- Plastics, Polymers & Resins

- Electric Motor Insulation Material Market

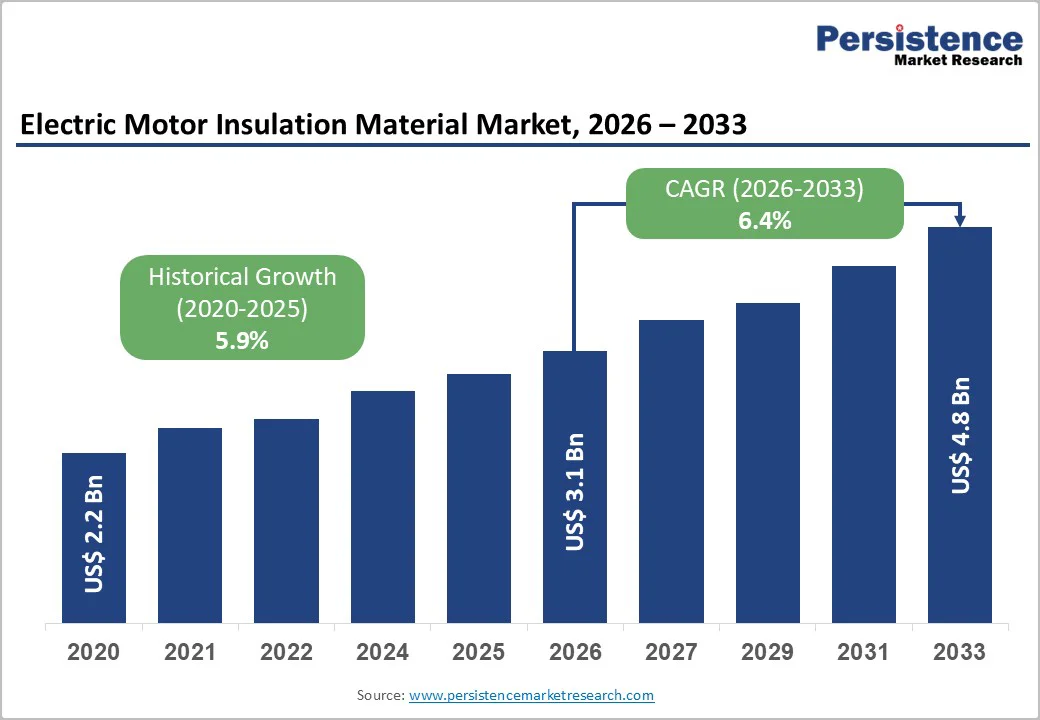

Electric Motor Insulation Material Market Size, Share, and Growth Forecast, 2026 – 2033

Electric Motor Insulation Material Market by Material (Thermoset Insulation, Thermoplastic Insulation, Ceramic Insulation, Paper & Films, Others), Insulation Type (Slot Insulation, Phase Insulation, Wedge Insulation, Others), End-User (Automotive, Industrial Machinery, Aerospace, Consumer Electronics, Energy & Power Generation, Others), and Regional Analysis for 2026-2033

Electric Motor Insulation Material Market Share and Trends Analysis

The global electric motor insulation material market size is likely to be valued at US$ 3.1 billion in 2026 and is estimated to reach US$ 4.8 billion by 2033, growing at a CAGR of 6.4% during the forecast period 2026−2033. Accelerating electrification across automotive, industrial, and energy infrastructure, coupled with rising deployment of high-efficiency electric motors that demand superior insulation performance is aiding market growth. Expanding regulatory mandates requiring thermal durability and energy performance compliance are broadening addressable market opportunities, while widespread adoption of electric vehicles (EVs) and modernization of power generation systems create sustained demand for reliable, durable insulation solutions that can withstand demanding operational environments. Technological advancement is reshaping competitive dynamics and unlocking new growth pathways. Breakthroughs in thermoset and thermoplastic insulation formulations are enabling manufacturers to design lighter, more efficient motor systems while maintaining thermal stability and mechanical resilience across extended service lifecycles. Energy transition policies and stringent international safety standards are reinforcing specification requirements and creating barriers that favor suppliers with proven technical capabilities and regulatory certifications.

Key Industry Highlights

- Dominant Region: Asia Pacific is expected to lead market in 2026 with around 45% share, driven by strong automotive production and rapid growth in renewable energy projects.

- Fastest-growing Market: Asia Pacific is projected to emerge as the fastest-advancing market between 2026 and 2033, propelled by surging use of high-performance insulation across EV platforms.

