- Food Packaging

- Cold Chain Packaging Materials Market

Cold Chain Packaging Materials Market Trends, Size, Share, and Growth Forecast, 2025 - 2032

Cold Chain Packaging Materials Market By Material Type (Expanded Polystyrene (EPS), Polyurethane Rigid Foam (PUR), Paper & Paperboard and Others), End -user (Food, Pharmaceutical and Industrial), Product Type, and Regional Analysis for 2025 - 2032

Cold Chain Packaging Materials Market Size and Trends Analysis

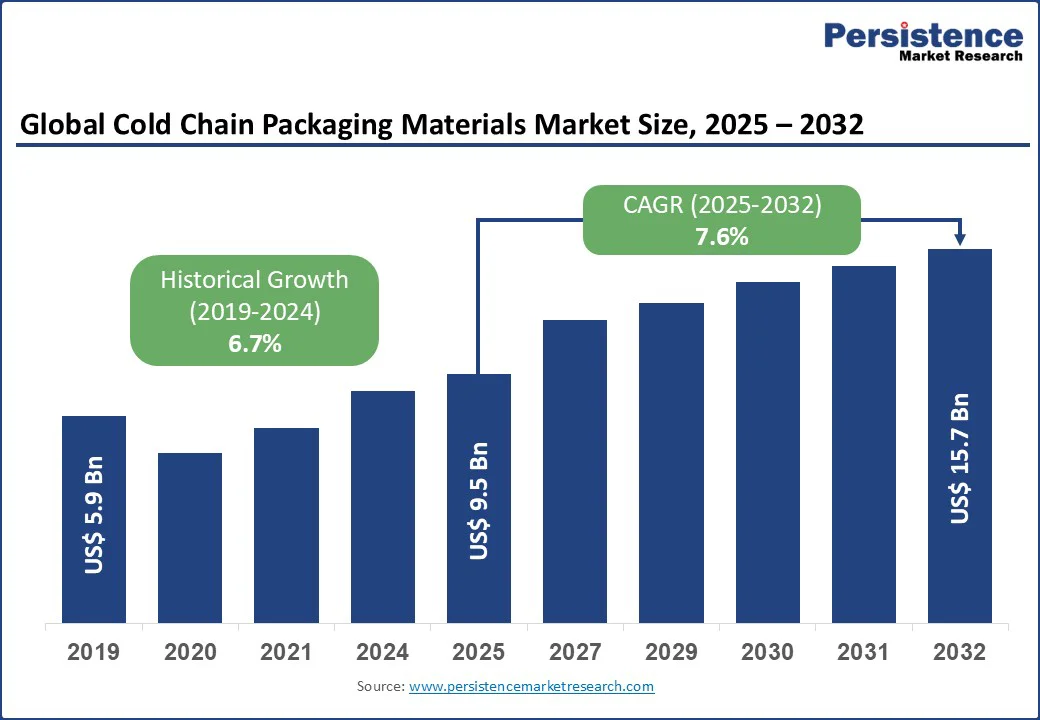

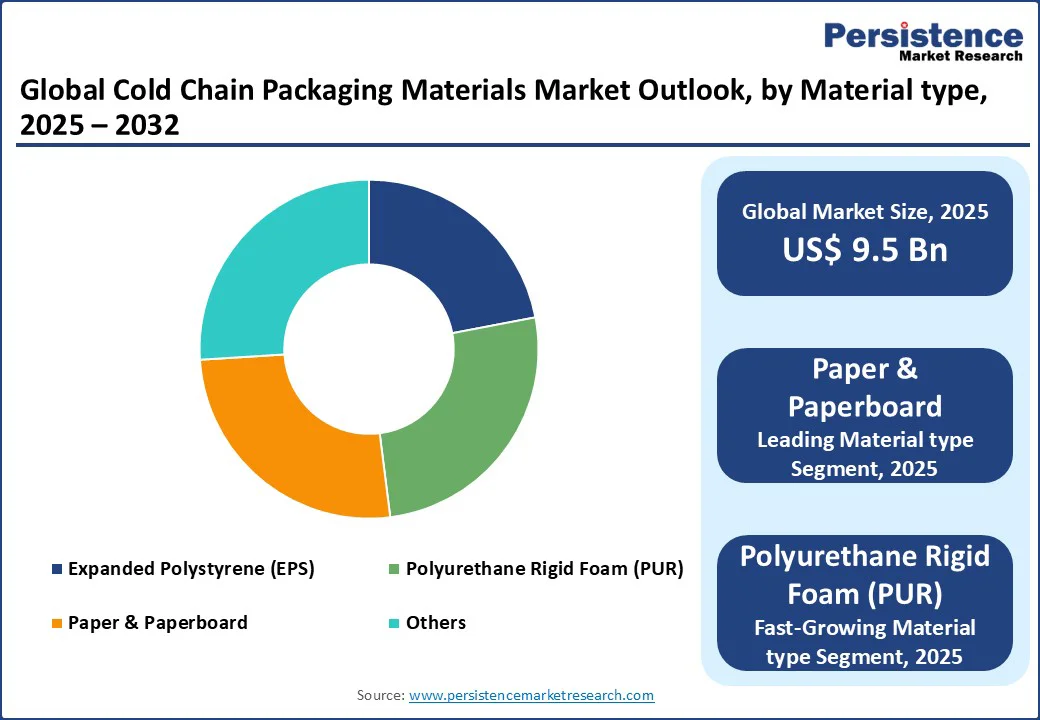

The global cold chain packaging materials market size is likely to value at US$ 9.5 Bn in 2025 and is projected to reach US$ 15.7 Bn by 2032 growing at a CAGR of 7.6% during the forecast period from 2025 to 2032 due to the rising pharmaceutical demand, the frozen food industry, and sustainability efforts. Key players focus on eco-friendly innovations and real-time monitoring with emerging markets offering significant growth potential.

Key Industry Highlights:

