- Telecommunications

- NB-IoT Chipset Market

NB-IoT Chipset Market Size, Share, and Growth Forecast, 2026 - 2033

NB-IoT Chipset Market by Chipset Type (Standalone, In-Band, Guard Band), Device Type (Small & Medium Enterprises (SMEs), Large Enterprises), Device Type (Smart Appliances, Smart Meters, Trackers, Alarms & Detectors, Wearable Devices, Others), Industry (Energy, Automotive & Transportation, Infrastructure & Building Automation, Others) and Regional Analysis for 2026 - 2033

NB-IoT Chipset Market Size and Trends Analysis

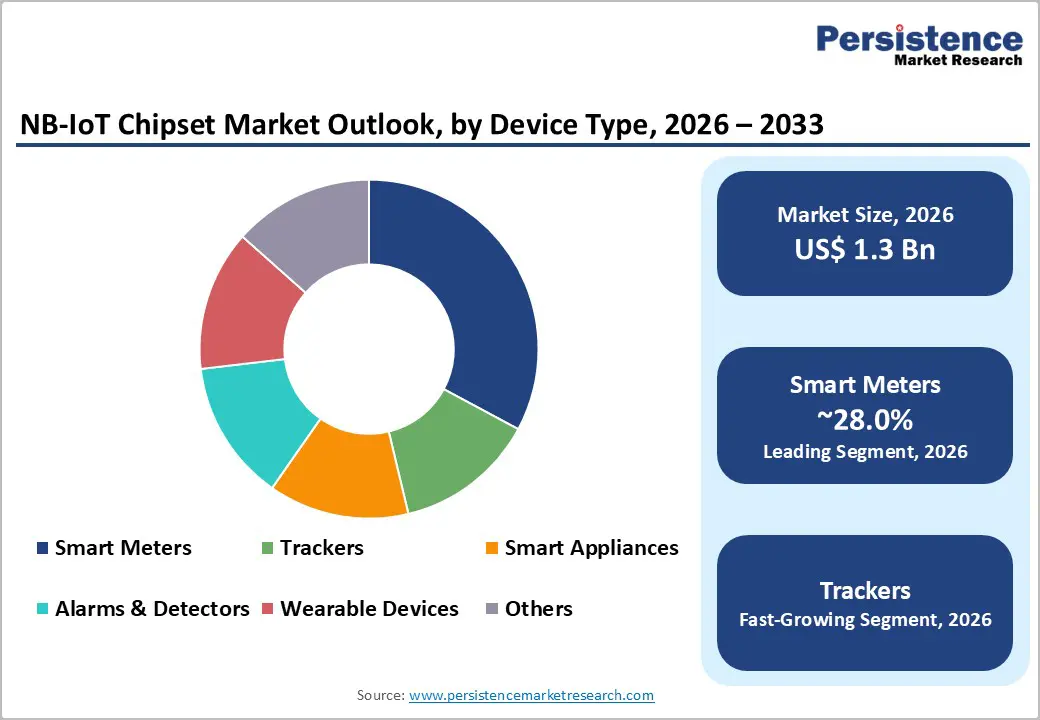

The global NB-IoT chipset market size is likely to be valued at US$ 1.3 billion in 2026 and is projected to reach US$ 5.3 billion by 2033, growing at a CAGR of 22.3% between 2026 and 2033.

This substantial expansion reflects the accelerating adoption of narrowband cellular connectivity across critical infrastructure and IoT applications globally. The market's trajectory demonstrates the fundamental shift toward standardised, power-efficient cellular solutions for distributed device ecosystems. Rising demand for connected smart meters, remote asset tracking, and energy management systems, coupled with aggressive infrastructure modernisation initiatives across emerging economies and developed regions, serves as the primary catalyst for market expansion.