- Leading Material: Thermoset insulation is set to command a projected 40% share in 2026, owing to its ability to deliver unwavering thermal and mechanical stability across EV, industrial, and grid systems.

- Fastest-growing Material: Thermoplastic insulation is expected to record the fastest growth between 2026 and 2033, supported by the rising demand for lightweight, recyclable materials that enhance production efficiency.

| Key Insights | Details |

|---|---|

| Electric Motor Insulation Material Market Size (2026E) | US$ 3.1 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Automation and Energy Efficiency Mandates

Industrial automation drives sustained demand for advanced insulation materials as automated systems rely on high-performance electric motors that operate under elevated thermal and mechanical stress. Rising adoption of robotic cells, automated conveyors, and digitally controlled machinery requires motors with greater operational reliability. High-grade insulation enhances winding protection, limits dielectric breakdown, and supports prolonged duty cycles in variable-speed environments. This performance expectation strengthens the preference for premium insulation solutions in automated production settings.

Energy-efficiency mandates reinforce this momentum by pushing industries toward motors that meet stringent efficiency classes such as IE3 and IE4 (International Efficiency Standards). These advanced motors demand insulation materials with superior thermal endurance, partial discharge resistance, and mechanical strength to maintain efficiency levels over extended operational life. Regulatory focus on reduced energy consumption across manufacturing, utilities, and infrastructure stimulates investment in upgraded motor systems that depend on next-generation insulating components. This alignment of compliance pressures with operational optimization elevates the strategic priority of advanced insulation materials within modernization programs across industrial facilities.

Raw Material Cost Volatility

Raw material price fluctuations create persistent uncertainty for manufacturers that depend on stable input costs to plan production schedules and maintain predictable margins. Insulation materials require polymers, resins, glass fibers, mica, specialty chemicals and engineered composites, all of which experience frequent pricing shifts driven by crude oil trends, petrochemical supply cycles, global logistics disruptions and shifts in commodity demand. Sudden cost spikes force producers to revise procurement strategies, renegotiate supplier contracts and recalibrate operating budgets, which slows operational agility and compresses profitability. Volatile input pricing also alters comparative cost advantages across material types, complicating long-term planning and strategic sourcing decisions.

Unstable raw material costs influence the pricing structure of finished insulation products and weaken competitive positioning. Manufacturers face a strategic challenge: absorb higher input expenses and reduce margins or pass the burden to customers and risk demand contraction. Frequent price adjustments in the supply chain disrupt project costing for motor producers, create delays in high-volume orders and reduce confidence in vendor partnerships. Forecasting difficulties limit investment in capacity expansion and restrict innovation in advanced insulation technologies that require high-value formulations. This cost unpredictability ultimately acts as a limiting factor for consistent industry growth.

Technological Convergence in High-Temperature Applications

Technological convergence in high-temperature applications creates a strategic opportunity as modern motors integrate advanced power electronics, compact winding architectures, and higher operational loads. This integration elevates thermal stress across components, increasing the need for insulation systems that sustain stability at elevated temperatures while supporting consistent electrical performance. The shift toward high-speed designs and greater power density elevates demand for insulation materials that deliver thermal endurance, dielectric integrity, and mechanical resilience under continuous stress.

New-age mobility solutions, electrified industrial equipment, aerospace propulsion systems, and renewable-energy machinery all transition toward higher temperature thresholds to unlock greater efficiency. This transition amplifies the requirement for specialized insulation grades engineered for thermal class upgrades, extended lifetime performance, and compatibility with digitally controlled motor platforms. Suppliers that innovate around such cross-technology requirements gain a pathway to premium product portfolios, long-term customer contracts, and competitive differentiation in an environment where advanced thermal capabilities become a core performance parameter.

Category-wise Analysis

Material Insights

Thermoset insulation is likely to be the leading segment with a projected 40% of revenue share in 2026, due to stable thermal performance and strong resistance to mechanical stress of the material. These materials support demanding operating cycles in EV traction motors, grid transformers, and high-load industrial drives. Epoxy-based systems maintain dimensional stability under vibration, moisture, and thermal shock, making them preferred for long-duty applications. An example is their use in high-speed traction motors, where thermoset laminates prevent dielectric breakdown during continuous acceleration cycles.

