- Automotive Components & Materials

- Automotive Electrical Products Market

Automotive Electrical Products Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Electrical Products Market: by Product Type (Light Equipment, Automotive Batteries, Automotive Connectors, Alternators & Starters, Ignition Systems & Parts and Others), by Application (ADAS, Infotainment, Body Electronics, Safety Systems and Powertrain Electronics), by Vehicle Type (Passenger Vehicles, LCV and HCV) and Regional Analysis for 2026 - 2033

Automotive Electrical Products Market Size and Trends Analysis

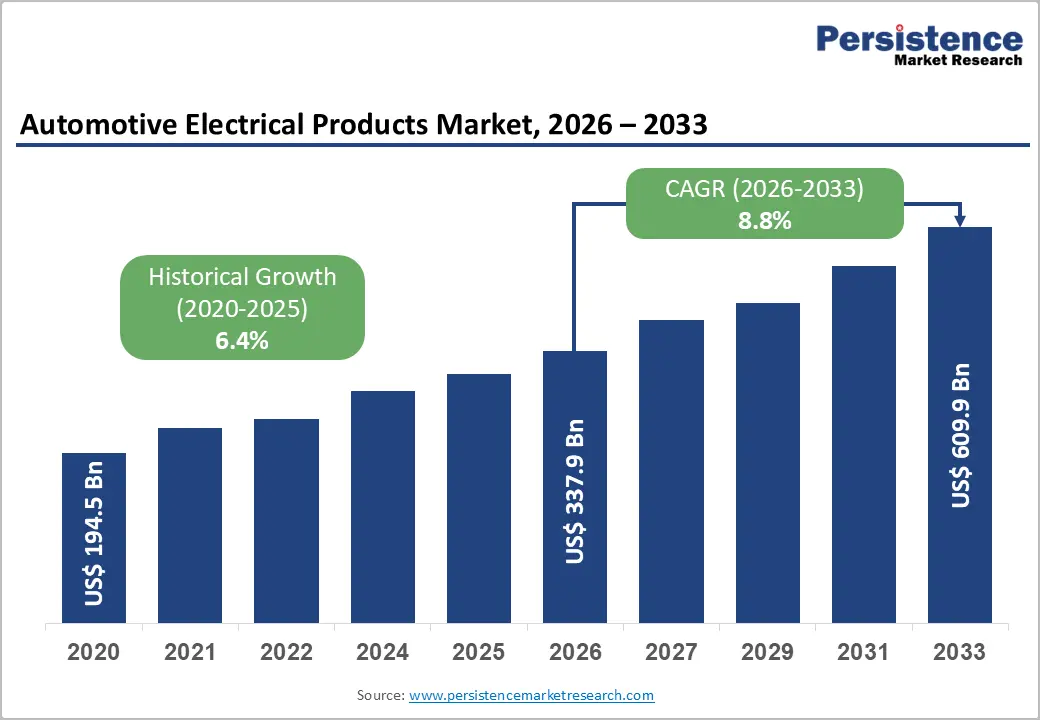

The global automotive electrical products market size is likely to be valued at US$ 337.9 Bn in 2026 and is projected to reach US$ 609.9 Bn by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

The automotive electrical products market is experiencing sustained expansion driven by accelerating vehicle electrification, with electric vehicle (EV) sales surpassing 17 million units in 2024, a 25% year-over-year increase, and continuing momentum through Q1 2026 with over 4 million EV units sold globally.

Key Industry Highlights:

- Dominant Segment Leadership: Automotive Batteries command 35.4% product type market share, supported by EV sales exceeding 17 million units in 2024 and battery demand reaching 950 GWh with 25% year-over-year growth, establishing baseline growth supporting sustained electrical component demand.

