- Metals & Minerals

- Electrical Insulation Coatings Market

Electrical Insulation Coatings Market Size, Share, and Growth Forecast, 2026 – 2033

Electrical Insulation Coatings Market by Resin Type (Epoxy, Acrylic, Polyurethane, Others), Product Form (Liquid, Powder, others), Application (Transformers, Motors/Generators, Others), and Regional Analysis 2026 – 2033

Electrical Insulation Coatings Market Size and Trends Analysis

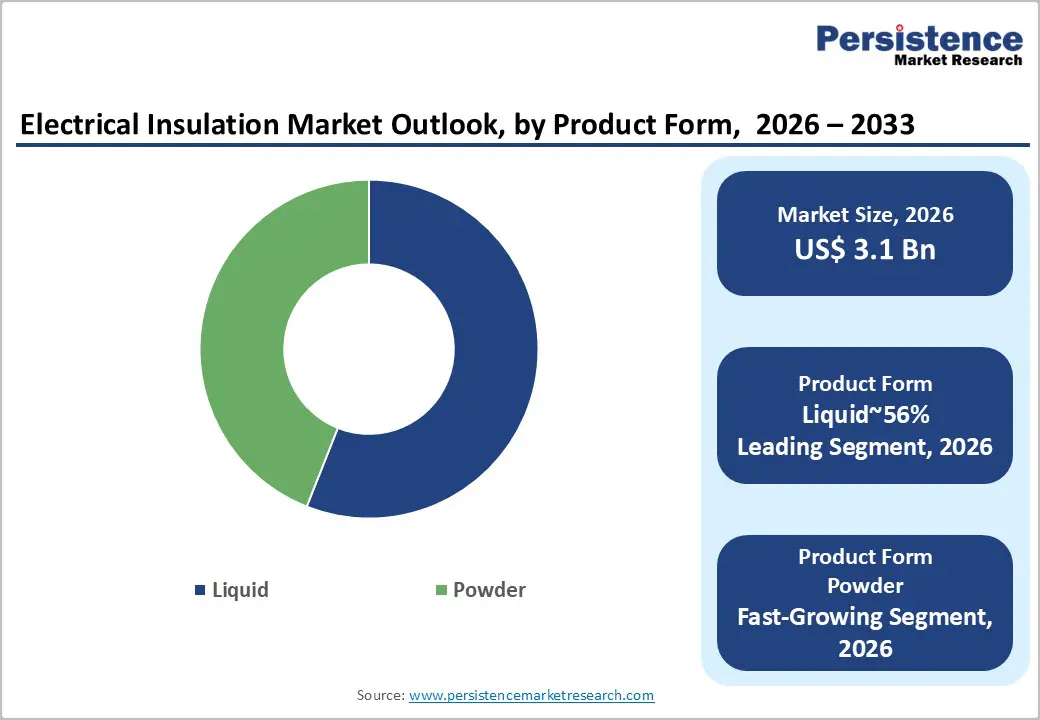

The global electrical insulation coatings market size is likely to be valued at US$3.1 billion in 2026 and is expected to reach US$4.2 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by the global electrification trend, particularly the rapid rise in electric vehicle (EV) production and the pressing need to modernize aging power grids.

This shift marks a transition from traditional maintenance-driven demand to capital expenditure-focused expansion, including investments in renewable energy infrastructure such as solar and wind projects, and the modernization of power grids.

Key Industry Highlights:

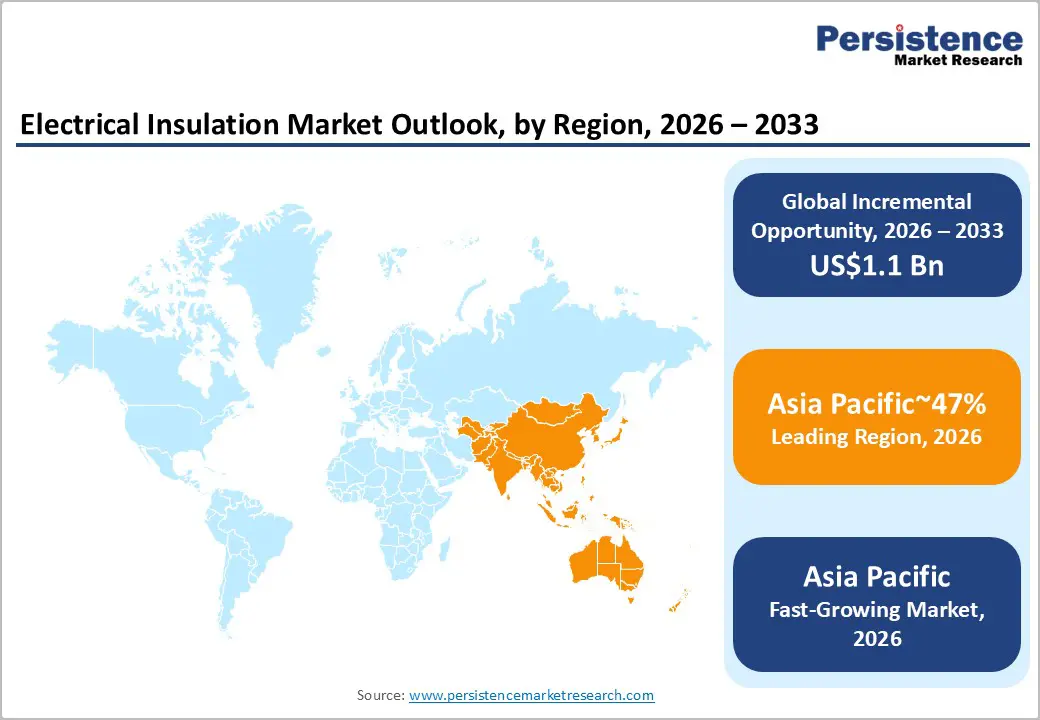

- Leading Region: Asia Pacific with approximately 47% share, driven by large-scale power infrastructure expansion, high-volume electrical equipment manufacturing, and accelerating EV production in China and India.

- Fastest-growing Region: Asia Pacific, supported by continued grid investments, industrial electrification initiatives, and rapid scaling of domestic electrical equipment supply chains.

- Leading Resin Type: Epoxy resins, holding around 36% share, as their strong dielectric strength, thermal stability, and chemical resistance support widespread use across transformers, motors, generators, and high-voltage industrial equipment.

- Leading Product Form: Liquid insulation coatings, accounting for approximately 56% share, due to ease of application, uniform surface coverage, and compatibility with dip-coating and spray processes across large electrical components.

| Key Insights | Details |

|---|---|

| Electrical Insulation Coatings Market Size (2026E) | US$ 3.1 Bn |

| Market Value Forecast (2033F) | US$ 4.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Electrification of the Automotive Sector

Electrification is fundamentally transforming demand for electrical insulation coatings as automotive powertrains shift from combustion-based architectures to high-voltage, high-thermal-density electric platforms. This transition is moving the market from general-purpose insulation toward advanced, application-specific coatings designed for thermal management, flame retardancy, dielectric performance, and compact power electronics packaging. Components such as battery packs, inverters, onboard chargers, and e-axles impose tight electrical and thermal constraints, elevating coatings from passive protection to performance-critical enablers of safety, efficiency, and packaging density. As EV platforms consolidate functions into smaller footprints, coatings with high dielectric strength, thin-film performance, and durable adhesion under thermal cycling are essential for system reliability in harsh automotive duty cycles.

At the component level, insulation coatings mitigate thermal propagation in battery assemblies, maintain electrical isolation in high-voltage architectures, and enable higher rotational speeds and power densities in electric motors through low-loss electrical steel coatings. Materials innovation is accelerating toward lightweight, high-temperature formulations that preserve insulation under sustained heat while supporting miniaturization and weight reduction. On the supply side, EV-driven localization and platform standardization are tightening qualification loops between OEMs, Tier-1s, and coatings suppliers, favoring vendors with automotive-grade process control and co-development capabilities. Collectively, EV adoption is expanding the per-vehicle insulation footprint, increasing specification rigor, and anchoring long-term volume growth across batteries, power electronics, charging hardware, and traction motors. In October 2025, Axalta launched EV powder coatings engineered for 1200°C heat resistance, enhancing battery insulation and mitigating fire risks, aligned with UL 94 V-0 standards for dielectric integrity and thermal safety.

