- Metals & Minerals

- Electrical Steel Market

Electrical Steel Market Size, Share, and Growth Forecast 2025 - 2032

Electrical Steel Market by Product Type (CRNO (Cold Rolled Non-Oriented, CRGO (Cold Rolled Grain-Oriented), End Product (Transformers, Generators, Alternators), End-use (Energy and Power Generation, Automotive, Industrial Automation), and Regional Analysis 2025 - 2032

Electric Steel Market Share and Trends Analysis

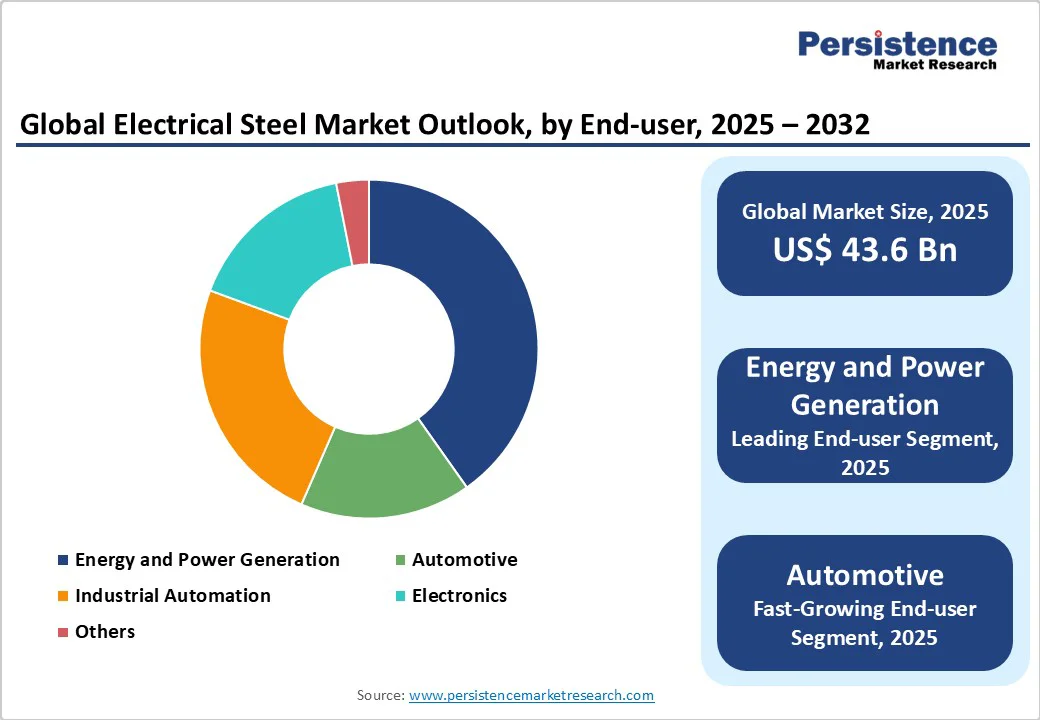

The global Electrical Steel Market size was valued at US$43.6 Bn in 2025 and is projected to reach US$73.3 Bn by 2032, growing at a CAGR of 7.7% between 2025 and 2032. This growth is driven by electrification trends, including EV adoption requiring high-performance traction motors, grid modernization with energy-efficient transformers, and renewable energy integration demanding advanced power conversion infrastructure.

