- Agrochemicals

- Plant Biotechnology Services Market

Plant Biotechnology Services Market Size, Share, and Growth Forecast 2026 - 2033

Plant Biotechnology Services Market by Service Type (Genomics Services, Proteomics Services, Metabolomics Services, Analytical Chemistry, Cellular Imaging, Forage Analysis, Others), by Crop (Cereals & Grains, Fruits & Vegetables, Oilseeds & Pulses), End-user (Research Institutes, Pharmaceuticals Companies, Biotechnology Companies, Academic Institutes, Agriculture Industry), and Regional Analysis, 2026 - 2033

Plant Biotechnology Services Market Size and Trend Analysis

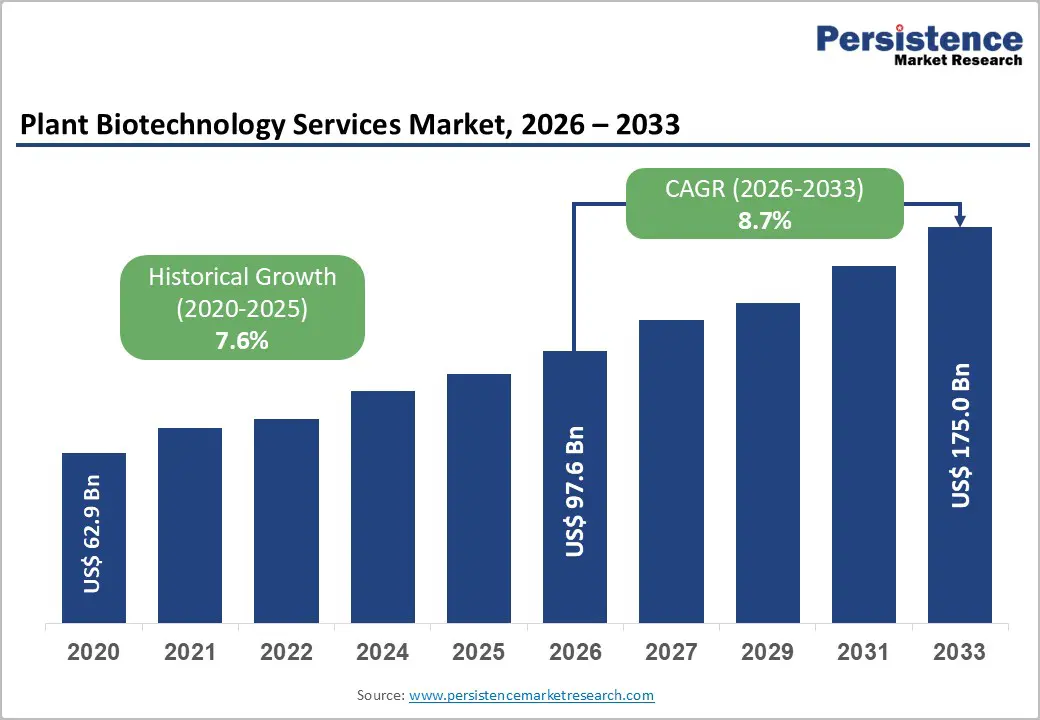

The global Plant Biotechnology Services market size is likely to be valued at US$ 97.6 billion in 2026 and is expected to reach US$ 175.0 billion by 2033, growing at a CAGR of 8.7% during the forecast period from 2026 to 2033. The market's strong growth is driven by increasing global food security needs, the rise of precision genomics and gene editing in crop improvement, and the growing pharmaceutical and nutraceutical use of plant-based compounds, all requiring specialized biotechnology services in genomics, proteomics, and metabolomics.

