- Testing, Inspection, & Certification

- IoT Managed Services Market

IoT Managed Services Market Size, Share, and Growth Forecast, 2026 - 2033

IoT Managed Services Market by Product Type (Security Management, Network Management, Infrastructure Management, Device Management, Data Management, Misc.), Application (Manufacturing, Transportation & Logistics, Energy & Utilities, Healthcare, IT & Telecom, Retail & Consumer Goods, BFSI (Banking, Financial Services & Insurance), and Regional Analysis for 2026 - 2033

IoT Managed Services Market Size and Trends Analysis

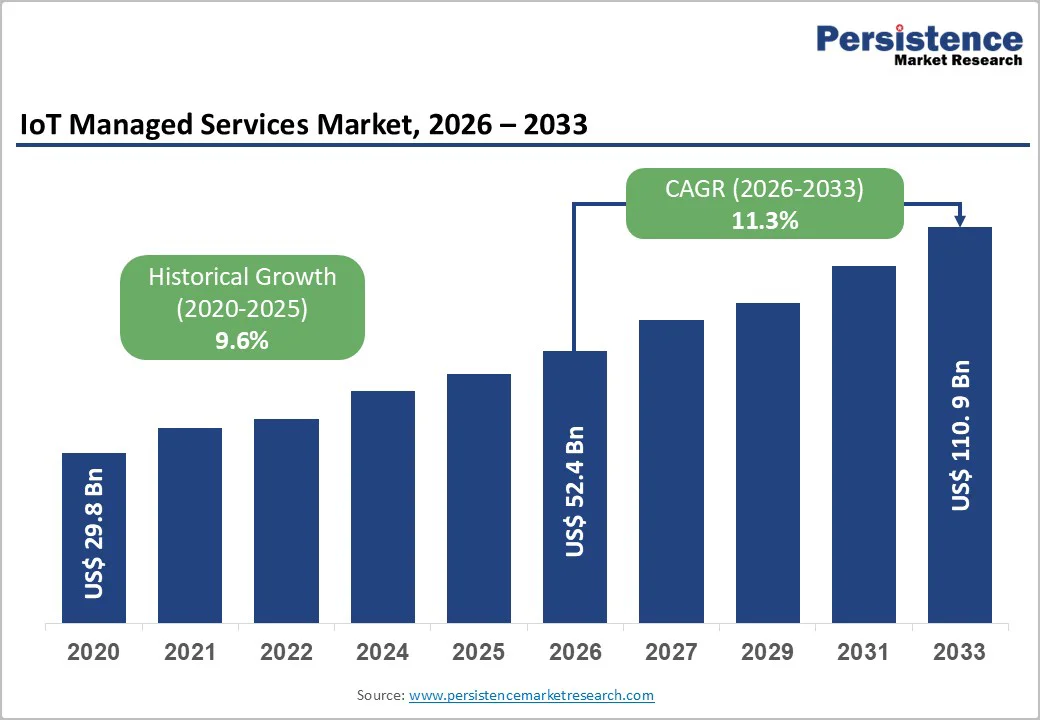

The global IoT managed services market size is likely to be valued at US$ 52.4 billion in 2026 and is projected to reach US$ 110.9 billion by 2033, growing at a CAGR of 11.3% between 2026 and 2033.

The market is currently experiencing a structural shift driven by the transition from simple connectivity to complex, value-added integration across industrial and automotive sectors.

Growth is primarily underpinned by the escalating demand for security management in enterprise environments and the rapid digitisation of manufacturing infrastructures, particularly in East Asia and Europe. While the market historically grew at a 9.6% CAGR, the acceleration to a projected 11.3% signifies the maturing of IoT ecosystems where third-party management has become essential for scalability rather than an optional luxury.

Key Industry Highlights:

