- Biotechnology

- Nano Healthcare Technology for Medical Equipment Market

Nano Healthcare Technology for Medical Equipment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Nano Healthcare Technology for Medical Equipment Market by Product (Implantable Devices, Dental Filling Materials, Medical Textile and Wound Dressing, Others), by Application (Dentistry, Orthopedics, Hearing Loss, Wound Care, Others), End-user (Hospitals, Clinics, and Others), and Regional Analysis, from 2026 to 2033

Nano Healthcare Technology for Medical Equipment Market Share and Trends Analysis

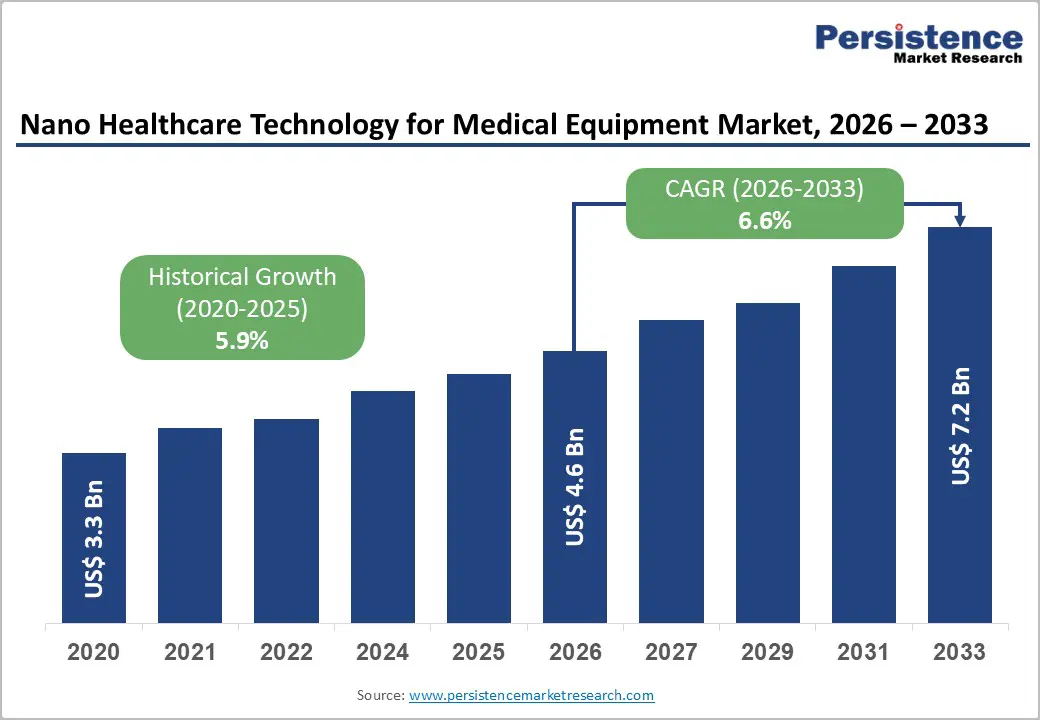

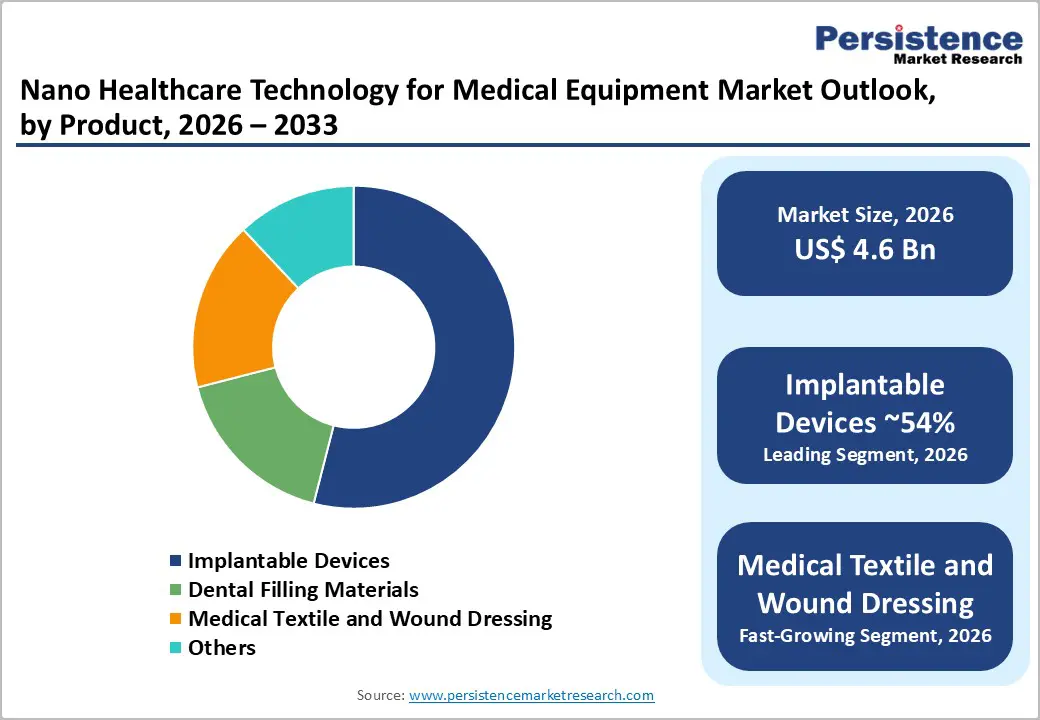

The global nano healthcare technology for medical equipment market size is likely to be valued at US$ 4.6 billion in 2026 to US$ 7.2 billion by 2033, growing at a CAGR of 6.6% during the forecast period from 2026 to 2033.

The healthcare industry has been undergoing various transformations over the past few years. Nano technology in healthcare is one such reform that is expected to enhance the efficacy of various healthcare platforms and offer significant opportunities to transform the field of healthcare with respect to diagnosis, treatment, and prevention of various diseases. Biochips, implantable materials, and active implantable devices are among the products used in the healthcare sector. Nano healthcare technology can improve disease diagnosis by incorporating it in monitoring devices, bioassays, and imaging.

Key Industry Highlights:

- Leading Region: North America has the largest market share, supported by strong R&D capacity, high adoption of nano-engineered implants, and a well-established regulatory and clinical infrastructure.