Thermoplastic insulation is expected to witness the fastest growth between 2026 and 2033, as increasing demand for lightweight and circular-material solutions drives higher adoption across electronics, appliances, and automation equipment. Recyclability and lower processing requirements streamline production workflows, creating a favourable shift for mid-volume industrial machinery. Applications such as modular household appliances and compact servo motors benefit from thermoplastic films that deliver flexible formability and consistent electrical stability. As industries focus on material efficiency and modern manufacturing practices, thermoplastics gain momentum through scalable design integration, improved thermal classes, and compatibility with automated insulation placement systems.

Insulation Type Insights

Slot insulation is poised to lead with a forecasted 40% share in 2026, owing to its critical role in preventing short circuits within motor windings. It ensures operational safety and reliability, particularly in high-voltage environments such as EV stators, industrial drives, and renewable-energy generators. Slot insulation maintains consistent dielectric strength under thermal and mechanical stress. For example, in electric vehicle stators, proper slot insulation safeguards winding integrity during rapid acceleration and regenerative braking, supporting long-term performance and compliance with original equipment manufacturer (OEM) safety standards.

Phase insulation is anticipated to be the fastest-growing segment between 2026 and 2033, fueled by the massive demand for compact and lightweight motor designs in aerospace, robotics, and high-performance industrial motors. Innovations in advanced films and laminates reduce overall motor weight, enhancing energy efficiency and system responsiveness. Applications such as small-scale aerospace propulsion motors and precision servo units benefit from improved phase separation, thermal stability, and dimensional flexibility. Adoption accelerates as industries prioritize miniaturization, high-voltage safety, and integration with automated motor assembly processes.

End-User Insights

The automotive sector is slated to hold a dominant position, with an anticipated 45% of the electric motor insulation material market revenue share in 2026, driven by the meteoric growth in electric vehicle production in recent years and growing adoption of high-efficiency motors. Insulation solutions play a critical role in ensuring motor reliability under high-voltage and high-temperature conditions. For example, in passenger EV traction motors, advanced insulation systems prevent electrical faults during frequent acceleration cycles, regenerative braking, and extreme ambient temperatures, supporting long-term durability and compliance with stringent safety standards.

The energy and power generation segment is forecasted to be the fastest-growing between 2026 and 2033, boosted by rising investments in renewable energy projects, including offshore wind and solar facilities. High-performance insulation materials provide the necessary dielectric strength and thermal stability for turbines, generators, and grid-connected motors. In offshore wind platforms, these materials offer resilience against moisture, vibration, and temperature fluctuations while ensuring reliable electrical operation. Continued growth in renewable energy infrastructure, along with emphasis on durable and low-maintenance solutions, is driving widespread adoption of specialized insulation in this sector.

Regional Insights

North America Electric Motor Insulation Material Market Trends

North America is anticipated to maintain a dominant market position in 2026, driven by accelerating deployment of high-efficiency motors and automation infrastructure across industrial, aerospace, and energy sectors. Specialized insulation materials command strong demand to deliver thermal stability, mechanical strength, and dielectric reliability in mission-critical applications. The region benefits from advanced manufacturing capabilities and robust research and development (R&D) infrastructure that enables development of tailored insulation solutions for EVs, industrial motor drives, and smart manufacturing systems. This combination of technical expertise, manufacturing scale, and innovation capacity reinforces North America's strategic standing in the global insulation materials market and attracts continued investment from leading suppliers.

Widespread adoption of lightweight, durable, and high-dielectric insulation solutions aligns with broader industry objectives around system miniaturization, energy efficiency, and extended operational reliability. Concurrent expansion of renewable energy installations such as wind and solar farms creates additional demand for insulation materials engineered to withstand demanding environmental conditions, including temperature fluctuations, moisture exposure, and mechanical stress. Growing emphasis on sustainable, low-maintenance material options directly supports cost reduction across component lifecycles and enhances overall system performance, aiding the North America electric motor insulation material market growth.

Europe Electric Motor Insulation Material Market Trends

Europe is set to remain a high-value market for advanced electrical insulation, supported by rapid electrification and strict regulatory expectations. High adoption of electric vehicles EVs, rising industrial automation, and large-scale renewable energy programs are increasing requirements for materials that deliver strong dielectric strength, reliable thermal stability, and robust mechanical resilience in demanding duty cycles. Key end uses such as EV traction motors, industrial drives, and wind and solar power systems also push suppliers to prove compliance with rigorous environmental and safety rules, which raises the importance of validated performance data and traceable production. Strong regional R&D depth, combined with local manufacturing know-how, enables faster iteration of thermoset and thermoplastic insulation solutions that match European standards and operating conditions.

