- Electrical Equipment & Services

- Electrical Coil Windings Market

Electrical Coil Windings Market Size, Share, and Growth Forecast for 2025 - 2032

Electrical Coil Windings Market by Product (Copper Winding and Aluminum Winding), Application (Motors, Transformers, and Inductors/Other), End-user (Industrial, Automotive & EV and Power & Utilities) and Regional Analysis from 2025 to 2032

Electrical Coil Windings Market Size and Share Analysis

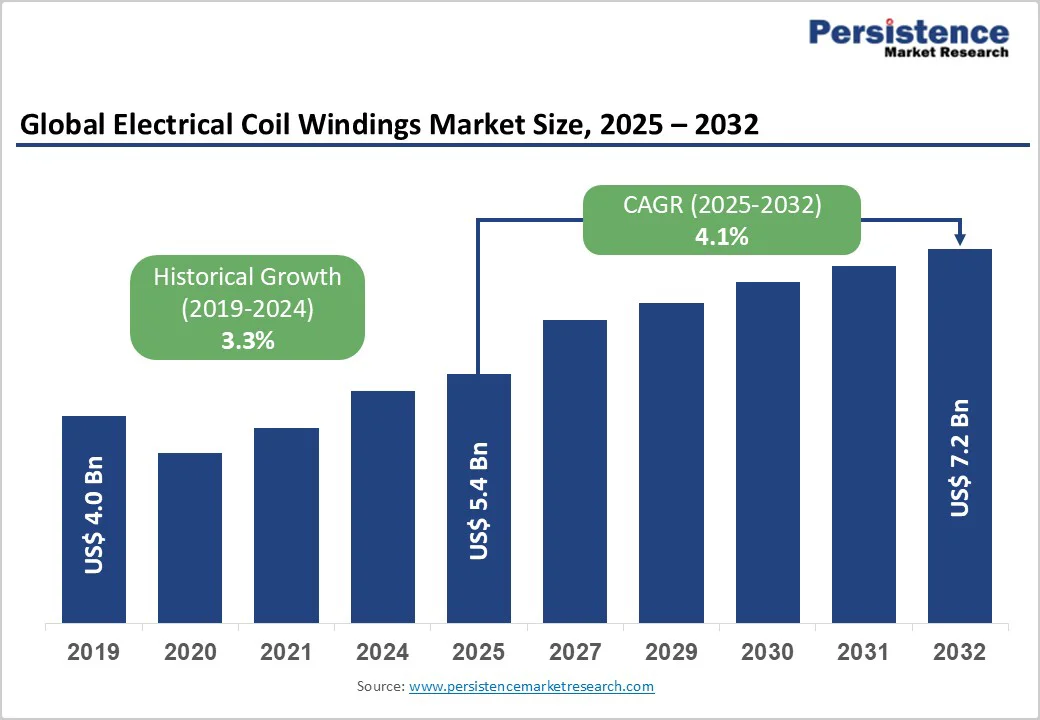

The global electrical coil windings market size is likely to value at US$5.4 billion in 2025 and is projected to reach US$7.2 billion, growing at a CAGR of 4.1% between 2025 and 2032.

This trajectory represents a fundamental shift in the electrical components sector, driven by accelerating electrification across industries and the increasing demand for energy-efficient solutions. The market's expansion reflects the critical role of coil windings in electric motors, transformers, and inductors that power modern infrastructure and technology applications.

Key Industry Highlights:

- Leading Winding Type: The copper winding segment dominates the market with a 61% share in 2025, attributed to its superior conductivity, thermal performance, and reliability across industrial and power applications. The aluminum winding segment emerges as the fastest-growing category, offering 15-25% cost advantages that are accelerating its adoption in cost-sensitive and lightweight motor designs.

- Application Leadership: The motor segment leads the market with a 52% share (USD 2.8 billion), supported by rising demand for energy-efficient motors across manufacturing, EV, and HVAC applications. The transformer segment is projected to be the fastest-growing application area, driven by large-scale infrastructure modernization and renewable energy grid integration initiatives worldwide.