- Fastest Growing Region: Asia Pacific is expanding at the fastest pace due to rising surgical volumes, strengthened manufacturing ecosystems, and increasing government support for nanotechnology-enabled medical devices.

- Dominant Segment: Implantable devices lead the market with the highest share in 2025, driven by widespread use of nano-coatings and engineered surfaces that improve osseointegration, durability, and infection resistance.

- Fastest Growing Segment: Orthopedics represents the fastest-growing application area as demand rises for nano-enhanced joint replacements, trauma fixation systems, spinal implants, and regenerative solutions.

| Key Insights | Details |

|---|---|

| Nano Healthcare Technology for Medical Equipment Market Size (2026E) | US$ 4.6 Bn |

| Market Value Forecast (2033F) | US$ 7.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Dynamics

Driver - Rising Burden of Musculoskeletal and Degenerative Disorders

The rapid increase in musculoskeletal disorders such as osteoarthritis, osteoporosis, and trauma-related fractures is shaping demand for advanced orthopedic solutions built at the nanoscale. With ageing populations and lifestyle changes, a large share of adults now experiences chronic joint damage or bone degeneration that limits mobility and quality of life. Health agencies, including the World Health Organization, highlight musculoskeletal diseases as one of the leading contributors to disability worldwide. As a result, healthcare providers are increasingly prioritizing implants that promise stronger bone integration, improved durability, and minimal long-term complications.