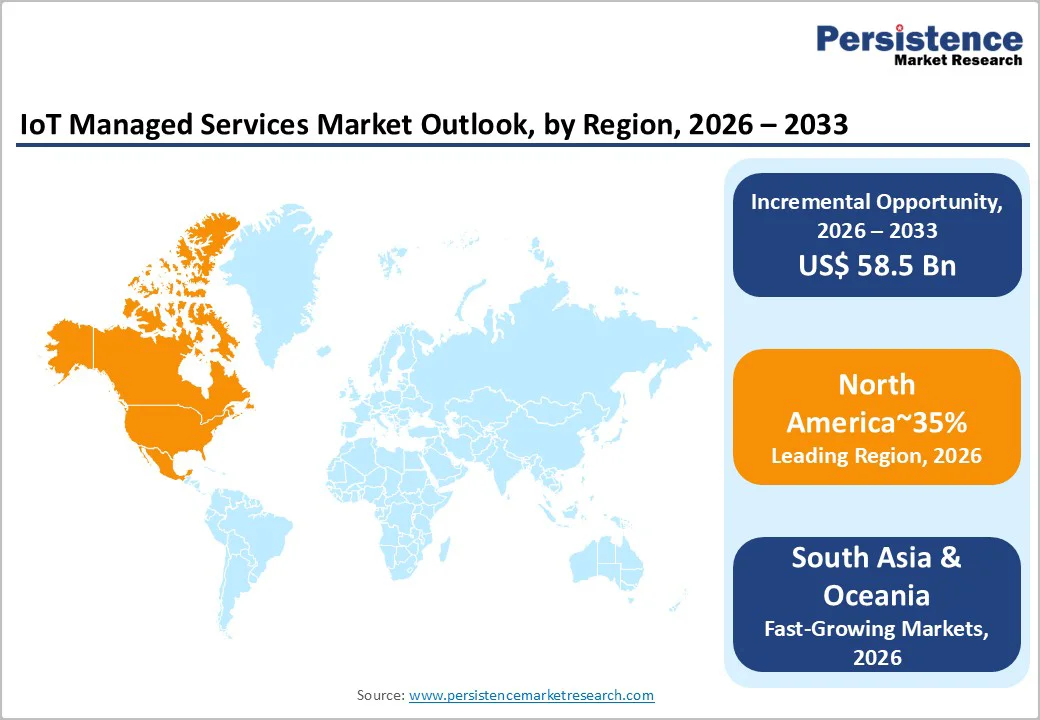

- Regional Leadership: North America leads the IoT Managed Services Market with 35% share in 2026, driven by robust automotive and transportation sectors, along with high-value asset management and rapid EV adoption.

- Fastest-Growing Region: East Asia captures 18% share in 2026, with China’s dominance in global automotive manufacturing and government spending on R&D driving the surge in IoT adoption, particularly in industrial IoT.

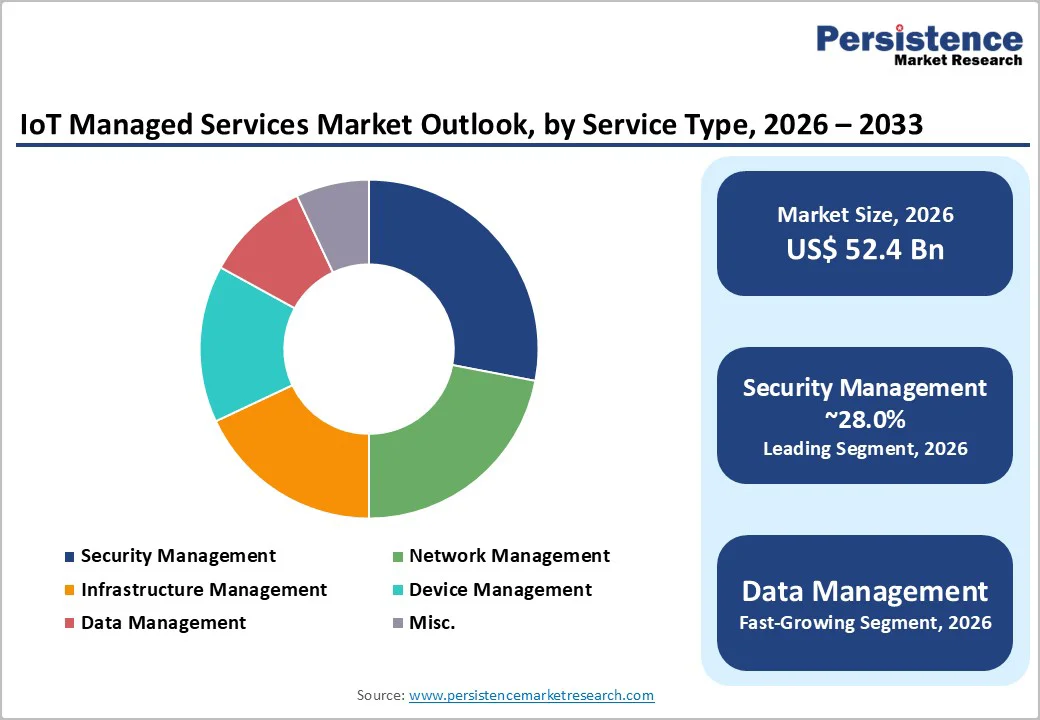

- Leading Service Segment: Security Management dominates the service type segment, accounting for 28% of the market in 2026, propelled by increasing IoT endpoints like smart locks and cameras across enterprises.

