- Food Ingredients & Additives

- Dry Molasses Market

Dry Molasses Market Size, Share, and Growth Forecast 2026 - 2033

Dry Molasses Market by Source (Sugarcane, Sugar beet, Others), by Form (Powdered Dry Molasses, Granular, Flakes, Others), End-user (Food Industry, Crop Protection, Animal Feed, Nutraceuticals, Other), Distribution Channel (Business to Business, Business to Consumer), and Regional Analysis, from 2026 - 2033

Dry Molasses Market Share and Trends Analysis

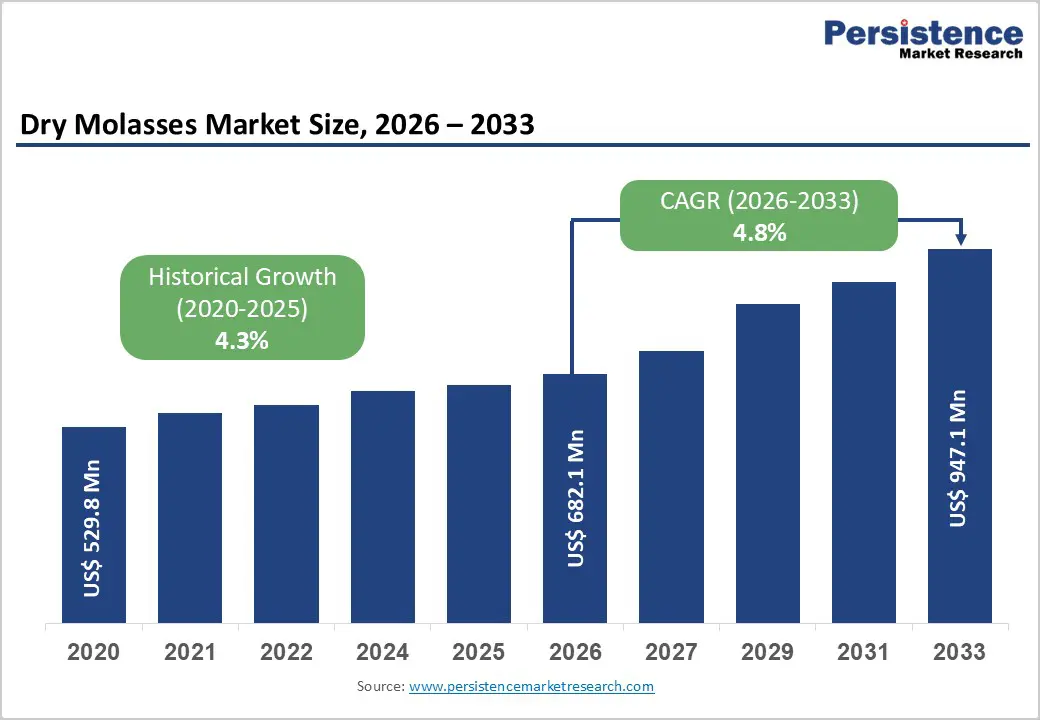

The global Dry Molasses Market size is expected to be valued at US$ 682.1 million in 2026 and projected to reach US$ 947.1 million by 2033, growing at a CAGR of 4.8% between 2026 and 2033.

The market is expanding due to increasing applications across food processing, animal nutrition, crop protection, and nutraceuticals, driven by demand for natural sweeteners, organic fertilizers, and functional feed additives. Growth is supported by rising consumer preference for clean-label products, sustainable agriculture practices, and the nutritional benefits of molasses in both human and animal diets. Expanding livestock sectors and organic farming trends further reinforce steady demand.