Nano-enabled orthopedic and implantable devices address these exact needs by providing surfaces that promote better bone cell adhesion, reduce microbial colonization, and minimize wear from repeated motion. Enhanced osseointegration and improved material strength can help lower the rate of revision surgeries, thereby reducing the economic burden on hospitals and insurers. The shift toward personalized and regenerative orthopedic solutions further supports the uptake of nano-engineered materials. These developments align with ongoing advancements across the orthopedic devices market, where manufacturers continue to invest in nanocoatings, biologically active surfaces, and engineered biomaterials to meet patient expectations for long-lasting and reliable implants.

Restraints - Regulatory and safety uncertainties around nano-enabled devices

Despite the strong clinical promise of nano-engineered orthopedic implants, regulatory pathways remain challenging. Agencies such as the U.S. FDA, the EMA, and regional Asian regulators are still developing detailed guidelines for the use of nanotechnology in medical devices. As a result, companies must complete extensive testing to prove that nanoparticles or nano-modified surfaces are safe, stable, and do not migrate or accumulate in tissues over long periods. This includes assessments of toxicity, biocompatibility, and environmental impact, often adding years of evaluation before market approval.

The tightening of rules under frameworks such as the EU Medical Device Regulation further increases the evidence burden, leading to higher costs for data generation, quality control, and post-market surveillance. Variations in classification criteria across different geographies complicate global product launches, especially for mid-sized manufacturers without large compliance teams. These uncertainties delay commercialization timelines and may discourage smaller innovators from investing aggressively in nano-based orthopedic technologies.

Opportunity - Expansion of Nano-Engineered Orthopedic and Spinal Implants

Nanotechnology is opening new avenues for growth in orthopedic and spinal implant markets, where performance, longevity, and patient outcomes are key differentiators. Manufacturers are increasingly designing implants with nano-textured titanium, advanced ceramic coatings, and antimicrobial nanosurfaces to enhance bone bonding and reduce wear and infection rates. These improvements directly address common causes of implant failure, such as loosening, inflammation, and microbial contamination, giving companies the opportunity to position nano-optimized products as premium, high-value offerings.

As minimally invasive and robotic-assisted surgeries become mainstream, surgeons are seeking implants that provide superior mechanical stability and faster biological integration, particularly for younger patients who require longer-lasting solutions. This shift supports the adoption of nanoscale engineering in joint replacements, spinal fixation systems, and trauma devices. Collaborations between orthopedic firms, including major players such as Stryker and Zimmer Biomet, and research institutes are accelerating the development of next-generation implants with regenerative and bioactive features. These partnerships offer opportunities to expand product portfolios, enter higher-margin segments, and strengthen competitive advantage in a market increasingly shaped by nanoscale innovation.

Category-wise Analysis

By Product Insights

Implantable devices remain the largest product category in the nano healthcare technology for medical equipment market, capturing an estimated 54% share in 2025. Their dominance is supported by the expanding use of nano-engineered surfaces and coatings across orthopedic, cardiovascular, and neuromodulation implants. These nanoscale modifications help improve tissue integration, reduce microbial attachment, and enhance durability, which are critical factors influencing implant performance and patient outcomes. Hospitals and surgical centers increasingly prefer implants that can lower revision rates and extend functional lifespan, especially as surgical volumes rise among ageing populations.

Peer-reviewed research has consistently demonstrated the benefits of nanostructured materials in promoting osteoblast activity, improving bone anchoring, and delivering better long-term success in procedures such as joint replacement and spinal fusion. As a result, manufacturers including Stryker, Zimmer Biomet, Boston Scientific, and others are upgrading their implant portfolios with advanced nano-coatings and engineered biomaterials. This sustained investment supports the continued leadership of implantable devices across the product landscape.