Renewable Energy Infrastructure Expansion

The growth of renewable energy infrastructure is a key driver for the market, as power systems increasingly integrate solar, wind, grid-scale storage, and distributed assets. These technologies impose demanding electrical, thermal, and environmental requirements, making coatings critical for reliability across inverters, generators, transformers, switchgear, and power electronics exposed to UV, moisture, salt spray, thermal cycling, and high voltages.

Rising renewable integration and grid complexity are prompting utilities and EPCs to adopt higher-grade dielectric, flame-retardant, and corrosion-resistant coatings, extending asset life and reducing maintenance intervals. Renewable-driven capex expands coated surface area per installed megawatt, particularly for transformers and high-voltage components, favoring suppliers with proven performance under partial discharge, humidity, and long-term thermal aging. Powder coatings are gaining adoption for outdoor durability, while aerogel- and nanocomposite-enhanced formulations support thermal management, weight reduction, and compact enclosures. Overall, renewable infrastructure expansion is structurally increasing both coating volumes and specification intensity across generation, storage, and grid modernization projects.

Barrier Analysis – High Production and Application Costs

High production and application costs continue to constrain the market, particularly for small-to-medium enterprises and cost-sensitive project developers. These costs are embedded across the value chain, from specialty resin inputs and energy-intensive processing to capital-heavy application infrastructure. High-performance formulations rely on complex chemical precursors and tightly controlled synthesis routes, increasing exposure to feedstock volatility and energy price fluctuations. On the application side, advanced systems such as powder and UV-curable coatings require dedicated spray booths, electrostatic deposition equipment, and controlled curing environments, raising entry barriers and extending payback periods.

For high-voltage and high-reliability applications, achieving micron-level thickness control, repeatable deposition, and rigorous dielectric validation necessitates automated application platforms, in-line inspection, and post-coating testing, all of which inflate the total cost of ownership. Skilled technicians for thermal spray and plasma-applied systems are limited, further driving labor costs and project timelines. Suppliers are addressing these challenges by developing thin-film formulations, expanding water-based systems, and optimizing manufacturing footprints. While these strategies partially mitigate costs, structural constraints continue to limit adoption in price-sensitive industrial, grid, and utility segments, where performance premiums are difficult to justify.

Opportunity Analysis – Expansion into Renewable Energy Storage

The expansion of renewable energy storage systems presents a structurally attractive growth opportunity for electrical insulation coatings, driven by the rapid scale-up of grid-connected batteries and increased deployment of power electronics across generation, storage, and conversion assets. Energy storage architectures concentrate high voltages, currents, and thermal loads within compact enclosures, intensifying the need for dielectric integrity, arc suppression, and heat management across modules, busbars, inverters, and enclosure interiors. This drives demand for advanced insulation coatings that combine electrical isolation with thermal stability, flame retardancy, and long-term durability under cyclic load conditions.

The opportunity extends beyond battery cells into the broader balance-of-system layer, including transformers, switchgear, and thermal management assemblies. As renewable penetration rises, grid operators increasingly rely on storage assets for frequency regulation, peak shaving, and intermittency management, expanding the installed base of high-reliability electrical equipment. Coatings suppliers can capture recurring demand through both new-build deployments and lifecycle maintenance, refurbishment, and retrofitting. Product strategies that emphasize thin-film dielectric performance, compatibility with compact power electronics, and resilience under thermal cycling align closely with storage-centric applications. Over time, standardization of storage architectures and modular power blocks is expected to support scalable procurement, enhancing supplier visibility and reinforcing insulation coatings as a critical enabler of safe, reliable renewable energy infrastructure.

