- Electrical Equipment & Services

- Electrical Testing Services Market

Electrical Testing Services Market Size, Share, and Growth Forecast 2025 - 2032

Electrical Testing Services Market Analysis by Service Type(Transformer Testing, Circuit Breaker Testing, Battery Testing, Others), End-user (Power Generation Stations, Transmission Distribution System Data Centers), Testing Standards Compliance (IEC Standards, ASTM Standards, NEMA Standards), and Regional Analysis 2025 - 2032

Electrical Testing Services Market Share and Trends Analysis

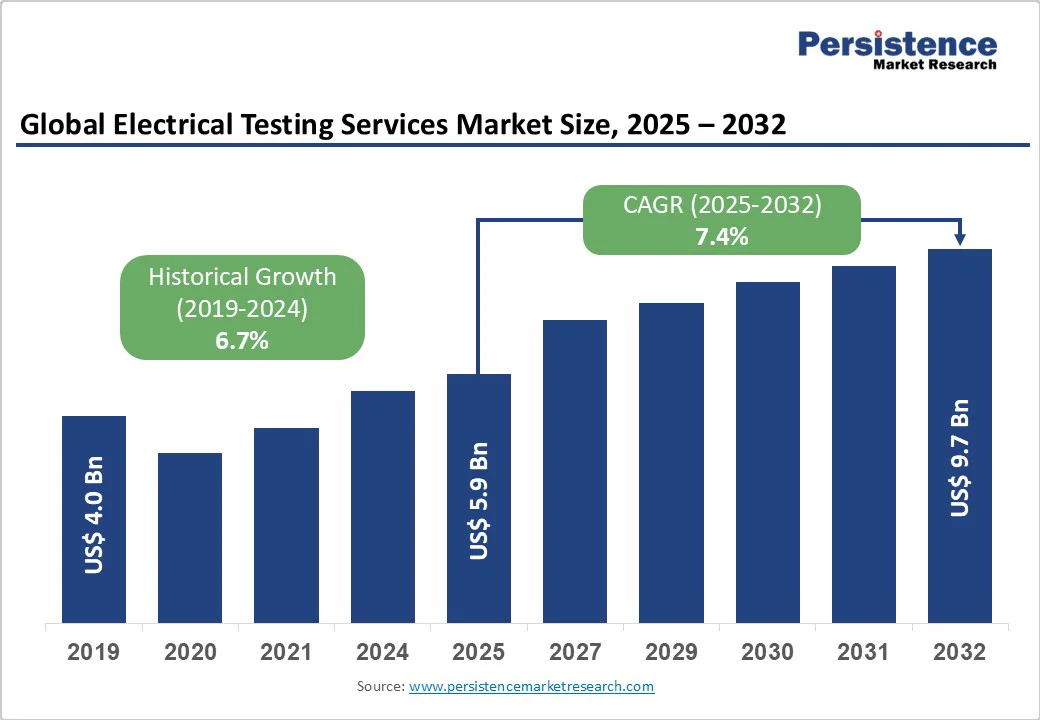

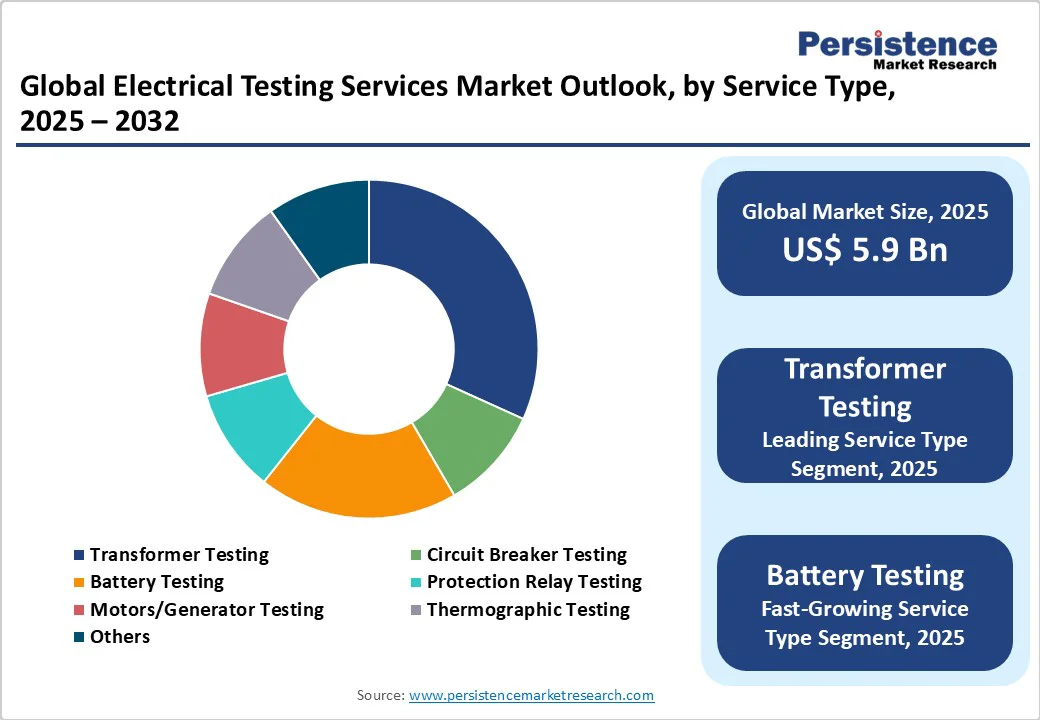

The global electrical testing services market size was valued at US$5.9 Bn in 2025 and is projected to reach US$9.7 Bn by 2032, growing at a CAGR of 7.4% between 2025 and 2032. The