Key Industry Highlights:

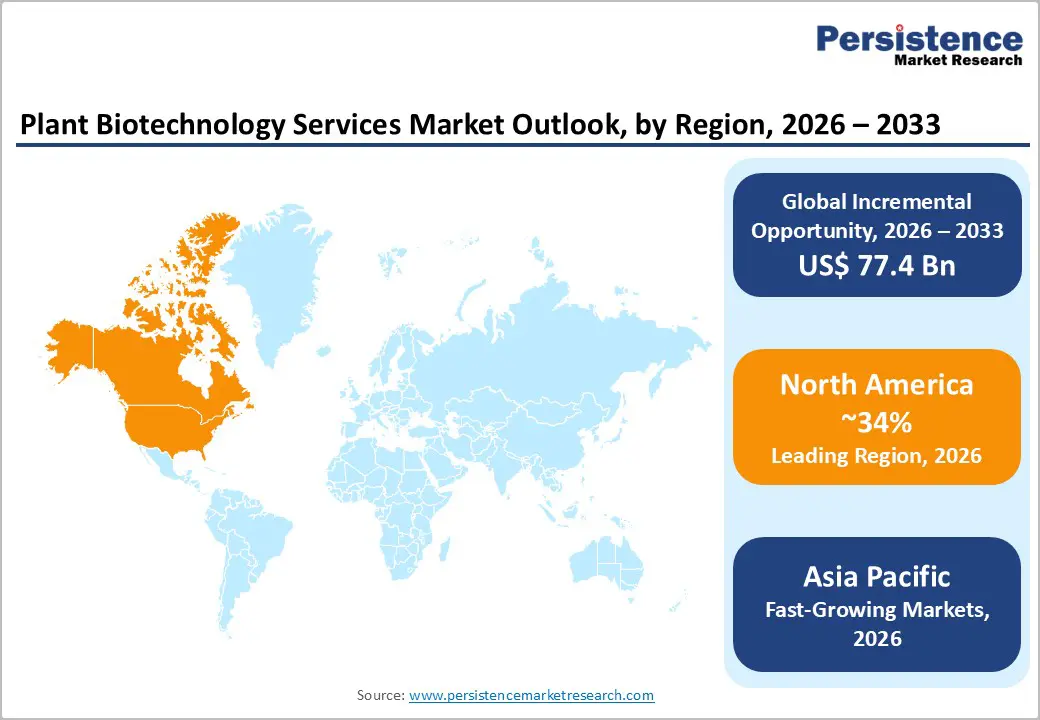

- Leading Region: North America leads the Plant Biotechnology Services market holding 34% share, due to high biotech crop adoption in the U.S., strong government funding for plant genome research, and the presence of major companies such as Thermo Fisher Scientific, Agilent Technologies, and Corteva Agriscience.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 9.8%, driven by China’s approval of transgenic crops, India’s biotechnology initiatives, and the region’s large agricultural production base, creating strong demand for plant genomics and molecular.