Shift to Powder Coatings in Emerging Markets

The transition to powder-based electrical insulation coatings presents a structurally attractive opportunity in emerging manufacturing ecosystems, driven by tightening environmental regulations, rising quality standards, and the operational advantages of powder formulations over conventional liquid systems. Powder coatings offer process efficiencies through higher material utilization, reduced waste, and elimination of solvent handling, improving shop-floor safety and simplifying compliance management for manufacturers scaling output in motors, generators, transformers, and power electronics. These benefits suit cost-sensitive production environments aiming to enhance performance without adding operational complexity. As local supply chains mature, regional compounding, toll manufacturing, and application services reduce adoption barriers for small and mid-sized fabricators, accelerating diffusion beyond large OEMs.

From an industrialization perspective, powder coatings enable higher-throughput production through faster cure cycles, improved film uniformity, and superior adhesion on complex geometries, particularly for compact, high-density electrical components. The opportunity also extends to aftermarket refurbishment of rotating equipment and grid assets, where powder systems offer durable recoating at lower lifecycle costs and reduced downtime. Over time, standardization of coating specifications across motor platforms and power equipment families is expected to institutionalize powder coatings within procurement frameworks, strengthening recurring demand and positioning suppliers with localized production and application support to capture a disproportionate share of incremental growth.

Category–wise Analysis

Resin Type Insights

Epoxy resin is expected to lead with approximately 36% share in 2026, underpinned by its entrenched role across transformers, motors, generators, and EV powertrains. Adoption remains anchored by a balanced performance envelope combining dielectric strength, adhesion to copper and aluminum, chemical resistance, and scalable cost structures that suit high-volume manufacturing. Ongoing platform evolution, including nanoparticle-enhanced thermal pathways, dual-cure chemistries for complex geometries, and lower-temperature powder curing, continues to reinforce replacement cycles and utilization intensity in grid modernization and e-mobility programs. Suppliers such as AkzoNobel, PPG Industries, and Axalta are expanding portfolios with EV battery-box coatings, high-voltage busbar systems, and next-generation compliant formulations to secure long-term OEM qualification pathways. This combination of mature infrastructure, formulation flexibility, and predictable demand sustains epoxy’s dominance within standardized deployment models.

PTFE and polyurethane are projected to be the fastest-growing resin types within the electrical insulation coatings market, driven by unmet needs in high-temperature, high-frequency electronics and flexible outdoor power infrastructure. Growth is catalyzed by functionalized fluoropolymer chemistries, water-borne dispersions, and rapid-curing PU systems that materially improve thermal stability, abrasion resistance, and production throughput. Accelerating adoption is supported by automation-ready processing and laser-compatible stripping capabilities that reduce operational friction in electronics assembly and cable manufacturing. Companies including Chemours, Daikin Industries, Covestro, and Huntsman are scaling PTFE films for RF laminates and polyurethane elastomers for robotics and renewable-energy cabling.

Product Form Insights

Liquid coatings are expected to maintain leadership in the electrical insulation coatings market, capturing approximately 56% share in 2026, supported by a deeply entrenched installed base across winding wires, transformers, generators, and traction motors. Their adoption is driven by low-viscosity penetration into dense copper windings, ultra-thin film capability that preserves slot fill in compact EV motors, and compatibility with dip-and-bake and trickle impregnation lines already scaled in global factories. Advances in high-solids chemistries, rapid UV/EB curing, and nano-silica enhanced corona resistance are anticipated to reinforce replacement cycles and utilization intensity in grid refurbishment and electrified powertrains. Portfolio expansions, such as ELANTAS’ ELAN-Protect systems and Axalta’s Voltatex water-borne impregnating resins and advanced wire enamels across APAC electronics manufacturing, position suppliers to secure long-cycle OEM qualifications. This combination of mature infrastructure, formulation flexibility, and predictable high-volume demand sustains liquid coatings’ dominance in standardized production workflows.

Powder-based coatings are projected to be the fastest-growing product segment, driven by unmet needs in EV battery enclosures, busbars, and large-format power cabinets requiring thick, uniform dielectric coverage in a single pass. Growth is fueled by low-bake chemistries, induction-assisted curing, and epoxy-polyester hybrids that enhance throughput, edge coverage, and outdoor durability. Reclaimable overspray, non-flammable handling, and thin-film powder innovations reduce historical application constraints on smaller components. Examples include AkzoNobel’s Resicoat EL for battery-box insulation and PPG’s Envirocron Extreme Protection for high-voltage assemblies, embedding switching costs across OEM programs. As EV pack architectures scale and factory electrification accelerates, powder systems are expected to outpace overall market growth over the forecast period.

