- Food Ingredients & Additives

- Organic Dry Pulses Market

Organic Dry Pulses Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Organic Dry Pulses Market by Product (Organic and Inorganic), by Plant Type (Chickpeas, Lentils, Dry Beans, and Cowpeas), by Application (Retail, Food Industry, and Animal Feed Industry) by Distribution Channel (Business to Business, Business to Consumer, Hypermarkets, Convenience Stores, and Online Retail), and Regional Analysis from 2026 to 2033

Organic Dry Pulses Market Share and Trend Analysis

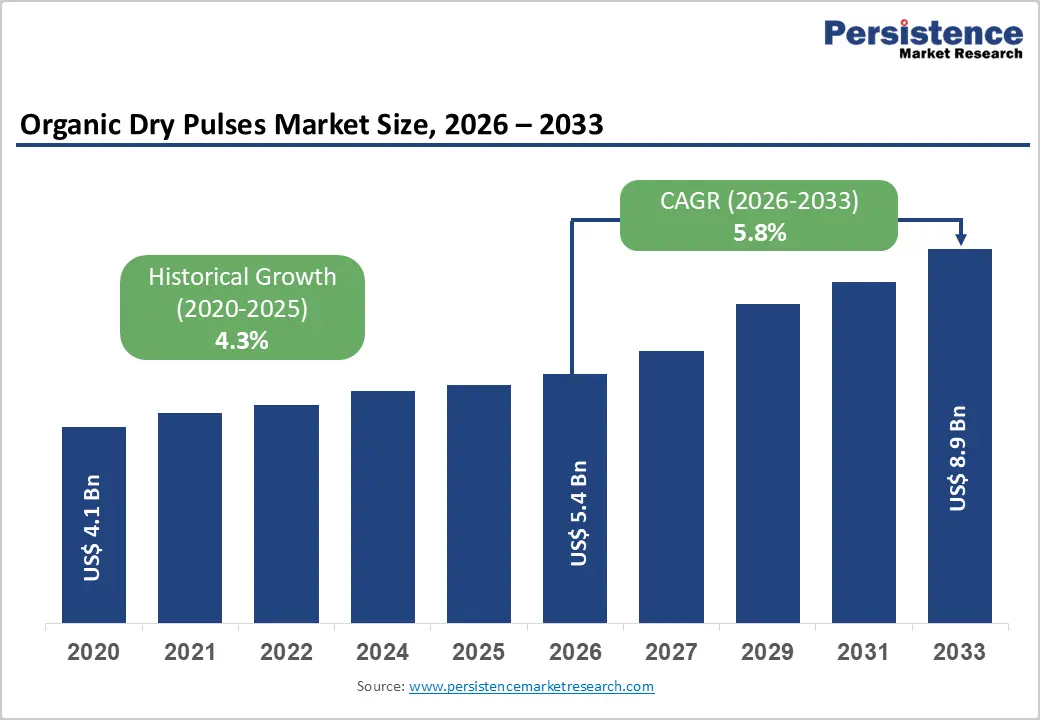

The global organic dry pulses market size is estimated to grow from US$ 5.4 billion in 2026 to US$ 8.9 billion by 2033. The market is projected to record a CAGR of 5.8% during the forecast period from 2026 to 2033. Global demand for organic dry pulses is expanding consistently, supported by increasing consumer preference for plant-based nutrition, rising awareness of clean-label food consumption, and growing interest in sustainably produced agricultural products. Consumers are incorporating organic pulses into daily diets as reliable sources of protein, fiber, and essential nutrients while reducing dependence on highly processed foods.

Wider product availability across supermarkets, specialty organic stores, online grocery platforms, and institutional supply chains is strengthening market penetration. Concerns regarding pesticide residues, food safety, and environmental sustainability are further encouraging adoption. Increasing use of organic pulses in ready meals, plant-protein foods, and health-focused recipes is accelerating commercial demand.

