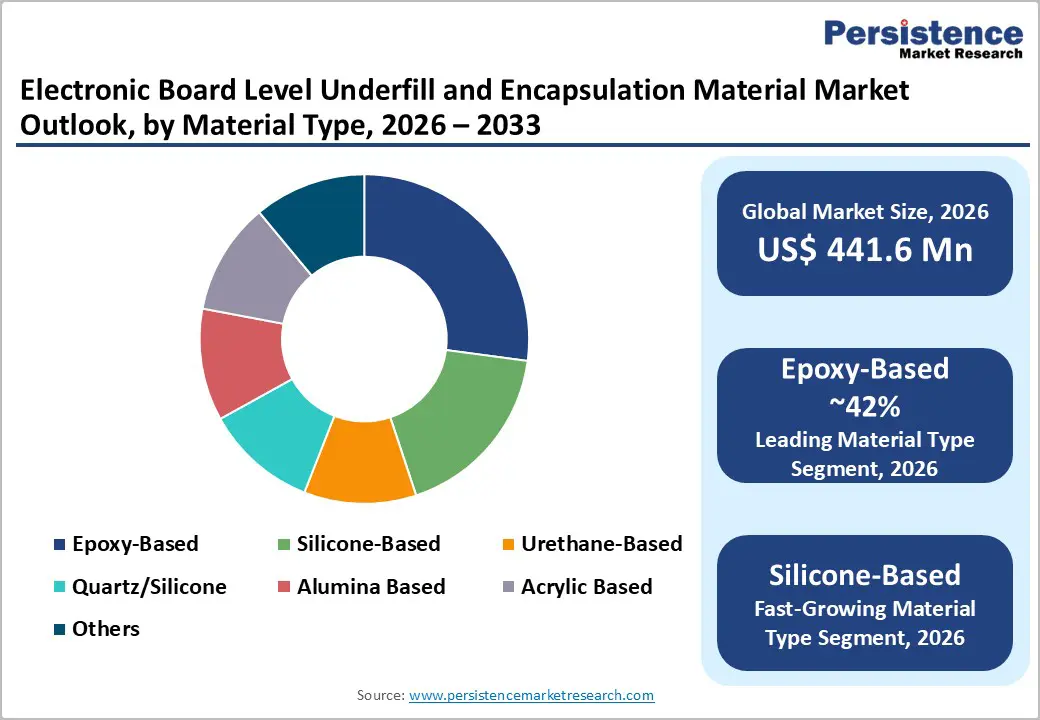

- Leading Material Type: Epoxy-based materials dominate the market with a 42% share in 2025, prized for high reliability, thermal stability, and lead-free solder compatibility.

- Fastest-Growing Board Type: BGA packages are the fastest-growing board type with a 50% share in 2025, essential for high-density, miniaturized devices requiring edge underfills to extend solder joint life.

- Key Market Opportunity: 5G infrastructure presents significant opportunities as billions of connections require reliable underfill and encapsulation materials to protect high-frequency modules and ensure signal integrity.

| Global Market Attribute | Key Insights |

|---|---|

| Electronic Board Level Underfill and Encapsulation Material Size (2026E) | US$ 441.6 million |

| Market Value Forecast (2033F) | US$ 713.8 million |

| Projected Growth CAGR (2026 - 2033) | 7.1% |

| Historical Market Growth (2020 - 2025) | 6.7% |

Market Dynamics

Drivers - Rapid Semiconductor Miniaturization and High-Density Packaging Driving Underfill and Encapsulation Demand

The ongoing trend of semiconductor miniaturization is significantly driving demand for electronic board-level underfill and encapsulation materials. As devices become more compact, fine-pitch connections in CSP, BGA, and WLCSP packages require reliable protection against mechanical and thermal stresses. These materials fill microscopic gaps, preventing solder fatigue and enhancing joint reliability in high-density boards.