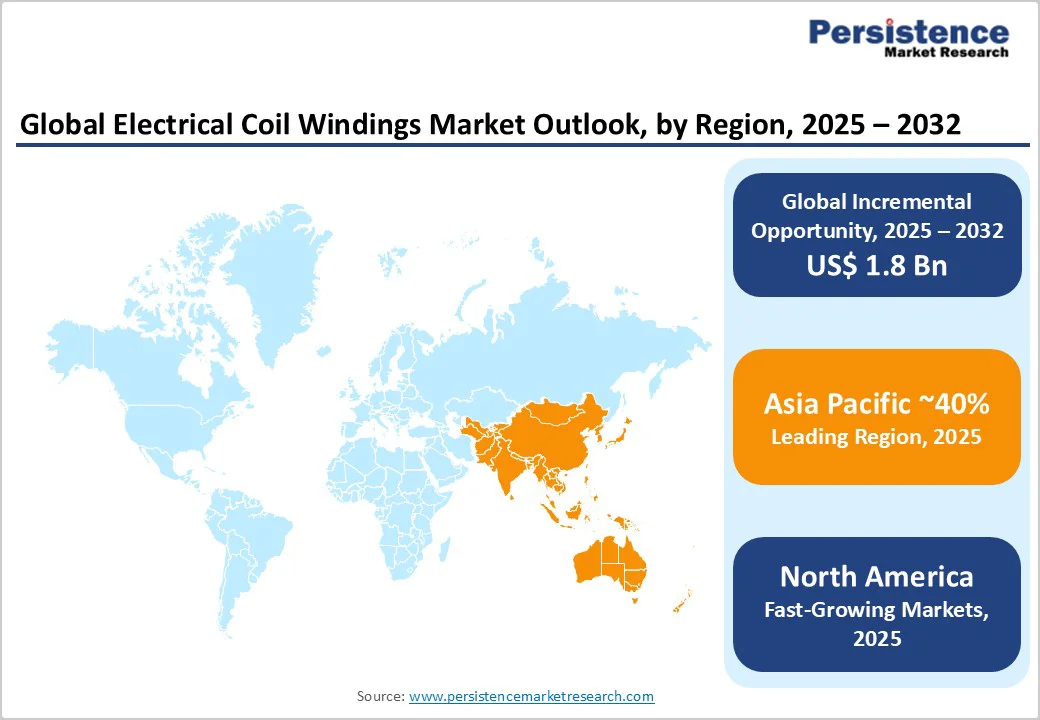

- Regional Dominance: Asia Pacific commands a 40% share of the global market in 2025, led by China’s 56.9% contribution within the region, supported by robust manufacturing and electrification programs. North America follows with a 25% share, underpinned by a strong innovation ecosystem and advanced automation in electric machinery production.