Key Industry Highlights:

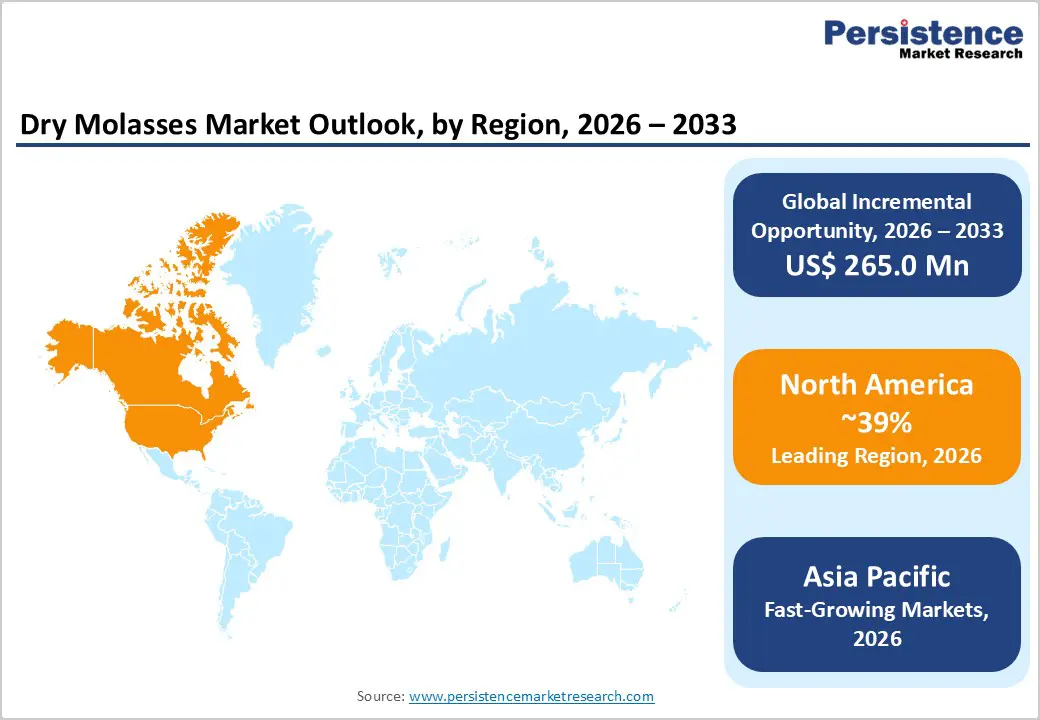

- North America dominates Dry Molasses Market with 39% share in 2025, driven by U.S. livestock demand and processing infrastructure.

- Asia Pacific grows fastest through India/China feed demand and organic farming expansion in ASEAN countries.

- Sugarcane source leads with ~65% share due to abundant supply from Brazil, India, Thailand.

- Granular form expands rapidly for precision agriculture and dust-free industrial handling applications.

- Major opportunity in nutraceutical applications leveraging natural mineral content for functional foods.

| Key Insights | Details |

|---|---|

|

Dry Molasses Market Size (2026E) |

US$ 682.1 million |

|

Market Value Forecast (2033F) |

US$ 947.1 million |

|

Projected Growth CAGR(2026-2033) |

4.8% |

|

Historical Market Growth (2020-2025) |

4.3% |

DRO Analysis

Drivers - Rising demand in animal feed and livestock nutrition

Dry molasses serves as a highly palatable, energy-dense feed ingredient that enhances intake and provides essential minerals for livestock. With global meat consumption projected to rise by 14% by 2030 according to FAO estimates, animal feed formulations increasingly incorporate natural carbohydrate sources like dry molasses to improve growth rates and feed efficiency. Its high sugar content delivers quick energy while trace minerals support rumen health in cattle and swine. This makes it particularly valuable in dairy, beef, and poultry sectors where cost-effective nutrition is critical. Manufacturers benefit from its long shelf life and ease of handling compared to liquid alternatives, driving adoption across integrated farming operations worldwide.

Expanding use in organic farming and crop protection

Dry molasses is gaining traction as a natural biostimulant and soil amendment in organic agriculture. When applied to soil, it stimulates beneficial microbial activity that improves nutrient availability and suppresses soil pathogens. USDA organic standards recognize molasses products as approved inputs, supporting its use in certified farming systems. Research from agricultural universities demonstrates that dry molasses applications can increase crop yields by 10-15% through enhanced soil biology. This aligns with the global organic farmland expansion, which grew by 25% between 2019 and 2024. Farmers increasingly adopt it for sustainable pest management and as a carbon source for compost enhancement, creating steady demand from the agricultural sector.