Regional Insights

Asia Pacific Electrical Insulation Coatings Market Trends

Asia Pacific is expected to remain the leading region in the electrical insulation coatings market, accounting for approximately 47% of global share, driven by its concentration of high-volume electronics manufacturing, grid equipment production, and electric vehicle supply chains. China is likely to continue anchoring regional demand through its scale in EV motors, battery packs, transformers, and industrial machinery, while India is projected to contribute incrementally via power transmission upgrades and renewable capacity additions. Japan and Southeast Asia are expected to sustain baseline demand through shipbuilding, consumer electronics, and industrial automation, reinforcing APAC’s role as the primary consumption and production hub. Regional leaders such as Nippon Paint Holdings, Kansai Paint, AkzoNobel, and 3TREESGROUP are poised to maintain strong positions across wire enamels, motor insulation, and transformer coatings, supported by entrenched OEM relationships and localized manufacturing footprints. The structural shift toward water-borne and low-VOC systems is expected to continue shaping product portfolios across the region’s industrial clusters.

APAC is also projected to be the fastest-growing region, driven by grid modernization, renewable integration, and transport electrification across China and India. Capacity expansions by global suppliers such as BASF, Axalta, and PPG will deepen regional self-sufficiency in high-performance insulation chemistries, while domestic formulators scale offerings for motors, generators, and high-voltage components. Growth in Japan and South Korea is expected as miniaturization intensifies thermal and dielectric performance requirements. Sustained investment in EV platforms, power infrastructure, and localized coating ecosystems positions APAC as both the volume anchor and growth engine of the global market.

North America Electrical Insulation Coatings Market Trends

North America is expected to remain a strategically important but mature market for electrical insulation coatings, driven more by technology-led replacement demand than by volume growth. Steady adoption is anticipated across high-specification applications in EV powertrains, aerospace electrical systems, grid transformers, and renewable energy generators. Product innovation will continue to focus on enhanced thermal management, fire-retardant performance, and long-term dielectric stability, with coating specifications increasingly embedded in OEM qualification processes. Established suppliers, including PPG Industries, Sherwin-Williams, Axalta Coating Systems, Dow, and 3M, are likely to retain strong positions through long-term agreements with automotive, utility, and industrial OEMs, while Henkel, DuPont, and Hempel continue to expand specialty insulation resins and protective coating offerings. The market is expected to favor high-reliability formulations over cost-driven commoditized products.

Growth in North America will be supported primarily by infrastructure refurbishment, EV platform refresh cycles, and the expansion of domestic battery manufacturing, rather than new greenfield capacity. Demand will focus on advanced wire enamels, transformer varnishes, and battery pack fire-protection layers, with increasing adoption of low-VOC, water-borne, and bio-derived chemistries. Nearshored manufacturing by PPG, Axalta, and Sherwin-Williams, alongside high-performance additives and binders from Dow, DuPont, and 3M, will reinforce the region’s sustainability. Combined, entrenched incumbents, diversified end-market exposure, and continuous product innovation are expected to underpin North America’s long-term stability in the electrical insulation coatings market.

Europe Electrical Insulation Coatings Market Trends

Europe is expected to remain a structurally stable yet mature market for electrical insulation coatings, with growth driven primarily by premium, regulation-led applications rather than volume expansion. Demand is projected to focus on high-value end uses such as offshore wind generators, high-speed rail traction systems, aerospace electrical assemblies, and advanced EV power electronics, where lifecycle durability, thermal stability, and low-emission chemistries are critical. Product specifications are increasingly shifting toward PFAS-free, low-VOC, and bio-derived formulations, reinforcing the competitive advantage of established suppliers with strong formulation expertise. Key players such as AkzoNobel, BASF, Elantas (ALTANA Group), Hempel, and Sika are expected to remain central to industrial supply chains, supported by Covestro and Solvay in specialty resins and performance polymers, while smaller specialty formulators in Germany and the Benelux region continue to serve niche insulation requirements for transformers and traction motors.