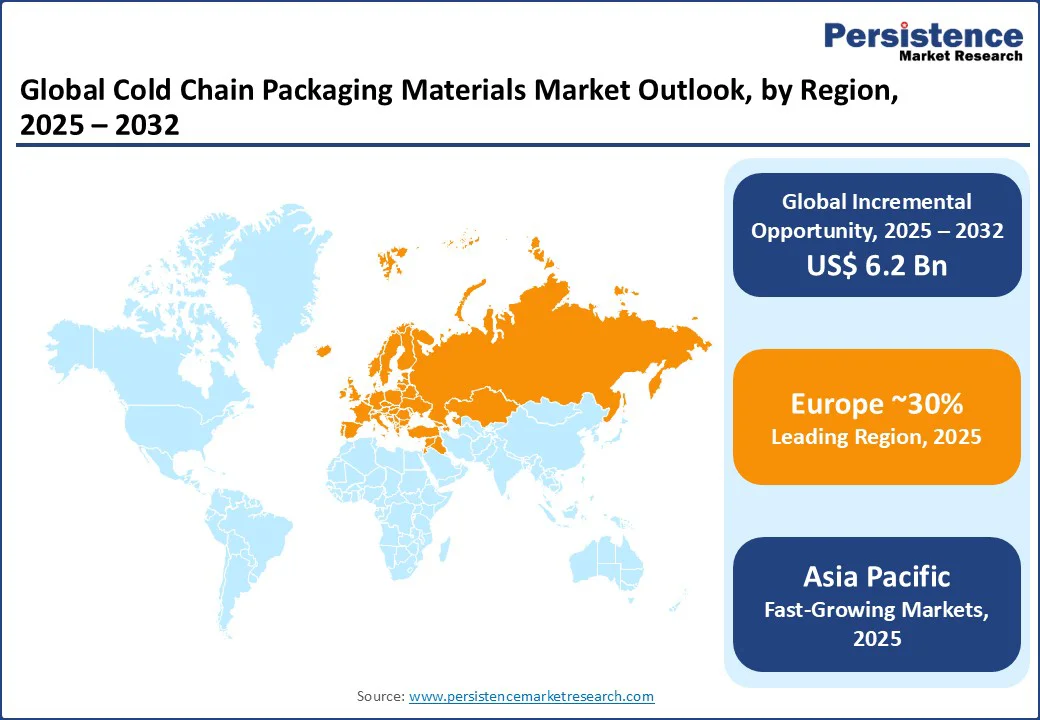

- Leading Region: Europe, accounting for over 30% revenue share in 2025, driven by strong pharmaceutical production, stringent regulatory compliance, advanced food logistics, and rising demand for sustainable cold chain packaging solutions.

- Fastest-growing Region: Asia Pacific, projected CAGR of 7.2% from 2025 to 2032, is fueled by rapid pharmaceutical expansion, booming e-commerce grocery delivery, rising demand for perishable foods, and growing investments in advanced cold chain infrastructure.

- Dominant Product Type: Paper & paperboard will account for 42% of the market share in 2025, driven by their cost-effectiveness, recyclability, sustainability, and increasing preference for eco-friendly cold chain packaging solutions across industries.

- Material Type: Insulated containers dominated the market in 2025 and accounted for a share of 40.4%. Insulated containers are typically robust and durable, providing excellent protection against physical damage during transit.

- Country Dominance: The U.S. dominates the Cold Chain Packaging Materials market in 2025, supported by its strong pharmaceutical sector, advanced logistics infrastructure, high perishable food demand, and stringent regulatory compliance for temperature-sensitive product safety.

- Import-Export Scenario: The Cold Chain Packaging Materials market’s import-export scenario is driven by pharmaceutical and perishable food trade, with developed nations exporting advanced solutions, while emerging economies increasingly import to support expanding cold chain infrastructure.

| Key Insights | Details |

|---|---|

| Cold Chain Packaging Materials Market Size (2025E) | US$ 9.5 Bn |

| Market Value Forecast (2032F) | US$ 15.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.7% |

Market Dynamics

Growth Driver - Rising Demand for Temperature-Sensitive Pharmaceuticals Remains

One of the key growth drivers for the cold chain packaging materials market is the increasing demand for temperature-sensitive pharmaceuticals, particularly biologics, vaccines, and specialty drugs. Biologics, including vaccines, gene therapies, and monoclonal antibodies, require stringent temperature control from production to patient delivery to maintain efficacy.