By Application Insights

Orthopedics represents the largest application segment in the nano healthcare technology for medical equipment market, accounting for roughly 32% of the total share in 2025. Demand is driven by the rising prevalence of osteoarthritis, degenerative spine disorders, sports-related injuries, and age-associated fractures, all of which require durable and biologically compatible implants. Nanotechnology plays a central role in addressing these clinical needs by improving properties such as wear resistance, osseointegration, and corrosion protection in joint replacement components, plates, screws, and spinal fixation systems.

Surgeons and healthcare providers increasingly recognize the value of nano-modified orthopedic devices in reducing complication rates and supporting quicker rehabilitation. Advancements in nano-enhanced arthroscopy tools, bioactive coatings, and regenerative bone graft substitutes are expanding the scope of applications, enabling more targeted and effective surgical interventions. These innovations align with the shift toward minimally invasive and high-precision orthopedic procedures, strengthening the segment’s position as a key contributor to revenue growth within the broader nano-enabled medical equipment market.

Region-wise Insights

North America Nano Healthcare Technology for Medical Equipment Market Trends

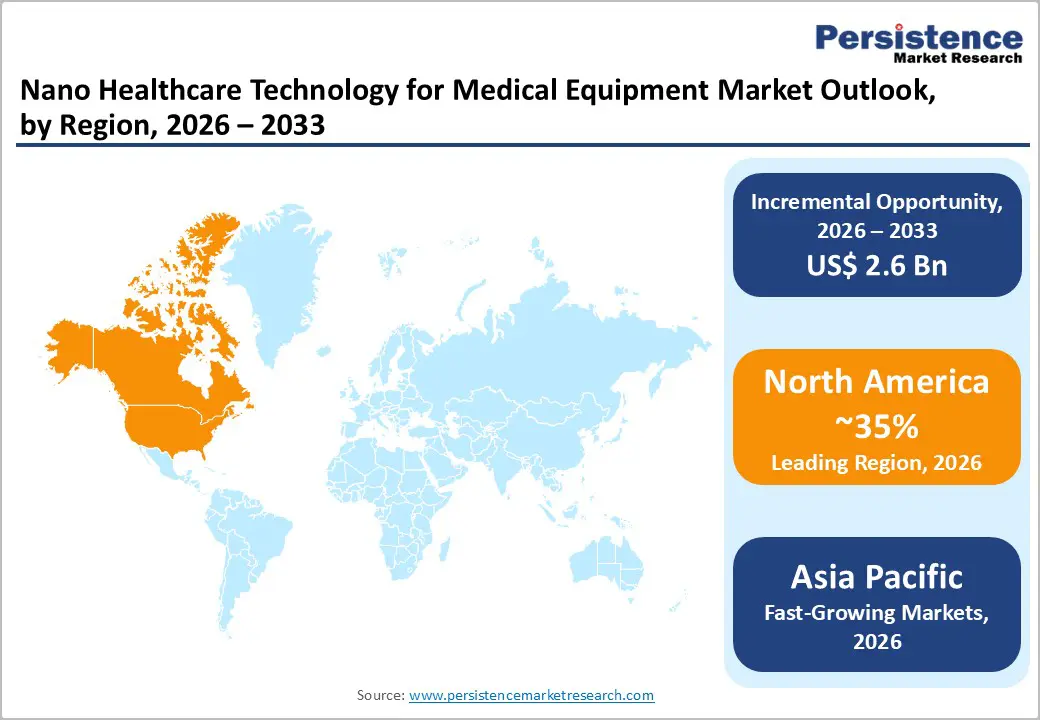

North America commands around 35% of the nano healthcare technology for medical equipment market in 2025, supported by strong clinical adoption and one of the most advanced innovation ecosystems worldwide. The U.S. drives most of the regional demand due to high utilization of nano-engineered orthopedic implants, cardiovascular devices, and advanced wound management products. Large surgical volumes established reimbursement frameworks, and strong participation from academic medical centers encourages early evaluation and integration of nanoscale coatings, engineered surfaces, and bioactive materials into routine care. The U.S. FDA continues to refine guidance for emerging materials and surface-modified devices, helping manufacturers bring new products to market while maintaining rigorous safety and performance expectations.