Market resilience is likely to be sustained through diversified industrial exposure and entrenched OEM relationships rather than rapid capacity growth. Refurbishment cycles in grid infrastructure, offshore wind cabling, and rail electrification will reinforce demand, while European manufacturing footprints benefit from proximity to automotive and energy OEMs. Material innovators such as Covestro, Solvay, and Arkema are expected to supply next-generation binders and additives for high-temperature, high-voltage insulation. This dense ecosystem of chemical majors, specialty coating suppliers, and industrial OEMs underpins Europe’s long-term sustainability and technological leadership in the electrical insulation coatings market.

Competitive Landscape

The global electrical insulation coatings market is moderately fragmented, led by major players such as PPG, 3M, AkzoNobel, Evonik, Axalta, and Elantas, which shape pricing norms and technology standards through scale, certification depth, and long-standing relationships with OEMs and electrical equipment manufacturers. These companies matter because their materials science capabilities and application know-how influence qualification cycles across motors, transformers, and emerging EV platforms. While leadership is concentrated at the top, competition remains active as smaller suppliers address niche, low-voltage, and regional applications, sustaining fragmentation beneath the leading tier.

Competitive positioning centers on innovation-led differentiation, total system solutions, and compatibility across multilayer insulation stacks, rather than coatings alone. Industry behavior reflects ongoing consolidation through M&A, platform expansion into EV and renewable energy use cases, and tighter collaboration with equipment manufacturers to shorten qualification timelines. Looking ahead, competitive pressure is expected to intensify around advanced formulations, sustainability-aligned chemistries, and integrated application technologies, reinforcing gradual consolidation while preserving fragmentation in specialized subsegments.

Key Industry Highlights

- In December 2025, Installed Building Products acquired CKV Finished Products LLC, expanding its insulation installation capabilities. This move strengthens service offerings in electrical and mechanical insulation for industrial projects, improving market reach and operational synergies.

- In November 2025, Siemens Energy introduced a new range of eco-friendly, high-voltage insulation materials for digital transformers and smart grids. The materials offer superior efficiency and reliability, facilitating the transition to smarter, more sustainable energy systems.

- In October 2025, Axalta Coating Systems introduced two new powder coatings designed for EV battery heat protection and electrical insulation. These coatings resist extreme temperatures up to 1200°C, enhancing battery safety and performance in electric vehicles.

Companies Covered in Electrical Insulation Coatings Market

- Akzo Nobel N.V.

- PPG Industries, Inc.

- Elantas (ALTANA Group)

- Axalta Coating Systems

- The Sherwin-Williams Company

- 3M Company

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- BASF SE

- DuPont de Nemours, Inc.

- Hempel A/S

- Solvay S.A.

- Dow Inc.

- Von Roll (Sika AG)

- Evonik Industries AG

Frequently Asked Questions

The global electrical insulation coatings market is projected to be valued at US$3.1 billion in 2026 and is expected to reach US$4.2 billion by 2033, driven by the electrification megatrend, including EV production and power grid modernization.

The rapid transition to electric vehicles is a primary driver, as it shifts demand from general-purpose coatings to advanced, high-performance formulations that ensure dielectric integrity, thermal management, and safety in high-voltage EV powertrains, batteries, and power electronics.

The electrical insulation coatings market is forecast to grow at a CAGR of 4.8% from 2026 to 2033, reflecting steady demand from infrastructure upgrades and electrification.

Asia Pacific is the leading regional market, accounting for approximately 47% share, driven by large-scale power infrastructure expansion, high-volume electrical equipment manufacturing, and accelerating EV production in China and India.

The electrical insulation coatings market is moderately fragmented, with key players including Akzo Nobel N.V., PPG Industries, Inc., 3M Company, Axalta Coating Systems, and Elantas (ALTANA Group). These leaders compete through scale, material science expertise, and long-standing relationships with OEMs.