Key Industry Highlights:

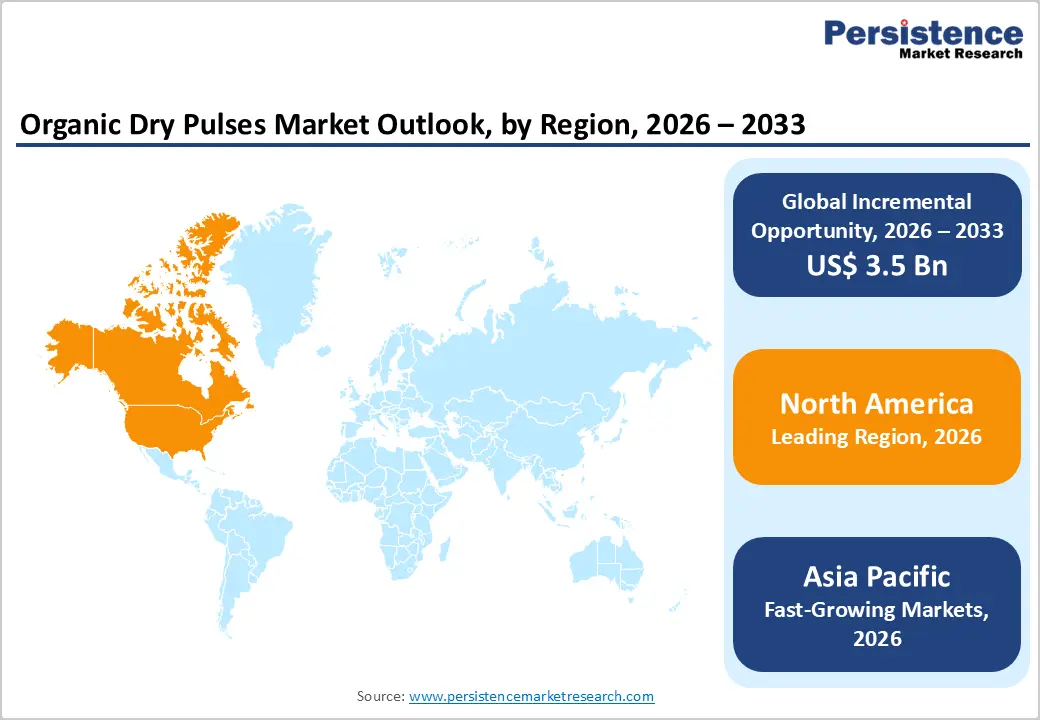

- Leading Region: North America holds the largest share at 46.7%, supported by strong organic food awareness, well-established certification systems, advanced retail infrastructure, high purchasing power, and widespread adoption of plant-based dietary habits.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rising urban populations, increasing disposable incomes, growing focus on healthy eating, traditional pulse consumption patterns, and rapid expansion of organized retail and e-commerce platforms.

- Leading Product Segment: Inorganic dominates the market owing to wider availability, lower pricing, established consumption habits, and strong supply volumes across developing economies.

- Fastest-Growing Product Segment: Organic is witnessing rapid expansion as consumers increasingly prioritize chemical-free cultivation, sustainability, and nutrient-rich natural foods.

- Leading Application Segment: Retail remains the largest segment, driven by strong household consumption, pantry stocking behavior, and increasing preference for packaged organic staples.

- Fastest-Growing Application Segment: Food industry applications are growing quickly as manufacturers incorporate organic pulses into plant-based foods, protein ingredients, snacks, and convenience meal solutions.

| Global Market Attributes | Key Insights |

|---|---|

| Organic Dry Pulses Market Size (2026E) | US$ 5.4 Bn |

| Market Value Forecast (2033F) | US$ 8.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8 % |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3 % |

Market Dynamics

Driver - Rising Demand for Plant-Based Nutrition and Clean-Label Food Consumption

Growing awareness around balanced nutrition and sustainable eating habits is significantly accelerating demand for organically cultivated pulses worldwide. Consumers are increasingly shifting toward natural protein sources as part of preventive health management, driven by concerns related to lifestyle disorders, obesity, and excessive consumption of processed foods. Organic dry pulses such as chickpeas, lentils, and beans provide a nutrient-dense combination of plant protein, dietary fiber, vitamins, and minerals, making them attractive alternatives to animal-based protein. The expansion of vegetarian, vegan, and flexitarian dietary patterns across developed and emerging economies further strengthens consumption frequency.

In addition, heightened concern regarding pesticide residues and soil degradation has encouraged buyers to prefer organically certified agricultural products. Governments and agricultural organizations are promoting sustainable farming practices, indirectly supporting organic pulse cultivation. Rising home cooking trends and demand for minimally processed ingredients have also reinforced pantry stocking behavior, particularly after shifts in consumer lifestyles toward healthier meal preparation. Food manufacturers are increasingly incorporating organic pulses into snacks, ready meals, and protein-enriched products, expanding commercial demand beyond household consumption. Improved packaging, branding transparency, and traceability systems further enhance consumer trust. As sustainability, nutrition, and ethical sourcing become central purchasing criteria, organic dry pulses are evolving from traditional staples into modern health-oriented dietary essentials, driving consistent global market expansion.