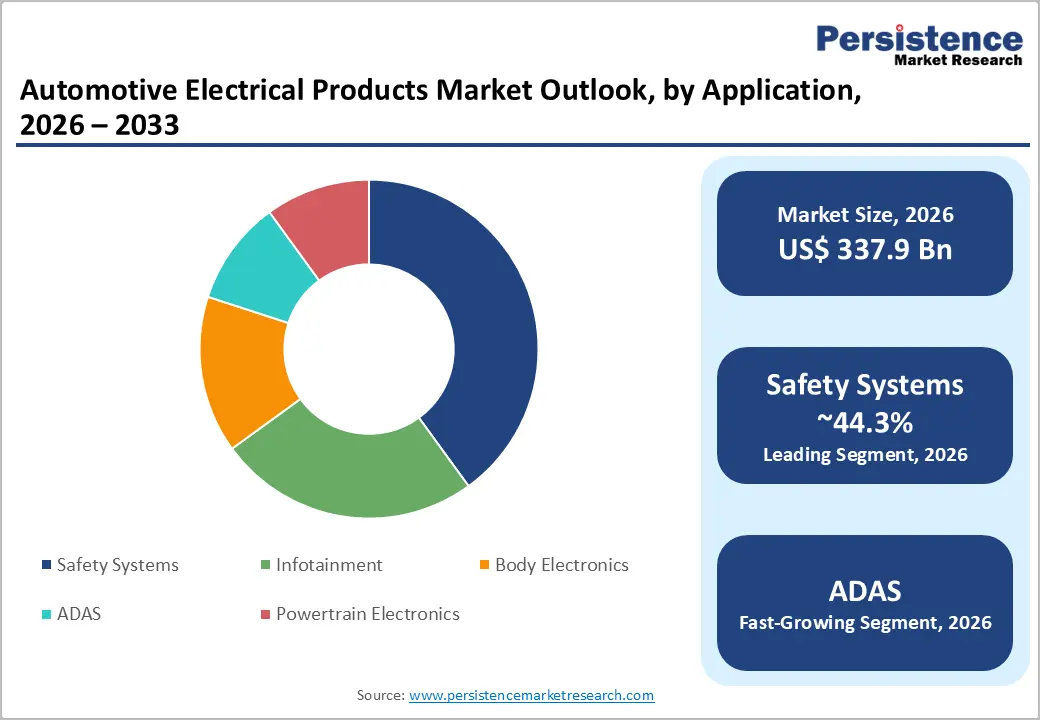

- Safety Systems Application Dominance: The Safety Systems segment maintains a 44.3% market share across automotive electrical applications, while Advanced Driver Assistance Systems (ADAS) is the fastest-growing application category, growing at 30%+ annually, driven by regulatory mandates across North America, Europe, and Asia-Pacific.

- Passenger Vehicle Market Leadership with LCV Growth: Passenger Vehicles command a 62.4% market share, while Light Commercial Vehicles are the fastest-growing segment, driven by e-commerce expansion, urban logistics demand, and accelerating LCV electrification, outpacing overall vehicle electrification growth.

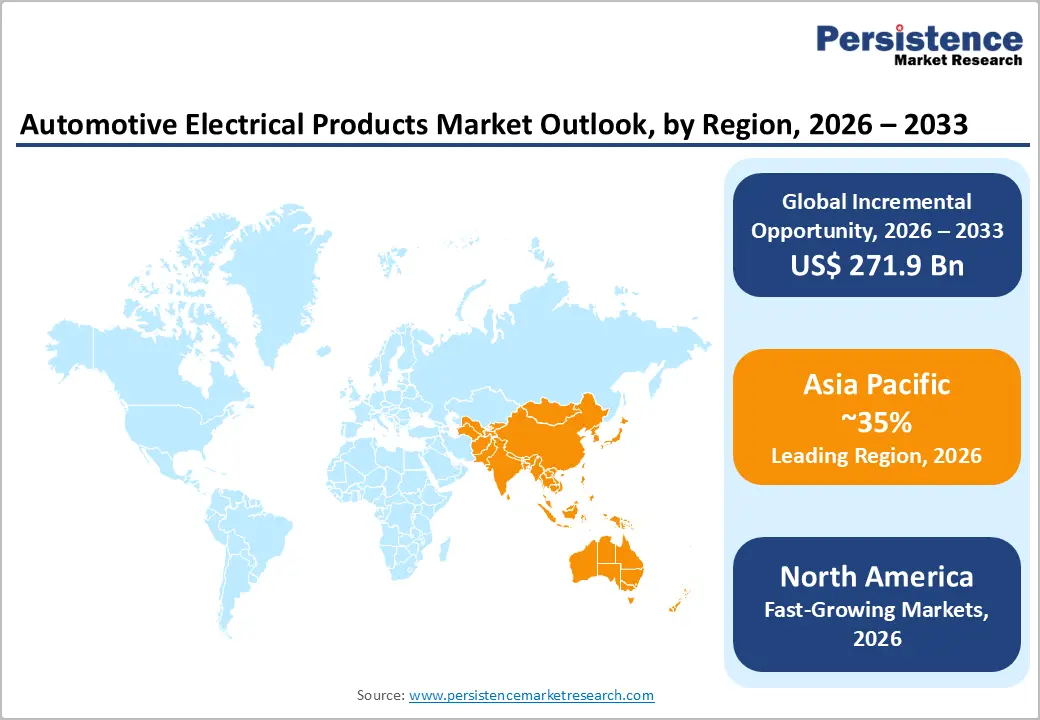

- Asia Pacific Regional Acceleration: The Asia Pacific region is projected to deliver a 10% CAGR, led by China's 60% global EV sales dominance and 80% concentration of battery cell production, establishing manufacturing scale advantages and supply chain integration that support the fastest regional growth through 2033.