According to IPC standards, capillary underfills can improve solder joint durability by up to 30%, which is critical in consumer electronics where over 1.5 billion smartphones are shipped annually. Additionally, the rise of heterogeneous integration in AI and high-performance chips increases the need for low-CTE, high-performance encapsulants to ensure operational stability under harsh thermal conditions.

Growth of Electric Vehicle Electronics and High-Reliability Applications Fueling Market Expansion

The rapid adoption of electric vehicles (EVs) is boosting the need for advanced underfill and encapsulation materials in automotive electronics. Power modules, inverters, and battery management systems require materials that can withstand high temperatures, mechanical vibration, and long-term thermal cycling. Durable epoxy underfills reduce delamination and solder fatigue by up to 40%, ensuring compliance with ISO 26262 safety standards.

With the International Energy Agency reporting 14 million EVs sold in 2024 a 25% increase, manufacturers are increasingly integrating high-reliability electronics into vehicles. This trend supports the adoption of advanced encapsulants for autonomous driving systems and electric powertrain modules, highlighting the role of robust material solutions in enabling safe and long-lasting automotive electronics.

Restraints - Rise in Raw Material Costs and Price Volatility Creating Market Challenges

The electronic board-level underfill and encapsulation material market faces significant restraints due to rising raw material costs. Epoxies, silicones, and specialty petrochemical-based resins have experienced 15-20% price increases, as reported by the American Chemistry Council in 2024. These fluctuations create challenges for manufacturers in maintaining consistent pricing and profitability.

Price-sensitive sectors, particularly consumer electronics, often resist passing these cost increases to end users, squeezing margins for smaller and mid-sized producers. In addition, supply chain disruptions further hinder scalability, especially for urethane-based and filler-heavy formulations, delaying production and affecting the timely delivery of high-performance materials for high-density assemblies.

Stringent Regulatory Compliance Requirements Slowing Market Growth

Compliance with strict environmental and safety regulations poses another restraint for the market. RoHS, REACH, and other mandates require manufacturers to reformulate materials to meet halogen-free and low-toxicity standards, adding 10-15% to development costs, according to the European Chemicals Agency (ECHA).

Certification delays under ISO 10993 and other medical or safety standards can further hinder product launches, particularly in medical and automotive applications. These compliance hurdles deter new entrants and slow innovation in highly regulated segments, limiting the speed at which advanced underfill and encapsulation materials can be adopted across sensitive electronics markets.

Opportunities - Rapid Expansion of 5G Infrastructure Driving Significant Market Opportunities

The global rollout of 5G networks presents lucrative opportunities for electronic board-level underfill and encapsulation materials. Base stations and small cells rely on BGA and CSP packages that require robust underfills to maintain signal integrity and protect against moisture and thermal stress. GSMA forecasts 2.5 billion 5G connections by 2025, growing at an annual rate of 20%, creating strong demand for reliable packaging materials.

Low-modulus, no-flow underfills are increasingly adopted to enhance mmWave performance, ensuring stable connectivity in dense network deployments. In addition, incentives from initiatives like the U.S. CHIPS Act support domestic production and innovation, enabling material manufacturers to scale advanced formulations, strengthen supply chains, and capitalize on the rapidly expanding telecommunications infrastructure market.

Growing Adoption of Medical Wearables Stimulating Innovative Material Development

The rise of medical and consumer wearable devices is driving demand for biocompatible encapsulants in electronic assemblies. Wearables incorporate sensors and Flip Chip components that require materials with high reliability under mechanical stress and moisture exposure. The World Health Organization reports a 30% adoption increase in wearable health devices post-2023, reflecting aging demographics and heightened health awareness.

Silicone-based and low-CTE encapsulants reduce failure rates by up to 25% while meeting FDA and ISO 10993 standards, ensuring safety and performance in continuous-contact applications. This trend encourages manufacturers to innovate material formulations for miniaturized electronics, opening opportunities in diagnostics, remote monitoring, and smart healthcare applications across global markets.

