- Metals & Minerals

- India Electrical Steel Market

India Electrical Steel Market Size, Share, and Growth Forecast, 2026 - 2033

India Electrical Steel Market by Product Type (Grain-oriented Electrical Steel and Non Grain-oriented Electrical Steel), Product (Transformers, Alternators/Generators, Motors, EV Motors, and Others), End-use (Energy and Power Generation, Automotive, Industrial Automation, Electronics, and Others), and Regional Analysis for 2026 - 2033

India Electrical Steel Market Size and Trends Analysis

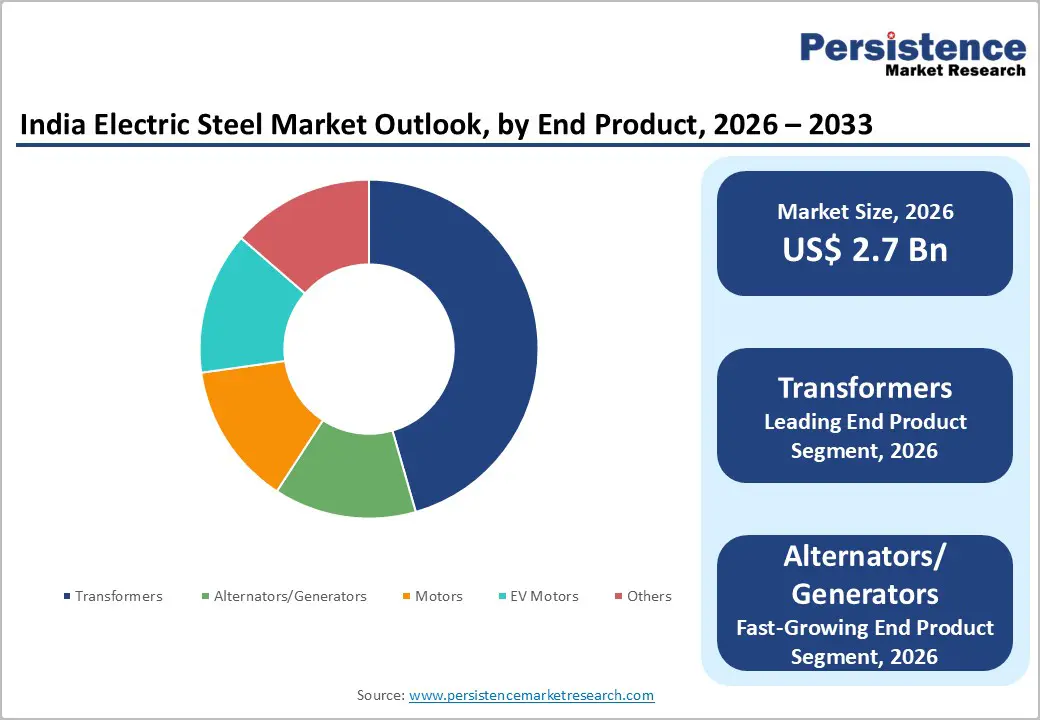

The India electrical steel market size is likely to be valued US$ 2.7 billion in 2026, with projections to achieve US$ 7.6 billion by 2033, representing exceptional growth at a CAGR of 16.0% between 2026 and 2033.

This accelerated expansion reflects the convergence of three structural forces: India's grid modernization agenda targeting 500 GW renewable energy integration by 2030, rapid electric vehicle (EV) adoption with government-backed penetration targets of 30% by 2030, and industrial automation expansion across manufacturing sectors.

The market's trajectory indicates electrical steel's transition from a specialized industrial input to a fundamental enabler across the country's energy transition, transportation electrification, and industrial productivity initiatives. Supply-side constraints in transformer manufacturing (current capacity of 350,000 MVA against demand of 450,000-460,000 MVA) and localization mandates under the Production Linked Incentive (PLI) scheme are reshaping competitive dynamics, creating both capacity expansion opportunities and margin pressures for market participants.