- Emerging Service Segment: Data Management is the fastest-growing segment, driven by the massive volume of data generated by IoT devices, with 36% of large EU enterprises utilising IoT for improving operational performance.

- Leading Industry: Industrial & Manufacturing holds the largest share at 25.2% in 2026, fueled by the global automotive manufacturing base, particularly in China and India, where millions of vehicles require ongoing IoT management.

- Key Development: On November 6, 2025, Arviem AG and Tech Mahindra formed a strategic partnership to develop IoT-enabled supply chain visibility solutions, combining real-time cargo monitoring with global technology capabilities to optimise supply chains.

- Expanding Opportunity in EV Infrastructure: With India expecting a US$ 206 billion EV opportunity by 2030, the demand for managed services to handle EV charging infrastructure and telematics is growing rapidly, offering lucrative entry points for global providers.

| Key Insights | Details |

|---|---|

| IoT Managed Services Market Size (2026E) | US$ 52.4 Bn |

| Market Value Forecast (2033F) | US$ 110.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.6% |

Market Dynamics

Drivers - Industrial Transformation and Automotive Production Complexity

The expansion of the IoT Managed Services Market is fundamentally linked to the sheer scale of global industrial and automotive production, which necessitates third-party management for device connectivity and data flow.

The complexity of modern manufacturing is evident in the global automotive sector, where global car sales reached 74.6 million units in 2024, with China alone contributing nearly 23 million units. As production lines become more digitised to handle this volume, manufacturers are turning to managed services to oversee the operational technology (OT) layers.

For instance, China increased its production output by 5.2%, capturing 35.4% of the global production share. This volume of manufacturing output creates a direct requirement for managed infrastructure services to ensure uptime and efficiency.

In India, the automotive sector produced over 31 million vehicles in FY25, with exports surging 19%. The management of the sensors and telematics embedded in these millions of vehicles-from the factory floor to the end-consumer-drives substantial demand for outsourced IoT management solutions.

Government-Led Smart Infrastructure and Digitalisation Initiatives

State-sponsored digital transformation projects serve as a critical catalyst for the adoption of managed services, as governments outsource the complex maintenance of smart cities grids and public utilities.

In India, the Smart City Mission, backed by an allocation of INR 7,060 crores, aims to develop 100 smart cities featuring intelligent transportation and smart parking systems. These massive public sector deployments rely on managed service providers to handle the vast networks of sensors and data endpoints that government bodies lack the internal resources to maintain.

The European Union’s digital agenda has resulted in significant enterprise adoption; Eurostat data (2021) indicates that 29% of EU enterprises used IoT devices, with adoption rates climbing to 51% in Austria and 49% in Slovenia. This government-level push creates a stable, high-volume baseline for managed service contracts, particularly in utility and energy sectors, where 46% of EU enterprises in electricity and gas supply have already integrated IoT systems.

Enterprise Imperatives for Security and Operational Efficiency

The primary operational driver for managed services is the critical need for security and energy efficiency within enterprise environments. Security Management is the leading service segment, driven by the fact that 72% of EU enterprises utilising IoT cite "securing premises" as their primary use case. As security perimeters expand beyond physical walls to include digital endpoints like smart locks and cameras, the complexity of managing these threat surfaces exceeds internal IT capabilities.

Energy management is a significant factor; 30% of EU enterprises use IoT for energy optimisation, with this figure rising to 56% among large enterprises. The data demonstrates that as organisations scale, their reliance on managed services for non-core functions like energy monitoring and condition-based maintenance (used by 44% of large EU enterprises) intensifies. This trend effectively converts IoT from a capital expenditure into an operational service model, fueling market revenue growth.

Restraint - Specialised Skills Gap and Implementation Complexity

A primary restraint hindering broader market adoption is the acute shortage of technical talent capable of managing complex IoT architectures, necessitating significant investment in training before services can be deployed.

The technical requirements are rigorous; as highlighted by the "IoT course" curriculum references, effective management requires mastery of microcontroller programming (ADC, DAC, PWM), communication protocols (SPI, I2C, UART), and full TCP/IP stack implementation.

