- Plastics, Polymers & Resins

- Electrical Conduit Pipe Market

Electrical Conduit Pipe Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Electrical Conduit Pipe Market by Metal Conduits (Rigid Metal Conduit (RMC), Galvanized Rigid Steel (GRC), Intermediate Metal Conduit (IMC), and Electrical Metallic Tubing (EMT)) and Non-Metal Conduits (Rigid Nonmetallic Conduit (RNC), RTRC (Fiberglass Conduit), PVC Conduit, and Electrical Nonmetallic Tubing (ENT)), Industry and Regional Analysis for 2026 - 2033

Electrical Conduit Pipe Market Size and Trends Analysis

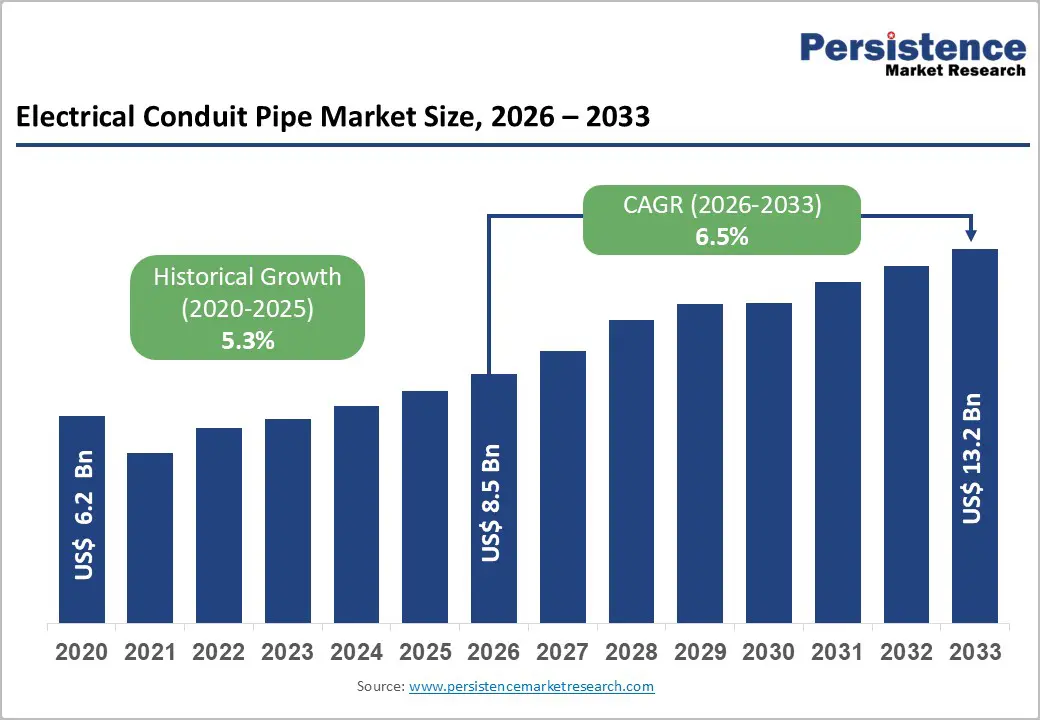

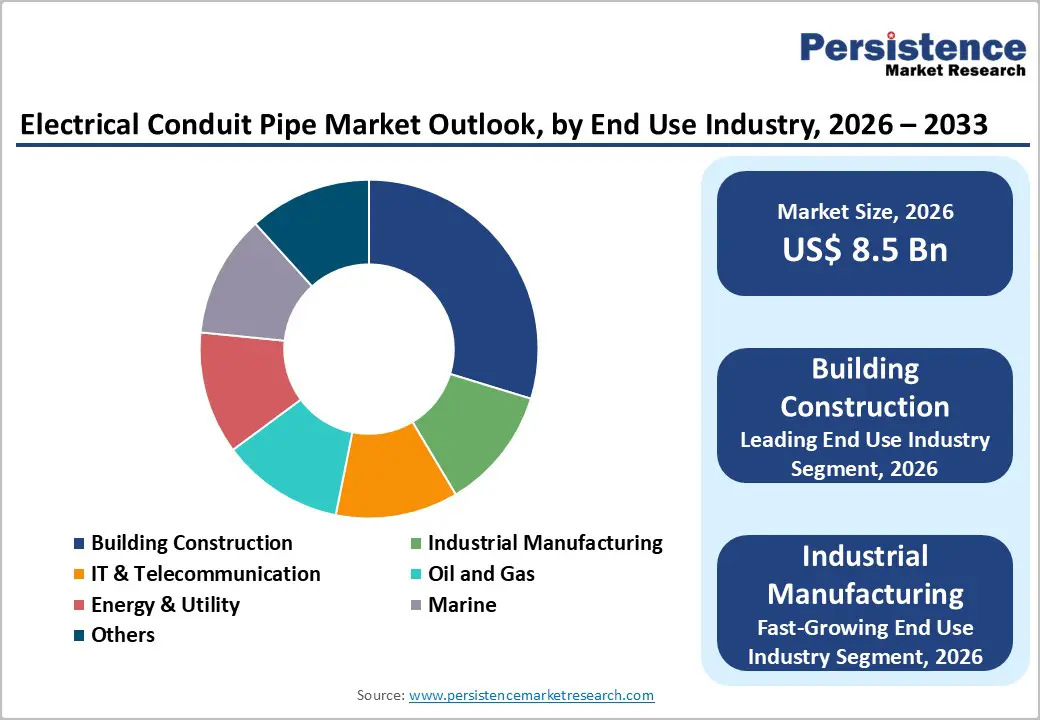

The global electrical conduit pipe market size was valued at US$ 8.5 billion in 2026 and is projected to reach US$ 13.2 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033. This market expansion is primarily driven by accelerating global urbanization, increasing infrastructure investments, and the growing adoption of renewable energy systems worldwide.