In November 2023, Cryopak introduced Eco Gel, manufactured from a patented blend of natural, biodegradable components. This gel is designed for optimal performance in diverse weather conditions and is resilient to withstand repeated use and maintain consistent temperature control. Eco Gel is recyclable and biodegradable; it has a lower environmental impact than traditional refrigerant gels used in gel packs, demonstrating more sustainability.

The COVID-19 pandemic underscored the need for efficient cold chain logistics, with massive vaccine distribution efforts highlighting gaps in the supply chain. As the pharmaceutical industry continues to shift toward personalized medicine and biologics, the need for reliable and innovative cold-chain packaging materials has surged. This trend is expected to continue as pharmaceutical companies develop complex drugs that require specialized storage and transportation, driving significant market growth.

Restraint - High Costs of Advanced Cold Chain Packaging Solutions

One of the primary restraints for the cold chain packaging materials market is the high cost associated with advanced packaging solutions. Technologies such as phase-change materials (PCMs), vacuum-insulated panels (VIPs), and reusable packaging systems offer superior temperature control. Still, they are significantly expensive than traditional materials like expanded polystyrene (EPS).

Adopting high-end solutions can be prohibitive for small and medium-sized companies, especially in developing markets, limiting their ability to invest in advanced packaging options. The initial investment required for reusable packaging systems, despite long-term savings, is often a barrier for companies with limited capital.

The cost challenge is compounded by rising raw material prices, impacting profit margins for businesses operating in competitive sectors like food and pharmaceuticals. As a result, the high cost of cold chain packaging materials can deter widespread adoption, especially in price-sensitive regions.