The complexity of setting up MQTT architectures for device-to-device communication acts as a barrier for many organisations. While initiatives like India’s MeitY approving INR 436.87 crores for the "FutureSkill PRIME" initiative attempt to bridge this gap, the current lack of ready-to-deploy talent slows down the onboarding of managed services, particularly for small to medium enterprises (SMEs) that cannot afford expensive external consultants.

Opportunity - Electrification of Transport and EV Infrastructure Management

The global shift toward electric mobility presents a massive, actionable opportunity for managed service providers to oversee the charging infrastructure and telematics of millions of new electric vehicles (EVs). The U.S. market saw EV sales surge in August 2026, driven by federal subsidies of up to US$7,500, while Germany has already deployed over 106,000 charging stations and registered 1.65 million all-electric vehicles.

Each of these charging points and vehicles represents a node requiring remote monitoring, billing management, and software updates-core functions of IoT managed services.

In emerging markets like Brazil, where EV sales skyrocketed by 219.2% in 2024, and India, which anticipates a US$ 206 billion EV opportunity by 2030, the demand for platforms that can manage this new electrified grid is outpacing local supply, offering a lucrative entry point for global managed service providers.

Expansion into Edge Computing and 5G-Enabled Industrial Applications

Technological convergence between 5G and Industrial IoT opens significant avenues for services that manage data processing at the "edge" of the network rather than in the cloud.

The market is evolving toward low-latency applications; the provided text highlights the educational focus on "Edge computing" and "Wireshark-based packet analysis," indicating a maturation of the technology stack.

With Japan investing 3.9 trillion yen in R&D and focusing heavily on automotive and industrial machinery, there is a distinct opportunity for managed services that offer real-time data analytics and "condition-based maintenance" currently used by 24% of EU enterprises.

As industrial sectors move toward Industry 4.0, the fastest-growing application segment, IT & Telecom, will increasingly rely on managed services to handle the massive data throughput generated by these advanced manufacturing environments.

Category-wise Analysis

Service Type Insights

Security Management dominates the service type segment, capturing 28.0% of the market in 2026. This dominance is substantiated by usage patterns in the European Union, where 72% of all enterprises deploying IoT systems utilise them primarily for securing premises.

The ubiquity of connected endpoints-ranging from cameras to smart alarms-has created an expansive attack surface that requires constant, professional monitoring. Large enterprises, in particular, drive this segment, as they integrate security protocols across complex supply chains and physical assets.

Data Management is the fastest-growing segment, fueled by the sheer volume of telemetry generated by billions of devices. With the number of connected devices projected to have reached 30-50 billion by 2020, the challenge has shifted from connectivity to intelligence.

Organizations are increasingly contracting managed services to handle the ingestion, storage, and analytics of this data to drive decision-making, such as the 36% of large EU enterprises now using IoT specifically to streamline production processes and improve operational performance.

End User Insights

The Industrial & Manufacturing sector holds the largest market share at 25.2% in 2026. This leadership is anchored in the global automotive manufacturing base, particularly in China, which alone accounts for 35.4% of global car production.

The integration of sensors for quality control, supply chain tracking, and assembly line automation in markets like Germany, producing 4.1 million cars annually and India, over 31 million total vehicles produced in FY25, creates a massive installed base of industrial IoT assets that require managed maintenance and oversight to prevent costly downtime.

IT & Telecom is the fastest-growing application segment, driven by the deployment of 5G networks and the proliferation of data centres requiring environmental monitoring. As indicated by the learning curriculum emphasising "Wi-Fi and BLE networks" and "TCP/IP stack" implementation, the telecom sector is the backbone of IoT.

The expansion of digital infrastructure, such as the "Digital India" program and similar global initiatives, necessitates robust managed services to maintain the network integrity and uptime required for critical communications.

Regional Insights and Trends

North America IoT Managed Services Market Trends

North America holds the leading regional share at 35% of the global market. The region's growth is characterised by high-value asset management, particularly in the automotive and transportation sectors. In the U.S., the automotive market demonstrated resilience with a 3.8% sales increase in 2024, alongside a 5.1% growth in light truck sales.

This robust automotive activity, combined with the rapid adoption of electric vehicles stimulated by federal subsidies of US$7,500, generates substantial demand for fleet management and telematics services.

The region's focus on "Internet of Things" technologies is further evidenced by advanced inventory management practices; for instance, Japanese brands in the U.S. maintain lean inventories (Toyota at 22 days), a feat made possible through precise, IoT-enabled supply chain tracking. The mature regulatory environment and high adoption of cloud technologies in the U.S. favour the expansion of sophisticated managed service models over basic connectivity.