Key Industry Highlights:

- Product Segment Leadership: Grain-oriented electrical steel commands 65%+ revenue share as the dominant product category (primarily transformer applications), while non-grain-oriented steel grows fastest at 17.5% CAGR, driven by accelerating EV motor demand and industrial motor electrification requirements.

- End-user Dominance: Transformers represent 60%+ revenue share of the market (grid infrastructure and renewable integration applications), while alternators/generators segment fastest at 17.7% CAGR and automotive applications accelerate at 17.8% CAGR, reflecting EV motor demand intensification.

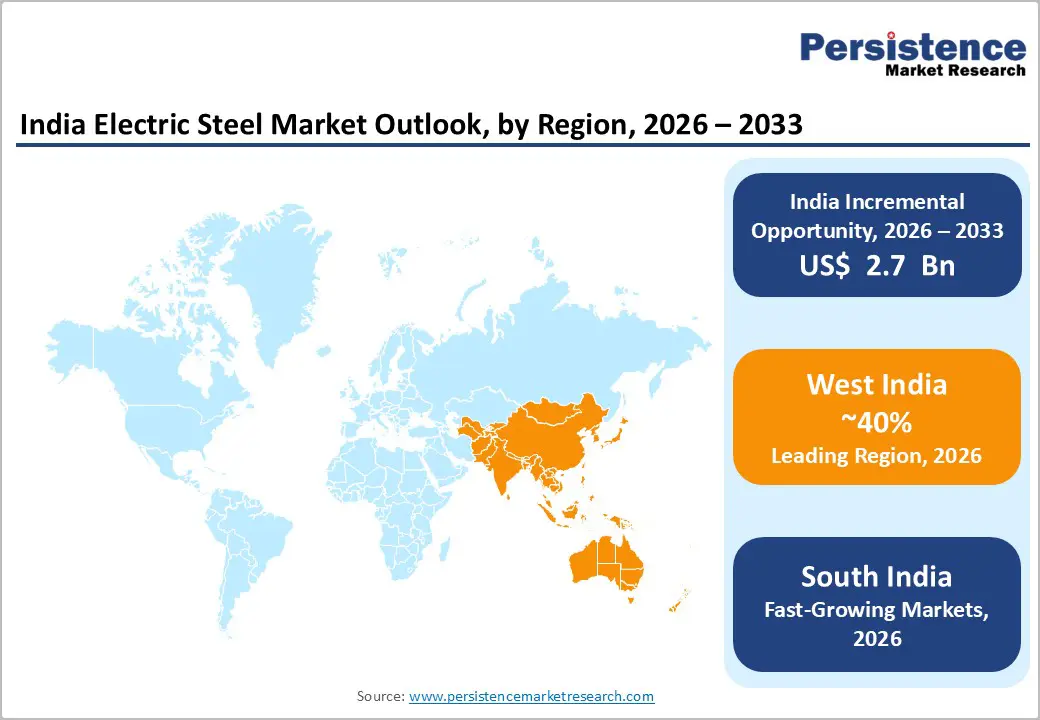

- Regional Growth Leaders: West India maintains 40%+ revenue share through automotive manufacturing concentration and renewable energy infrastructure investment, while South India emerges as the fastest-growing region with 18% CAGR, supported by automotive manufacturing diversification and renewable energy priority investment.

- Supply-Demand Dynamics: Current transformer manufacturing capacity (350,000-370,000 MVA) falls short of rising demand (450,000-460,000 MVA currently; 780,000 MVA target by 2029), creating a structural supply shortage that ensures sustained electrical steel demand growth and pricing support through 2030-31.