Electrical conduit is a protective raceway-and a specific type of metal or plastic pipe used to safeguard electrical wires from breakage, pressure, and disconnection. Widely used in buildings, data centers, transport systems, and industrial sites, conduits may be rigid or flexible and offer protection against impact, corrosion, moisture, fire, and EMI. NEC permits direct concrete encasement for commercial applications.

Key Industry Highlights:

- Product Segment Leadership: Metal conduits maintain market dominance with above 60% revenue share, while non-metallic conduits represent the fastest-growing segment, expanding at 7.1% CAGR, driven by cost advantages and increased code acceptance.

- End-Use Industry Dynamics: Building construction dominates with above 50% revenue share, while industrial manufacturing represents the fastest-growing end-use sector at 8.5% CAGR, driven by Industry 4.0 implementation and automation expansion.

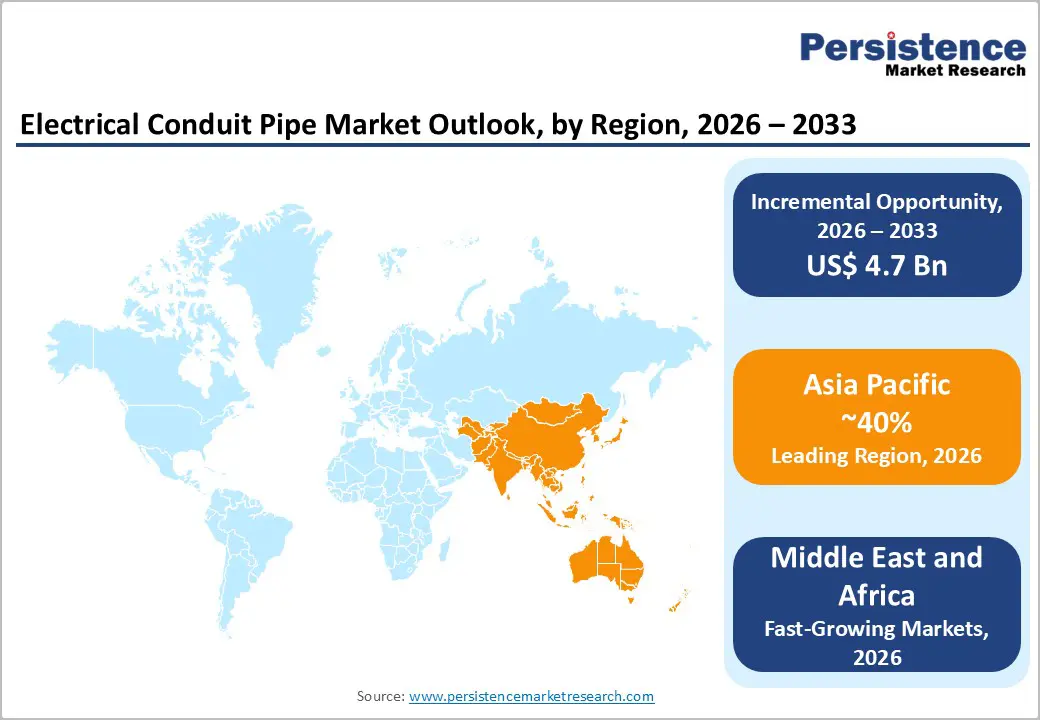

- Regional Market Leadership: Asia Pacific commands above 40% global revenue share with highest growth rates, while North America maintains 25-28% market share with infrastructure modernization focus; Europe represents 18-22% share emphasizing sustainability and circular economy compliance.