| Key Insights | Details |

|---|---|

| Automotive Electrical Products Market Size (2026E) | US$ 337.9 Bn |

| Market Value Forecast (2033F) | US$ 609.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.8% |

| Historical Market Growth (CAGR 2020 to 2024) | 6.4% |

Market Dynamics

Drivers - Vehicle Electrification and Battery Demand Acceleration

Vehicle electrification is the primary market driver, with global electric vehicle sales exceeding 17 million units in 2024, reflecting 25% year-over-year growth and establishing a precedent for continued sector expansion. EV battery demand exceeded 950 GWh in 2024, reflecting 25% growth versus 2023, with demand concentration increasingly shifting toward high-capacity battery systems (201-300 kWh and above) supporting electric SUVs, trucks, and long-range passenger vehicles.

China dominates global EV manufacturing, accounting for approximately 60% of global EV sales, and controls 80% of global battery cell production, thereby establishing manufacturing leadership that supports component supply chain integration. Battery electric vehicles (BEVs) comprise over 70% of EV demand, requiring sophisticated electrical architectures including battery management systems, power distribution modules, high-voltage connectors, and thermal management systems driving incremental component demand. Q1 2026 global EV sales exceeded 4 million units, signaling sustained momentum as government electrification targets establish baselines.

Advanced Driver Assistance Systems Regulatory Mandates and Safety Compliance Requirements

Advanced Driver Assistance Systems (ADAS) integration represents the second major driver, with regulatory mandates establishing universal baseline requirements across major automotive markets. European Union compliance rates reached 70% for vehicles equipped with Level 1 ADAS features (lane-keeping assist, adaptive cruise control, automatic emergency braking), driven by EU General Safety Regulation (GSR) establishing mandatory equipment standards. North American regulatory frameworks, including FMVSS standards and NHTSA requirements, mandate collision avoidance and crash mitigation system implementation, with an estimated strong annual growth of up to 30% for Level 2 ADAS through 2026.

ADAS integration requires substantial electrical infrastructure, including radar sensors, LiDAR systems, camera modules, ultrasonic sensors, and electronic control units (ECUs) supporting real-time processing and system coordination. The automotive electronics market addressing ADAS applications is projected to expand at 8.6% CAGR through 2033, substantially outpacing traditional automotive component growth trajectories.

Restraints - Raw Material Cost Volatility and Supply Chain Complexity

Automotive electrical products manufacturing relies on critical materials, including copper, lithium, cobalt, nickel, and rare-earth elements, creating exposure to substantial commodity price fluctuations that affect production economics. Supply chain disruptions from geopolitical tensions, semiconductor shortages, and logistics network constraints continue to create procurement delays and cost uncertainty. Battery raw material costs remain volatile, with lithium prices fluctuating significantly, affecting battery component costs and automotive manufacturer profitability. Semiconductor chip availability constraints, although improving from pandemic-era peaks, continue to limit production capacity for electronic control units and sensor systems, thereby restricting market growth.

Electric Vehicle Adoption Rate Variability and Regional Market Disparities

EV adoption rates demonstrate substantial geographic variation, with Europe achieving 70% ADAS adoption compared to emerging market penetration rates of 15-25%, creating uneven demand distribution across electrical component categories. Infrastructure development gaps in charging networks, particularly in developing economies, constrain EV adoption prospects and consequently limit growth in electrical product demand. Consumer purchasing power variations across regions affect average vehicle price points and consequently electrical component integration levels, with premium segment vehicles commanding substantially higher electrical content versus budget vehicle segments.

Opportunities - Advanced Battery Management Systems and Integrated Power Electronics for Electric Vehicle Platforms

Battery management systems (BMS) represent the most significant growth opportunity, with the EV battery market projected to expand from $92.7 billion in 2026 to $181.8 billion by 2033 (representing 10.1% CAGR), driven by global EV adoption accelerating toward 20+ million annual sales by 2026. Integrated power electronics solutions that combine inverters, converters, and thermal management systems address the high-voltage electrical architecture requirements of next-generation EV platforms. 48V mild hybrid systems represent an expanding opportunity segment, offering cost-effective electrification for internal combustion engine vehicles, with estimated market penetration projected to reach 30-40% of global vehicle production by 2033. Integrated starter-generator (ISG) systems address energy-efficiency requirements while supporting start-stop technology and regenerative braking, thereby increasing electrical component demand across hybrid and conventional vehicle segments.