Key Industry Highlights:

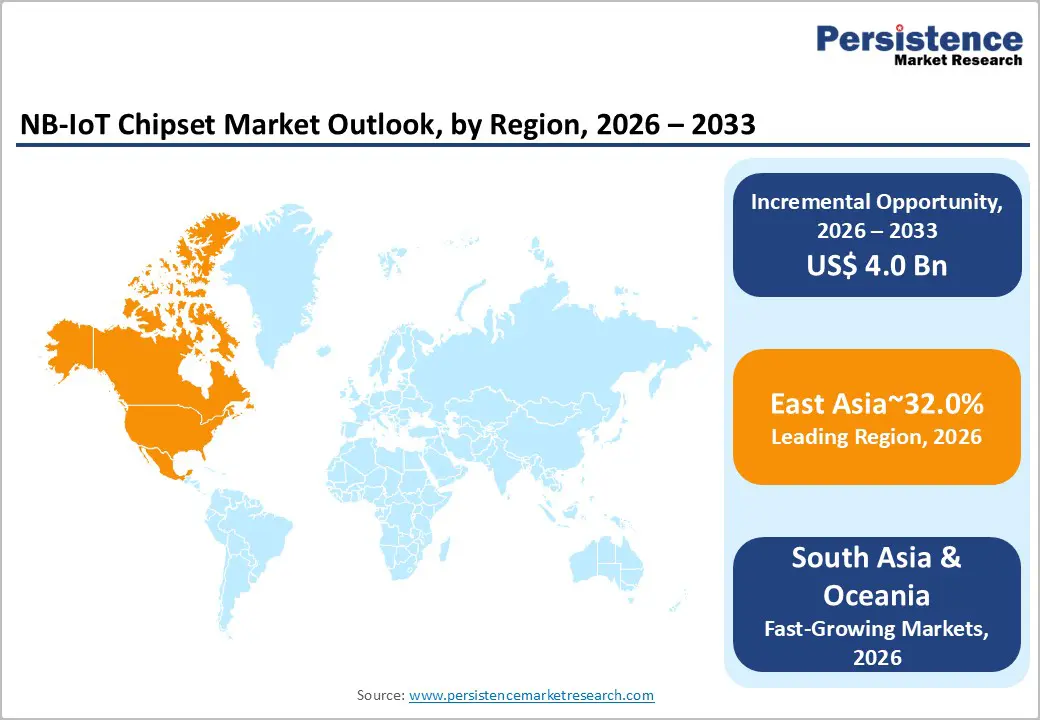

- Regional Leadership: North America leads the global NB-IoT Chipset Market with ~32% share, driven by grid modernisation, smart meter rollouts, and strong regulatory support for secure cellular IoT infrastructure.

- High-Volume Growth Engine: East Asia accounts for ~20% market share and remains the largest volume driver, supported by China’s annual procurement of 65-70 million smart meters and large-scale renewable energy integration.

- Regulation-Led Adoption: Europe captures ~24% share, benefiting from mandatory smart metering programs, strict cybersecurity and data privacy regulations, and advanced smart city deployments.

- Leading End-user: The energy sector dominates end-use demand with ~24% share, underpinned by global smart grid deployment, renewable integration, and real-time grid monitoring requirements.

- Fastest-Growing Application: Automotive and transportation emerge as the fastest-growing segment, driven by connected vehicle mandates, fleet telematics, EV charging infrastructure, and OTA compliance requirements.

- Technology & Product Leadership: Standalone NB-IoT chipsets lead with ~45% share due to low BOM cost, compact design, and ultra-long battery life enabled by 3GPP standardisation and power-efficient modem innovations.

| Key Insights | Details |

|---|---|

| NB-IoT Chipset Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 5.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 22.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.5% |

Market Dynamics

Drivers - Rise in Energy Security Concerns and Renewable Energy Integration Driving Smart Grid Deployment

The global energy landscape faces unprecedented pressures from geopolitical fragmentation, supply chain vulnerabilities, and the imperative for clean energy transitions. The International Energy Agency reports that escalating conflicts and market concentration have created significant energy security risks, with nearly 200 trade measures affecting clean energy technologies introduced since 2020, compared to just 40 over the previous five years. This fragmentation has catalysed governments and utilities to prioritise grid modernization and real-time monitoring infrastructure.

The NB-IoT Chipset Market stands to benefit substantially from this directive, as utilities require ultra-reliable, distributed connectivity solutions for smart meter deployment, grid monitoring, and renewable asset management.

India's government mandates 250 million smart prepayment meters as part of its energy security strategy, while China's State Grid continues tendering 65-70 million smart meters annually. This infrastructure demand directly translates to substantial chipset volume requirements, as each smart meter deployment incorporates NB-IoT connectivity.