Key Market Highlights

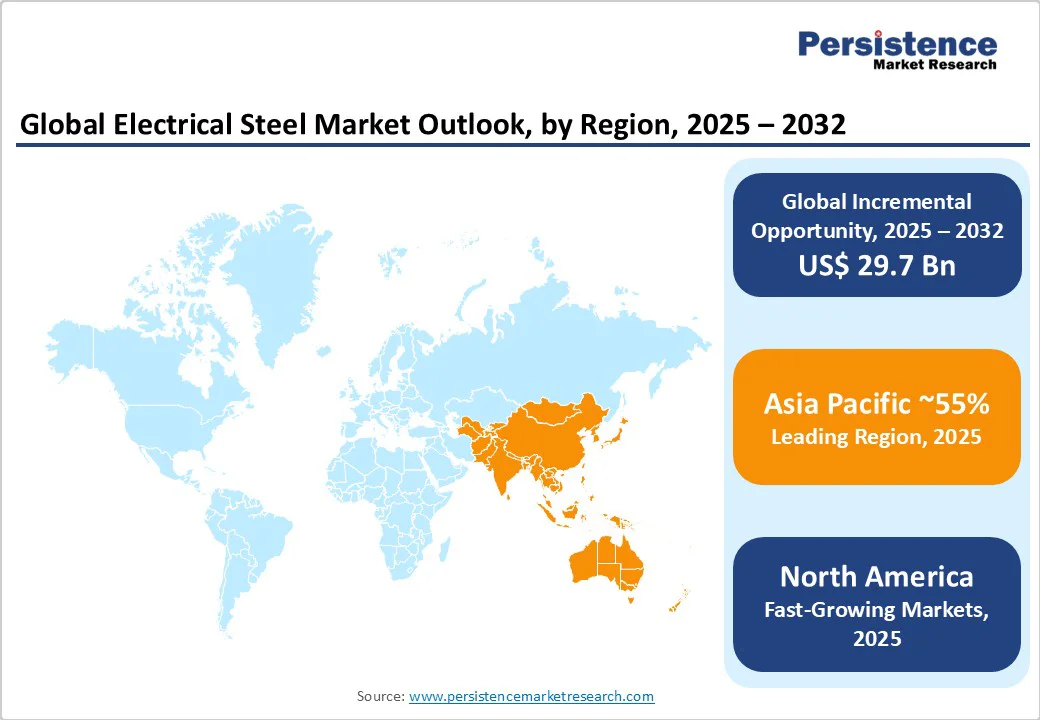

- Asia Pacific leads global electrical steel with a 55% market share in 2025.

- China's production and consumption, with China accounting for 72% of non-grain-oriented and 56% of grain-oriented electrical steel output, dominate the regional production and demand.

- North America emerges as the fastest-growing regional market, driven by substantial federal infrastructure investments, aggressive electric vehicle adoption policies, and strategic capacity expansions, including ArcelorMittal's $1.2 billion Alabama facility, which targets 150,000 metric tons of annual electrical steel production to serve automotive and renewable energy applications, leveraging domestic supply chain advantages.

- Cold Rolled Non-Oriented (CRNO) steel maintains market dominance with approximately 70% revenue share in 2025, reflecting versatile magnetic properties, cost-effectiveness for rotating machinery applications, and established supply relationships across industrial motors, generators, automotive components, and HVAC systems requiring consistent performance and competitive pricing.

- EV Motors represent the fastest-growing end product segment with 9.6% CAGR from 2025-2032, driven by global automotive electrification trends, OEM platform refresh cycles demanding ultra-thin electrical steel laminations, and requirements for high-performance materials optimized for traction motor efficiency and thermal management in next-generation electric vehicles.

- Smart grid development and renewable energy integration create substantial market opportunities as utilities invest in advanced transformer technologies that require premium CRGO grades with enhanced magnetic properties, reduced energy dissipation characteristics, and superior performance under variable loading conditions, all of which are essential for modern electrical infrastructure supporting decarbonization objectives.

| Key Insights | Details |

|---|---|

|

Electrical Steel Market Size (2025E) |

US$ 43.6 Bn |

|

Market Value Forecast (2032F) |

US$73.3 Bn |

|

Projected Growth CAGR (2025-2032) |

7.7% |

|

Historical Market Growth (2019-2024) |

12.7% |

Market Dynamics

Market Growth Drivers

Accelerating Electric Vehicle Adoption and Advanced Motor Technologies

The global automotive shift toward electrification is the strongest growth driver for electrical steel, as the EV market expands rapidly due to stringent emissions regulations, incentives, and advancements in battery technologies. Electric vehicles require specialized non-grain-oriented electrical steel (NOES) for traction motors, with premium platforms demanding ultra-thin laminations of 0.1–0.25?mm to achieve high-frequency efficiency above 10,000?RPM. The EV hub motor segment is projected to grow at a 14.1% CAGR through 2031, driven by the optimization of power density and thermal management needs.

Advanced motor designs, including permanent magnet and induction architectures, rely on steel with enhanced magnetic properties, reduced core losses, and dimensional stability. Expansion of the E-bike and permanent magnet motor markets further increases demand. OEMs are localizing their supply chains and forming long-term partnerships with producers to deliver consistent material quality. Emerging 800V architectures and integrated e-axles intensify requirements for high-performance electrical steel with superior insulation and magnetic stability.