Opportunities - Sustainable and Eco-Friendly Packaging Solutions

One of the most transformative opportunities in the cold chain packaging materials market lies in developing and adopting sustainable and eco-friendly packaging solutions. With increasing global awareness around environmental conservation, there is a growing demand for packaging materials that are biodegradable, recyclable, or reusable.

Companies that can innovate in this space, offering materials such as plant-based insulators, recycled plastics, or reusable phase-change materials (PCMs) stand to capture significant market share.

Eco-conscious consumers influence this shift with businesses increasingly prioritizing sustainability in their operations. This presents an opportunity for packaging manufacturers to differentiate themselves by developing solutions that reduce carbon footprints while maintaining high performance in temperature control.

Category-wise Analysis

Material Type Insights - Paper and Paperboard Leads Material Type

The paper and paperboard category is expected to experience a significant share in the global market. The expansion of this segment is ascribed to the characteristics of paper and paperboards, including their lightweight nature, robustness, and biodegradability.

Paperboard is utilized to manufacture multi-layered cold-chain containers such as pallet shippers. The enforcement of strict environmental restrictions and the growing preference for sustainable packaging solutions will result in segmental expansion.

The polyurethane sector has witnessed significant growth in the cold chain packaging market, primarily due to the rising demand from producers of cold chain containers. This material, known for its high reusability and recyclability, has a minimal environmental impact, making it a preferred choice. The eco-friendly attributes of PUR are driving its integration into the cold chain packaging sector.

End-user Insights - Food Sector Dominates, While Pharmaceutical Sector Leads Future Growth

The food sector is estimated to account for 65% share in 2025. The substantial quantity of food carried globally is the primary element propelling the market expansion. Frozen meat, exotic fruits, pulp, beverages, dairy goods, agricultural produce, and other items are globally shipped via cold chain packaging. Moreover, the rise in international and domestic trade activities worldwide enhances segment expansion.

The pharmaceutical sector is expected to demonstrate a high growth rate during the projection period, largely due to technological advancements. These improvements are facilitating the transportation of temperature-sensitive pharmaceutical items using cold-chain packaging. The increasing number of organ transplantation procedures and the rising prevalence of hormone therapy will also contribute to the sector's expansion.

Regional Insights and Trends

Europe Leads in the Cold Chain Packaging Materials Market Trends

The cold chain packaging market in Europe is driven by growing developments in the cold chain logistics market. According to A.P. Moller-Maersk, the cold chain industry in Europe is facing challenges such as proper handling (63%), product packaging (31%), and adequate storage (31%).

These prevailing issues have attracted investments targeted toward the development of cold chain infrastructure in Europe, which can positively influence market growth. For instance, in May 2023, UK’s one of the UK's leading cold storage providers, Cold Chain Federation Magnavale, announced to invest USD 161.3 million (GBP 130 million) to construct a 101,000-pallet cold store.

Germany cold chain packaging market accounted for the largest share of 17.87% in 2025. High share can be attributed to growing dairy production in Germany. According to Statistics’ Bundesamt (Destatis), Germany is largest milk producer in Europe. Storage of milk and other dairy products is sensitive.

In general, dairy products contain microorganisms that make long-term use of these products almost impossible without proper storage and temperature conditions. Hence these products require continuous and excellent protection to prevent any degradation of product quality, thus increasing demand for cold chain packaging.

North America’s Cold Chain Packaging Materials Market Trends

North America dominated the global cold chain packaging market and accounted for the largest revenue share of 33.10% in 2025. North America, particularly the U.S., has a highly developed healthcare and pharmaceutical industry.

According to the European Federation of Pharmaceutical Industries and Associations (EFPIA) 2023 report, North America accounted for 52.3% of world pharmaceutical sales, thus presenting a positive market drive for cold chain packaging from the pharmaceutical end-use segment.

The cold chain packaging market in the U.S. held the largest share in the North America region. According to NOAA Fisheries, the U.S. harvests seafood of USD 6.3 billion dockside value annually. In August 2023, the National Seafood Strategy was released by the NOAA Fisheries.