Restraints - Supply Chain Limitations and Price Sensitivity Affecting Market Penetration

The structural challenges continue to restrict wider adoption of organically produced pulses. Organic cultivation typically involves lower crop yields compared to conventional farming due to restrictions on synthetic fertilizers and pesticides, resulting in higher production costs and limited supply availability. Farmers transitioning to organic practices also face certification timelines and compliance requirements, which can delay market entry and increase operational complexity. These factors collectively contribute to premium pricing, making organic pulses less accessible to price-sensitive consumers, particularly in developing economies where conventional pulses remain the dominant choice.

Inconsistent supply volumes caused by climate variability, pest exposure, and fragmented farming systems further complicate procurement for large-scale processors and retailers. Additionally, lack of standardized awareness about organic certification among certain consumer groups leads to confusion regarding product value, reducing willingness to pay higher prices. Distribution challenges in rural and semi-urban regions restrict accessibility, while logistics costs associated with maintaining product quality add additional pressure on margins. Competition from cheaper non-organic alternatives also limits rapid conversion rates. Retailers must invest in consumer education and transparent labeling to justify premium positioning. Until supply chains achieve greater efficiency and production scalability improves, cost barriers and sourcing constraints will continue to moderate the pace of market expansion.

Opportunity - Expansion of Value-Added Pulse Products and Emerging Market Adoption

Changing dietary preferences and innovation across food processing industries are creating strong growth opportunities for organic pulse producers and manufacturers. Increasing utilization of pulses as functional ingredients in plant-based foods, gluten-free products, and protein-enriched snacks is expanding demand beyond traditional cooking applications. Organic pulse flours, ready-to-cook meal kits, and minimally processed convenience formats are gaining popularity among urban consumers seeking nutrition combined with convenience. Manufacturers are investing in advanced cleaning, grading, and milling technologies to enhance product consistency and improve usability in modern food formulations.

Emerging economies present substantial untapped potential as rising disposable income and expanding middle-class populations drive interest in premium and health-oriented foods. Rapid growth of organized retail and online grocery platforms enables wider reach for organic brands, allowing smaller producers to access global markets directly. Sustainability-driven purchasing behavior among younger consumers is encouraging adoption of responsibly sourced products, opening avenues for differentiated branding strategies. Export opportunities are also increasing as international buyers seek certified organic pulses from established agricultural regions. Collaborative initiatives between farmers, cooperatives, and food companies are improving traceability and supply stability. As innovation aligns with convenience, nutrition, and sustainability trends, organic dry pulses are positioned to benefit from diversified applications and expanding global consumer acceptance.