The energy sector's projected utilisation of over 1 billion cellular IoT connections by 2028, with smart metering and grid monitoring generating over US$ 1 billion in annual connectivity revenue, demonstrates the structural market support for NB-IoT Chipset Market expansion.

Standardization and Extended Battery Life Enabling Multi-Year Device Operations

The completion of 3GPP NB-IoT standardization in Release 13 (2016) established a unified global framework that eliminated fragmentation and accelerated commercial deployment across all major telecom networks.

This regulatory clarity has enabled chipset manufacturers to achieve unprecedented power efficiency improvements. Qualcomm's 212 LTE IoT Modem, introduced in April 2020, delivered the industry's most power-efficient single-mode NB-IoT solution, enabling devices to operate for up to 15 years on battery charge. Subsequently, Qualcomm's 9205 LTE modem achieved 70% power savings in idle mode, supporting 10-year battery life requirements. These advancements have catalysed adoption across battery-powered applications, particularly in remote asset tracking, environmental monitoring, and healthcare.

The NB-IoT Chipset Market benefits from these efficiency gains through expanded addressable markets, previously infeasible applications now become commercially viable when device maintenance cycles extend to 10-15 years. Renesas Electronics' RH1NS200 chipset, specifically designed for India's smart metering market, demonstrates ultra-low power consumption of just 1µA in deep sleep mode, directly addressing utility operator requirements for multi-year meter replacement cycles.

This technical convergence between standardization, battery efficiency, and commercial viability has established a self-reinforcing cycle driving NB-IoT Chipset Market adoption across industrial IoT, smart infrastructure, and resource monitoring segments.

Satellite Connectivity Integration and Non-Terrestrial Network Expansion

The recent proliferation of satellite-enabled NB-IoT solutions represents a fundamental market expansion catalyst. In June 2023, Qualcomm introduced the 212S and 9205S modems with satellite capability, supporting 3GPP Release 17 standards for non-terrestrial network (NTN) connectivity developed in collaboration with Skylo. These solutions enable off-grid IoT devices to maintain connectivity in remote areas, fundamentally expanding the addressable market for NB-IoT Chipset applications.

Voice-over-NB-IoT (VoNB) capability in satellite mode, validated by Mavenir and Terrestar Solutions, further broadens use cases to emergency communication, disaster response, and maritime operations. Sony Semiconductor's Altair ALT1250 chipset earned certification from Skylo for dual-mode satellite-terrestrial IoT connectivity, creating a new market segment for hybrid connectivity solutions. STMicroelectronics' November 2025 release of ST87M01-1001 and ST87M01-1301 modules with optional geolocation capabilities demonstrates industry-wide commitment to satellite-terrestrial integration.

This technological convergence extends the NB-IoT Chipset Market beyond terrestrial cellular coverage, addressing previously unserved regions in agriculture, mining, maritime, and utility infrastructure. The ability to deliver reliable connectivity to remote monitoring stations without extensive terrestrial network expansion significantly reduces infrastructure costs and deployment timelines, thereby accelerating NB-IoT Chipset Market penetration in developing regions and underserved geographic areas.

Restraint - Competitive Fragmentation and Interoperability Challenges

The NB-IoT Chipset Market faces significant competitive pressure from alternative low-power wide-area (LPWA) technologies including LTE-M, EC-GSM-IoT, and unlicensed spectrum solutions such as LoRaWAN and Sigfox. This technological diversity creates procurement complexity for device manufacturers and operators, fragmenting chipset demand across competing platforms.

Global standardization efforts through 3GPP have mitigated but not eliminated these tensions, particularly as regional operators maintain preferences for specific technologies based on network infrastructure investments. Additionally, interoperability testing and certification requirements create substantial barriers to market entry, limiting the number of commercially viable chipset suppliers.

The lack of consistent security standards and device management protocols across different regions increases implementation costs for multinational IoT deployments. These structural constraints limit the concentration of demand among leading chipset manufacturers, preventing the substantial economies of scale necessary to reduce unit costs and improve profitability. Regulatory ambiguity regarding spectrum allocation and cross-border data governance further compounds interoperability challenges, particularly in emerging markets where regulatory frameworks remain under development.