Renewable Energy Infrastructure Expansion and Grid Modernization Imperatives

The global shift to renewable energy is driving sustained demand for high-grade grain-oriented electrical steel (GOES) in transformers, distribution equipment, and synchronous generators, which are essential for integrating variable generation into existing grids. The IEA projects that renewable capacity will nearly double from 2024 to 2030, with wind and solar installations requiring 50-200 tons and 35-45 tons of steel per megawatt, respectively. Smart grid modernization and the deployment of advanced transformers increase the demand for ultra-low-loss GOES to reduce energy dissipation and improve efficiency.

Expanding synchronous generator installations in hybrid renewable and grid-stabilization projects require steel that maintains magnetic performance under variable conditions. Utilities replacing aging transformers, along with data center growth and industrial electrification, further support premium electrical steel demand. Offshore wind and large-scale solar interconnections drive the need for specialized high-voltage transmission applications, necessitating materials that ensure stability under dynamic load conditions.

Market Restraints

Raw Material Cost Volatility and Supply Chain Vulnerabilities

The electrical steel industry faces ongoing challenges from volatile raw material prices, including iron ore, silicon, aluminum, and energy, making manufacturers sensitive to commodity fluctuations and geopolitical supply disruptions. Producing grain-oriented electrical steel involves energy-intensive heat treatment, secondary recrystallization, and precision coating, adding operational complexity and exposure to variations in energy costs. With fewer than 20 mills worldwide capable of ultra-low-loss GOES production, supply concentration creates pricing power for established producers while limiting customer negotiation flexibility.

Global supply chain disruptions, such as pandemic logistics challenges and geopolitical tensions, further expose vulnerabilities. Trade disputes, anti-dumping duties, and domestic content requirements in key markets introduce additional uncertainty, complicating efforts to secure reliable, cost-effective electrical steel supply for critical power generation, automotive, and industrial applications.

Technology Transition Challenges and Capital Investment Requirements

The electrical steel industry faces significant challenges in adopting advanced grades and sustainable production methods, as manufacturers must invest heavily to produce thinner gauges, improved coatings, and enhanced magnetic properties for next-generation applications. Transitioning to amorphous metal cores, which reduce core losses by 70–80% compared to conventional CRGO, is hindered by higher costs, handling complexities, and design adaptation barriers.

Environmental regulations and decarbonization mandates further pressure producers to implement cleaner technologies, such as electric arc furnace (EAF) and direct reduced iron (DRI) processes, which require substantial capital and operational expertise, and may potentially impact short-term output and costs. Producing ultra-thin steel with consistent magnetic and dimensional properties remains a technically complex task, necessitating continuous investment in process control, quality assurance, and workforce training to maintain competitiveness in an evolving market.

Market Opportunities

Advanced Electric Vehicle Powertrains and Micromobility Solutions

The automotive shift toward high-performance electric powertrains is driving strong demand for ultra-thin, low-loss electrical steel optimized for high-frequency motors and advanced thermal management. Next-generation EVs with 800V architectures, silicon carbide inverters, and integrated e-axle systems require steel with enhanced insulation, reduced magnetostriction, and dimensional stability under extreme conditions.

Growth in E-bike motors and micro mobility further expands demand for compact, lightweight steel that improves efficiency and range. OEM focus on vertical integration and localized supply chains creates opportunities for regional producers to supply tailored materials. Emerging applications such as wireless EV charging and autonomous vehicle systems also require advanced electrical steel with high-frequency performance and electromagnetic compatibility, highlighting the material’s critical role in next-generation mobility solutions.

Smart Grid Technologies and Energy Storage Integration

The global rollout of smart grid infrastructure and energy storage systems presents significant opportunities for electrical steel suppliers supporting advanced power distribution and conversion technologies. Solid-state transformers, offering up to 20% higher efficiency and bidirectional power flow for grid-scale storage, require specialized steel optimized for high-frequency operation and compact design.

Renewable energy integration demands power electronics and conversion equipment with premium electrical steel to handle variable loads and maintain power quality. Smart grid modernization in developed economies emphasizes energy efficiency and digitalization, driving demand for high-performance steel in distribution transformers, voltage regulators, and power factor correction systems. Additionally, the growth of data centers and cloud computing facilities increases demand for specialized transformers and distribution equipment using electrical steel engineered for efficiency, reduced losses, and lower environmental impact.