- Critical Market Drivers: Rapid urbanization, accelerating infrastructure demand, renewable energy capacity expansion exceeding 1.2 trillion watts globally, and tightened electrical safety regulations establishing non-discretionary compliance requirements drive sustained market expansion.

- Strategic Developments: Manufacturer focus on sustainable product development, manufacturing capacity expansion in nearshoring locations, and technology partnerships supporting IoT and smart building integration establish competitive differentiation and support premium positioning in developed markets.

| Key Insights | Details |

|---|---|

|

Electrical Conduit Pipe Market Size (2026E) |

US$ 8.5 Bn |

|

Market Value Forecast (2033F) |

US$ 13.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.3% |

Market Dynamics

Drivers - Rapid Urbanization and Infrastructure Development

Urbanization stands as the primary catalyst for the electrical conduit pipe market expansion. The United Nations projects that approximately 68% of the global population will reside in urban areas by 2050, compared to 56% in 2020. This demographic shift necessitates unprecedented infrastructure development across residential, commercial, and industrial sectors. In Asia Pacific alone, urban populations are expected to increase by 650 million people by 2050, creating substantial demand for building construction and electrical systems.

The Indian construction sector, for instance, is projected to grow at 8-10% annually through 2030, directly correlating with heightened conduit pipe demand. Developing economies in Southeast Asia and Africa demonstrate similar growth trajectories, with construction gross value added expanding at 4-6% annually. These macro-scale urbanization trends translate directly into increased demand for reliable electrical infrastructure, establishing urbanization as a non-cyclical, structural growth driver for the conduit pipe market over the medium to long term.

Regulatory Compliance and Safety Standards Strengthening

Tightened electrical safety regulations across jurisdictions mandate upgraded conduit specifications and installations. The National Electrical Code (NEC) in North America, the IEC 61386 series in Europe, and emerging standards in Asia Pacific establish increasingly rigorous requirements for electrical wiring protection, flame resistance, and impact durability. These regulatory frameworks directly mandate greater conduit specifications and accelerate replacement cycles for legacy installations.

The European Union's CPR (Construction Products Regulation) requires comprehensive compliance documentation and performance certifications, effectively raising barriers to non-compliant products. India's Bureau of Indian Standards (BIS) has strengthened electrical safety requirements for building and infrastructure projects, requiring certified conduit systems across all new constructions. These regulatory drivers are structural in nature—non-discretionary compliance requirements—ensuring steady, predictable demand independent of economic cyclical pressures. Manufacturers investing in compliance infrastructure gain competitive advantages, while non-compliant suppliers face market exclusion.

Restraint - Price Volatility of Raw Materials and Supply Chain Disruptions

Electrical conduit pipes depend heavily on raw material inputs, including steel, aluminum, PVC, and HDPE polymers. Commodity price volatility directly impacts production costs and profit margins. Steel prices experienced 40-60% fluctuations during 2021-2023, creating cost uncertainty for metal conduit manufacturers. Supply chain disruptions post-COVID and geopolitical tensions have increased logistics costs by 15-25% in certain regions, elevating final product pricing and limiting demand from price-sensitive markets. Smaller regional manufacturers face particular vulnerability to raw material shocks, lacking the hedging capabilities and procurement scale of multinational corporations. These cost pressures compress margins and delay capital investments in capacity expansion, potentially constraining market growth in price-competitive segments.

Opportunity - Smart Infrastructure Adoption and Sustainability Transition: Unlock High-Value Opportunities in the Global Electrical Conduit Market

The electrical conduit market is positioned for substantial opportunity as buildings become smarter and sustainability pressures intensify. The rapid integration of smart electrical systems, IoT sensors, and energy-intelligent infrastructure is reshaping conduit requirements, driving demand for products that support both power and low-voltage data transmission while offering enhanced shielding to prevent electromagnetic interference. As smart buildings expand globally, supported by strong growth in automation, real-time monitoring, and digital load management, manufacturers that introduce conduits with embedded sensing features and dual-function compatibility can secure premium pricing and strengthen technological differentiation.