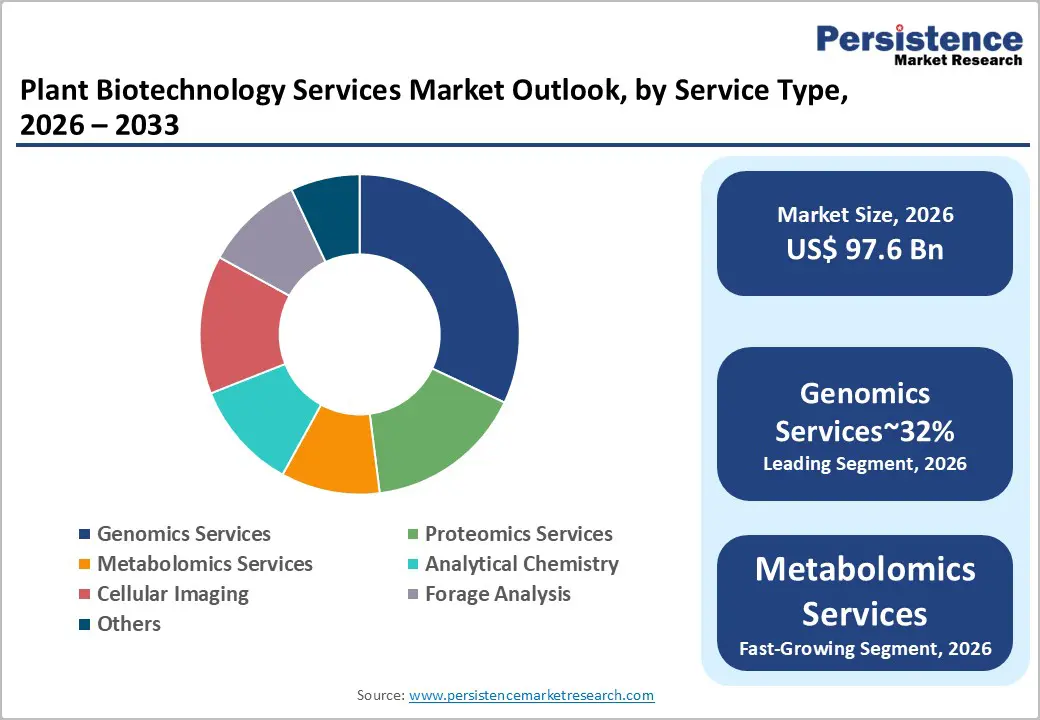

- Leading Segment: Genomics services dominate the service segment with around 32% market share, supported by declining sequencing costs and the essential role of genomics in CRISPR gene editing, molecular breeding, QTL mapping, and crop trait development.

- Fastest-Growing Segment: Fruits & vegetables are the fastest-growing segment, driven by increasing demand for disease-resistant, high-yield, and nutritionally enhanced horticultural crops, along with rising adoption of molecular breeding technologies in commercial horticulture.

- Key Opportunity: Plant molecular farming and CRISPR editing services present major growth opportunities, supported by evolving regulatory frameworks and rising pharmaceutical interest in plant-based protein production, vaccine development, and advanced crop improvement technologies.

| Key Insights | Details |

|---|---|

|

Plant Biotechnology Services Market Size (2026E) |

US$ 97.6 Billion |

|

Market Value Forecast (2033F) |

US$ 175.0 Billion |

|

Projected Growth CAGR (2026–2033) |

8.7% |

|

Historical Market Growth (2020–2025) |

7.6% |

Market Dynamics

Drivers - Global Food Security Crisis and Climate-Resilient Crop Development Programs Driving Plant Biotechnology Service Demand

Feeding the rapidly growing global population while facing worsening climate conditions has become one of the biggest structural challenges for the agriculture sector. Rising temperatures, irregular rainfall patterns, and frequent extreme weather events are reducing crop productivity in many regions. These challenges are significantly increasing the demand for plant biotechnology services that help accelerate the development of climate-resilient and high-yield crop varieties. The Sixth Assessment Report of the Intergovernmental Panel on Climate Change (IPCC) highlights declining crop yields due to climate stress as a major threat to global food security. As a result, governments, global research organizations, and agri-biotech companies are investing heavily in genomics-driven crop improvement programs.

The Consultative Group on International Agricultural Research (CGIAR) manages a coordinated network of global crop research programs that invests over US$1 billion annually in plant science research. These programs rely extensively on plant biotechnology services such as high-throughput genotyping, genomic selection modeling, and molecular marker-assisted breeding. These services accelerate the development of drought-tolerant, heat-resistant, and disease-resistant crop varieties for regions most vulnerable to food insecurity.

Precision Gene Editing Technologies and CRISPR Applications Creating New High-Value Plant Biotechnology Service Categories

The rapid advancement and commercialization of CRISPR-Cas9 and other precision gene editing technologies for crop improvement are creating entirely new service opportunities within the plant biotechnology services market. These technologies allow researchers to make highly precise genetic modifications in plants, significantly accelerating crop development timelines. As a result, specialized services such as guide RNA design, editing efficiency optimization, off-target mutation analysis, edited plant characterization, and regulatory documentation preparation are becoming increasingly important. These services are generating substantial new revenue streams across the plant biotechnology services ecosystem.

Regulatory developments are also supporting market growth. For example, the European Commission proposed new regulations in 2023 for New Genomic Techniques (NGT), which aim to simplify the approval process for CRISPR-edited crops that could naturally occur through traditional breeding. This policy change is expected to significantly accelerate CRISPR-based crop development across Europe and boost demand for gene editing services. Companies such as GenScript Biotech Corporation and Thermo Fisher Scientific have introduced comprehensive CRISPR-as-a-service platforms that integrate guide RNA synthesis, Cas9 protein supply, plant transformation, and molecular characterization services. Additionally, the updated biotechnology regulatory framework of the USDA Animal and Plant Health Inspection Service exempts certain gene-edited crops from full GMO review, further encouraging new commercial gene-editing projects and increasing service procurement demand.