growth trajectory reflects the increasing demand for reliable electrical infrastructure validation driven by aging power grids that require modernization, stringent safety regulations, and the rapid expansion of renewable energy installations necessitating comprehensive testing protocols.

Key Market Highlights

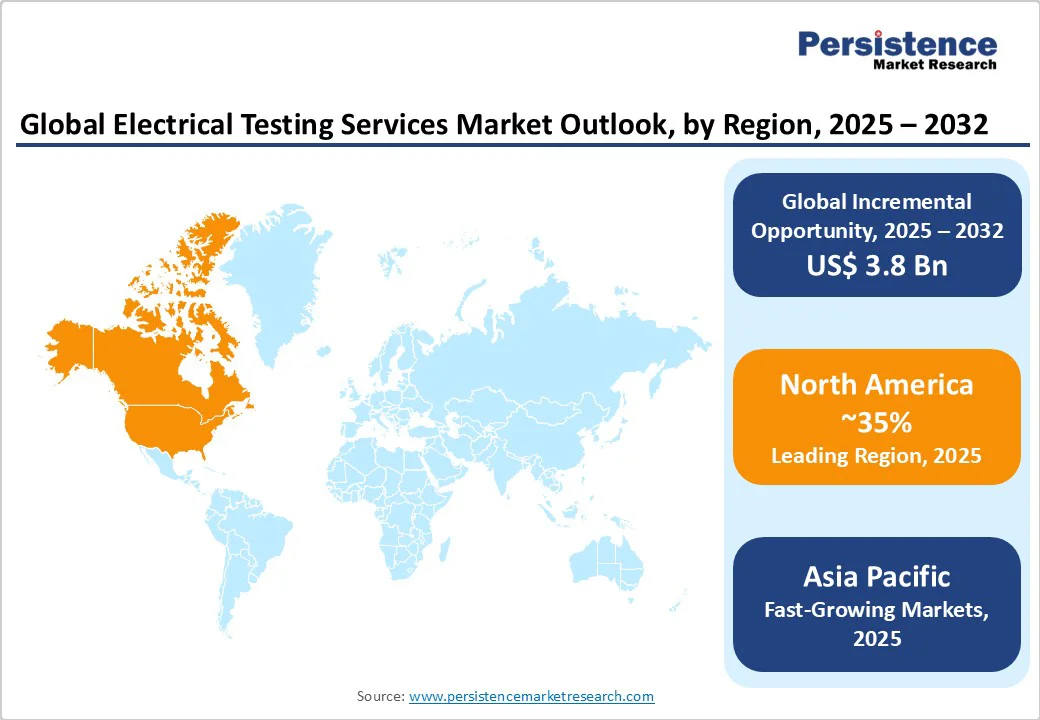

- Leading Region: North America leads the global electrical testing services market through extensive power grid modernization initiatives and stringent OSHA regulatory frameworks, driving sustained demand across utility and industrial sectors.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing regional market, propelled by China’s manufacturing expansion, India’s renewable energy commitments, and infrastructure development across ASEAN countries.