Restraints - Raw Material Price Volatility and Supply Constraints

Dry molasses production is intrinsically tied to the sugar industry, as it is derived from byproducts of sugarcane and sugar beet processing. This dependency exposes manufacturers to significant price volatility driven by fluctuations in global sugar output. Weather irregularities such as droughts, floods, and changing monsoon patterns in key producing countries like Brazil and India directly impact raw material availability and pricing. When sugar production declines, molasses supply tightens, increasing procurement costs for dry molasses processors. Additionally, molasses is increasingly diverted toward ethanol blending programs and alcoholic beverage production, intensifying competition for limited supply. Seasonal harvesting cycles further create inconsistent availability, leading to supply chain disruptions. Smaller manufacturers face greater challenges due to limited sourcing capabilities, while larger companies must invest heavily in supplier diversification and storage infrastructure to maintain stable production and ensure consistent product quality.

Regulatory Complexity Across Food and Feed Applications

The dry molasses market faces significant challenges due to stringent and often fragmented regulatory frameworks governing its use in food, feed, and nutraceutical applications. Authorities such as the U.S. Food and Drug Administration and the European Food Safety Authority impose strict guidelines on product composition, hygiene standards, contaminant limits, and labeling requirements. Manufacturers must conduct detailed testing for microbial safety, heavy metals, and allergens, which increases operational costs and extends product approval timelines. For feed-grade molasses, compliance with varying regional feed additive regulations particularly in Asia Pacific creates additional complexity for exporters. Nutraceutical and functional food applications face even higher scrutiny regarding health claims, requiring scientific validation and regulatory approval. These factors collectively raise entry barriers for new players, strain smaller manufacturers with limited compliance resources, and slow down innovation and product commercialization across global markets.

Opportunities - Development of Granular and Specialty Forms for Diverse Applications

The evolution of granular and specialty dry molasses formats presents a strong growth avenue as industries prioritize efficiency, precision, and ease of handling. Unlike powdered variants, granular molasses offers superior flowability, minimal dust formation, and accurate dosing, making it highly suitable for automated feed systems, precision agriculture equipment, and large-scale food processing. With increasing mechanization in agriculture and livestock management, demand for uniform and easy-to-apply feed ingredients is rising steadily. Granular forms also reduce wastage during transport and application, improving cost efficiency for end users. In the food industry, they provide consistent texture and controlled solubility, enhancing product quality in bakery and processed foods. Manufacturers investing in advanced granulation and spray-drying technologies can differentiate their offerings, achieve premium pricing, and cater to industrial buyers seeking standardized, high-performance ingredients with improved storage stability.

Nutraceutical and Functional Food Formulation Expansion

Rising consumer focus on health and wellness is creating new opportunities for dry molasses in nutraceutical and functional food applications. Rich in naturally occurring minerals such as iron, calcium, and potassium, dry molasses is increasingly being positioned as a value-added sweetener in energy bars, protein powders, and fortified baked goods. Consumers are shifting away from refined sugars toward recognizable, plant-based ingredients that offer additional nutritional benefits. This trend supports the inclusion of molasses in clean-label formulations, particularly in products targeting sports nutrition and lifestyle health segments. Manufacturers can collaborate with nutraceutical companies to develop standardized, nutrient-rich molasses extracts with consistent quality and verified health benefits. Its generally recognized as safe status simplifies regulatory pathways, enabling faster product launches. Premium positioning in health-focused categories allows suppliers to command higher margins while expanding into differentiated, high-growth consumer segments.

Category-wise Analysis

Source Insights

Sugarcane dominates as the leading source with approximately 65% market share in 2025 due to its abundant global production and established processing infrastructure. Brazil, India, and Thailand collectively produce over 70% of world sugarcane, ensuring reliable supply for dry molasses manufacturing. Sugarcane molasses offers higher sugar content (45-55%) and richer mineral profiles compared to beet alternatives, making it preferred for animal feed palatants and food sweeteners. Its tropical climate resilience provides year-round availability versus seasonal beet harvests. Major refineries integrated with sugar mills streamline production economics, supporting competitive pricing for bulk B2B customers across feed and fertilizer applications.

