- Specialty & Fine Chemicals

- Cold Insulation Materials Market

Cold Insulation Materials Market Trends, Size, Share, and Growth Forecast 2025 - 2032

Cold Insulation Materials Market by Material Type (Fiber Glass, Polyurethane Foam, Polystyrene Foam, Phenolic Foam, and Others), Insulation Type (Fibrous, Cellular, and Granular), Application (HVAC Systems, Refrigeration, and Others), Industry, and Regional Analysis for 2025 - 2032

Cold Insulation Materials Market Size and Share Analysis

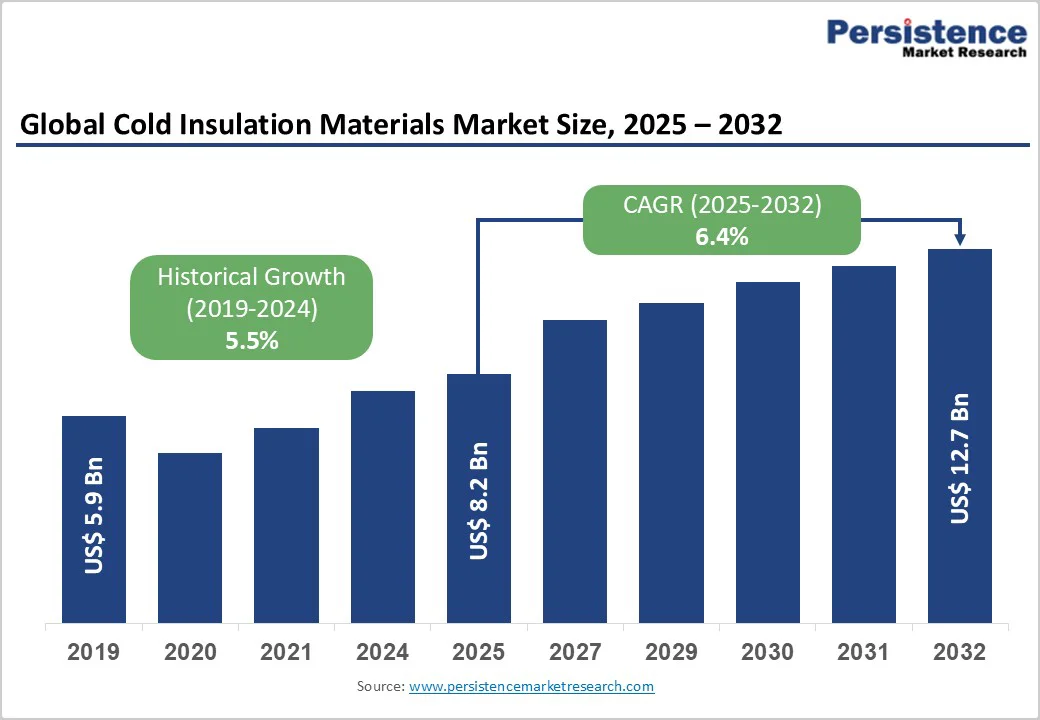

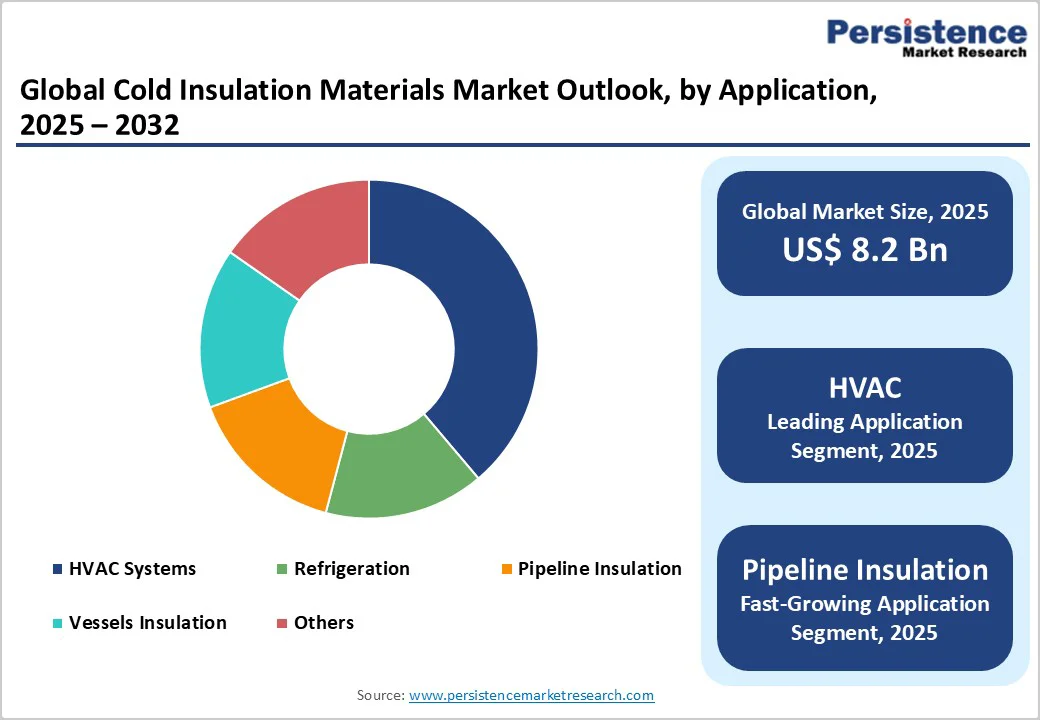

The global cold insulation materials market size was valued at US$8.2 billion in 2025 and is projected to reach US$12.7 billion, growing at a CAGR of 6.4% between 2025 and 2032. Market expansion is driven by accelerating demand for energy-efficient refrigeration systems, the rapid expansion of LNG infrastructure and cold chain logistics, and the increasing adoption of cryogenic insulation across the industrial, pharmaceutical, and food processing sectors.

Additionally, technological advancements in aerogel insulation materials, innovations in polyurethane foam, and regulatory emphasis on energy efficiency further stimulate market growth.