Opportunity - Government-Mandated Smart City Infrastructure and Digital India Initiatives

Government commitment to smart cities development presents substantial structural demand for NB-IoT Chipset deployment across municipal infrastructure, utilities, and transportation systems. India's Cabinet Committee on Economic Affairs approved 12 new smart city projects under the National Industrial Corridor Development Programme with an investment of US$ 3.41 billion in August 2024, representing a direct demand catalyst for connectivity infrastructure.

The Indian government's expanded Smart Cities Mission targeting modernisation of 4,000 cities represents a fundamental shift in urban infrastructure investment, directly supporting deployment of connected smart meters, environmental sensors, and traffic management systems. These smart city implementations inherently require standardised, cost-effective cellular connectivity solutions at a massive scale, precisely the addressable market for NB-IoT chipsets.

The Ministry of Communications' Universal Connectivity and Digital India initiatives have deployed over 213,570 gram panchayats with fibre connectivity and 1,056,968 fibre-to-home connections as of July 2024, establishing the foundational network infrastructure necessary for comprehensive IoT deployment.

India's target of 250 million smart prepayment meters creates direct demand for NB-IoT connectivity across the utility sector, potentially translating to hundreds of millions of chipset units over the deployment cycle. Beyond India, similar government-sponsored smart city initiatives across Southeast Asia, Latin America, and Africa represent comparable demand drivers for NB-IoT Chipset deployment. The policy certainty and capital commitment associated with government-mandated infrastructure projects substantially reduce commercial uncertainty for chipset manufacturers and device integrators, enabling confidence in long-term production planning and supply chain investments. This government-driven demand represents a multi-year expansion opportunity for the NB-IoT Chipset Market, supporting sustained revenue growth aligned with infrastructure deployment timelines.

Automotive and Transportation Connectivity Requirements

The automotive industry's accelerating IoT adoption for connected vehicle platforms, fleet management systems, and telematics presents a substantial market expansion opportunity for NB-IoT chipsets. Regulatory frameworks, including ISO/SAE 21434 for cybersecurity, UNECE WP.29 R155 and R156 for software updates, and regional data privacy regulations, have mandated standardised, secure connectivity solutions for vehicle data transmission and over-the-air (OTA) updates. These regulatory mandates have created structural demand for certified, secure cellular IoT solutions compatible with automotive-grade security requirements. Connected vehicle platforms require reliable connectivity for real-time telematics, emergency communication, and predictive maintenance functionality that NB-IoT provides at substantially lower power and cost compared to broadband alternatives.

Fleet management systems enhanced by IoT technologies enable automated compliance reporting, vehicle tracking, fuel tax reporting, and driver inspection record management under regulations such as the Electronic Logging Device (ELD) Hours of Service mandate. These compliance requirements translate to connectivity obligations for commercial vehicle operators, creating demand for cost-effective, ubiquitous coverage.

The expansion of autonomous vehicle development and testing creates additional connectivity requirements for real-time vehicle monitoring, sensor data collection, and remote safety intervention. Government support for electric vehicle charging infrastructure further expands the addressable market, as smart charging systems require connectivity for demand-side management, energy optimisation, and billing integration. The automotive and transportation industry's regulatory pressures and operational requirements create sustained, structural demand for NB-IoT Chipset solutions. This represents one of the fastest-growing end-use segments projected to substantially expand market volume and revenue through 2033.

Category-wise Analysis

Chipset Type Insights

Standalone NB-IoT chipsets command the dominant market position, representing 45% of the total market share in 2026. These solutions integrate all necessary functionality on a single silicon die, eliminating the need for external modems or ancillary components. Qualcomm's 212 LTE IoT Modem exemplifies this architecture, delivering complete NB-IoT functionality with integrated power management, security processing, and RF transmission in a single integrated package.

Standalone designs minimise bill-of-materials costs, reduce device footprint, and simplify manufacturing processes critical advantages for high-volume IoT deployments. The architectural simplicity of standalone solutions enables rapid time-to-market for device manufacturers and supports cost optimization critical for price-sensitive applications, including smart meters and basic trackers.