- Leading Services Segment: Transformer Testing dominates the service categories with a 35% market share, reflecting the critical infrastructure reliability requirements and aging power grid modernization needs worldwide.

- Leading Testing Standards Compliance: IEC Standards compliance represents the fastest-growing segment, with a 38% market share, driven by global harmonization trends and the adoption of the CB Scheme for international market access.

- Key Opportunity: Renewable energy integration testing presents the most significant market opportunity, supported by a projected 400% growth in renewable capacity and 500 GW capacity targets in major markets.

| Key Insights | Details |

|---|---|

|

Electrical Testing Services Market Size (2025E) |

US$5.9 Billion |

|

Market Value Forecast (2032F) |

US$9.7 Billion |

|

Projected Growth CAGR (2025–2032) |

7.4% |

|

Historical Market Growth (2019–2024) |

6.7% |

Market Dynamics

Driver - Grid Modernization and Infrastructure Upgrades Drive Testing Demand

The global power grid infrastructure modernization initiative represents a significant growth catalyst for electrical testing services, with utilities worldwide investing heavily in upgrading aging electrical systems that are over 30 years old. North American utilities are leading this transformation, implementing smart grid technologies and renewable energy integration projects that require comprehensive testing protocols to ensure system reliability and safety.

The expansion of the power quality instruments market directly correlates with these infrastructure investments, as utilities seek advanced monitoring and testing capabilities to maintain grid stability during the transition to distributed energy systems. These modernization efforts necessitate extensive transformer testing, circuit breaker validation, and protection relay calibration, creating sustained demand for specialized electrical testing services across transmission and distribution networks.

Stringent Regulatory Compliance Requirements

The implementation of increasingly rigorous safety standards by regulatory bodies, including OSHA, IEEE, IEC, and NEMA, is compelling organizations across industries to prioritize comprehensive electrical testing protocols. European Union directives, particularly the Low Voltage Directive (LVD) 2014/35/EU, mandate extensive electrical safety testing for equipment compliance, driving substantial demand for certification services.

The growth of the electrical compliance and certification market reflects this regulatory environment, as companies adhere to multiple international standards, including IEEE 1613 for power grid equipment and IEC 61850-3 for substation communications. These compliance requirements generate recurring revenue streams for testing service providers, as organizations must undergo periodic recertification and ongoing monitoring to maintain regulatory approval across diverse market jurisdictions.

Restraint - High Capital Investment Requirements for Advanced Testing Equipment

The electrical testing services industry faces significant barriers due to the substantial capital investments required for acquiring and maintaining sophisticated testing equipment. Modern Test and Measurement Equipment Market solutions demand considerable financial resources for implementation and calibration. Service providers must continually upgrade their instrumentation to support emerging technologies and comply with evolving testing standards, creating ongoing financial pressures that particularly impact smaller testing organizations. The preference among end-users for equipment rental over purchase further constrains market growth, as organizations seek to minimize capital expenditure by accessing testing services on a temporary basis rather than investing in permanent solutions.

Shortage of Skilled Technical Personnel

The electrical testing services sector faces persistent challenges related to the availability of qualified technical personnel who can operate complex testing equipment and interpret sophisticated diagnostic results. The specialized nature of electrical testing requires extensive training and certification, creating workforce development bottlenecks that limit service capacity and market expansion potential. This skills gap is particularly pronounced in emerging markets, where technical education infrastructure may be insufficient to meet growing demand for electrical testing expertise.

Market Opportunities - Renewable Energy Integration Testing Services

The rapid expansion of renewable energy installations worldwide presents exceptional growth opportunities for electrical testing service providers, particularly in solar and wind power integration projects requiring specialized grid connection testing protocols. British Petroleum estimates indicate a 400% growth in renewable energy by 2040, creating unprecedented demand for DC testing capabilities as renewable sources generate primarily direct current compared to traditional alternating current systems.