Key Market Highlights

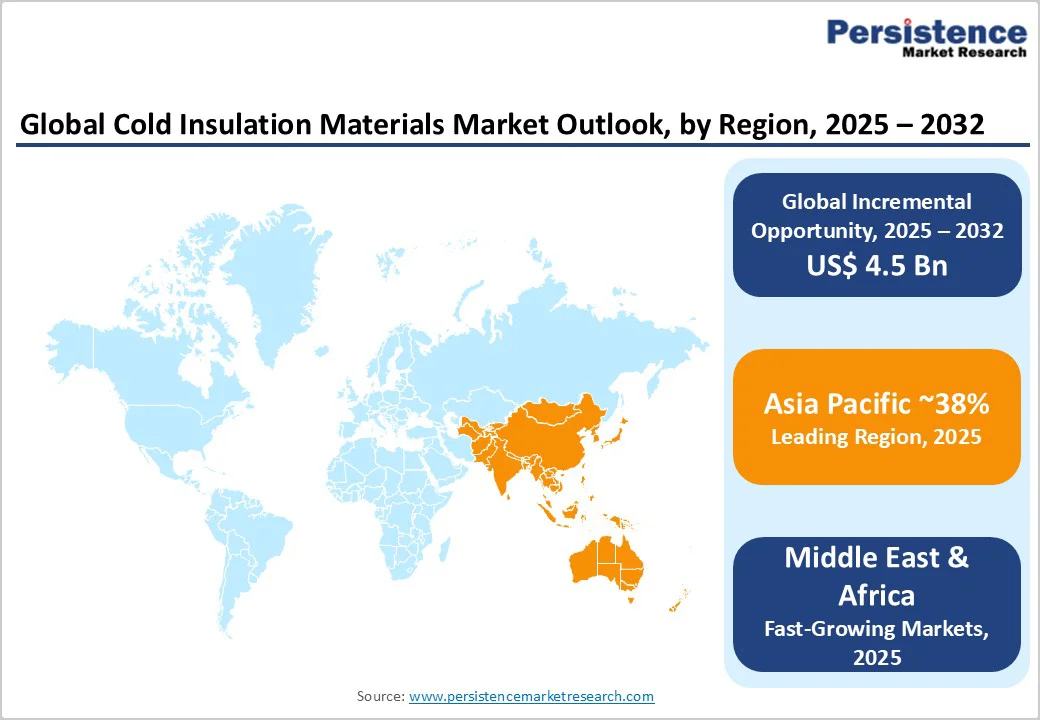

- Leading Region: Asia Pacific dominates the global cold insulation materials market, accounting for approximately 38% of total market share in 2025, driven by rapid industrialization, robust manufacturing growth, and expanding cold chain logistics infrastructure

- Fastest Growing Region: Middle East & Africa demonstrates the highest growth trajectory at approximately 6.8% CAGR, propelled by rapid industrialization, cold chain logistics expansion, manufacturing growth, and government infrastructure investment supporting long-term market expansion.

- Dominant Material Type: Polyurethane Foam commands the largest material type segment at 42% market share, driven by superior thermal conductivity, moisture resistance, versatile applications, and widespread HVAC and refrigeration adoption.

- Dominant Application: HVAC Systems represent the leading application segment in the global cold insulation materials market, accounting for approximately 34% of total market share in 2025.

- Key Market Opportunity: LNG infrastructure expansion targeting 500 million tonnes annual production by 2030 presents a substantial cryogenic insulation opportunity for specialized materials supporting storage, transport, and safety requirements.

| Key Insights | Details |

|---|---|

|

Cold Insulation Materials Market Size (2025E) |

US$8.2 Bn |

|

Market Value Forecast (2032F) |

US$12.7 Bn |

|

Projected Growth CAGR(2025-2032) |

6.4% |

|

Historical Market Growth (2019-2024) |

5.5% |

Market Dynamics

Drivers - Surging Liquefied Natural Gas Production and Cryogenic Infrastructure Expansion

Global LNG production and infrastructure expansion are demonstrating exceptional growth momentum, creating massive demand for specialized cold-insulation materials. Global LNG production is projected to exceed 500 million tonnes per year by 2030, requiring advanced cryogenic insulation for storage tanks, pipelines, and transport vessels operating at temperatures below -162 °C. LNG is stored and transported at extremely low temperatures, requiring superior insulation materials, including polyurethane foam, polystyrene, and phenolic foam, to prevent heat ingress and maintain cryogenic integrity.

Strategic LNG expansion projects, including Qatar's North Field Expansion Project, significantly increase demand for cryogenic insulation materials across upstream and downstream operations. Emerging LNG infrastructure across the Asia Pacific and Middle East regions drives multi-year procurement opportunities for high-performance insulation solutions. Superior thermal resistance, moisture control, and structural stability achieved through advanced material formulations justify premium pricing and sustained adoption among LNG operators prioritizing operational efficiency and safety.

Expanding Refrigerated Warehousing and Cold Chain Logistics Growth

Global cold chain logistics and refrigerated storage expansion create exceptional market opportunities driven by food safety regulations, pharmaceutical requirements, and e-commerce growth. Refrigerated warehouse capacity increased by 616 million cubic meters between 2016 and 2018, with continuing expansion across developed and emerging markets. China's surge in refrigerated warehousing demand reflects rapid urbanization, rising disposable incomes, and consumer preference for fresh and frozen products that require temperature-controlled storage and transport.

India's infrastructure development, targeting 500 million new urban residents, is generating substantial demand for cold storage facilities to support the food processing, pharmaceutical, and dairy industries. Global food and beverage industry expansion is driving refrigeration demand across manufacturing, distribution, and retail sectors. Advanced polyurethane and elastomeric foam insulation materials enable efficient temperature maintenance while reducing energy consumption, supporting cost optimization and regulatory compliance across cold chain operations.