In-band NB-IoT solutions, utilizing spectrum within existing LTE band allocations, represent the fastest-growing segment driven by operator network efficiency requirements and minimal spectrum acquisition costs. In-band deployment allows existing LTE network operators to enable NB-IoT connectivity through software upgrades and minor hardware modifications, eliminating the need for additional spectrum licenses.

Industry Insights

The energy sector maintains the leading position within the industry segmentation, accounting for 24% of the total NB-IoT Chipset Market share in 2026. This dominance reflects the structural imperative for smart grid modernisation, renewable energy integration, and real-time distribution system monitoring across developed and developing economies. Electric and gas utilities held 46% of global IoT spending in the energy sector in 2024, with approximately 38% of energy sector IoT revenue concentrated in North America, driven by federal grid resilience programs and state-level clean energy standards. Smart meter deployments, distribution grid monitoring, and renewable asset performance analytics represent the primary applications driving energy sector NB-IoT adoption.

Automotive and transportation applications represent the fastest-growing end-use industry segment, driven by connected vehicle requirements, fleet electrification, and regulatory mandates for cybersecurity and over-the-air update capability.

The regulatory imperative for ISO/SAE 21434 cybersecurity certification and UNECE WP.29 standards compliance has created structural demand for secure, standardised cellular connectivity solutions that NB-IoT provides. Electric vehicle charging infrastructure, vehicle telematics, predictive maintenance systems, and autonomous vehicle development collectively create a multifaceted demand for IoT connectivity.

Regional Insights and Trends

North America NB-IoT Chipset Market Trends

North America commands 32% of the global NB-IoT Chipset Market, reflecting the region's mature technological infrastructure, early IoT adoption, and substantial capital investment in grid modernisation.

AT&T launched its narrowband IoT network across the United States in July 2019, complementing its existing LTE-M network and expanding low-power wide-area (LPWA) capabilities to millions of IoT devices. This network infrastructure investment established North American operators as early commercial deployments of NB-IoT technology.

Federal and state governments have prioritised grid resilience and smart meter deployment as critical infrastructure security measures, creating sustained demand for cellular IoT solutions. Utility commitments to smart electricity meter deployment, combined with federal infrastructure programs supporting EV charging networks and grid modernization, establish North America as a primary addressable market for NB-IoT chipset suppliers.

The region's advanced cybersecurity regulatory framework, established through standards including ISO/SAE 21434 and UNECE vehicle communication protocols, has created a stringent compliance environment that favours standardised cellular solutions over fragmented proprietary platforms.

North America's mature telecom infrastructure and high network coverage penetration enable rapid NB-IoT deployment without requiring extensive spectrum acquisition or network buildout investments. The region's capital-intensive infrastructure modernization cycle, particularly surrounding electric vehicle charging expansion and distributed renewable energy integration, continues generating sustained demand for connected sensing and control systems.

East Asia NB-IoT Chipset Market Trends

East Asia represents 20% of the global NB-IoT Chipset Market and operates as the critical growth engine for volume expansion through 2033. China, as the world's largest contributor to renewable energy capacity additions with 60% of global 2023 renewable deployments, requires massive IoT connectivity infrastructure for distributed energy resource management and grid optimization. China's State Grid continues annual procurement of 65-70 million smart meters, establishing a structural demand baseline of unprecedented scale for NB-IoT chipsets.

Japan, as one of the world's most advanced cellular markets, has achieved completion of national smart meter rollout, with first-generation meter replacement now underway. NTT DOCOMO's validation of Altair Semiconductor's ALT1250 chipset in 2019 established Japan as an early commercial deployment market, with ongoing integration of NB-IoT connectivity across smart city infrastructure and industrial IoT applications.

South Korea's smart meter rollout, initially delayed but targeted for completion by the end of 2024 through Korea Electric Power Corporation (KEPCO) deployment, creates sustained demand for embedded cellular connectivity.

Europe NB-IoT Chipset Market Trends

Europe accounts for 24% of the global NB-IoT Chipset Market, driven by stringent environmental regulations, renewable energy deployment requirements, and advanced smart city initiatives. European Union member states have implemented mandatory smart meter deployment programs as part of clean energy directives and grid modernization strategies. Germany, the United Kingdom, and Scandinavian countries have established early adoption markets for connected utility infrastructure and distributed energy resource management.

