- Inks, Coatings, Adhesives & Sealants (ICAS)

- Electrically Conductive Coatings Market

Electrically Conductive Coatings Market Size, Share, and Growth Forecast, 2026 - 2033

Electrically Conductive Coatings Market by Product Type (Polyesters, Epoxy, Polyurethanes, Acrylics), Application (Electrical & Electronics, Automotive, Medical, Aerospace, Military), and Regional Analysis for 2026 - 2033

Electrically Conductive Coatings Market Size and Trends Analysis

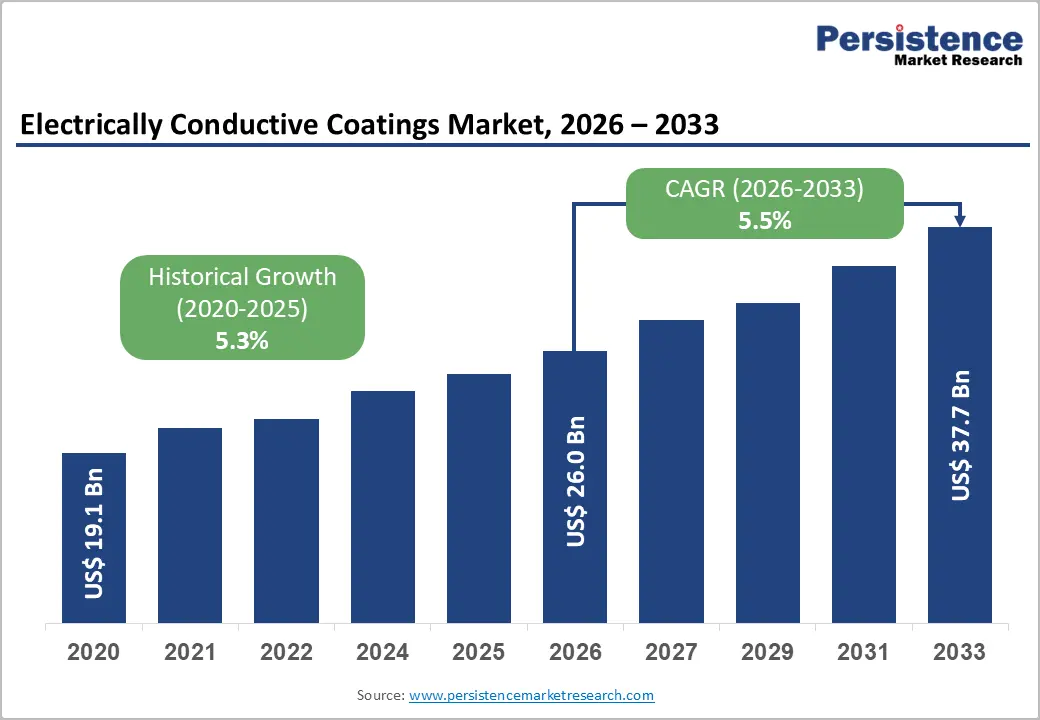

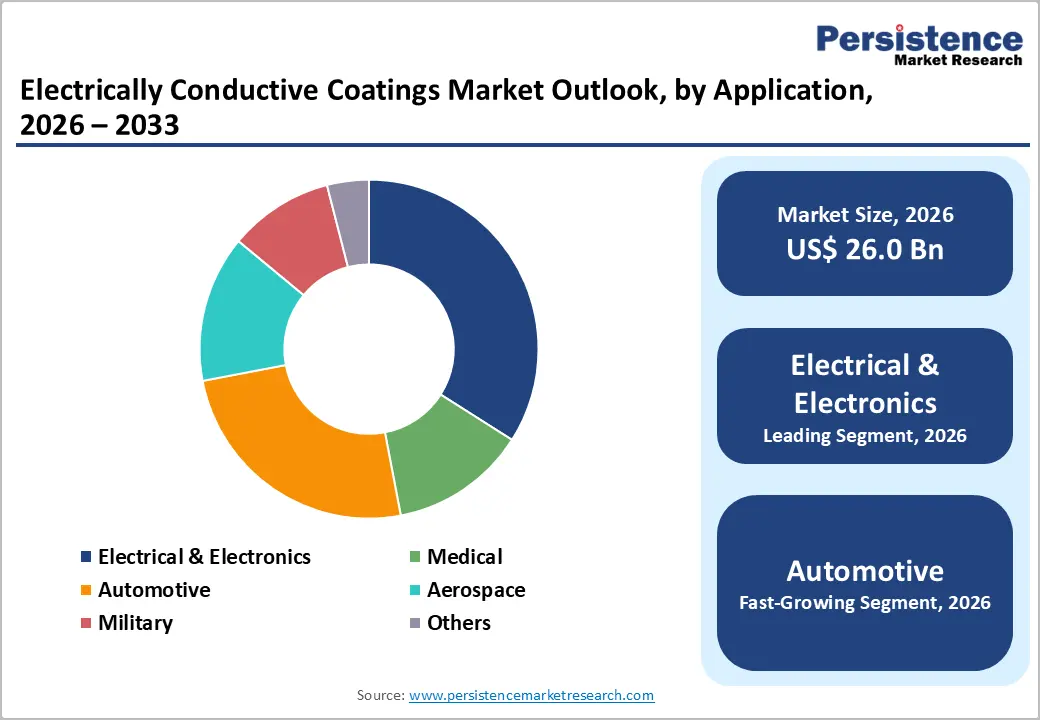

The global electrically conductive coatings market size is likely to be valued at US$26.0 billion in 2026 and is expected to reach US$37.7 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033, driven by increasing demand in the electronics sector for EMI/RFI shielding, anti-static protection, and miniaturized device applications amid the 5G rollout, alongside rising adoption in the automotive industry, particularly in electric vehicles, and in aerospace and defense for lightweight and high-performance conductive solutions.

Growth is supported by technological advancements in conductive fillers, including silver, copper, and carbon-based materials, as well as the development of water-based and low-VOC coatings to meet environmental regulations. Expanding applications in medical devices, renewable energy systems, and wearable electronics, coupled with increasing regulatory and performance requirements.

Key Industry Highlights:

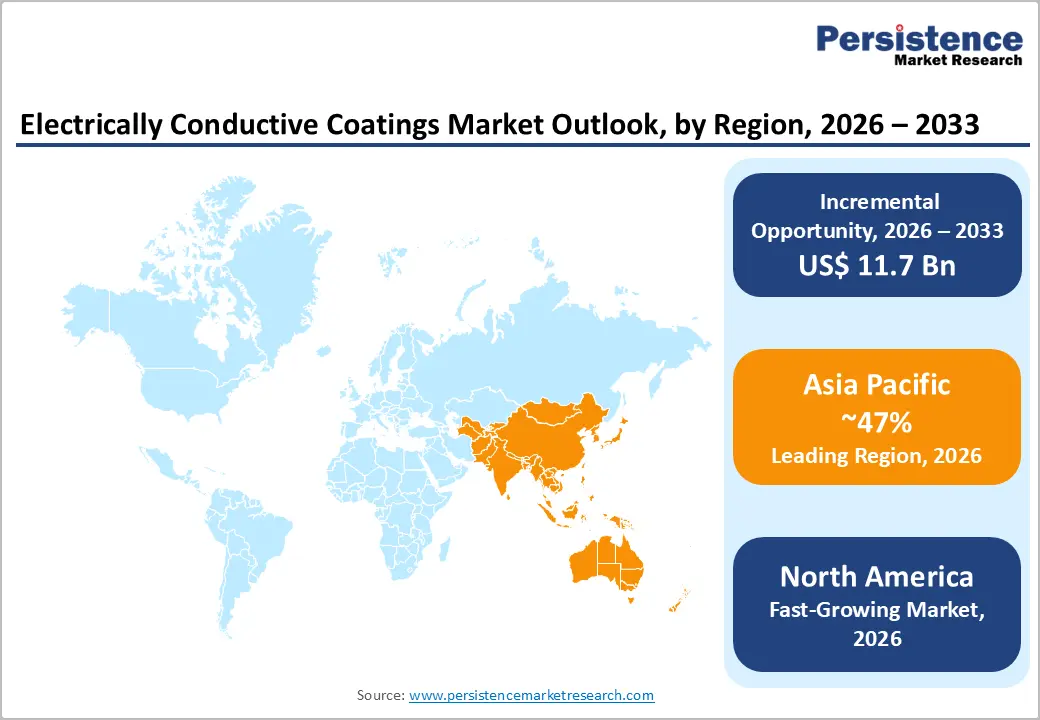

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 47% in 2026, driven by the presence of established electronics and automotive industries, advanced R&D infrastructure, and growing adoption of electric vehicles and aerospace applications.

- Fastest-growing Region: North America is likely to be the fastest-growing region, supported by rapid adoption of electric vehicles, increasing aerospace and defense investments, advanced electronics manufacturing, and strong R&D initiatives.

- Leading Product Type: Polyesters are projected to represent the leading product type in 2026, accounting for 35% of the revenue share, driven by their balanced properties of flexibility, durability, and conductivity, making them ideal for electronics and automotive applications.

- Leading Application: The electrical & electronics segment is anticipated to be the leading application type, accounting for over 42% of the revenue share in 2026, supported by growing demand for EMI/ESD protection in consumer electronics, telecom devices, and miniaturized components.

| Key Insights | Details |

|---|---|

|

Electrically Conductive Coatings Market Size (2026E) |

US$26.0 Bn |

|

Market Value Forecast (2033F) |

US$37.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis- Rising Demand from the Electrical & Electronics Sector

The rising demand from the electrical and electronics industry, where coatings are essential for EMI/RFI shielding, anti-static protection, and maintaining electrical conductivity in miniaturized and high-performance devices. Rapid growth in smartphones, tablets, laptops, and printed circuit boards is pushing manufacturers to adopt advanced coatings that ensure signal integrity, device reliability, and thermal stability. As the electronics sector expands, particularly in Asia-Pacific and North America, demand for coatings that combine durability, conductivity, and cost-effectiveness continues to rise, making this sector a major revenue contributor.

The proliferation of 5G technology, IoT devices, and wearable electronics has intensified the need for high-performance coatings. Conductive coatings ensure long-term reliability in devices exposed to electromagnetic interference and static discharge. Manufacturers are focusing on silver, copper, and carbon-based fillers to enhance performance in increasingly compact components. Strong investments in electronics manufacturing hubs, such as China, Japan, and the U.S., also drive steady adoption.

Solar and Renewable Energy Adoption

Conductive coatings play a critical role in solar and renewable energy systems by enhancing efficiency and reliability in photovoltaic panels, inverters, and energy storage systems. Conductive coatings reduce resistive losses and protect components against environmental degradation, enabling longer system lifespans. Government policies encouraging renewable energy investments in regions such as Europe, North America, and Asia Pacific are stimulating market demand. As solar installations, wind energy projects, and battery storage solutions expand, manufacturers increasingly require coatings that provide both high conductivity and environmental durability to meet performance standards.

Renewable energy systems demand high-performance conductive coatings that withstand UV exposure, temperature variations, and moisture. Advanced fillers, including silver, copper, and graphene-based materials, are being incorporated to meet these requirements. The drive toward decarbonization and sustainability accelerates adoption, creating a lucrative market opportunity. Companies developing environmentally compliant, efficient coatings can capture a growing share of the renewable energy segment. The combination of technological advancements, supportive policies, and expanding solar and renewable projects continues to fuel growth in conductive coatings for sustainable energy applications.

Barrier Analysis - Regulatory and Environmental Compliance Hurdles

Manufacturers invest in eco-friendly, water-based, or low-VOC formulations, which can increase production costs and affect profit margins. Compliance with REACH, EPA, and local environmental standards adds complexity, particularly for small or regional players. Legacy solvent-based coatings are increasingly restricted, requiring material reformulation, testing, and certification to meet standards. Regulatory hurdles slow product adoption and market expansion in regions with stricter environmental laws, affecting overall growth potential.