Category-wise Insights

Product Type Analysis - Cold Rolled Non-Oriented Steel Maintains Market Leadership Through Versatile Applications

Cold Rolled Non-Oriented steel accounts for approximately 70% of global electrical steel revenue in 2025, driven by its suitability for rotating machinery where magnetic flux varies in multiple directions and cost efficiency is essential. Its isotropic properties ensure uniform performance in electric motors, generators, alternators, and automotive components. CRNO production avoids the complex grain-orientation processes of GOES, enabling higher volumes and attractive unit economics for industrial automation, HVAC, and consumer appliances.

Strong supply relationships and established qualification histories accelerate adoption in new applications. Leading producers like POSCO, with over 1 million tons of annual electrical steel output including NOES, offer diverse thicknesses, coatings, and grades. The electric vehicle market further reinforces CRNO demand, as traction motors require thin-gauge laminations with advanced insulation and enhanced magnetic properties to meet efficiency and thermal performance targets under high-frequency operation.

End Product Analysis - Industrial Motors Dominate Market Share Through Broad Application Spectrum and Replacement Cycles

The Industrial Motors segment holds a leading position with approximately 35% of the global electrical steel market in 2025, driven by its widespread use across manufacturing, building services, infrastructure, and process industries. Electric motors are essential for converting electrical energy to mechanical work in applications ranging from heavy machinery and material handling to precision automation.

Demand is fueled by predictable replacement cycles, energy-efficiency upgrades, and the adoption of variable frequency drives (VFDs) requiring high-performance NOES laminations with low core loss and stable magnetic properties. Growth is further supported by global industrial automation, Industry 4.0 adoption, and factory modernization initiatives. Rapid industrialization in emerging economies expands opportunities for motors using premium electrical steel, enhancing reliability, reducing maintenance, and improving operational efficiency in demanding industrial environments.

End Use Analysis - Energy and Power Generation Segment Leads Through Infrastructure Investment and Grid Modernization

The Energy and Power Generation segment is the largest end-use market for electrical steel, accounting for approximately 40% of global share in 2025. Its growth is driven by ongoing investments in power generation, transmission expansion, and distribution upgrades that support electrification and economic development. Electrical steel is critical in transformer cores, generator rotors, and power conversion equipment, where energy efficiency impacts both system costs and environmental performance.

Grain-oriented steel dominates applications in power and distribution transformers, supported by long equipment lifecycles, regulatory efficiency mandates, and utility CAPEX programs. Renewable energy integration, smart grid deployment, and substation modernization further increase demand for premium GOES materials with advanced magnetic properties. China Baowu Steel Group leads this segment with a 33% global share in GOES, highlighting the scale and strategic importance of electrical steel in enabling reliable, high-efficiency power infrastructure worldwide.

Regional Insights

North America Electrical Steel Market Trends

Infrastructure Modernization and Electrification Policies Drive Market Leadership

North America’s electrical steel market is expanding rapidly, supported by infrastructure modernization, electric vehicle adoption, and supply chain localization to reduce import reliance. Federal initiatives like the Infrastructure Investment and Jobs Act and Inflation Reduction Act are fueling investments in grid upgrades, renewable integration, and EV infrastructure, driving sustained demand for high-performance CRGO and NOES materials.

Regional utilities are advancing grid hardening, smart grid deployment, and transmission expansion, requiring premium transformer-grade steel. The automotive sector’s push toward electrification, aiming for all-electric fleets by 2030–2035, further boosts domestic steel demand. ArcelorMittal’s US$1.2 billion Calvert, Alabama project, the largest in North American history, will add 150,000 TPA of NOES for EV and renewable applications. Additionally, renewable energy expansion and data center growth intensify demand for ultra-low-loss GOES in transformers and power distribution systems.

Europe Electrical Steel Market Trends

Regulatory Harmonization and Sustainability Mandates Shape Market Development

Europe’s electrical steel market is shaped by strict regulatory frameworks that emphasize energy efficiency, sustainability, and supply chain resilience across key economies, including Germany, the U.K., France, Spain, and emerging Eastern European countries. The EcoDesign Regulation enforces transformer and motor efficiency standards requiring premium low-core-loss steels, while EU anti-dumping duties on GOES imports from China, Japan, South Korea, Russia, and the U.S. safeguard domestic capacity.

Automotive electrification drives demand for ultra-thin electrical steel laminations, exemplified by BMW’s use of voestalpine materials at its Steyr facility, highlighting Europe’s expertise in precision lamination and advanced coatings. Sustainability policies and decarbonization goals accelerate adoption of advanced transformer technologies and renewable integration. Tata Steel Nederland’s transition to DRI–EAF production reinforces green steel initiatives, as regional manufacturers innovate in insulation coatings, magnetostriction control, and OEM collaboration to support next-generation e-mobility and grid modernization.