- Strategic Capacity Expansion: PLI scheme implementation launched capacity expansion programs across the industry, with Tata Steel targeting US$ 1.2 billion specialty steel capacity investment and SAIL committing Rs 7,500 crore (US$ 875 million) capex in FY26, expected to bring an additional 1.5-2.0 million tonnes of electrical steel capacity online by 2027-28.

| Key Insights | Details |

|---|---|

| India Electrical Steel Market Size (2026E) | US$ 2.7 Bn |

| Market Value Forecast (2033F) | US$ 7.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 16.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.4% |

Market Dynamics

Drivers - Grid Expansion and Renewable Energy Integration

India's energy infrastructure modernization is the primary driver of electrical steel demand. The nation's power sector is pursuing an unprecedented transmission and distribution (T&D) network upgrade to integrate 500 GW of renewable energy by 2030 (280 GW solar and 140 GW wind). This renewable integration imperative requires transformers with superior core materials to minimize energy losses during power transmission, precisely where electrical steel's low core loss and high permeability characteristics provide technical advantages. The Central Electricity Authority (CEA) projects peak electricity demand to rise from 250 GW in FY2024-25 to approximately 458 GW by 2031-32, necessitating simultaneous expansion of transmission infrastructure and distribution substations across both urban and rural geographies.

Government programs including the Revamped Distribution Sector Scheme (with over Rs 3 trillion capex allocation), the Green Energy Corridor initiative (enabling 20 GW renewable evacuation across seven states), and rural electrification schemes (Deendayal Upadhyaya Gram Jyoti Yojana and Saubhagya) are driving consistent transformer demand growth. The distribution transformer procurement index grew by 32.8% in FY2024. Current transformer manufacturing capacity stands at approximately 350,000-370,000 MVA against rising demand of 450,000-460,000 MVA, creating a structural supply-demand gap that projects to reach 780,000 MVA requirement by 2029, ensuring sustained demand for electrical steel as manufacturers scale capacity. This supply-demand mismatch directly translates to volume growth for electrical steel suppliers targeting transformer manufacturers and creates pricing stability for core material suppliers despite competitive pressures in finished transformer markets.

Electric Vehicle Adoption and Motor Electrification

India's electric vehicle sector represents the fastest-growing end-use market for electrical steel, driven by convergent government policies, cost curve improvements, and consumer adoption momentum. EV sales surged from approximately 4,700 units annually in 2018 to nearly 500,000 units in 2023 (representing ~5% of the automotive market), with government targets projecting 30% market penetration by 2030. The Ministry of Power estimates annual EV sales could reach 17 million units by 2030 across all segments. This trajectory translates to exponential demand for high-performance electrical steel in EV motors, which require non-grain-oriented steel for precise electromagnetic control and efficiency optimization compared to conventional internal combustion engine drivetrains.

The FAME (Faster Adoption and Manufacturing of Hybrid and Electric Vehicles) scheme, with a Rs 11,500 crore budget allocation, achieved 69% fund utilization, while the new EV Policy 2024 (featuring reduced import duties) and the Electric Mobility Promotion Scheme (EMPS), with a Rs 5 billion allocation, are accelerating local manufacturing investment. Major automotive OEMs including Tata Motors (US$ 3.08 billion investment over five years), Mahindra & Mahindra (US$ 1.2 billion), Maruti Suzuki (US$ 865.12 million), and MG Motor India (US$ 100 million) have committed substantial capex for EV production capacity. Two-wheelers and three-wheelers dominate current EV sales volume (over 50% and 36% respectively), each requiring electrical steel for motor cores. The global EV population reached 14 million units in 2023, with India's penetration rates accelerating faster than adoption curves in developed markets, creating supply-side urgency for electrical steel dedicated to motor applications. The EV motor market alone was valued at US$ 1.35 billion in 2023 and is projected to reach US$ 4.16 billion by 2030, representing 300% growth, which directly correlates with the acceleration of non-grain-oriented electrical steel consumption.

Restraint - Localization Mandates and Technology Dependency

Government localization policies, while designed to build domestic manufacturing ecosystems, impose transition costs on suppliers and create complexities in technology transfer that moderate near-term growth. The PLI scheme for specialty steel provides production incentives but requires minimum domestic value-addition thresholds and domestic component sourcing commitments, necessitating supply chain restructuring. Electrical steel technology, particularly for grain-oriented variants used in power transformers, remains concentrated among specialized global manufacturers (primarily Japanese and European firms including Nippon Steel, JFE Steel, ArcelorMittal, and ThyssenKrupp), with India's domestic producers still developing equivalent manufacturing capabilities. Domestic producers achieve 60-70% of global efficiency standards in cold-rolling grain-oriented steel, requiring continued technology partnerships and capital investment to close performance gaps.