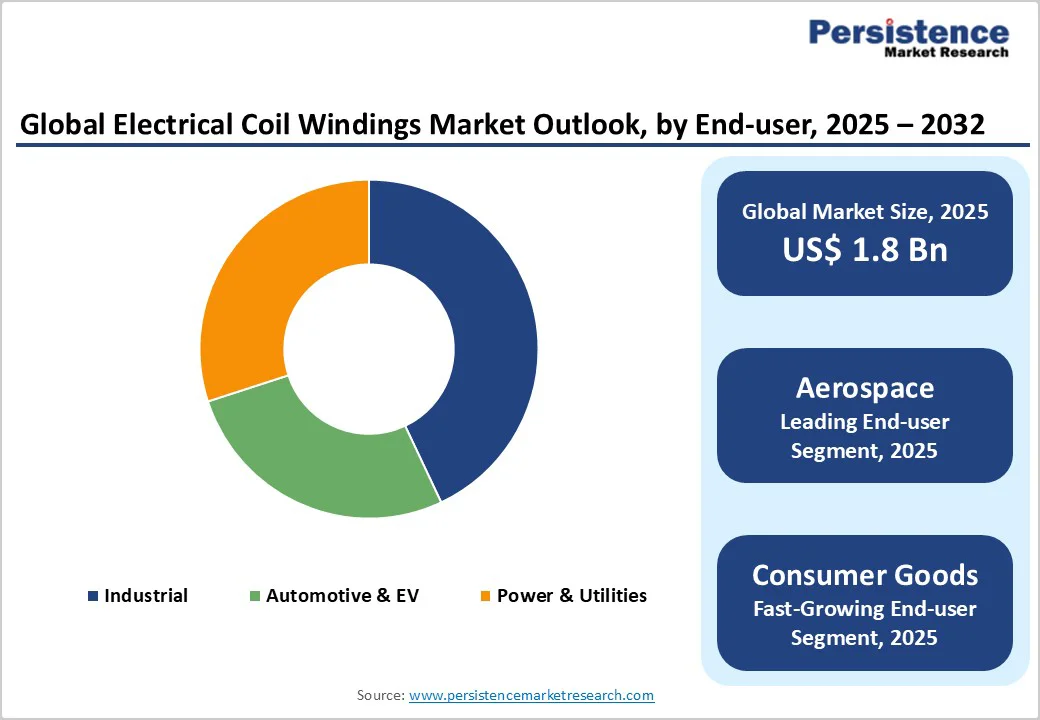

- Leading End-User: The industrial segment holds a 42.3% market share in 2025, driven by extensive adoption in machinery, process industries, and automation systems. The power and utilities segment represents the fastest-growing end-user category, fueled by grid modernization, electrification projects, and clean energy transition policies.

- Technological Advancement: The ongoing electric vehicle revolution acts as a market multiplier, with each EV requiring substantially more coils than conventional vehicles. Simultaneously, the 5G infrastructure rollout and renewable energy expansion are creating new high-performance winding applications, accelerating product innovation and diversification across the industry.

| Key Insights | Details |

|---|---|

| Electrical Coil Windings Market Size (2025E) | US$ 5.4 Bn |

| Projected Market Value (2032F) | US$ 7.2 Bn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 4.1% |

| Historical Market Growth Rate (CAGR 2019 to 2023) | 3.3% |

Market Dynamics

Electric Vehicle Revolution and Automotive Electrification

The electric vehicle segment represents the most significant growth catalyst, with global EV sales reaching 10 million units in 2020 and projected to reach 23 million units by 2030. This dramatic expansion directly translates to increased demand for precision coil windings in traction motors, charging infrastructure, and power electronics systems.

Each EV requires significantly more coils than traditional internal combustion engine vehicles, creating a multiplier effect for market demand. The automotive industry's shift toward electrification is driving investments in high-speed, automated coil winding systems capable of handling the volume requirements for motor production.

Furthermore, advanced winding techniques like rectangular magnet wire technology are enabling lighter, more powerful motors essential for EV performance optimization.

Renewable Energy Infrastructure Expansion

The global transition to sustainable energy sources is generating substantial demand for coil windings in wind turbines, solar inverters, and grid-scale energy storage systems. Government policies promoting renewable energy adoption are driving significant infrastructure investments, particularly in emerging markets where rapid industrialization coincides with clean energy initiatives.

Wind turbine manufacturers require specialized winding services for their generators, while solar installations demand high-efficiency transformers and inductors. The International Renewable Energy Agency (IRENA) policies support this growth, with renewable energy project investments creating expanding application scope for coil winding equipment.

Restraint - Raw Material Cost Volatility and Supply Chain Constraints

The electrical coil windings market faces significant challenges from fluctuating copper and aluminum prices, which directly impact production costs and profit margins. Copper price volatility has historically created pricing pressure, making cost-effective alternatives like aluminum windings increasingly attractive despite performance trade-offs.

Supply chain disruptions, particularly affecting specialized insulation materials and advanced conductor alloys, create operational challenges for manufacturers. Additionally, stringent environmental regulations regarding material usage and waste disposal are influencing the adoption of more sustainable winding techniques, requiring investments in new production processes and compliance systems.

High Capital Investment and Technical Complexity

The transition to advanced coil winding technologies requires substantial capital investments that can be prohibitive for small and medium enterprises. SMEs often have restricted financial resources, making it challenging to allocate significant budgets to capital-intensive equipment.