Software-Defined Vehicle Architecture and Vehicle-to-Everything (V2X) Connectivity Infrastructure

Software-defined vehicle (SDV) architecture transformation creates substantial opportunities for electrical products, with OEMs transitioning from distributed electronic control units (ECUs) toward centralized computing architectures that require sophisticated zonal controllers, domain control modules, and high-speed communication networks. Vehicle-to-Everything (V2X) connectivity integration, enabling vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I), and vehicle-to-cloud (V2C) communication, requires advanced connectivity modules, antenna systems, and protocol integration to support autonomous driving development and fleet management optimization. Autonomous vehicle platform development across Level 3 and Level 4 autonomy requires substantial electrical infrastructure investment, including sensor fusion modules, AI-capable processors, and fail-safe control systems, with an estimated market sizing projecting a $15-20 billion opportunity within autonomous vehicle electrical systems through 2033.

Category-wise Analysis

Product Type Insights

Automotive Batteries maintain dominant market positioning within product segmentation, commanding 35.4% market share and representing the foundational component supporting vehicle electrification initiatives globally. Battery systems encompass diverse configurations from 48-50 kWh systems (conventional hybrid vehicles) through 200+ kWh installations (long-range electric vehicles and commercial applications), with market concentration increasingly shifting toward larger capacity systems supporting SUV electrification and truck applications. Battery demand growth reflects momentum toward passenger-vehicle electrification, with battery-electric vehicles accounting for 70% of EV sales in 2026 and requiring increasingly sophisticated battery management systems (BMS) that incorporate real-time monitoring, thermal regulation, and predictive maintenance algorithms.

The fastest-growing product segment comprises Ignition Systems and Parts, reflecting emerging technologies including advanced starter systems, integrated power modules, and intelligent voltage regulators supporting 48V electrification, start-stop technology, and regenerative braking system integration across both conventional and hybrid vehicle architectures.

Application Insights

Safety Systems command a dominant application position, with a 44.3% market share, encompassing anti-lock braking systems (ABS), electronic stability control (ESC), airbag control modules, and emission control systems that require sophisticated electrical infrastructure and real-time processing capabilities. Safety systems are universal requirements across all vehicle categories, supported by stringent regulatory mandates from FMVSS (North America), NHTSA, and EU GSR standards, creating non-discretionary baseline demand.

Advanced Driver Assistance Systems (ADAS) represent the fastest-growing application category, with annual growth rates exceeding 30% through 2026 driven by regulatory requirements, consumer safety preferences, and automotive manufacturer competitive differentiation strategies. ADAS integration requires substantial electrical component investment, including camera modules, radar/LiDAR sensor systems, ultrasonic sensors, electronic control units with advanced processing capabilities, and communication modules supporting inter-system coordination, establishing escalating electrical product demand as ADAS sophistication advances toward Level 3 and Level 4 autonomous driving capabilities.

Vehicle Type Insights

Passenger Vehicles maintain dominant market share at 62.4%, reflecting highest global production volumes (approximately 70 million units annually) and universal electrical component requirements across all market segments. Passenger-vehicle dominance reflects broad consumer demand for connectivity features, safety systems, infotainment integration, and emerging electrification, thereby establishing baseline component demand across all electrical product categories.

Light Commercial Vehicles (LCVs) constitute the fastest-growing vehicle segment, driven by e-commerce expansion, urban logistics development, and investment in last-mile delivery infrastructure, which require specialized electrical systems that support extended operating cycles, meet heavier-duty requirements, and integrate fleet management telematics. LCV electrification is accelerating rapidly, with commercial vehicle operators prioritizing cost reduction through EV adoption despite higher capital expenditures relative to conventional alternatives, thereby driving increased demand for electrical components in this segment.

Regional Market Insights

North America Automotive Electrical Products Market Share

North America maintains dominant market position driven by U.S. automotive manufacturing leadership and strong OEM presence including Ford, General Motors, Tesla, and established Tier-1 suppliers (Bosch, Continental, Denso) maintaining significant regional manufacturing and distribution operations. The north American market benefits from the FMVSS and NHTSA regulatory framework, establishing mandatory safety technology deployment requirements, with regulatory alignment driving consistent electrical product demand across major manufacturers. Commercial vehicle dominance in the alternator and starter motor segments reflects an 80.2% market share for these components, driven by logistics sector expansion and heavy-duty vehicle operational requirements that sustain component demand.