India’s commitment to achieve 500 GW of non-fossil fuel capacity by 2030 exemplifies the scale of testing opportunities emerging in developing markets, where comprehensive electrical validation services are essential for successful renewable energy deployment. Advanced testing methodologies, including power quality analysis, grid stability assessment, and inverter testing, are becoming critical services as utilities integrate distributed energy resources while maintaining system reliability and regulatory compliance.

Electric Vehicle Infrastructure Testing Market

The global transition toward electric mobility is generating substantial demand for specialized electrical testing services focused on EV charging infrastructure and battery systems, with companies like DEKRA reporting 500 monthly EV battery tests in 2024 alone. The expansion of electric vehicle charging networks requires comprehensive testing of high-voltage systems, safety protocols, and grid interconnection standards, creating new service categories within the electrical testing market.

Future Mobility testing services are projected to grow by 200% compared to 2022 levels by 2025, reflecting the automotive industry's accelerating shift toward electrification and the associated infrastructure development requirements. This market segment encompasses not only charging station validation but also advanced driver assistance systems testing and connected vehicle functionality assessment, positioning electrical testing providers to capture significant revenue from the evolving transportation landscape.

Category-wise Insights

Service Type Analysis

Transformer Testing emerges as the dominant service segment, capturing approximately 35% of the global electrical testing services market due to the critical role of transformers in power transmission and distribution systems. The prevalence of aging transformer infrastructure across global power grids necessitates regular diagnostic testing to prevent catastrophic failures and ensure operational reliability.

Power utilities and industrial facilities prioritize transformer testing services, including insulation resistance measurement, dissolved gas analysis, and turn ratio testing, to optimize maintenance schedules and extend equipment lifespan. The Test and Measurement Equipment Market growth directly supports this segment, as transformer testing requires sophisticated instrumentation capable of analyzing complex electrical parameters and identifying potential failure modes before they impact system performance.

End User Analysis

Power Generation Stations represent the leading end-user segment, accounting for approximately 32% of market demand, driven by the critical nature of electrical equipment reliability in power production facilities. Nuclear power plants, with over 450 reactors operating globally and an additional 50 under construction, require extensive electrical testing protocols to ensure the functionality of safety systems and regulatory compliance.

The segment's dominance reflects the high-stakes environment of power generation, where equipment failures can result in significant economic losses and safety risks. Renewable energy facilities, particularly solar and wind installations, are contributing increasingly to this segment's growth, as they require specialized testing for grid integration, power quality monitoring, and inverter performance validation.

Testing Standards Compliance Analysis

IEC Standards compliance represents the largest market segment, with an approximate 38% share, reflecting the global adoption of International Electrotechnical Commission protocols for electrical equipment testing and certification. The widespread acceptance of IEC standards across international markets makes them the preferred framework for manufacturers seeking global market access through the CB Scheme certification process. IEEE

Standards maintain significant market presence, particularly in North American markets, where protocols such as IEEE 1613 for power grid communications and IEEE 43 for insulation testing are extensively utilized. The Electrical Compliance and Certification Market expansion supports this segment's growth as organizations require adherence to multiple international standards to access diverse geographic markets and satisfy regulatory requirements across different jurisdictions.

Regional Insights

North America Electrical Testing Services Trends

North America maintains market leadership in electrical testing services, driven by extensive power grid modernization initiatives and stringent regulatory frameworks enforced by OSHA and other federal agencies. The region's mature industrial infrastructure requires comprehensive testing protocols to maintain operational reliability, with United States utilities investing significantly in smart grid technologies and renewable energy integration projects. Intertek and other major testing service providers have established extensive networks across North America, offering NRTL certification services that enable manufacturers to access both US and Canadian markets through standardized testing protocols.

The regulatory environment in North America emphasizes electrical safety compliance, with OSHA requirements mandating that virtually all electrical devices in workplace environments meet relevant UL standards and obtain certification from nationally recognized testing laboratories. This regulatory framework creates sustained demand for electrical testing services across industrial, commercial, and utility applications, positioning North America as a primary growth market for testing service providers.