Rapid technological advancements create concerns about equipment obsolescence, increasing financial risk for manufacturers. The complex manufacturing processes involved in high-performance coil windings require specialized technical expertise and training, creating barriers to market entry and expansion.

Opportunities - Electric Grid Modernization and Smart Infrastructure

The global emphasis on power grid modernization presents substantial opportunities for electrical coil windings manufacturers. Utilities worldwide are expanding transmission and distribution networks while upgrading aging infrastructure, creating demand for advanced transformers and electrical components.

Smart grid implementations require sophisticated coil winding solutions capable of handling variable loads and enhanced monitoring capabilities. Emerging markets experiencing rapid urbanization and industrialization represent particularly attractive growth opportunities, with countries like India and China making significant investments in power distribution networks.

5G Infrastructure and Telecommunications Growth

The global rollout of 5G networks is creating significant demand for high-frequency coils requiring specialized winding techniques and equipment. 5G infrastructure deployment necessitates advanced electromagnetic components with precise performance characteristics.

This technological transition is driving innovation in coil winding technology and creating opportunities for manufacturers who can meet the stringent requirements of telecommunications applications. The expansion of IoT devices and smart city initiatives further amplifies demand for sophisticated coil winding solutions.

Category-wise Analysis

Material Type Insights

Copper winding dominates the market with a 61% share, valued at about USD 3.3 billion in 2025, driven by its superior electrical conductivity (100% IACS vs. aluminum’s 61%), excellent heat dissipation, and long-term reliability.

Its strong oxidation resistance minimizes corrosion, making it the preferred choice for precision motors, advanced transformers, and critical power systems. In automotive applications, especially electric vehicles, copper’s efficiency and durability outweigh higher material costs.

However, aluminum winding is emerging as the fastest-growing segment, offering 15-25% cost savings and significant weight reduction. These advantages make aluminum increasingly attractive for high-power transformers and cost-sensitive applications, where material expenses account for a major share of total production costs.

Application Insights

The motors segment holds a dominant 52% share, valued at approximately USD 2.8 billion in 2025, underscoring the widespread use of electric motors in industrial automation, automotive systems, and consumer electronics.

Growth is primarily fueled by electric vehicle production, as each EV incorporates multiple precision-wound motors for propulsion, thermal management, and auxiliary functions. Rising industrial automation further drives demand for servo, stepper, and variable-speed motors, supported by efficiency standard upgrades and retrofitting initiatives.

In contrast, the transformer segment is the fastest-growing application area, propelled by global grid modernization, renewable energy integration, and smart grid deployments. Expanding wind and solar installations, along with emerging market infrastructure and EV charging network development, continue to strengthen transformer demand.

End-user Analysis

The industrial sector leads the market with a 42.3% share, driven by the extensive use of electrical coil windings in manufacturing machinery, process automation, and material handling systems. Industry 4.0 adoption is accelerating demand for precision motors and actuators within automated production environments.

Continuous investments in efficiency enhancement and advanced automation technologies further strengthen this segment. Industrial applications require high-reliability winding systems capable of sustaining performance in harsh operating conditions with minimal maintenance.

The power and utilities sector is the fastest-growing end-user segment, supported by large-scale infrastructure modernization and renewable energy expansion. Clean energy initiatives, grid upgrades, and rapid electrification in emerging economies are fueling demand for advanced transformers and high-performance coil winding solutions.

Regional Market Insights

North America Electrical Coil Windings Market Trends

North America represents approximately 25% of the global market share with a projected CAGR of 5.5% through 2032. The United States dominates the regional market with an estimated 72.4% market share in 2024, valued at approximately $1.35 billion.

The region's leadership position stems from advanced automotive manufacturing capabilities, particularly in electric vehicle production and supporting infrastructure development. Major automotive OEMs and Tier 1 suppliers are driving demand for precision coil winding solutions to support EV motor production scaling.

The regulatory framework emphasizing energy efficiency and environmental protection creates favorable conditions for high-performance winding technologies. Government incentives promoting electric vehicle adoption and renewable energy projects are generating substantial market opportunities.