Regulatory pressures also influence research and development priorities, compelling companies to balance performance with sustainability. Non-compliance can result in fines, market restrictions, and reputational risks. Frequent updates to environmental standards require continuous monitoring and adaptation, increasing operational challenges. While large multinational players can absorb these costs, smaller manufacturers may face barriers to entry, limiting competition. These compliance requirements act as a restraint on rapid market expansion, particularly in high-growth regions such as Europe and North America.

Technical Challenges in Dispersion and Application Quality

Technical difficulty of achieving uniform dispersion of conductive fillers, such as silver, copper, or carbon-based materials. Uneven distribution can result in inconsistent conductivity, reduced adhesion, and compromised performance, particularly in thin-film applications. Coating quality is also affected by substrate compatibility, curing processes, and environmental factors, requiring precise control during manufacturing. These technical challenges can limit production scalability and reduce efficiency, impacting cost-effectiveness. High-performance applications, such as aerospace, automotive, EV components, and medical devices, demand strict quality control, adding complexity to the manufacturing process.

Application challenges include achieving consistent layer thickness, ensuring strong adhesion, and maintaining performance under mechanical stress and thermal cycling. Manufacturers must invest in advanced dispersion technologies, mixing equipment, and R&D to overcome these issues. Failure to address these technical barriers can lead to product defects, reduced reliability, and customer dissatisfaction, limiting market penetration. Continuous innovation in coating formulations and application methods is necessary to mitigate these risks.

Opportunity Analysis - Flexible Electronics and Wearables

These applications require lightweight, flexible, and durable conductive layers that maintain performance under bending, stretching, and repeated mechanical stress. Advanced fillers such as silver nanowires, graphene, and carbon nanotubes are increasingly used to meet the conductivity and flexibility requirements of flexible displays, sensors, and medical wearables. As wearable adoption grows, particularly in North America, Europe, and Asia-Pacific, manufacturers can capitalize on this segment by offering high-performance, compliant, and thin coatings tailored for next-generation electronics.

Flexible electronics demand coatings that are environmentally stable, durable, and compatible with diverse substrates, including polymers and textiles. The trend toward miniaturization and multifunctional devices expands market potential, enabling conductive coatings to play a critical role in signal transmission, shielding, and anti-static protection. Companies investing in innovative, flexible coating solutions can capture a growing share of the wearable and flexible electronics market.

EV Infrastructure Expansion

Coatings are essential in battery packs, charging stations, power electronics, and wiring systems to enhance conductivity, reduce heat generation, and provide EMI shielding. Government initiatives promoting EV adoption, sustainable mobility, and clean energy are accelerating market demand in the U.S., Europe, and China. Manufacturers developing lightweight, durable, and cost-effective conductive coatings for automotive applications can benefit from increasing EV production and infrastructure investments.

As EV technology evolves, the need for efficient thermal management, lightweight components, and durable coatings becomes critical. Conductive coatings also support high-voltage systems, charging equipment, and energy storage solutions, increasing their importance in the EV ecosystem. Expansion of EV charging networks, energy storage systems, and supportive government policies enhances growth prospects. Companies offering innovative, high-performance coatings are well-positioned to capitalize on this emerging segment, making EV infrastructure a significant opportunity for market expansion and revenue growth.

Category-wise Analysis

Product Type Insights

Polyesters are projected to dominate the electrically conductive coatings market, accounting for approximately 35% of total revenue in 2026. This leadership is driven by their well-balanced properties, including reliable electrical conductivity, flexibility, chemical resistance, and cost-effectiveness. These characteristics make polyester-based conductive coatings highly suitable for applications such as electronics housings, connectors, and automotive electronic components, where durability and stable performance are critical. Polyesters offer strong adhesion to both plastic and metal substrates, supporting their widespread use in high-volume manufacturing processes. They are extensively utilized in consumer electronics enclosures and internal shielding layers, where they deliver effective electromagnetic interference (EMI) protection while enabling lightweight and compact device designs.