Form Insights

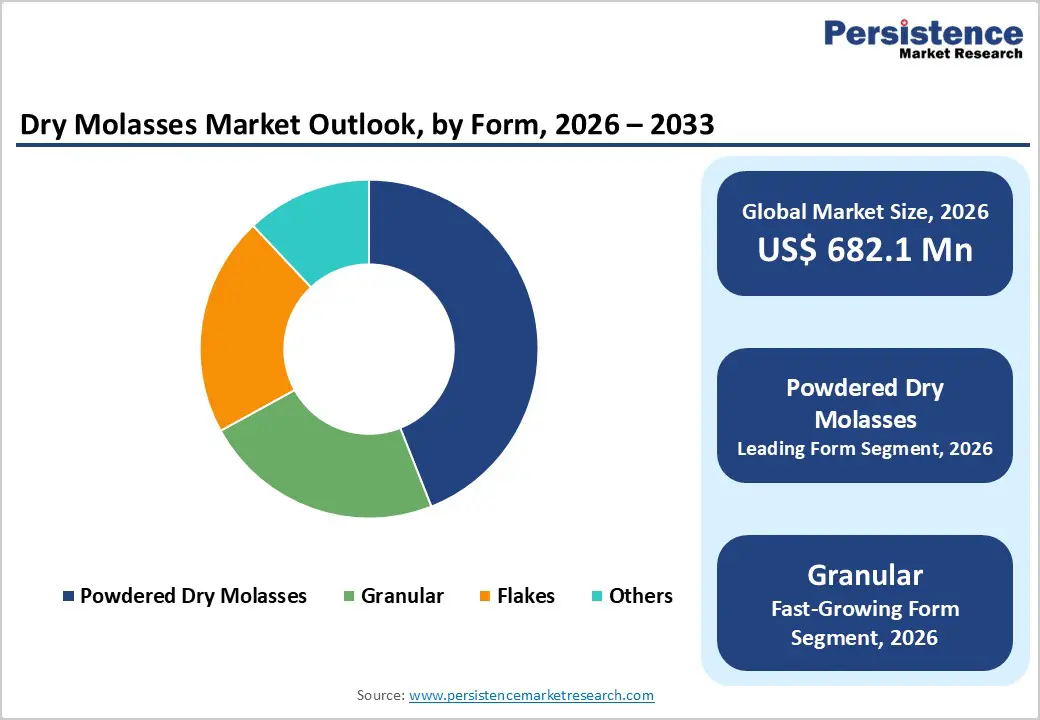

Powdered Dry Molasses leads with 44% market share in 2025 because it offers maximum dispersibility, quick dissolution, and formulation versatility across food, feed, and agricultural uses. Fine particle size (80-100 mesh) ensures uniform blending in dry mixes, animal rations, and soil amendments. Powder format dominates food industry applications like baking powders, seasoning blends, and instant beverages where rapid solubility matters. Its lightweight nature reduces shipping costs for international trade. However, Granular forms are gaining fastest as dust control improves worker safety and equipment performance, particularly in large-scale livestock operations and precision agriculture systems.

End-user Insights

Animal Feed commands the leading position because dry molasses serves as a cost-effective energy source and intake stimulant for livestock. It provides 50-60% carbohydrates while trace minerals support rumen fermentation and overall health. Global compound feed production reached 1.2 billion tons in 2024, with molasses incorporated at 2-5% inclusion rates across poultry, swine, and ruminant rations. Granular formats facilitate automated feed mills while maintaining palatability. Food industry applications trail but grow steadily for natural sweetening in bakery and sauces.

Distribution Channel Insights

Business to Business (B2B) dominates with over 85% volume share due to bulk packaging economics and customized specifications for industrial buyers. Large food processors, feed mills, and fertilizer blenders require tonnage quantities with consistent moisture content (<5%) and particle specifications. B2B channels benefit from long-term supply contracts that stabilize pricing amid commodity fluctuations. Technical support for formulation optimization creates switching barriers. Business to Consumer (B2C) remains niche but grows through e-commerce for organic gardeners and artisanal bakers seeking small-batch quantities.