The U.S. EV adoption trajectory, established by federal incentives and state-level emission regulations, supports gradual electrification momentum, with government projections indicating 25% EV market penetration by 2030. Innovation ecosystem concentrated in California, Michigan, and Texas drives ADAS development, battery technology advancement, and autonomous vehicle platform creation, establishing regional technological leadership. Tier-1 supplier consolidation and strategic partnerships between OEMs and electrical component manufacturers characterize the competitive landscape, with integrated electrical system solutions becoming a key differentiation mechanism.

Europe Automotive Electrical Products Market Share

Europe demonstrates a world-leading ADAS adoption rate of 70% for vehicles equipped with Level 1 systems, driven by the EU General Safety Regulation (GSR) establishing mandatory equipment standards and strong consumer safety preferences. European automotive market emphasizes electrification commitment, with national targets establishing binding EV adoption requirements (Germany, France, Spain) supporting sustained electrical product demand growth. Germany's automotive leadership in electrical system innovation reflects Bosch, Continental, and ZF manufacturing presence and advanced technology development capabilities supporting Level 3 autonomous vehicle platform commercialization.

Regulatory harmonization efforts through EU directives create standardized technical requirements across member states, facilitating manufacturer economies of scale in electrical product development. ADAS system penetration continues accelerating toward market saturation, with 40+ state governments establishing autonomous vehicle testing frameworks creating demonstration markets for advanced electrical system integration. European supply chain maintains competitive cost positioning through manufacturing excellence, engineering capabilities, and strategic supplier networks supporting continued regional market competitiveness.

Asia Pacific Automotive Electrical Products Market Trends

Asia Pacific emerges as the fastest-growing region with 10% CAGR projection through 2035, driven by China's dominant EV market, capturing 60% of global EV sales and 80% of global battery cell production, establishing manufacturing scale advantages. China's aggressive electrification targets supported by government incentives, charging infrastructure investment, and domestic OEM competition (BYD, NIO, XPeng) create unprecedented electrical product demand growth.

India's EV adoption trajectory is accelerating rapidly, with the government PM Surya Ghar program supporting distributed renewable energy, supporting gradual electrification pathway aligned with 40% EV target by 2030. Japan's automotive technology leadership in autonomous vehicle development, advanced sensors, and connectivity systems drives regional innovation momentum.

Competitive Landscape

The global automotive electrical products market is marked by fierce competitiveness among major companies seeking to boost their market presence through innovation, strategic alliances, and broadening their product lines. Firms are making significant investments in research and development to produce lightweight, durable, and efficient balance shafts. Innovations such as forged balance shafts are gaining popularity due to their compact size and effective natural damping properties. Additionally, as regulatory pressures to lower greenhouse gas emissions rise, manufacturers are concentrating on creating balance shafts that enhance fuel efficiency and decrease vehicle emissions. This trend is encouraging the use of balance shafts in both passenger cars and commercial vehicles.

Key Industry Developments:

- In Jan 2024, YAZAKI expanded its product portfolio with the launch of high-voltage harness solutions for EVs and plug-in hybrids. This development addresses the growing demand for 800V architectures, already adopted by 26% of new electric vehicle models. YAZAKI’s new line improves power transmission efficiency by nearly 19% and supports rapid EV battery charging.

- In June 2024, Fujikura launched flexible printed harnesses using polyimide film, reducing harness volume by 16% and improving thermal resistance. This product is being deployed in more than 35% of premium electric vehicle models in collaboration with Japanese and European OEMs, enhancing durability in high-vibration environments.

Companies Covered in Automotive Electrical Products Market

- Altera (Intel Corporation)

- BBB Industries Ltd

- Broadcom Ltd.

- Continental AG

- DENSO CORPORATION

- Hella Gmbh & Co. Kgaa (Hella)

- Hitachi Automotive Systems, Ltd.

- Infineon Technologies AG

- Microchip Technology, Inc.

- NXP Semiconductors N.V.

- Others Key Players

Frequently Asked Questions

The Automotive Electrical Products market is estimated to be valued at US$ 337.9 Bn in 2026.

The key demand driver for the Automotive Electrical Products market is the rapid increase in vehicle electrification and the growing integration of electronic systems across all vehicle segments.

In 2026, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Automotive Electrical Products market.

Among the Application Type, Inline 4 Cylinder holds the highest preference, capturing beyond 44.3% of the market revenue share in 2026, surpassing other Application Type.

The key players in Automotive Electrical Products are Altera (Intel Corporation), BBB, Industries Ltd, Broadcom Ltd., Continental AG and DENSO CORPORATION.