Asia Pacific Electrical Steel Market Trends

Manufacturing Scale and Technology Leadership Drive Global Market Dominance

Asia Pacific is the world’s largest and fastest-growing electrical steel market, led by China, which accounts for about 72% of global non-grain-oriented and 56% of grain-oriented electrical steel output. The region is estimated to hold 55% market share in 2025. Backed by integrated manufacturing ecosystems and strong industrial policy, China’s capacity is projected to rise from 16.67 million tons in 2023 to 18-20 million tons by 2026, driven by electric vehicle, renewable energy, and industrial modernization initiatives.

India is emerging as a key growth hub, with JSW Steel and JFE Steel investing US$669 million to establish 350,000 TPA of grain-oriented electrical steel capacity at Vijayanagar and Nashik, supporting its expanding power infrastructure and automation sectors. Japan’s leadership in high-performance grades for EV traction motors and ASEAN’s accelerating industrialization further strengthen regional demand, supported by integrated supply chains and cost-competitive manufacturing capabilities.

Competitive Landscape

The global electrical steel market is moderately concentrated, dominated by major producers leveraging advanced technology, integrated production, and strategic regional presence, while numerous local players cater to niche applications. Competition focuses on high-quality CRGO grades, with only about 20 mills worldwide capable of producing ultra-low-loss materials that meet stringent automotive and power generation standards.

Leading firms pursue vertical integration to control costs and ensure quality, investing heavily in R&D for thinner gauges, superior coatings, and enhanced magnetic performance tailored to EVs and smart grid systems. Increasing collaboration between steelmakers and automakers through long-term supply agreements supports joint innovation in specialized materials. Industry leaders such as ArcelorMittal, China Baowu, POSCO, and Nippon Steel differentiate via proprietary technologies, global reach, and strong OEM partnerships, while new models emphasize localized finishing, digital quality systems, and optimized logistics.

Key Market Developments:

- In February 2025, ArcelorMittal announced a US$1.2 billion investment to build a non-grain-oriented electrical steel (NOES) plant in Calvert, Alabama, targeting 150,000 metric tons per year of output.

- In August 2025, JSW Steel and JFE Steel revealed a joint investment of ?5,845 crore (approx. US$669 million) to expand grain-oriented electrical steel capacity across Nashik and Vijayanagar, aiming to raise total output to 350,000 TPA.

- In June 2025, Nippon Steel finalized its acquisition of U.S. Steel for US$14.9 billion, completing the transaction under agreed national security safeguards.

Companies Covered in Electrical Steel Market

- ArcelorMittal

- China Baowu

- Steel Group Corporation

- POSCO

- Nippon Steel Corporation,

- Voestalpine AG

- Jindal Steel and Power,

- JFE Steel Corporation

- Tata Steel Limited

- NLMK Group

- SAIL (Steel Authority of India)

- Essar Steel

- MMK (Magnitogorsk Iron and Steel Works)

- Hyundai Steel

- Maithan Steel

- Sunflag Iron and Steel

Frequently Asked Questions

The global electrical steel market was valued at US$ 43.6 billion in 2025 and is projected to reach US$ 73.3 billion by 2032, representing a compound annual growth rate of 7.7% during the forecast period.

Key drivers include accelerating electric vehicle adoption requiring specialized traction motor materials, renewable energy infrastructure expansion necessitating high-performance transformer cores, smart grid modernization demanding advanced electrical components, and industrial automation requiring efficient motor technologies with superior magnetic properties.

Cold Rolled Non-Oriented (CRNO) steel dominates with approximately 70% market share by revenue in 2025, driven by versatile magnetic properties suitable for rotating machinery applications, cost-effectiveness for volume applications, and established supply relationships across industrial motor and automotive component manufacturers.

Asia Pacific leads global production and consumption with China accounting for 72% of non-grain-oriented electrical steel output, while North America shows the fastest growth driven by infrastructure investments, electric vehicle policies, and strategic capacity expansions including major manufacturing facility developments.

EV motor applications present exceptional growth potential as the fastest-growing end product segment at 9.6% CAGR, requiring ultra-thin, low-loss electrical steel materials optimized for high-frequency traction motors, while smart grid infrastructure creates sustained demand for premium transformer core materials with enhanced efficiency characteristics.