Restraints - Complex and Divergent Global Regulatory Frameworks for Biotech Crops Creating Service Pipeline Delays and Cost Escalation

Despite strong technological progress, the plant biotechnology services market faces significant challenges due to complex and inconsistent regulatory frameworks governing genetically modified and gene-edited crops across different countries. These regulatory differences create long approval timelines, higher development costs, and fragmented commercialization strategies for agri-biotech companies. In particular, the European Union has one of the most stringent regulatory frameworks for genetically modified organisms under Directive 2001/18/EC.

This regulation requires extensive environmental risk assessments, multi-year field trials, and safety evaluations conducted by the European Food Safety Authority before commercial cultivation approval is granted. As a result, obtaining approval for a single crop-trait combination in Europe can take between seven and ten years and may cost between US$35 million and US$50 million. These regulatory complexities force biotechnology companies to allocate significant financial and technical resources toward regulatory compliance and documentation services rather than focusing on innovation and research activities.

Ethical Concerns and Public Perception Challenges Around GMO Crops Limiting Commercial Adoption in Key Markets

Public perception and ethical concerns surrounding genetically modified crops continue to create challenges for the plant biotechnology services industry in several major global markets. In regions such as Europe, Japan, and parts of Africa, consumer skepticism toward genetically modified organisms has led to strong opposition from advocacy groups and non-governmental organizations. This resistance influences government policies and regulatory decisions, which ultimately restrict the commercial adoption of biotechnology-derived crops.

Surveys such as the Eurobarometer on Science and Technology consistently show that many European consumers prefer food products that are labeled GMO-free. Such consumer preferences strongly influence agricultural policies in countries including Germany, France, and Austria, where governments maintain cautious or restrictive positions regarding GMO crop cultivation. As a result, the commercial market for biotech crops remains limited in these otherwise technologically advanced economies. These perceptions also affect emerging applications such as plant molecular farming and pharmaceutical protein production using transgenic plants. Concerns related to food safety, environmental impact, and ethical considerations continue to shape regulatory policies and consumer behavior, creating uncertainty for companies investing in plant biotechnology research and services.

Opportunities - Agricultural Genomics and Molecular Breeding Services Expansion Driven by Precision Agriculture Adoption

The rapid adoption of precision agriculture technologies is creating strong growth opportunities for genomics-based molecular breeding services across the global agriculture industry. Modern precision farming practices, including GPS-guided equipment, satellite monitoring, and data-driven crop management systems, are enabling farmers and seed companies to optimize agricultural productivity with greater accuracy. To fully leverage these technologies, agricultural companies require improved crop varieties that offer higher yields, stronger disease resistance, better drought tolerance, and improved nutritional value. Genomics-based molecular breeding services play a crucial role in developing such advanced crop varieties.

According to research by the International Maize and Wheat Improvement Center (CIMMYT), genomic selection techniques can accelerate crop improvement programs by two to three times compared with traditional breeding methods. This significant improvement in breeding efficiency is encouraging seed companies and research organizations to invest heavily in high-throughput genotyping and genomic selection services. Leading companies such as Eurofins Scientific and Keygene provide advanced genomics platforms and molecular breeding technologies that support crop improvement programs across cereals, oilseeds, vegetables, and specialty crops.

Plant Molecular Farming and Pharmaceutical-Grade Plant Protein Production Creating High-Value Service Opportunity

Plant molecular farming is emerging as an innovative field that combines plant biotechnology with pharmaceutical manufacturing, creating new high-value service opportunities within the plant biotechnology services market. This technology enables the production of pharmaceutical proteins, vaccines, monoclonal antibodies, and industrial enzymes using genetically engineered or transiently expressed plant systems. Compared with traditional cell culture systems, plant-based production platforms offer several advantages, including lower facility costs, faster scalability, and simplified manufacturing processes. Successful examples have already demonstrated the potential of this technology.