Government policy continues to reinforce this trajectory by prioritizing electrification, the green energy transition, and low-emission technologies across transport, industry, and power generation. As manufacturers reduce size and weight in applications such as compact industrial motors, aerospace platforms, and smart factory equipment, they increasingly specify lightweight, durable, high-performance insulation that supports efficiency targets without sacrificing long-term reliability. Renewable build-outs, especially offshore wind and expanding solar capacity, intensify demand for insulation engineered for harsh environments, including moisture, salt exposure, vibration, and temperature cycling. To compete effectively, suppliers can focus on sustainable formulations, low-maintenance performance profiles, and region-specific qualification strategies that align product roadmaps with evolving European compliance and end-market requirements.

Asia Pacific Electric Motor Insulation Material Market Trends

Asia Pacific is positioned to dominate in 2026, capturing an estimated 45% of the electric motor insulation material market share, driven by large-scale automotive manufacturing, extensive industrial motor deployment, and accelerating renewable energy infrastructure buildouts. The region functions as a global manufacturing hub for EV traction motors, industrial drives, and high-efficiency generators, creating sustained demand for advanced insulation materials that deliver superior performance across diverse operating conditions. Government policies actively promoting electrification and energy-efficient technologies strengthen this foundation, while established local supply chains enable faster time-to-market and cost advantages. Strategic investments in R&D are advancing next-generation solutions with enhanced high-temperature tolerance, improved dielectric properties, and stronger mechanical durability, positioning regional suppliers to capture both domestic and export opportunities.

Beyond its current leadership, Asia Pacific is also forecast to emerge as the fastest-growing market through 2033, propelled by the rising adoption of lightweight, high-performance insulation across electric vehicles, industrial robotics, and automated manufacturing platforms. Expanding solar capacity and offshore wind projects demand insulation systems engineered for moisture resistance, thermal stability, and long-term durability in harsh installation environments. The region's deep expertise in polymer and resin technologies, combined with production scale advantages and localized manufacturing capabilities, accelerates material qualification and commercial adoption. For suppliers targeting this market, success increasingly depends on demonstrating energy efficiency gains, extended maintenance intervals, and proven system reliability.

Competitive Landscape

The global electric motor insulation material market structure is moderately consolidated, with several players exerting significant influence through comprehensive insulation portfolios, advanced material technologies, and strong partnerships with OEMs. Leading companies maintain competitive advantages by investing in research and development, leveraging supply chains, and ensuring compliance with international standards. DuPont, 3M, Elantas, BASF SE, Toray Industries, Von Roll Holding AG, and Henkel AG & Co. KGaA are key players shaping the competitive landscape, offering a wide range of thermoset, thermoplastic, and specialty insulation solutions for high-performance motors and industrial applications.

New and emerging companies are focusing on specialized materials, including ceramic composites and high-frequency insulation systems, to capture targeted segments. Intense competition exists in high-temperature insulation and EV-grade materials, with differentiation driven by durability, thermal performance, and cost efficiency. Manufacturers continuously innovate to meet evolving requirements across electric vehicles, industrial motors, and renewable energy installations, ensuring long-term reliability and enhanced system efficiency.

Key Industry Developments

- In November 2025, CWIEME Berlin launched the Electric Motor Forum to unite manufacturers and suppliers, focusing on motor components, insulation materials, and winding technologies to foster innovation and collaboration.

- In September 2025, Yutong conducted rigorous high?speed and extreme temperature tests on its electric buses to validate battery safety systems, including multi?layer protection and nitrogen injection to prevent thermal runaway, reinforcing confidence in EV bus reliability under harsh conditions.

- In June 2025, Mavel Powertrain adopted Syensqo’s advanced materials to enhance EV motor efficiency and thermal performance, supporting higher-voltage designs and better heat management.

Frequently Asked Questions

The global electric motor insulation material market is projected to reach US$ 3.1 billion in 2026.

Unprecedented expansion of electric vehicle production, industrial automation, renewable energy growth, and the increasing need for high-efficiency, high-reliability motor insulation solutions are driving the market.

The market is poised to witness a CAGR of 6.4% from 2026 to 2033.

Rising demand for EV-grade insulation, growth in renewable energy systems, advancements in high-temperature materials, and increased adoption of automation-ready motor insulation solutions are key market opportunities.

DuPont, 3M, Elantas, BASF SE, Toray Industries, Hitachi Chemical, Von Roll Holding AG, Henkel AG & Co. KGaA, and Nitto Denko Corporation are some of the key players in the market.