Under this strategy, NOAA Fisheries will partner with Interstate Commissions, Regional Fisheries Management Councils, National Sea Grant College Program, seafood farmers, harvesters, non-government organizations, and other partners or stakeholders to address challenges faced by the seafood sector, especially when resources are limited.

Such initiatives aimed at boosting the domestic seafood industry can drive demand for cold chain packaging solutions for seafood packaging.

Asia Pacific is the Fastest-Growing Cold Chain Packaging Market

The cold chain packaging market in the Asia Pacific is projected to grow with the fastest CAGR owing to growing pharmaceutical production in the region. According to the United Nations ESCAP, Asia-Pacific accounts for the largest share of global research and development spending and large shares in patents and publications on vaccine research and development.

Countries in the Asia Pacific have incentivized investments in vaccine research and development, thus driving global pharmaceutical firms to not only offshore part of their production but also transfer some of their research and development activities to the region.

For instance, in September 2023, Bio Farma and Coalition for Epidemic Preparedness Innovations (CEPI) entered into a 10-year agreement to manufacture vaccines to tackle future outbreaks and pandemics, which can drive demand for cold chain packaging products.

China cold chain packaging market held a significant share in 2025. China’s growing population has escalated demand for fresh produce and temperature-sensitive products. For instance, the health benefits of blueberries have resulted in the growing demand for blueberries as a viable option among Chinese consumers.

Even U.S.-based Driscoll has estimated that the volume of blueberries harvested in China can grow significantly in the coming years, which can drive demand for cold chain packaging in China.

Competitive Landscape

The global cold chain packaging materials market is highly competitive with several key players vying for market share through innovation and sustainability. Leading companies like Sonoco ThermoSafe, Cold Chain Technologies, and Pelican BioThermal dominate the space, offering advanced temperature-controlled packaging solutions for pharmaceuticals, food, and biotechnology.

Market players focus on sustainable packaging innovations such as reusable materials and eco-friendly insulation to meet rising environmental standards. Small and regional companies also compete by offering cost-effective and customized solutions for emerging markets.

Strategic mergers, acquisitions, and partnerships are common as companies aim to expand their global reach and product portfolios. Increasing demand for real-time monitoring and smart packaging further intensifies competition, driving technological advancements in the market.

Key Industry Developments

- In March 2023, Ranpak launched the RecyCold climaliner solution, a thermal liner constructed from paper for cold chain packaging. RecyCold climaliner maintains products at their optimal temperature range for up to 48 hours while promoting sustainability and recyclability.

- In October 2023, Cold Chain Technologies purchased Exeltainer, a global producer of thermal packaging solutions for life sciences with manufacturing operations in Brazil and Spain. This acquisition will enable Cold Chain Technologies to enhance its sustainable cold chain packaging product offerings.

Companies Covered in Cold Chain Packaging Materials Market

- Cold chain Technologies

- Cryopak

- Sonoco Thermosafe

- SOFRIGAM

- Softbox Systems Ltd

- Pelican Products, Inc.

- CSafe

- TOWER Cold Chain Solutions

- Sealed Air Corporation

- CoolPac

- Nordic Cold Chain Solutions

- Global Cooling Inc.

- Other Market Players

Frequently Asked Questions

The Cold Chain Packaging Materials market is estimated to be valued at US$ 9.5 Bn in 2025.

The key demand driver for the Cold Chain Packaging Materials market is the surging need to preserve and safely transport temperature-sensitive products, particularly in the pharmaceutical (e.g., biologics, vaccines), food, and biotechnology sectors.

In 2025, the Europe region will dominate the market with an exceeding 30% revenue share in the global Cold Chain Packaging Materials market.

Among the Material, paper & paperboard hold the highest preference, capturing beyond 42% of the market revenue share in 2025, surpassing other Material.

The key players in the Cold Chain Packaging Materials market are Cold chain Technologies, Cryopak, Sonoco Thermosafe, SOFRIGAM and Softbox Systems Ltd.