Localization mandates create supply uncertainty for end users during technology transition periods, particularly when switching from established global suppliers to domestic alternatives that require qualification cycles. Regulatory complexity around compliance documentation, quality certification, and duty structure changes adds administrative overhead to procurement processes. Additionally, preference policies for domestic products may inadvertently limit competition, potentially moderating price competitiveness and innovation incentives in protected market segments.

Opportunity - Green Energy Transition and Transformer Technology Upgrades

Grid modernization initiatives increasingly favor inverter-duty transformers designed for renewable energy integration, solid-state transformers for enhanced grid flexibility, and phase-shifting transformers for dynamic power management, each representing higher-value electrical steel applications than conventional transformer cores. The opportunity extends to distribution transformer upgrades in industrial clusters and urban commercial areas, where smart grid technologies and renewable integration requirements are driving replacement cycles, accelerating beyond historical depreciation schedules. The government's target of 500 GW of renewable capacity by 2030 implies approximately 10,000-12,000 new substations and 40,000-50,000 km of transmission line additions, translating to an estimated electrical steel demand of 2.2-2.5 million tonnes dedicated to transformer applications alone. This addressable opportunity positions electrical steel suppliers for consistent growth as renewable integration progresses through the 2026-2033 forecast period.

Category-wise Analysis

Product Type Insights

India Electrical Steel Market Dynamics Driven by Transformer Efficiency and EV Motor Demand

Grain-oriented (GO) electrical steel dominates the Indian electrical steel market, accounting for over 65% of revenue, primarily due to its superior magnetic performance in transformer applications. Its directional grain alignment significantly reduces core losses and enhances magnetic flux, making it indispensable for both distribution and high-capacity transmission transformers. These efficiency gains directly lower lifecycle energy costs, justifying GO steel’s 15-30% price premium over non-grain-oriented variants. However, domestic production remains constrained, with Indian manufacturers achieving only 60-70% of global efficiency benchmarks in advanced cold-rolling and grain optimization. As a result, premium GO grades continue to be import-dependent. Demand is expected to accelerate at a 14-15% CAGR through 2033, supported by grid modernization, renewable energy integration, and large-scale transformer capacity expansion.

In contrast, non-grain-oriented (NGO) electrical steel represents the fastest-growing segment, expanding at a CAGR of 17.5%. Growth is driven by rising electric vehicle penetration, industrial automation, and demand for high-efficiency motors and generators. NGO steel’s isotropic magnetic properties suit rotating machinery, while evolving motor designs increasingly require ultra-precise thickness control, low core losses at higher operating frequencies, and advanced insulation coatings. Although domestic supply currently meets demand, rapid EV adoption could lead to import reliance after 2028. Despite price pressures and commoditization, premium NGO variants for high-frequency EV and automation applications offer strong differentiation opportunities through technical customization, quality consistency, and reliable supply.

Application Insights

Petrochemical Dominance and Rapid Water Infrastructure Expansion Drive Application Market Dynamics

Transformers constitute the dominant end-product segment in India’s electrical steel market, accounting for over 60% of total revenue, underscoring their central role in the country’s power transmission and distribution infrastructure. Demand is primarily driven by large-scale grid expansion to integrate renewable energy, significant transmission capacity additions aligned with India’s 500 GW renewable target, and the replacement of aging transformer assets in distribution networks. A persistent transformer manufacturing capacity shortfall of nearly 100,000-110,000 MVA continues to support strong pricing and volume growth for transformer-grade electrical steel through the 2026-2033 period. Distribution transformers in the 10-100 MVA range dominate unit volumes, with 45,000-50,000 installations expected annually, favoring high-quality grain-oriented steel for efficiency and reduced lifecycle losses. Larger transmission transformers, though fewer in number, consume substantially higher steel tonnage per unit. Long procurement cycles and utility-approved specifications create predictable demand and pricing stability, despite moderate exposure to infrastructure execution delays.