Europe Electrical Testing Services Trends

European markets demonstrate strong growth in electrical testing services, driven by harmonized regulatory standards and the implementation of the Low Voltage Directive (LVD) 2014/35/EU, requiring comprehensive electrical safety compliance. Germany, the United Kingdom, France, and Spain lead regional demand through their advanced manufacturing sectors and commitment to renewable energy deployment. European testing providers benefit from the CE marking process, which requires extensive validation of electrical safety for products marketed within the European Union.

The region's emphasis on environmental sustainability and energy efficiency drives demand for specialized testing services supporting renewable energy projects and smart grid implementations. European testing laboratories operate under UKAS accreditation systems, providing manufacturers with access to global markets through CB Scheme participation and reducing duplicate testing requirements across international jurisdictions.

Asia Pacific Electrical Testing Services Trends

Asia Pacific represents the fastest-growing regional market for electrical testing services, with China, Japan, and India leading expansion through massive infrastructure development projects and industrial growth. China’s substantial manufacturing base and India’s commitment to 500 GW of renewable energy capacity by 2030 create unprecedented demand for comprehensive electrical testing services. Japan’s mature industrial infrastructure and emphasis on technological innovation foster sophisticated testing requirements across electronics, automotive, and energy sectors.

The region benefits from significant foreign investment in manufacturing and infrastructure projects, with Vietnam and other ASEAN countries emerging as important growth markets for electrical testing services. Asia Pacific’s manufacturing advantages and cost-competitive service delivery position the region as a global hub for electrical testing, with international companies establishing testing facilities to serve both regional and global markets.

Competitive Landscape

The global electrical testing services market exhibits a moderately fragmented structure with several established global players competing alongside regional specialists and niche service providers. Market concentration is characterized by the presence of major multinational testing organizations such as Intertek, TÜV SÜD, Element, and DEKRA, which leverage extensive laboratory networks and comprehensive accreditation portfolios to serve diverse industry verticals. These market leaders employ expansion strategies focused on geographic penetration, technological capability enhancement, and strategic acquisitions to strengthen their competitive positions.

Key Developments:

- In September 2024, DEKRA introduced its Digital Trust Service, combining functional safety, cybersecurity, and AI testing into a single integrated certification offering. This streamlined approach is designed to accelerate product innovation timelines, enabling manufacturers to address multiple compliance requirements more efficiently and strengthen trust in advanced digital and connected systems.

- In May 2024, Intertek signed a Master Services Agreement with Korea Testing & Research Institute, enhancing cooperation through the CB Scheme. The collaboration improves global market access for electrical and electronic manufacturers by offering harmonized testing and certification, helping companies achieve compliance faster and expand into international markets more seamlessly.

- In April 2024, DEKRA launched a patented EV battery testing technology, performing around 500 battery health assessments per month. This innovation supports the rising used electric vehicle market by providing reliable safety and performance validation, helping manufacturers, dealers, and consumers build confidence in second-life EVs while ensuring sustainability in the mobility ecosystem.

Companies Covered in Electrical Testing Services Market

- Intertek

- TÜV SÜD

- Element

- Applus+ Laboratories

- QAI

- EMC Technologies

- JM Test Systems

- Carelabs

- Saf-T-Gard International

- Clever Compliance

- RN Electronics

- DEKRA

- FORCE Technology

- ITC India

- LabTest

- UL Solutions

- CSA Group

- Bureau Veritas

- SGS

- Eurofins

Frequently Asked Questions

The global electrical testing services market is projected to reach US$ 9.7 billion by 2032, growing from US$ 5.9 billion in 2025 at a CAGR of 7.4% during the forecast period.

Key growth drivers include power grid modernization initiatives, stringent regulatory compliance requirements from OSHA, IEEE, and IEC, aging infrastructure upgrades, and rapid renewable energy integration projects worldwide.

Transformer Testing represents the dominant service segment with approximately 35% market share, driven by critical infrastructure reliability requirements and the need for preventive maintenance of aging power grid equipment.

Asia Pacific exhibits the fastest regional growth, led by China’s manufacturing expansion, India’s commitment to 500 GW renewable energy capacity by 2030, and substantial infrastructure development across emerging ASEAN markets.

Renewable energy integration testing presents the largest growth opportunity, supported by British Petroleum’s projection of 400% renewable energy growth by 2040 and the expanding EV charging infrastructure requiring specialized testing protocols.