Category-wise Analysis

Product Type Insights

Underfill materials lead the market with a 48% share in 2025, driven by the dominance of capillary underfills in BGA packages. These materials excel at filling fine gaps, reducing vibration-induced solder fatigue, and improving thermal reliability. JEDEC studies report up to a 35% reduction in void formation, making underfills crucial in telecom, high-density computing, and miniaturized consumer devices. Edge bond underfills further reinforce joint stability in high-volume assemblies.

No-flow and molded underfills are emerging as the fastest-growing segments, particularly for advanced heterogeneous integration and flip-chip assemblies. Their ability to simplify assembly processes, support higher thermal loads, and maintain low-stress connections in complex, miniaturized devices is driving adoption across automotive electronics, 5G modules, and AI-enabled systems.

Material Type Analysis

Epoxy-based materials hold a 42% share in 2025, prized for their high glass transition temperature (>150°C) and strong adhesion (~20 MPa per ASTM D5229). Fast-curing epoxy formulations, often completed within 15 minutes, suit large-scale production and cover roughly 80% of board-level applications. Lead-free solder compatibility reinforces their dominance, particularly in consumer electronics and industrial electronics requiring reliable thermal and mechanical performance.

Silicone-based and urethane encapsulants are the fastest-growing materials, favored in high-temperature, flexible, and vibration-resistant applications. Their thermal shock resistance, elasticity, and chemical stability make them ideal for automotive power modules, EV battery management systems, and wearable electronics, where reliability and durability are critical under harsh operating conditions.

Board Type Insights

BGA (Ball Grid Array) dominates with a 50% market share in 2025, especially in high-performance servers and networking equipment requiring dense I/O configurations. Edge underfills applied to BGA packages can double solder joint fatigue life, enhancing reliability in telecom and computing applications. Cost-efficient manufacturing in Asia further strengthens BGA adoption, supporting both consumer and enterprise electronics deployment.

Flip-chip and wafer-level packaging (WLP) are the fastest-growing board types due to miniaturization and heterogeneous integration. These advanced packages demand underfills and encapsulants that can withstand tight pitches, high thermal loads, and mechanical stress, making them increasingly relevant in AI chips, 5G modules, and compact automotive electronics.

Industry Insights

Consumer electronics lead with a 38% share in 2025, powered by smartphone, tablet, and wearable production. Encapsulation protects CSP and BGA packages from drops, moisture, and thermal stress, reducing defects by approximately 25% per SMTA. High-density packaging in laptops, IoT devices, and smart appliances further reinforces this dominance, making consumer electronics the largest end-user segment globally.

Automotive electronics is the fastest-growing sector, driven by EVs, autonomous driving systems, and advanced ADAS modules. Increasing integration of power electronics, sensors, and high-reliability computing in vehicles requires robust underfill and encapsulation solutions capable of withstanding vibration, thermal cycling, and harsh operating environments, pushing manufacturers to innovate in epoxy, silicone, and hybrid formulations.

Regional Insights

North America Electronic Board Level Underfill and Encapsulation Material Market Trends

North America is the leading region with a 37.4% share of the global Electronic Board Level Underfill and Encapsulation Material market in 2025. The U.S. continues to drive innovation through the CHIPS Act’s $52 billion fab investments, boosting AI-focused encapsulants and advanced packaging technologies. SEMI reports 20% growth in high-density packaging, while EPA regulations encourage low-VOC epoxies for healthcare electronics, reinforcing the region’s leadership in sustainable material solutions.

FDA approvals for medical wearables further strengthen North America as a leading market for high-reliability underfill and encapsulation materials. The presence of R&D centers and manufacturing hubs supports rapid commercialization, enabling adoption across AI, EV, and 5G electronics, and solidifying the region’s position as an innovation and market growth leader.