Category-wise Analysis

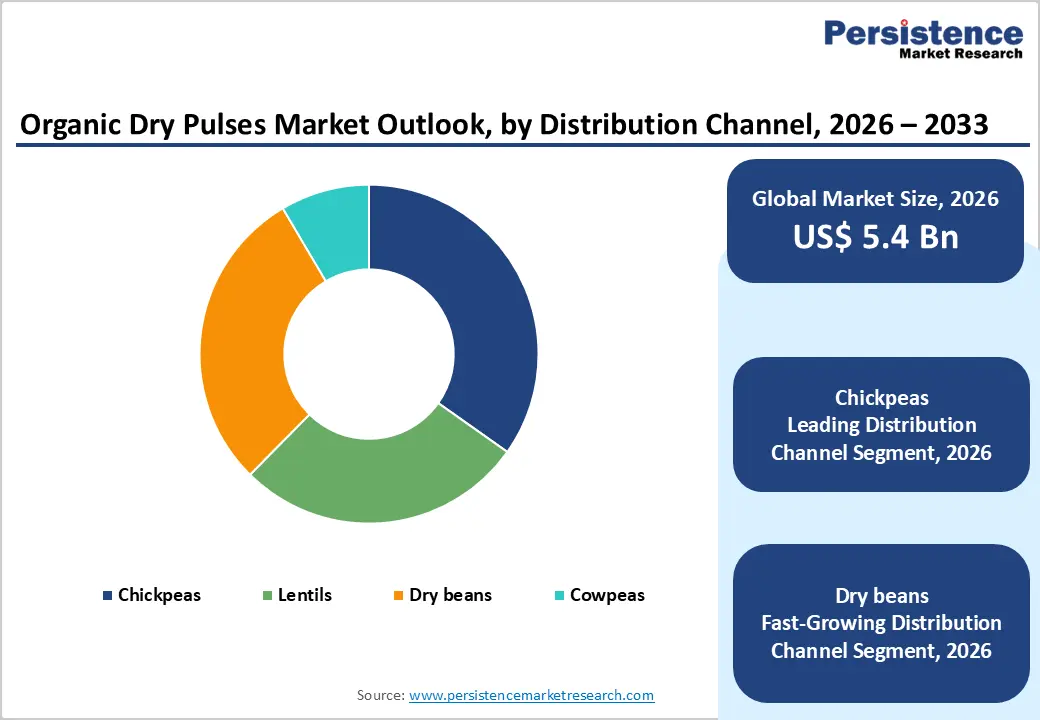

By Plant Type, Chickpeas Segment Dominates Owing to Versatile Culinary Usage and High Protein Preference

Chickpeas are anticipated to remain the leading plant type in the global organic dry pulses market in 2026, holding a 34.8% revenue share. Their dominance stems from widespread culinary acceptance across regions, particularly in Asia, the Middle East, and Europe, where chickpeas form a staple ingredient in traditional diets. Organic chickpeas benefit from growing consumer interest in plant-based nutrition, as they offer high protein, dietary fiber, and micronutrient content aligned with clean-eating trends. Food manufacturers increasingly utilize chickpeas in flour blends, snacks, ready-to-cook meals, and protein-rich formulations, further strengthening demand. Their adaptability across multiple cuisines, including hummus, curries, and roasted snack formats, enhances retail turnover. Additionally, organic certification improves export value, encouraging farmers and suppliers to expand cultivation. Improved processing technologies and packaged pulse offerings have enhanced shelf life and convenience, reinforcing chickpeas as the most commercially attractive and widely consumed organic pulse category worldwide.

By Application, Retail Leads Due to Household Consumption Patterns and Daily Dietary Integration

The retail segment is projected to account for a 56.7% revenue share of the global organic dry pulses market in 2026, primarily supported by strong household consumption. Organic dry pulses are increasingly purchased as pantry staples due to their affordability, long storage stability, and suitability for regular meal preparation. Consumers favor packaged organic pulses that offer quality assurance, traceability, and convenience compared to loose bulk products. Rising adoption of home cooking, health-focused diets, and plant-protein intake has strengthened retail demand across supermarkets and specialty organic stores. Smaller pack sizes and transparent labeling help consumers evaluate origin, certification, and nutritional benefits easily. Retail availability also enables frequent purchase cycles, especially in urban markets where awareness of organic food benefits continues to rise. As consumers prioritize minimally processed ingredients and balanced nutrition, retail channels remain central to market expansion and consistent volume sales globally.

By Distribution Channel, Hypermarkets Maintain Leadership through Product Visibility and One-Stop Purchasing Convenience

Hypermarkets are expected to capture a 32.5% revenue share in the global organic dry pulses market by 2026, driven by their ability to offer wide product assortments and competitive pricing. Large retail outlets provide dedicated organic food sections, allowing consumers to compare brands, pack sizes, and pulse varieties in a single shopping trip. High customer footfall supports impulse buying while promotional discounts and bundled offers encourage bulk purchases. For suppliers, hypermarkets ensure consistent demand volumes and efficient inventory turnover. These stores also enable better product display and consumer education through labeling and in-store promotions, improving awareness of organic certification standards. Urbanization and expansion of organized retail networks in developing economies further strengthen this channel. Although online grocery platforms are expanding rapidly, hypermarkets continue to serve as a trusted purchasing destination for staple foods, ensuring sustained dominance within distribution channels.

Regional Insights

North America Organic Dry Pulses Market Trends

North America is forecast to hold a 46.7% value share of the global organic dry pulses market in 2026, led mainly by the United States and supported by Canada’s expanding organic agriculture sector. The region benefits from a mature organic food ecosystem, high consumer awareness regarding clean-label nutrition, and strong demand for plant-based protein alternatives. Consumers increasingly incorporate organic pulses into everyday diets as substitutes for animal protein, aligning with sustainability and wellness objectives. Well-established certification frameworks and transparent labeling practices enhance buyer confidence and support premium pricing strategies.

Retail chains and natural food stores maintain extensive organic product assortments, while e-commerce platforms facilitate convenient access to specialty pulse varieties. Food manufacturers are integrating organic lentils, chickpeas, and beans into ready meals, snacks, and protein formulations, further boosting demand. Advanced logistics infrastructure and efficient supply chains enable consistent product availability across regions. Growing interest in preventive healthcare, weight management, and environmentally responsible food sourcing continues to reinforce North America’s leadership position in the global market landscape.