The region's strong focus on technological innovation, supported by significant R&D investments from both private companies and government agencies, positions North America as a leader in advanced winding technologies including superconducting coils and high-voltage applications.

Europe Electrical Coil Windings Market Trends

Europe accounts for approximately 20% of global market share with a projected CAGR of 5.8% through 2032. The region's growth is driven by stringent environmental regulations promoting energy efficiency and the aggressive transition toward renewable energy sources.

Germany, France, and the United Kingdom lead regional demand, with Germany particularly strong in automotive applications and industrial automation. The European Union's regulatory harmonization creates consistent standards across member states, facilitating market access and technology transfer.

European automotive manufacturers are investing heavily in electric vehicle production capabilities, creating substantial demand for precision motor windings and charging infrastructure components. The region's emphasis on reducing carbon emissions and promoting green energy is driving investments in wind power installations and smart grid technologies.

Industrial automation initiatives, particularly in Germany's manufacturing sector, are generating demand for high-precision coil winding solutions in robotics and process automation applications.

Asia Pacific Electrical Coil Windings Market Trends

Asia Pacific dominates the global market with approximately 40-45% market share and represents the fastest-growing region. China emerges as the key player with a 56.9% regional market share in 2024, driven by massive infrastructure investments and the world's largest electric vehicle market. The region benefits from cost-effective manufacturing capabilities, established supply chains, and growing domestic consumption of electrical equipment.

The region's rapid industrialization and urbanization are creating substantial demand for power generation and distribution infrastructure. Countries like India are making significant investments in renewable energy projects, with targets of 175 GW of renewable capacity creating demand for transformers and motor applications.

Japan and South Korea contribute significantly through advanced electronics manufacturing and automotive production, particularly in hybrid and electric vehicle technologies.

Competitive Landscape

The global electrical coil windings market exhibits a moderately concentrated structure with the top 5 players holding more than 70% market share.

Leading companies include Sumitomo Electric, Furukawa Electric, Superior Essex, LS Cable & System, and Nexans, each maintaining significant global presence through strategic manufacturing locations and distribution networks. The competitive landscape balances established multinational corporations with specialized regional players serving niche applications and local markets.

In pursuit of market growth, these companies actively engage in strategic collaborations, initiate product launches, and pursue acquisitions, all while implementing targeted marketing strategies. This multifaceted approach not only drives market expansion but also enables manufacturers to adapt their offerings to align with evolving consumer preferences, ultimately increasing sales and market share.

Recent Industry Developments

- In April 2024, Superior Essex and Furukawa Electric completed divestiture of their heavy magnet wire joint venture in April 2024, with Superior Essex becoming sole owner of facilities in Japan and Malaysia. This strategic realignment allows both companies to focus on core competencies while maintaining collaboration in high-performance winding wire technologies.

- In 2024, Essex Furukawa launched High Voltage Winding Wire (HVWW) technology for European electric vehicle markets, targeting increased motor output and efficiency while reducing assembly complexity.

Companies Covered in Electrical Coil Windings Market

- Stonite Coil Corporation

- Classic Coil Company Inc.

- APW Company

- Miles Platts Limited

- R Baker (Electrical) Ltd.

- National Electric Coil Inc.

- Selco Co. Ltd.

- Quartzelec Ltd.

- Sag Harbor Industries Inc.

- IK Electric Co., Ltd.

- North Devon Electronics

- Everson Tesla Inc.

- AGW Electronics Ltd.

- Stimple & Ward Co.

- Other Market Players

Frequently Asked Questions

The Electrical Coil Windings market is estimated to be valued at US$ 5.4 Bn in 2025.

The key demand driver for the Electrical Coil Windings market is the accelerating electrification across industrial, transportation, and energy sectors, fueled by the global shift toward energy efficiency and renewable integration.

In 2025, the Asia Pacifc region will dominate the market with an exceeding 40% revenue share in the global Electrical Coil Windings market.

Among the End-user, Industrial hold the highest preference, capturing beyond 42.3% of the market revenue share in 2025, surpassing other End-user.

The key players in the Electrical Coil Windings market are Stonite Coil Corporation, Classic Coil Company Inc., APW Company and Miles Platts Limited.