Europe Electronic Board Level Underfill and Encapsulation Material Market Trends

Europe is a key market, driven by automotive, telecom, and industrial electronics. Germany’s Fraunhofer institutes are developing halide-free underfills for EVs, while VDI reports a 15% adoption increase post-2024 mandates. Horizon Europe funding (€95 billion) accelerates UK and France telecom initiatives, enhancing deployment of advanced packaging solutions.

Sustainability mandates such as RoHS and REACH ensure compliant materials across Spain and other regions. Europe is projected to grow at a steady 7.4% CAGR, reflecting consistent adoption and regulatory-driven innovation. The region is emerging as a reliable and growing market for advanced underfill and encapsulation technologies, particularly in EVs, 5G, and energy-efficient consumer electronics.

Asia Pacific Electronic Board Level Underfill and Encapsulation Material Market Trends

Asia Pacific is the fastest-growing and leading region, commanding a 32.8% share of the global market in 2025. China’s “Made in China 2025” initiative drives 70% of regional output, supported by MIIT investments of $50 billion in 2024. Japan’s JEITA leads high-precision Flip Chip production, while India’s PLI program strengthens local manufacturing capabilities.

Taiwan and ASEAN leverage TSMC and regional semiconductor hubs, driving encapsulant adoption. This fastest-growing region benefits from high-volume electronics manufacturing and technological innovation, positioning Asia Pacific as the market leader in advanced board-level underfill and encapsulation materials for automotive, telecom, and consumer electronics applications.

Competitive Landscape

The global electronic board level underfill and encapsulation material market is highly consolidated, with the top players controlling around 65% of the total market share. Leading companies focus on expanding their footprint through intensive R&D, strategic partnerships, and collaborations targeting high-growth sectors such as 5G infrastructure and electric vehicle electronics. Custom low-CTE formulations and advanced packaging solutions are key differentiators, enabling superior performance in high-density and high-reliability applications.

Sustainability and circular economy trends are driving the development of environmentally friendly materials and processes. Mergers and acquisitions in Asia are strengthening regional capabilities, enabling faster market penetration and technological innovation, while reinforcing the dominance of leading market participants globally.

Key Developments:

- In June 2025, Henkel AG & Co. KGaA introduced halide-free epoxy underfill materials for electric vehicle applications, offering a 25% improvement in thermal performance and enhanced reliability for high-density automotive packaging and power electronics assemblies.

- In March 2024, Dow Inc. launched advanced silicone-based encapsulation materials for 5G modules, providing 40% greater moisture resistance, improved thermal stability, and superior protection for high-frequency telecom components in base stations and small-cell devices.

- In October 2024, Shin-Etsu Chemical Co., Ltd. scaled production of quartz-reinforced underfill materials specifically for BGA packages in automotive electronics, enhancing solder joint fatigue life, thermal performance, and reliability under harsh operating and vibration conditions.

Companies Covered in Electronic Board Level Underfill and Encapsulation Material Market

- Henkel AG & Co. KGaA

- Namics Corporation

- ASE Group

- MacDermid Alpha Electronic Solutions

- Parker LORD Corporation

- H.B. Fuller Company

- Dow Inc.

- ELANTAS GmbH

- Zymet Inc.

- Hitachi Chemical Co., Ltd. / Showa Denko Materials Co., Ltd.

- Panasonic Corporation

- AI Technology, Inc.

- Indium Corporation

- Sanyu Rec Co., Ltd.

- Protavic International

Frequently Asked Questions

The market is projected at US$ 441.6 million in 2026, driven by electronics miniaturization and high-reliability packaging demand.

Growing miniaturization, EV electronics, and advanced packaging increase the need for underfill and encapsulation materials to ensure board reliability.

North America leads with a 37.4% share in 2025, supported by U.S. innovation, CHIPS Act investments, and AI/5G applications.

5G deployment offers major opportunities as billions of connections require protection and high-frequency performance.

Key players in the Electronic Board Level Underfill and Encapsulation Material market include Henkel AG & Co. KGaA, Namics Corporation, ASE Group, MacDermid Alpha Electronic Solutions, and Parker LORD Corporation.