Europe Organic Dry Pulses Market Trends

Europe’s organic dry pulses market is expected to witness steady expansion in 2026, supported by heightened environmental awareness and established organic consumption habits across Germany, the U.K., France, Italy, and Nordic countries. European consumers prioritize sustainably produced foods, encouraging demand for organically cultivated lentils, beans, and chickpeas sourced through responsible farming practices. Strict regulatory frameworks governing organic certification and labeling strengthen trust and promote consistent product quality. Pulses are widely integrated into vegetarian and flexitarian diets, which are growing rapidly across the region due to climate and health considerations.

Retailers increasingly promote locally sourced and ethically produced pulse varieties, while private-label organic offerings improve affordability. Innovation in convenient cooking formats such as pre-cleaned and quick-cook pulses supports adoption among busy urban households. Foodservice operators and plant-based food manufacturers also contribute to rising demand. Sustainability initiatives, recyclable packaging adoption, and emphasis on transparent sourcing collectively support Europe’s stable long-term growth trajectory within the organic dry pulses sector.

Asia Pacific Organic Dry Pulses Market Trends

The Asia Pacific organic dry pulses market is projected to register a higher CAGR of around 7.9% between 2026 and 2033, fueled by rapid urbanization and increasing disposable income across China, India, Japan, and South Korea. Pulses already form a dietary cornerstone in many Asian cuisines, providing a strong foundation for organic adoption as consumers become more health conscious.

Rising awareness of chemical-free farming and food safety concerns is encouraging a gradual shift toward certified organic staples. Government initiatives promoting sustainable agriculture and organic cultivation are strengthening supply capabilities in several countries. Expansion of modern retail infrastructure and digital grocery platforms is improving product accessibility beyond metropolitan areas. Younger consumers, influenced by wellness trends and social media education, are actively seeking plant-based protein options aligned with healthier lifestyles. International brands are collaborating with regional suppliers to localize offerings and optimize pricing. These combined factors position Asia Pacific as the fastest-growing regional market, with substantial long-term consumption potential.

Competitive Landscape

The global organic dry pulses market is highly competitive, with strong participation from GT' SunOpta, brebio, Nature Bio-Foods Ltd, Vestkorn, Pulse USA, and Organic LRM. These players leverage extensive sourcing networks, organic certification capabilities, diversified retail and e-commerce distribution, and continuous innovation in cleaning, grading, processing efficiency, and packaging solutions to meet rising demand for natural plant-based protein sources.

Increasing health awareness, preference for clean-label foods, and sustainable agricultural practices are accelerating market expansion. Manufacturers are emphasizing traceability, minimally processed products, improved shelf stability, and expansion into emerging markets while strengthening supply chains and investing in product quality and organic cultivation partnerships.

Key Developments:

- In February 2026, the International Center for Agricultural Research in the Dry Areas (ICARDA) inaugurated advanced facilities at its Food Legume Research Platform (FLRP) in Amlaha, Madhya Pradesh, representing a significant step toward strengthening India’s climate-resilient, nutrition-focused, and farmer-oriented pulse production systems.

- In October 2025, the Prime Minister of India announced the launch of two major initiatives PM Dhan-Dhaanya Yojana and the Self-Reliance in Pulses Mission aimed at increasing pulse cultivation area from 27.5 million hectares to 31 million hectares by 2030-31.

Companies Covered in Organic Dry Pulses Market

- SunOpta

- brebio

- Nature Bio-Foods Ltd

- Vestkorn

- Pulse USA

- Organic LRM

- GPA Capital Food Pvt. Ltd.

- Pro Nature Organic Foods (P) Ltd

- Lemberona Organic Passion

- Organic Tattva

- Popular Pulse Products Pvt. Ltd

- Terra Greens Organic.

- Suminter India Organics

- MANTRA ORGANIC

- TRADIN ORGANIC AGRICULTURE B.V.

- Others

Frequently Asked Questions

The global organic dry pulses market is projected to be valued at US$ 5.4 Bn in 2026.

Rising adoption of plant-based diets, increasing health awareness, and growing preference for sustainable and chemical-free organic foods are primarily driving the global organic dry pulses market growth.

The global organic dry pulses market is poised to witness a CAGR of 5.8%between 2026 and 2033.

Expansion in emerging economies, growing use of pulses in processed and plant-protein foods, and widening online retail and distribution networks create major opportunities in the global organic dry pulses market.

GT' SunOpta, brebio, Nature Bio-Foods Ltd, Vestkorn, Pulse USA, and Organic LRM are some of the key players in the organic dry pulses market.