Federal research funding and longstanding industry-university partnerships enable steady progress in nanomaterials, regenerative technologies, and precision-engineered implant surfaces. Companies such as Stryker, Abbott, 3M, and Boston Scientific play central roles in shaping product development across the region. In Canada, growing investments in biomaterials research clusters and orthopedic innovation further support market expansion, particularly for implants and wound care devices incorporating nanoscale enhancements.

Asia Pacific Nano Healthcare Technology for Medical Equipment Market Trends

Asia Pacific is establishing itself as the fastest-growing region for nano healthcare technology in medical equipment, supported by rapid improvements in healthcare capacity and expanding domestic manufacturing capabilities across China, Japan, India, and ASEAN countries. Rising rates of osteoporosis, trauma-related injuries, diabetes, and chronic wounds are increasing the need for advanced orthopedic implants, dental materials, and high-performance wound dressings incorporating nanoscale features. Many governments are modernizing regulatory frameworks to encourage innovation, with China and Japan introducing accelerated pathways for priority medical devices while preserving safety requirements.

China has emerged as a major hub for producing orthopedic implants, nanosurface-enhanced biomaterials, and wound management products through a combination of domestic companies and international partnerships. Japan’s expertise in precision engineering and materials science supports the development of specialized nanocoatings and high-reliability implant designs. India and ASEAN nations continue to build specialized orthopedic and wound care centers that rely on advanced dressings and implant technologies. Competitive manufacturing costs and rising export strength further position the Asia Pacific as an essential production and innovation base for global medtech companies adopting nanotechnology.

Competitive Landscape

The competitive landscape of the global nano healthcare technology for medical equipment market is shaped by a mix of established medtech leaders and specialized material science companies advancing nanoscale innovations. Major players such as Stryker, Boston Scientific, Abbott Laboratories, and 3M integrate nanocoatings, engineered surfaces, and advanced biomaterials across orthopedic, cardiovascular, and wound care portfolios. These firms invest heavily in R&D, regulatory compliance, and clinical validation to strengthen product performance and maintain a competitive advantage. Alongside them, emerging companies and university-linked startups contribute innovations in nanostructured implants, antimicrobial surfaces, and regenerative technologies. Strategic collaborations, licensing agreements, and joint research programs are common as manufacturers seek to expand capabilities, accelerate commercialization, and secure higher-value positions within the evolving nano-enabled medical equipment market.

Key Industry Developments:

- In February 2024, researchers at the University of Illinois Urbana-Champaign created a silicon-based device built using microelectronics fabrication methods. This next-generation nanoscale sensor can monitor brain areas up to 1,000 times smaller than earlier technologies and identify minute shifts in chemical composition.

- In January 2023, HERAEUS MEDEVIO partnered with LipoCoat to integrate biomimetic coating technology into medical devices. LipoCoat, a spin-off from the University of Twente in the Netherlands, focuses on developing bio-inspired surface coatings designed to improve the safety, comfort, and overall performance of medical devices.

Companies Covered in Nano Healthcare Technology for Medical Equipment Market

- 3M Company

- Zimmer Biomet

- Stryker

- Starkey

- Smith & Nephew PLC

- Abbott Laboratories

- Dentsply Sirona

- Boston Scientific Corporation

- LivaNova PLC

- Cochlear Ltd

- Others

Frequently Asked Questions

The global nano healthcare technology for medical equipment market is projected to be valued at US$ 4.6 Bn in 2026.

Rising chronic diseases, demand for durable implants, and advances in nanoscale materials strongly accelerate market adoption.

The global nano healthcare technology for medical equipment market is poised to witness a CAGR of 6.6% between 2026 and 2033.

Expanding nano-engineered orthopedic and spinal implants, regenerative coatings, and minimally invasive device innovations offer significant growth potential.

Major players include 3M Company, Zimmer Biomet, Stryker, Starkey, and Smith & Nephew PLC.