Polyurethanes are likely to represent the fastest-growing segment, supported by rising demand for highly flexible, impact-resistant, and lightweight conductive coatings. Their superior elasticity and adhesion make them ideal for applications requiring repeated bending, stretching, or movement. Polyurethane coatings are increasingly adopted in electric vehicles and wearable electronics, where traditional rigid coatings may fail under mechanical stress. These materials also offer a favorable balance between conductivity performance and cost, supporting broader adoption across emerging applications. For example, polyurethane-based conductive coatings are widely used in EV battery pack enclosures, where flexibility, vibration resistance, and EMI shielding are essential.

Application Insights

The electrical and electronics segment is projected to lead the market, accounting for around 42% of total revenue in 2026, supported by sustained demand for EMI/RFI shielding and electrostatic discharge protection in consumer electronics and telecommunications equipment. The rapid expansion of smartphones, laptops, servers, and 5G infrastructure has significantly increased demand for coatings that ensure signal integrity and device reliability. These coatings provide an efficient solution without adding excessive weight or thickness. For example, conductive coatings are widely used in smartphone internal housings and shielding layers, where effective EMI protection is essential to prevent signal interference among densely packed components.

The automotive segment is likely to be the fastest-growing application, driven by accelerating vehicle electrification, EV adoption, and advanced driver-assistance systems. Modern vehicles contain a growing number of electronic components requiring EMI shielding, grounding, and thermal stability. Conductive coatings are increasingly used in battery systems, power electronics, sensors, and charging components, supporting efficiency and safety. Light-weighting mandates encourage the replacement of traditional metal shielding with advanced conductive coatings. For example, their use in EV charging connectors, where conductive coatings improve electrical performance while reducing component weight.

Regional Insights

North America Electrically Conductive Coatings Market Trends

North America is likely to be the fastest-growing region, driven by strong demand from electronics, aerospace, automotive, and defense sectors. The U.S. market dominates the region, supported by mature manufacturing ecosystems, advanced research capabilities, and early adoption of next-generation technologies, particularly in EMI/RFI shielding and current management applications. For example, PPG Industries Inc., a North American player expanding its conductive coatings portfolio to serve automotive OEMs and EV supply chains with advanced formulations tailored to high-voltage and EMI shielding applications.

Market trends in North America point toward innovation in material technologies, sustainability, and additive manufacturing integration. There is growing emphasis on the development of eco-friendly, low-VOC and water-based coatings to satisfy tightening regulatory requirements under U.S. EPA and related state standards, pushing formulators toward greener chemistries without sacrificing performance. Another emerging trend is the integration of conductive coatings with printed electronics and 3D printing, enabling lightweight circuitry and flexible substrates for IoT devices, wearables, and advanced industrial electronics.

Europe Electrically Conductive Coatings Market Trends

Market growth in Europe is driven by sustainability, regulatory compliance, and advanced manufacturing leadership. With Europe holding a meaningful portion of the market supported by automotive electrification, aerospace manufacturing, and industrial electronics demand, eco-friendly and low VOC conductive formulations are increasingly prioritized to align with EU regulatory frameworks and the Green Deal initiatives. For example, Akzo Nobel N.V.’s European operations have focused on tailored conductive coating solutions that comply with REACH and low-emission guidelines while supporting automotive and aerospace production lines with enhanced EMI performance.

Innovation and sectoral diversification define market trends in Europe, driven by the rapid expansion of electric mobility and renewable energy initiatives. As automotive manufacturers transition toward electric vehicle platforms, conductive coatings are increasingly used in battery modules, power electronics enclosures, and charging infrastructure, where durability, lightweight performance, and reliable conductivity are essential. Beyond the automotive sector, Europe’s aerospace and defense industries are adopting these coatings to meet stringent requirements for EMI shielding and lightning protection in avionics and other critical systems.