Restraint - High Installation Costs and Specialized Labor Requirements

Cold insulation systems, particularly for industrial and cryogenic applications, require specialized materials and skilled installation labor, creating significant cost barriers. High-performance cryogenic insulation materials commanding premium pricing 15-30% above standard insulation products due to superior thermal properties and specialized manufacturing requirements. Installation expenses, which represent 40-50% of total project costs, require specialized technicians and equipment, limiting adoption among cost-sensitive market participants. Retrofitting existing infrastructure with modern insulation systems creates operational disruptions and additional expenses, particularly challenging for small and medium enterprises with budget constraints. Ongoing maintenance, inspections, and repairs add substantial operational costs, limiting profitability expansion, particularly in developing regions.

Health and Environmental Concerns Regarding Traditional Materials

Health and environmental concerns regarding traditional insulation materials create market headwinds and regulatory compliance pressures. Exposure to fiberglass insulation, which can cause respiratory irritation and eye discomfort, raises occupational health concerns among installation workers. Polystyrene foam emission of styrene, classified as a potential carcinogen, limits regulatory approval and mainstream adoption in certain applications, particularly sensitive healthcare and pharmaceutical environments. Ozone-depleting potential and global warming potential (GWP) concerns surrounding certain foam formulations drive regulatory restrictions, including phased bans in developed markets. Environmental regulations restricting production and disposal of traditional, expanded and extruded polystyrene foam increase manufacturing compliance costs, limiting market expansion in environmentally-conscious regions.

Opportunities - Aerogel Technology Advancement and High-Performance Insulation Solutions Present Opportunities

Advanced aerogel insulation technology represents an exceptional market opportunity, delivering superior thermal performance with reduced thickness and weight. Aerogel-based insulation with thermal conductivity 5-10 times that of traditional foams, enabling compact designs and lightweight applications across aerospace, electronics, and specialty industrial sectors. Armacell's September 2024 launch of cutting-edge aerogel technology and expanded ArmaGel portfolio demonstrates the leading manufacturer's commitment to advanced material development.

Vacuum-insulated panels (VIPs) provide ultra-low thermal conductivity, enabling slim-line refrigeration equipment designs that support space-efficient cold storage and specialty applications. Multilayer insulation (MLI) systems combining aerogels with reflective coatings achieve exceptional performance in cryogenic and aerospace applications, justifying premium pricing. Aerogel adoption is expanding across pharmaceutical, medical gas storage, and electronics cooling applications, creating specialized market segments with limited competition and premium margin opportunities supporting accelerated innovation investment.

Eco-Friendly and Bio-Based Insulation Material Development Creates Future Growth Opportunities

Sustainable and bio-based insulation material development creates a substantial market opportunity, addressing environmental regulations and corporate sustainability commitments. Low-GWP (Global Warming Potential) blowing agents replacing traditional hydrofluorocarbon (HFC) formulations align with regulatory requirements and customer sustainability preferences. Bio-based polyurethane foams derived from renewable resources, including soy and corn oil, offer equivalent performance to petroleum-derived alternatives with reduced environmental impact. BASF and Shandong Wiskind Architectural Steel's partnership is launching eco-friendly polyurethane sandwich panels for cold chain applications, reflecting the manufacturer's commitment to sustainable solutions.

Recycled polyurethane polyol development enables a circular economy model, reducing waste and resource consumption, supporting regulatory compliance and environmental certifications. BASF and RAMPF Eco Solutions' partnership, developing depolymerization techniques for recycled refrigeration insulation, demonstrates technological advancement in sustainable material recovery. Premium pricing support for certified sustainable and recyclable solutions justifies investment, supporting competitive differentiation and margin expansion.