Medicago developed a plant-based COVID-19 vaccine using Nicotiana benthamiana plants, while Kentucky BioProcessing produced the ZMapp antibody treatment for Ebola using plant expression systems. These developments have increased global interest in plant-based pharmaceutical production. International organizations such as the World Health Organization have also highlighted plant molecular farming as a promising alternative manufacturing platform, particularly for developing countries. Governments and research institutions in countries such as India, Brazil, and South Africa are investing in plant-based vaccine and protein production initiatives. As a result, pharmaceutical companies increasingly outsource plant transformation, gene design, and protein expression services to specialized biotechnology service providers, creating strong growth opportunities for companies such as Thermo Fisher Scientific and GenScript Biotech Corporation.

Category-wise Analysis

By Service Type Insights

Genomics services lead the global plant biotechnology services market by service type, accounting for approximately 32% of total segment revenue in 2026. This leadership is driven by genomics’ fundamental role as the core scientific discipline supporting almost every plant biotechnology application, including molecular marker-assisted breeding, quantitative trait locus (QTL) mapping, CRISPR guide RNA design, transgenic event characterization, and gene expression profiling. The rapid decline in next-generation sequencing (NGS) costs has significantly expanded the accessibility of genomics services.

Major commercial providers supporting this segment include Thermo Fisher Scientific’s Ion Torrent sequencing platforms, Agilent Technologies’ genomic microarray solutions, and Eurofins Scientific’s plant genotyping services. Proteomics Services represent the second-largest segment, driven by growing pharmaceutical and nutraceutical demand for advanced plant protein analysis.

By Crop Analysis

Cereals & Grains dominate the global Plant Biotechnology Services market by crop type, accounting for approximately 44% of total crop segment revenue in 2026. This dominance reflects the critical role of crops such as wheat, rice, maize, sorghum, barley, and millet, which form the foundation of global food systems. According to the Food and Agriculture Organization (FAO), cereals provide nearly 50% of global caloric intake, making them the primary targets for biotechnology research focused on improving yield, climate resilience, nutritional quality, and disease resistance. Programs require specialized biotechnology services to accelerate crop breeding and genetic improvement.

Fruits & Vegetables represent the second-largest crop segment, supported by the growing adoption of molecular breeding technologies to develop disease-resistant and nutritionally enhanced horticultural crop varieties.

By End-user Insights

Biotechnology Companies lead the global market by end-user, accounting for approximately 35% of total segment revenue in 2026. The dominance of this segment reflects the private sector’s strong investment in agricultural biotechnology research and development. This outsourcing model allows companies to access advanced technologies and specialized expertise while improving research efficiency.

Leading service partners in this ecosystem include GenScript Biotech Corporation and Eurofins Scientific SE, which support major crop research programs worldwide. Research Institutes represent the second-largest end-user segment, supported by government-funded agricultural research organizations such as CGIAR, USDA Agricultural Research Service, and national agricultural research councils.

Regional Insights

North America Plant Biotechnology Services Trends

North America leads the global Plant Biotechnology Services market, supported by the United States’ strong biotechnology agriculture sector and its concentration of leading agri-biotech companies, research universities, and specialized service providers. According to the USDA Economic Research Service (ERS), more than 90% of U.S. corn, soybean, and cotton cultivation utilized biotech varieties in 2023, demonstrating the widespread adoption of biotechnology in crop production.

Government funding also plays a major role in supporting plant biotechnology research. Programs such as the National Science Foundation’s Plant Genome Research Program (PGRP) and the USDA National Institute of Food and Agriculture’s Agriculture and Food Research Initiative (AFRI) collectively invest billions of dollars annually in plant science research. Major companies, including Thermo Fisher Scientific and Agilent Technologies provide key genomics and analytical platforms supporting the industry. Additionally, Corteva Agriscience and Bayer CropScience’s North American operations represent some of the world’s largest buyers of plant biotechnology services. A streamlined regulatory environment, including the FDA’s Plant Biotechnology Consultation Program and the USDA APHIS SECURE Rule, further supports strong market growth.

Europe Plant Biotechnology Services Trends

Europe represents a technologically advanced and commercially important regional market for plant biotechnology services. The region benefits from a strong network of leading academic institutions, biotechnology companies, and pharmaceutical research centers. Although historically strict GMO cultivation policies have limited certain applications, regulatory developments such as the European Commission’s 2023 proposal on New Genomic Techniques are gradually creating new opportunities for innovation. Germany is a major hub for plant biotechnology research, hosting renowned institutions including the Max Planck Institute of Molecular Plant Physiology and the Leibniz Institute of Plant Genetics and Crop Plant Research, both of which generate significant demand for genomics, metabolomics, and analytical testing services.