East Asia IoT Managed Services Market Trends

East Asia accounts for 18% of the market, with growth accelerating due to dominance in global manufacturing and aggressive government spending on R&D. China remains the central engine, responsible for 35.4% of global car production and serving as the EU’s top source of car imports 17.2% share. This manufacturing density requires extensive industrial IoT (IIoT) managed services to maintain efficiency.

Japan contributes significantly through innovation, with its automotive sector alone investing 3.9 trillion yen in R&D, representing 30% of the nation's manufacturing R&D spending.

Furthermore, India is emerging as a high-growth frontier; the Zinnov report estimates IoT investments grew from US$ 5 billion in 2020 to US$ 15 billion in 2021. Supported by the "Smart City Mission" and a US$ 180 billion requirement for EV manufacturing infrastructure, the region is shifting from hardware production to comprehensive service management.

Europe IoT Managed Services Market Trends

Europe captures 26% of the global market, driven by strict regulatory frameworks regarding data privacy and a strong focus on sustainability. Germany serves as the region's industrial hub, producing nearly 4.1 million passenger cars and investing €30 billion in automotive R&D.

The region's market is heavily influenced by environmental regulations; Germany’s "Electric Mobility Act" and the deployment of over 106,000 charging stations have spurred demand for managed services in energy and utility sectors.

Eurostat data highlights that adoption is highest in the "electricity, gas, steam, and air conditioning" sectors (46%), reflecting the region's priority on energy efficiency. Additionally, the EU maintains a trade surplus of €81 billion in the automotive sector, necessitating global logistics and tracking services managed through IoT platforms to secure high-value exports to markets such as the US and China.

Competitive Landscape

The global IoT services market is highly fragmented in nature, with numerous players ranging from specialised startups to large-scale multinational corporations. The market is characterised by intense competition, driven by the growing demand for IoT solutions across industries such as manufacturing, healthcare, and energy.

While there is no single dominant player, key players like IBM, Cisco, Accenture, Vodafone, and Microsoft lead the market with strong service portfolios, including device management, data analytics, security, and infrastructure solutions. These companies have the advantage of large-scale operations, extensive partnerships, and robust technological expertise.

The presence of numerous smaller, niche players offering specialised services also fosters innovation and competition. As a result, the market exhibits oligopolistic characteristics in terms of its dominant players but remains highly dynamic and fragmented at the service level.

Key Industry Developments

- In November 2025, Arviem AG and Tech Mahindra have formed a strategic partnership to develop IoT-enabled supply chain visibility solutions. By combining Arviem's real-time cargo monitoring expertise with Tech Mahindra's global technology capabilities, the partnership aims to optimize supply chains, enhance operational transparency, and drive sustainable business outcomes. The collaboration leverages IoT, analytics, and AI to help global enterprises make data-driven decisions and improve supply chain resilience.

- In June 2025, KORE Group Holdings, Inc. reached a significant milestone, achieving 20 million total IoT connections, solidifying its position as a global leader in IoT connectivity. This accomplishment highlights KORE’s continued growth and reliability as a provider of scalable, secure, and seamless IoT solutions. With a focus on innovation, reliability, and customer success, KORE is expanding its capabilities to support the evolving needs of IoT deployments worldwide, aiming for its next milestone of 30 million connections.

Companies Covered in IoT Managed Services Market

- Cognizant

- Tech Mahindra

- Cisco Systems, Inc.

- Oracle

- IBM Corporation

- Accenture

- HCL Technologies Limited

- Microsoft Corporation

- Honeywell International Inc.

- Google LLC

- AT&T Inc.

- General Electric Inc.

- SAP SE

- Intel Corporation

- Amazon Web Services, Inc.

Frequently Asked Questions

The global IoT Managed Services Market is projected to be valued at US$ 52.4 Bn in 2026.

Security Management is expected to account for approximately 28% of the global IoT Managed Services Market by Service type in 2026.

The market is expected to witness a CAGR of 11.3% from 2026 to 2033.

The IoT Managed Services Market growth is driven by the increasing complexity of industrial and automotive production, government-led digitalisation initiatives, and the rising need for security and energy optimisation in enterprise environments.

Key market opportunities in the IoT Managed Services Market include managing EV infrastructure and telematics, expanding into edge computing and 5G-enabled industrial applications, and supporting the transition to Industry 4.0 with real-time data analytics and condition-based maintenance.

The key players in the IoT Managed Services Market include IBM, Cisco Systems, Vodafone Group, Accenture, Ericsson, and Amazon Web Services (AWS).