Parallel to this, the transition toward circular economy materials is accelerating, with recycled aluminum and HDPE conduits gaining preference due to their significantly reduced carbon footprints. Regulatory actions in the EU, along with green building standards such as LEED and BREEAM, are pushing construction firms to adopt low-carbon electrical components. This shift creates a high-value opportunity for manufacturers offering recyclable, environmentally certified conduit solutions, enabling margin expansion and strong adoption across sustainability-focused markets in North America and Europe.

Category-wise Analysis

Product Type Insights - Metal Conduits Dominate Global Revenue While Non-Metal Alternatives Rapidly Accelerate as the Fastest-Growing Electrical Conduit Segment Worldwide

Metal conduits remain the dominant product category in the global electrical conduit market, contributing more than 60% of total revenue due to their superior mechanical strength, electromagnetic interference protection, and compliance with stringent global electrical codes. Key metal conduit types—Rigid Metal Conduit (RMC), Galvanized Rigid Steel (GRC), Intermediate Metal Conduit (IMC), and Electrical Metallic Tubing (EMT)—serve high-demand applications across industrial, commercial, and infrastructure projects. RMC and GRC, both covered under NEC Article 344, offer exceptional durability and impact resistance but are heavier, costly, and labor-intensive to install. IMC, governed by Article 342, provides a lighter, more economical steel alternative suitable for outdoor use, while EMT, under Article 358, is widely used in commercial and residential construction due to its lightweight form and easy bendability despite offering lower mechanical protection. North America remains a major consumer of metal conduits, supported by industrial activity and strict electrical safety standards. Although the segment is projected to grow steadily at around 5.8% CAGR, rising adoption of cost-effective non-metal alternatives is expected to gradually reduce its share.

Non-metal conduits represent the fastest-growing segment, expanding rapidly as lightweight, corrosion-resistant, and flexible alternatives gain acceptance across residential, light commercial, and underground utility installations. Key types include Rigid Nonmetallic Conduit (RNC) under Article 352, RTRC fiberglass conduit under Article 355, PVC conduit, and Electrical Nonmetallic Tubing (ENT) governed by Article 362. RTRC is becoming increasingly favored for utility, data center, and transportation projects due to its exceptional corrosion resistance, low installation cost, and fire-rated performance. PVC and ENT remain widely used in concealed and low-stress environments because of their ease of handling and affordability.

Industry Insights - Building Construction Dominates Global Conduit Demand as Industrial Manufacturing Emerges Fastest-Growing Sector Amid Regional Expansion Trends

The global electrical conduit market is led by the building construction sector, which accounts for around 60% of total revenue, underscoring its universal requirement for safe electrical wiring infrastructure across residential, commercial, and institutional developments. Residential projects alone contribute nearly half of this segment’s activity, supported by rapid urbanization, housing expansion, and redevelopment initiatives, while commercial and institutional buildings make up the remaining share.

Regional dynamics significantly shape growth: Asia Pacific continues to dominate conduit consumption due to strong construction expansion, while the Middle East is rapidly accelerating. Saudi Arabia’s construction market, valued at USD 70.33 billion in 2024 and projected to reach USD 91.36 billion by 2029, benefits from Vision 2030 and major Public Investment Fund–backed giga-projects such as Neom, Red Sea Global, and Qiddiya, all of which intensify demand for advanced conduit systems. China, despite a 10.7% decline in real estate investment from January–May 2025, remains the world’s largest construction market at USD 4.82 trillion, ensuring sustained long-term installations.

Industrial manufacturing stands as the fastest-growing end-use sector, expanding at nearly 9% CAGR through 2033. Increasing automation, Industry 4.0 upgrades, and high-specification requirements in semiconductor, pharmaceutical, and automotive manufacturing drive premium conduit adoption and support higher-margin growth.

Regional Insights and Trends

Asia Pacific Dominates Global Electrical Conduit Market Growth Through 2033 with Expanding Construction, Manufacturing, and Renewable Energy Demand

Asia Pacific holds the leading position in the global electrical conduit market, contributing over 40% of total revenues and acting as the core engine of industry expansion through 2033. Its dominance is driven by rapid urbanization, massive infrastructure spending, strong manufacturing output, and accelerating renewable energy deployment. China and India account for the majority of regional demand, with combined market volumes projected to surpass US$ 6.5 billion by 2033.

China leads in absolute value, supported by large-scale industrial activity and world-leading renewable installations, while India is the fastest-growing market, propelled by construction growth, electrification initiatives, and major infrastructure programs. Japan, South Korea, and emerging Southeast Asian economies continue contributing steady to rising demand. Urban growth is adding hundreds of millions of new residents, fast-paced infrastructure development, and expanding automotive and electronics manufacturing, further sustaining conduit requirements. Harmonizing building codes and stricter fire and EMC standards are shaping product specifications, while global and regional players expand local manufacturing and distribution to capture rising demand.