In contrast, alternators and generators represent the fastest-growing segment, expanding at a 17.7% CAGR. Growth is driven by renewable energy integration and rising demand for backup power systems across industrial and commercial users. This segment increasingly favors premium non-grain-oriented electrical steel optimized for high-speed, high-efficiency operation, offering material suppliers opportunities for customization-led differentiation.

Energy Infrastructure Dominates Electrical Steel Demand as Electric Vehicles Accelerate Automotive Growth

Energy and power generation remains the dominant end-use segment in the India electrical steel market, accounting for over 55% of total revenue. This leadership reflects the indispensable role of electrical steel in India’s electricity infrastructure, particularly in transformer cores, generators, and power conditioning equipment. Virtually every unit of electricity consumed passes through multiple transformers, making electrical steel fundamental to transmission and distribution networks. Demand is reinforced by rising electricity consumption driven by urbanization, industrial expansion, and transport electrification, alongside renewable energy integration that requires extensive transformer capacity upgrades. Ongoing grid modernization programs focused on efficiency and reliability further strengthen long-term demand stability. Peak electricity demand is projected to increase from 250 GW in FY2024-25 to 458 GW by 2031-32, supporting sustained electrical steel consumption that outpaces overall GDP growth, although policy delays and financing constraints remain potential risks.

In contrast, automotive applications represent the fastest-growing end-use segment, expanding at a CAGR of 17.8%, primarily due to electric vehicle adoption. EV motors rely on high-performance NGO electrical steel to achieve superior efficiency, directly influencing driving range and operating costs. While passenger EV penetration remains modest, rapid electrification of two-wheelers and three-wheelers is driving volume growth. Government targets of 30% EV penetration by 2030 imply a multi-fold increase in motor production, creating strong opportunities for suppliers developing advanced electrical steel solutions optimized for next-generation motor technologies.

Country Insights and Trends

West India Leads India’s Electrical Steel Market Through Manufacturing and Renewable Energy Growth

West India dominates the Indian electrical steel market, accounting for over 40% of total revenue, driven by its strong concentration of industrial production, automotive manufacturing, and power infrastructure investments across Gujarat, Maharashtra, and Rajasthan. Gujarat’s role as a major automotive manufacturing hub, hosting production facilities of leading OEMs such as Maruti Suzuki, Tata Motors, and Mahindra & Mahindra, generates sustained demand for electrical steel through dense supplier and component manufacturing networks. In parallel, the state’s ambitious renewable energy targets-50 GW of solar and 30 GW of wind capacity-are accelerating transformer and grid equipment demand, reinforcing the region’s leadership in electrical steel consumption.

The region benefits from advanced industrial infrastructure, integrated steel and specialty steel facilities, and favorable manufacturing-oriented government policies, resulting in efficient supply chains and lower logistics costs. Maharashtra’s Pune and Aurangabad automotive clusters further strengthen regional demand through concentrated motor and drive system manufacturing. Looking ahead, Gujarat’s Green Energy Corridor and Phase II renewable evacuation plans, targeting nearly 20 GW, are expected to drive 18-20% electrical steel demand growth during 2026-2033. The market remains relatively consolidated, with a few dominant suppliers ensuring pricing discipline and consistent quality, while opportunities exist for specialized, application-specific electrical steel grades.

South India Emerges as Fastest Growing Equipment Market Driven by Renewables Automotive

South India has emerged as the fastest-growing regional market, registering an estimated CAGR of 18%, driven by concentrated renewable energy investments, expanding automotive manufacturing, and rapid industrial automation across Tamil Nadu, Telangana, and Karnataka. The region’s strong renewable energy potential, particularly solar capacity additions in Telangana and Tamil Nadu and wind installations along coastal corridors, is attracting a disproportionately high share of capital inflows. This momentum is further reinforced by Green Energy Corridor Phase II projects, which are creating sustained demand for transmission infrastructure and associated transformer and generator components.