Asia Pacific Electrically Conductive Coatings Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 47% in 2026, driven by rapid industrialization, extensive electronics manufacturing, and expanding automotive production across China, Japan, and India. China alone leads regional consumption due to its role as the world’s largest electronics producer, supplying advanced consumer devices, telecommunications equipment, and industrial electronics that require EMI shielding, ESD protection, and conductive pathways in compact designs. The region's strong supply chain integration, cost-effective production capabilities, and export-oriented manufacturing hubs reinforce Asia Pacific leadership position.

Amid this growth landscape, companies within the Asia Pacific are expanding capacities and refining technologies to meet evolving performance and sustainability criteria. For example, Henkel AG & Co. KGaA, which has been actively enhancing its conductive coatings portfolio tailored for Asia’s automotive and electronics sectors, including products optimized for EV components and high-frequency shielding in telecommunications modules. This reflects a broader regional trend where manufacturers invest in R&D, localized production, and partnerships with OEMs and tier suppliers to capture rising demand in dynamic end-use industries.

Competitive Landscape

The global electrically conductive coatings market exhibits a moderately fragmented structure, driven by a mix of established multinationals and innovative regional specialists competing for market share in electronics, automotive, aerospace, and industrial applications. These leaders leverage continuous R&D investment, extensive manufacturing footprints, and customer service excellence to maintain their positions against both midsize formulators and niche innovators focused on specialty coatings such as nanomaterial-enhanced and eco-friendly formulations.

With key leaders including PPG Industries, Henkel AG & Co. KGaA, and AkzoNobel N.V., the competitive landscape is shaped by product innovation, strategic partnerships, and sustainability initiatives. These players compete through enhanced formulation technologies, development of low-VOC and water-based coatings, and collaborations with electronics and automotive OEMs to tailor solutions for EMI shielding, EV components, and advanced electronics. Strategic activities such as capacity expansions, acquisitions, and ecosystem partnerships help firms extend their geographic reach and adapt to evolving regulatory and performance demands.

Key Industry Developments:

- In October 2025, Axalta announced the launch of two advanced powder coatings, Alesta e-PRO FG Black and Alesta e-PRO Dielectric Gray, specifically designed for electric vehicle (EV) battery applications. The new coatings address critical requirements for heat protection, fire resistance, and electrical insulation in EV battery systems. Alesta e-PRO FG Black offers high thermal stability and secondary fire protection, maintaining integrity under extreme heat and direct flame exposure, while Alesta e-PRO Dielectric Gray provides strong electrical insulation performance for high-voltage battery packs and energy storage systems.

- In April 2025, Henkel announced the launch of advanced AI-enabled virtual adhesives, next-generation conductive and safety coatings, and innovative debonding technologies for electric vehicle (EV) batteries, showcased at The Battery Show Europe 2025. The new solutions include AI-generated digital adhesives to shorten battery development cycles, conductive electrode coatings to enhance battery performance, mica-replacement safety coatings offering high thermal and electrical protection, and structural adhesive debonding technologies to support battery repair, reuse, and recycling.

Companies Covered in Electrically Conductive Coatings Market

- PPG Industries Inc.

- Axalta Coating Systems

- Henkel AG & Co. KGaA

- The Sherwin-Williams Company

- AkzoNobel N.V.

- Creative Materials Inc.

- MG Chemicals

- Fluoro Precision Coatings

Frequently Asked Questions

The global electrically conductive coatings market is projected to reach US$26.0 billion in 2026.

Rising demand for EMI/ESD protection in electronics, growing electric vehicle adoption, and increasing use of advanced electronic systems across automotive, aerospace, and energy applications.

The electrically conductive coatings market is expected to grow at a CAGR of 5.5% from 2026 to 2033.

Expansion of flexible and wearable electronics, rising renewable energy installations, and increasing demand for lightweight, high-performance conductive coatings.

PPG Industries Inc., Henkel AG & Co. KGaA, Axalta Coating Systems, and The Sherwin-Williams Company are the leading players.