Middle East & Africa Emerges as Fastest-Growing Electrical Conduit Market Driven by Expanding Construction and Infrastructure Investments

The Middle East & Africa have become the fastest-growing region with 8.4% in the global electrical conduit market, driven by large-scale construction, utility expansion, and accelerated urban development. According to the International Trade Administration, Saudi Arabia now leads the MENA construction landscape, with the market valued at USD 70.33 billion in 2024 and projected to reach USD 91.36 billion by 2029, reflecting the impact of the country’s Vision 2030 National Development Plan and substantial government-led infrastructure investments.

Mega-projects such as NEOM, The Red Sea Project, and major rail and airport expansions significantly increase demand for both metallic and non-metallic conduits. The UAE, Qatar, and Egypt continue contributing strong momentum through smart city programs, energy diversification, and industrial growth. Across Africa, rising electrification efforts, telecom network expansion, and growing commercial construction activity in economies such as Kenya, Nigeria, and South Africa further accelerate market uptake. Strengthening building codes and investment in renewable energy reinforce MEA’s position as the fastest-expanding conduit market through 2033.

Competitive Landscape

The global electrical conduit market exhibits moderate concentration, with the top five manufacturers controlling approximately 45-50% of the global market share. This structure reflects significant barriers to entry, including manufacturing capital requirements, regulatory compliance complexity, and established distribution networks, while enabling regional players to maintain niche positions through localized product development and customer relationships. Leading multinational corporations, including Schneider Electric, Legrand, ABB, and Siemens, leverage global scale, comprehensive product portfolios, and established distribution networks to maintain premium positioning in developed markets.

Mid-tier competitors focus on regional dominance or product specialization, while numerous smaller manufacturers serve localized markets through cost-competitive offerings. The market demonstrates typical industrial characteristics with 4-6 firms competing vigorously in each geographic region, supporting both volume-driven and specialty-product strategies. Competitive differentiation increasingly centers on sustainability credentials, smart technology integration, and customer service capabilities rather than traditional price competition alone.

Key Industry Developments:

- In August 2024, Male Water and Sewerage Company (MWSC) launched conduit pipes designed to protect electrical wires from damage. These pipes produced in the Maldives, meet international safety standards and are available in sizes of 16mm, 20mm, 25mm, 32mm, and 40mm. The pipes are sustainable and meet international safety standards.

- IN March 2024, Punjab Kings has announced Astral Pipes as an associate partner for the upcoming IPL 2024 cricket tournament. Astral Pipes, a manufacturer of plastic pipes, is known for its quality and innovative solutions. The partnership will enhance local connections and ensure excellence in the upcoming tournament.

- In February 2021, Atkore International Group Inc. acquired FRE Composites Group, a prominent manufacturer of fiberglass conduit solutions for electrical, transportation, telecommunication, and infrastructure applications. This acquisition significantly broadened Atkore’s conduit product portfolio and strengthened its presence in high-performance composite conduit technologies.

- In October 2020, Atkore International Group Inc. acquired the assets of Queen City Plastics, Inc., a producer of PVC conduit, elbows, and fittings for the electrical industry. This strategic move enhanced Atkore’s product offerings and improved its ability to serve customers across the Southeast and mid-Atlantic regions of the United States.

Companies Covered in Electrical Conduit Pipe Market

- Atkore International Group Inc.

- AKG Group of Companies

- Wienerberger AG

- Aliaxis Group S.A.

- Sekisui Chemical Co., Ltd.

- China Lesso Group Holdings Ltd.

- Nan Ya Plastics Corp.

- Zekelman Industries Inc.

- Orbia Advance Corporation

- OPW Corporation

- Supreme

- Other Market Players

Frequently Asked Questions

The Electrical Conduit Pipe market is estimated to be valued at US$ 8.5 Bn in 2026.

The key demand driver for the Electrical Conduit Pipe market is the rapid expansion of construction, industrial infrastructure, and smart utility networks, boosted by safety regulations, which drives increasing demand for durable, efficient electrical conduit pipes across global markets.

In 2026, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Electrical Conduit Pipe market.

Among industries, Building Construction has the highest preference, capturing beyond 50% of the market revenue share in 2026, surpassing other end-use industries.

Atkore International Group Inc., AKG Group of Companies, Wienerberger AG, Aliaxis Group S.A., Sekisui Chemical Co., Ltd., China Lesso Group Holdings Ltd. are a few leading players in the Electrical Conduit Pipe market.