The European Union's regulatory framework emphasizing data privacy (GDPR), cybersecurity (NIS2 Directive), and environmental sustainability, has created market conditions favouring standardised, secure connectivity solutions, including NB-IoT. These regulatory requirements have elevated security and data protection as competitive differentiators, supporting the adoption of 3GPP-standardised solutions with integrated security architecture.

European utilities and device manufacturers have prioritized interoperability and long-term regulatory compliance, supporting NB-IoT's standardized framework. The continent's advanced 4G/LTE infrastructure enables rapid NB-IoT deployment through network software upgrades and spectrum efficiency optimisation. Healthcare IoT adoption in Europe, particularly for remote patient monitoring and chronic disease management in ageing populations, creates additional demand drivers for wearable device connectivity.

Competitive Landscape

The global NB-IoT chipset market is largely consolidated, with a few leading players capturing the majority of the market share, while smaller vendors compete in specialised segments. Key companies, including Qualcomm Technologies, MediaTek Inc., Huawei (HiSilicon/Huawei IoT), Sequans Communications, and Nordic Semiconductor, dominate the landscape with advanced, low-power, wide-area network (LPWAN) solutions tailored for smart devices, industrial IoT, and connected infrastructure. These top players leverage strong R&D capabilities, proprietary chip designs, and extensive ecosystem partnerships to maintain leadership and address growing demand for reliable, energy-efficient connectivity.

The market exhibits moderate competitive pressure, driven by the rapid adoption of IoT applications in sectors such as smart metering, wearables, automotive, and industrial automation. While the leading vendors focus on scalability, power efficiency, and integration with 4G/5G networks, smaller players like Sony (Altair Semiconductor), u-blox, and STMicroelectronics compete on niche applications and cost-effective solutions for specific IoT deployments.

Key Industry Developments:

- Nov 17, 2025, STMicroelectronics introduced two new versions of its ST87M01 NB-IoT modules, the ST87M01-1001 and ST87M01-1301, supporting narrowband cellular connectivity and optional geolocation capabilities. These modules cater to a range of IoT applications, including smart logistics, environmental monitoring, and healthcare. The new ecosystem includes an evaluation kit, IoT SIM card, and software library, facilitating easy development of scalable and secure IoT solutions.

- June 22, 2023 - Qualcomm Technologies, Inc. launched the Qualcomm® 212S and Qualcomm® 9205S modems, featuring satellite capability to enable off-grid IoT devices with hybrid connectivity. These modems, developed in collaboration with Skylo, support 3GPP Release 17 standards for satellite communications, offering global coverage and real-time tracking via the Qualcomm Aware™ platform. The modems provide connectivity in remote areas, enhancing asset tracking and decision-making for industries relying on non-terrestrial network (NTN) solutions.

Companies Covered in NB-IoT Chipset Market

- Qualcomm Technologies

- MediaTek Inc.

- Huawei (HiSilicon / Huawei IoT)

- Sequans Communications

- Nordic Semiconductor

- Sony (Altair Semiconductor)

- u-blox

- STMicroelectronics

Frequently Asked Questions

The global NB-IoT Chipset Market is projected to be valued at US$ 1.3 Bn in 2026.

The Standalone segment is expected to account for approximately 45.0% of the global NB-IoT Chipset Market by Chipset Type in 2026.

The market is expected to witness a CAGR of 22.3% from 2026 to 2033.

The Global NB-IoT Chipset Market growth is driven by escalating energy security concerns and renewable integration accelerating smart grid deployments, 3GPP standardisation enabling ultra-low-power long-life devices, and satellite-terrestrial NB-IoT expansion extending reliable connectivity to remote and off-grid applications.

Key NB-IoT Chipset Market opportunities arise from government-mandated smart city and Digital India infrastructure driving mass smart meter and urban IoT deployments, alongside rising automotive and transportation connectivity needs for telematics, fleet management, regulatory compliance, and smart EV charging systems.

Key players in the NB-IoT Chipset Market include Qualcomm Technologies, MediaTek Inc., Huawei (HiSilicon / Huawei IoT), Nordic Semiconductor, and u‑blox.