Automotive manufacturing activity is increasingly shifting toward southern states, positioning the region as an alternative production hub beyond West India. Announced and ongoing OEM investments are catalyzing localized supply chains, accelerating demand for electrical steel, motors, and allied components at a pace exceeding the national average. Tamil Nadu’s diversified industrial ecosystem, spanning automotive components, textiles, and petrochemicals, is additionally supporting rising motor and automation-related demand.

Market dynamics in South India are shaped by relatively lower supplier concentration, with multiple regional players competing across product categories, resulting in a more competitive pricing environment. While supply chain maturity varies by state, this gap presents clear opportunities for suppliers investing in new distribution networks and technical partnerships. Supportive state-level policies focused on renewable energy and manufacturing are expected to sustain above-average growth through the forecast period.

Competitive Landscape

The India electrical steel market is characterized by moderate consolidation, with the top five manufacturers accounting for approximately 70-75% of total revenue, while secondary and regional players together hold the remaining 25-30%. Market concentration differs by product category. Grain-oriented (GO) electrical steel is more consolidated, with the top three suppliers controlling nearly 65-70% of the segment, reflecting high technical entry barriers and stringent quality requirements. In contrast, the non-grain-oriented (NGO) segment is relatively fragmented, with the top five players holding 55-60%, due to lower technical complexity and more commodity-like characteristics.

Tata Steel leads the market with an estimated 25-28% share, supported by integrated operations, advanced cold-rolling technology, and strong relationships with utility and automotive OEMs. SAIL follows with 18-22%, benefiting from extensive domestic distribution and preference in government-backed infrastructure projects, particularly in NGO grades. JSW Steel holds 12-15% share, driven by expanding specialty steel capabilities and increasing focus on automotive electrical steel optimization. Secondary suppliers, including ArcelorMittal and Nippon Steel, collectively account for 30-35%.

Competition is shaped less by pricing and more by technical qualification, grade customization, delivery reliability, and sustainability credentials. Backward integration provides cost and supply advantages to large players, while high capital requirements-estimated at US$ 200-300 million for new specialized facilities-are expected to keep market concentration largely stable through 2033.

Key Industry Developments

- In August 2025, JFE Steel and JSW Steel approved a major expansion of GOES capacity in India, investing about ¥120 billion to strengthen competitiveness and capture surging electrical steel demand nationwide grid upgrades.

Companies Covered in India Electrical Steel Market

- Tata Steel Limited

- SAIL (Steel Authority of India Limited)

- JSW Steel Limited

- Nippon Steel India Limited

- ArcelorMittal India Private Limited

- Essar Steel (Integrated Operations)

- Liberty Steel India

- Transformers & Rectifiers India Limited

- Emerson Electric Electrical Steel Division

- Siemens Energy India

- Hitachi Energy India

- Mahindra & Mahindra Electrical Motors

- ABB India Limited

- Havells India Limited

- Kirloskar Electric Company Limited

- Other Market Players

Frequently Asked Questions

The India Electrical Steel Market is estimated to be valued at US$ 2.7 Bn in 2026.

The primary demand driver for India’s electrical steel market is the rapid expansion and modernization of the power transmission and distribution (T&D) network, driven by rising electricity consumption, renewable energy integration, and grid reliability upgrades.

In 2026, the West India region will dominate the market with an exceeding 40% revenue share in the India Electrical Steel market.

Among product types, Grain-oriented Electrical Steel has the highest preference, capturing beyond 65% of the market revenue share in 2026, surpassing other product types.

Tata Steel Limited, SAIL (Steel Authority of India Limited), JSW Steel Limited, Nippon Steel India Limited, Arcelor Mittal India Private Limited, Essar Steel (Integrated Operations), Liberty Steel India, and Transformers & Rectifiers India Limited are a few leading players in the India electrical steel market.