Regional Insights

North America Dry Molasses Market Trends and Insights

The North America Dry Molasses Market continues to lead globally, driven by strong demand from the animal feed, biofuel, and food processing industries. The United States dominates regional consumption due to its advanced livestock sector, where dry molasses is widely used as a palatability enhancer and energy-rich additive. Increasing ethanol production and blending mandates are intensifying the use of molasses as a fermentation input, creating a competitive supply environment. At the same time, the shift toward sustainable and clean-label ingredients is boosting its adoption in functional foods and specialty sweeteners. Technological advancements in spray drying and granulation are improving product quality and expanding industrial applications. Additionally, well-established supply chains, strong presence of large agribusiness players, and ongoing innovation in feed efficiency solutions are supporting consistent market growth across the region.

Asia Pacific Dry Molasses Market Trends and Insights

The Asia Pacific Dry Molasses Market is emerging as a high-growth region, driven by expanding livestock production, rising demand for cost-effective feed ingredients, and increasing industrial utilization. Countries such as India, China, and Thailand are key contributors due to their large sugarcane production base, ensuring steady molasses availability. Rapid urbanization and growing consumption of meat and dairy products are fueling demand for nutritionally enhanced animal feed, where dry molasses plays a crucial role as an energy supplement and binding agent. Additionally, government support for ethanol blending programs is increasing competition for molasses, indirectly influencing dry molasses production dynamics. The food processing sector is also witnessing gradual adoption, particularly in bakery and traditional sweet products. However, evolving regulatory frameworks and inconsistent quality standards across countries present challenges. Despite this, improving processing infrastructure and rising investments in agri-value chains are expected to drive sustained market expansion.

Competitive Landscape

The Dry Molasses Market exhibits a moderately consolidated competitive landscape, characterized by the presence of large integrated processors alongside regional and niche manufacturers. Market participants compete primarily on pricing, product quality, and supply reliability, given the dependency on sugar industry byproducts. Companies are increasingly investing in advanced drying and granulation technologies to enhance product functionality and cater to diverse end-use industries such as animal feed, food processing, and fermentation. Strategic collaborations with feed manufacturers and distributors are common to strengthen market reach. Additionally, players focus on optimizing supply chains and securing consistent raw material sources to mitigate volatility and maintain competitive positioning in both domestic and export markets.

Key Developments:

- In March 2026, Blue Note Bourbon® launched its third annual Special Reserve Straight Bourbon Whiskey, further expanding its premium whiskey portfolio. The limited-edition release was crafted in Memphis and featured a unique blend of nine different cask finishes sourced from Kentucky and Tennessee, including cognac, madeira, sherry, port, vino de Naranja, vanilla cognac, apricot brandy, and winter bock.

- In April 2022, HEINZ launched an innovative product, HEINZ DIP & CRUNCH, aimed at enhancing the burger consumption experience through a unique two-in-one format. The product combined a flavorful dipping sauce with crispy potato crunchers in a single package, allowing consumers to add both taste and texture to their meals. It was introduced in two variants, including a classic and a spicy option, both formulated with ingredients such as tomato puree, molasses, and spices.

Companies Covered in Dry Molasses Market

- Cargill, Incorporated

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Associated British Foods plc

- Tereos Group

- Nordzucker AG

- Michigan Sugar Company

- Imperial Sugar Company

- Sugar Australia Pty Ltd

- Mitr Phol Sugar Corp Ltd.

- Louis Dreyfus Company, Bunge Limited

Frequently Asked Questions

The global Dry Molasses Market is expected to reach US$ 682.1 million in 2026, driven by animal feed, organic farming, and food industry applications.

Key drivers include livestock nutrition needs, organic soil amendments, and clean-label food sweetening preferences across global markets.

North America leads with 39% share in 2025, supported by U.S. livestock sector and advanced processing infrastructure.

Nutraceutical applications offer substantial opportunity through mineral-rich functional food formulations and health positioning.

Leading companies include Cargill, Incorporated, ADM, Tate & Lyle, Tereos, and Bunge Limited with integrated processing capabilities.