Category-wise Insights

Material Type Analysis

Polyurethane Foam dominates the cold insulation materials market, commanding approximately 42% market share, driven by superior thermal conductivity, exceptional moisture resistance, and versatile application capabilities. Polyurethane foam characteristics, including its lightweight nature, rigid panel-forming capability, and spray foam applicability, support diverse industrial requirements and installation methodologies. Integration with eco-friendly low-GWP blowing agents enables environmental compliance while maintaining superior thermal efficiency. Long-term performance preservation under varied temperature conditions and extended operational cycles justifies widespread adoption among quality-focused manufacturers prioritizing reliability and cost-effectiveness, supporting market leadership through the forecast period.

Application Analysis

HVAC systems represent the leading application segment in the global cold insulation materials market, accounting for approximately 34% of total consumption. This dominance stems from the extensive use of cold insulation materials in heating, ventilation, and air conditioning (HVAC) systems to minimize energy losses, prevent condensation, and maintain temperature efficiency across residential, commercial, and industrial buildings. Effective thermal insulation in HVAC ducts, chilled water pipes, and refrigeration lines ensures optimal system performance while reducing operational energy costs and greenhouse gas emissions.

The increasing global emphasis on energy-efficient building infrastructure and the adoption of green building standards such as LEED and BREEAM have significantly boosted demand for advanced insulation materials, including polyurethane (PU) foam, polyisocyanurate (PIR), expanded polystyrene (EPS), and elastomeric foams. Rising urbanization, coupled with the growing construction of commercial spaces, hospitals, and data centers requiring controlled indoor environments, further supports market expansion.

Industry Analysis

The oil & gas industry is expected to remain the leading end-use segment, accounting for approximately 32% of the total market share. The extensive use of cold insulation materials in LNG processing, cryogenic storage, gas separation units, and pipeline systems drives this dominance. Effective insulation is critical in these applications to minimize energy loss, prevent condensation, and maintain product stability at extremely low temperatures. The sector’s growth is further supported by rising global demand for liquefied natural gas (LNG), the expansion of offshore gas projects, and increasing investments in cryogenic infrastructure across the Middle East, the U.S., and Asia-Pacific.

Regional Insights

North America Cold Insulation Materials Trends

North America maintains a significant market position with a 3.7% CAGR through established industrial infrastructure, stringent energy efficiency codes, and advanced refrigeration technology adoption. DOE and EPA regulatory standards are driving the adoption of energy-efficient insulation solutions across HVAC systems and refrigeration equipment. The expansion of a cold storage facility supporting food processing, pharmaceutical manufacturing, and e-commerce logistics creates consistent multi-year material procurement requirements.

North American manufacturers, including Owens Corning and Johns Manville, lead the market through innovation and comprehensive product portfolios. Green building certifications and energy efficiency tax credits are incentivizing advanced insulation adoption across commercial and industrial projects. Regulatory emphasis on low-VOC and sustainable materials supporting premium formulation development and market differentiation. Industrial retrofitting programs and modernization initiatives drive demand for advanced cold insulation solutions, supporting sustained regional market expansion.

Europe Cold Insulation Materials Trends

Europe exhibits mature market characteristics, accounting for approximately 26.1% of the global cold insulation materials market share, driven by its stringent environmental regulations and strong commitment to sustainability. The region’s market growth is primarily shaped by the European Union’s energy efficiency and emissions management directives, which promote the adoption of eco-friendly and high-performance insulation materials across industrial and building applications.

Regulations such as the EU Energy Performance of Buildings Directive (EPBD) and the Green Deal objectives are compelling industries to reduce energy consumption and transition toward low-carbon construction materials. This has accelerated the demand for polyurethane (PU), polyisocyanurate (PIR), and elastomeric foams that offer superior insulation performance, durability, and compliance with environmental standards.

Asia Pacific Cold Insulation Materials Trends

Asia Pacific dominates the global market with 38% market share, driven by rapid industrialization, cold chain expansion, and manufacturing growth. China is consuming substantial volumes of cold insulation material at a 5.9% CAGR, supporting urbanization projects and industrial facility expansion. China's LNG infrastructure development and cryogenic equipment manufacturing are creating exceptional demand for specialized insulation solutions. India's cold insulation market is growing at a 5.5% CAGR, driven by infrastructure development and government support for refrigerated warehousing under food safety initiatives.