Merck KGaA, headquartered in Darmstadt, is a key supplier of life science tools and biotechnology services through its Sigma-Aldrich brand. The United Kingdom also plays an important role, supported by research centers such as Rothamsted Research, the John Innes Centre, and the Sainsbury Laboratory. In addition, the Horizon Europe research program, with a €95.5 billion budget, funds large collaborative biotechnology projects across Europe.

Competitive Landscape

Asia Pacific is the fastest-growing regional market for plant biotechnology services, driven by expanding biotechnology investment in China, India, and Japan, as well as the region’s central role in global food production. China is accelerating agricultural biotechnology development through national initiatives led by the Ministry of Agriculture and Rural Affairs. The approval of several transgenic maize and soybean varieties between 2022 and 2023 has stimulated rapid growth in domestic plant biotechnology research and service demand.

Institutions such as the National Agricultural Biotechnology Research Center are strengthening the country’s genomics and crop improvement capabilities. India is also emerging as an important market, supported by programs from the Department of Biotechnology, including the National Agricultural Bioinformatics Grid and the ICAR National Initiative on Climate Resilient Agriculture. These initiatives create strong demand for genomics, metabolomics, and analytical testing services. Meanwhile, Japan’s advanced plant science ecosystem, supported by institutions such as the RIKEN Center for Sustainable Resource Science and Nagoya University, drives demand for high-precision proteomics and plant physiology research technologies.

Key Developments:

- In January 2025: Thermo Fisher Scientific Inc. expanded collaboration with several centers under CGIAR to support plant genomics programs. The partnership focuses on next-generation sequencing and bioinformatics analysis for cereal crop breeding, helping researchers accelerate genomic selection and climate-resilient variety development across Africa, Asia, and Latin America.

- In September 2024: Eurofins Scientific SE strengthened its agricultural genomics capabilities by expanding its plant genotyping and sequencing operations in Bangalore, India. The facility supports high-throughput DNA sequencing, SNP marker genotyping, and molecular breeding services for seed companies and research institutions developing improved crop varieties.

- In March 2024: GenScript Biotech Corporation enhanced its plant gene-editing service portfolio by introducing an integrated CRISPR editing platform. The service provides guide RNA design, plant transformation, edited event screening, and molecular characterization, helping agri-biotech companies and academic researchers accelerate precision crop improvement projects.

Companies Covered in Plant Biotechnology Services Market

- Keygene N.V.

- Heinz Walz GmbH

- LemnaTec GmbH

- Photon Systems Instruments, spol. s.r.o.

- Thermo Fisher Scientific Inc.

- Agilent Technologies

- GenScript Biotech Corporation

- Eurofins Scientific SE

- Novo Nordisk A/S

- Merck KGaA

- Abbott Laboratories

- Pfizer, Inc.

- Biogen

- F. Hoffmann-La Roche Ltd.

- Bayer CropScience AG

- Corteva Agriscience

- Syngenta AG

- BASF Agricultural Solutions

Frequently Asked Questions

The global Plant Biotechnology Services market is valued at US$ 97.6 billion in 2026 and is projected to reach US$ 175.0 billion by 2033, registering a CAGR of 8.7%, supported by expanding genomics and biotech crop adoption.

Key drivers include the FAO’s projected 50% rise in global food demand by 2050, growing investment in crop genomics programs, and increasing adoption of CRISPR gene-editing technologies for advanced crop improvement.

Genomics Services lead the market with about 32% revenue share in 2026, supported by declining sequencing costs, rising high-throughput genotyping demand, and strong service platforms from major life science companies.

North America leads the market due to high biotech crop adoption in the U.S., strong agricultural R&D funding, advanced research infrastructure, and the presence of major biotechnology companies and service providers.

A major opportunity lies in CRISPR gene editing and plant molecular farming services, supported by regulatory progress and growing pharmaceutical interest in plant-derived proteins and vaccine manufacturing platforms.