Rapid cold chain logistics expansion supporting food export, pharmaceutical distribution, and e-commerce growth across the Asia Pacific. Regional manufacturers are establishing localized production capacity, reducing import dependency while capturing growing market opportunities. Government infrastructure investment, including refrigerated storage facilities and the development of the cold chain network, creates multi-year visibility into material procurement. Energy-efficiency awareness and a sustainability focus are accelerating the adoption of advanced insulation materials, supporting continued regional market expansion that exceeds global average growth rates through 2032.

Competitive Landscape

The cold insulation materials market exhibits moderate consolidation with leading manufacturers BASF SE, Armacell International, The Dow Chemical Company, and Kingspan Group PLC collectively commanding approximately 35-40% market share through comprehensive product portfolios, established distribution networks, and technological expertise. Tier-two participants including Huntsman International, Owens Corning, Evonik Industries, and CertainTeed capture significant market segments through specialized solutions and regional market focus.

Strategic capacity expansion and R&D investment demonstrate growth commitment. Companies emphasize R&D investment, sustainable formulation development, advanced aerogel technology, and customized industrial solutions, driving competitive differentiation. Regional specialists capitalize on localized requirements and supply chain advantages supporting diverse market coverage.

Key Market Developments:

- In September 2024, Armacell announces the launch of cutting-edge aerogel technology and expanded ArmaGel portfolio significantly enhancing cold insulation performance and market competitive positioning.

- In March 2024, BASF and Shandong Wiskind Architectural Steel strengthen partnership launching eco-friendly polyurethane sandwich panels designed specifically for cold chain logistics and refrigeration applications.

- In October 2022, BASF partners with RAMPF Eco Solutions developing depolymerization techniques producing polyol from waste polyurethane refrigeration insulation, supporting circular economy initiatives.

Companies Covered in Cold Insulation Materials Market

- BASF SE

- Huntsman International LLC

- Armacell International S.A.

- CertainTeed Corporation

- Arabian Fiberglass Insulation Co., Ltd

- Evonik Industries AG

- The Dow Chemical Company

- Fletcher Insulation Group

- Kingspan Group PLC

- Johns Manville Corporation

- Knauf Insulation Inc.

- Owens Corning

- Saint-Gobain

- Rockwool International

- Aspen Aerogels Inc.

Frequently Asked Questions

The global cold insulation materials market was valued at US$ 8.2 billion in 2025 and is projected to reach US$ 12.7 billion by 2032, representing a CAGR of 6.4% during the forecast period.

Primary demand drivers include accelerating LNG production projected to exceed 500 million tonnes annually by 2030, refrigerated warehouse capacity expansion, cold chain logistics growth supporting food and pharmaceutical sectors, energy efficiency regulations, and cryogenic equipment adoption across industrial applications.

Polyurethane Foam commands the dominant segment at approximately 42% market share, driven by superior thermal conductivity, exceptional moisture resistance, versatile application capabilities, and widespread adoption across HVAC, refrigeration, and cryogenic systems globally.

Asia Pacific dominates with 38% global market share, driven by rapid industrialization, cold chain logistics expansion, manufacturing growth, LNG infrastructure development, and government infrastructure investment supporting sustained regional market expansion.

LNG infrastructure expansion and cryogenic equipment manufacturing targeting 500 million tonnes annual LNG production by 2030 represents the highest-growth opportunity, requiring specialized cold insulation solutions for storage, transport, and operational safety.

Market leaders include BASF SE (Germany) with comprehensive polyurethane and phenolic foam portfolio, Armacell International S.A. (Germany) specializing in advanced aerogel technology, and Kingspan Group PLC (Ireland) leveraging cold storage expertise, collectively representing approximately 35-40% market concentration.