- Specialty & Fine Chemicals

- Dry Lubricant Market

Dry Lubricant Market Size, Share, and Growth Forecast, 2025 - 2032

Dry Lubricant Market By Product Type (PTFE (Polytetrafluoroethylene) Lubricants, Others), Application (Aerospace, Automotive, Other), End-use, and Regional Analysis for 2025 – 2032

Dry Lubricant Market Size and Trends Analysis

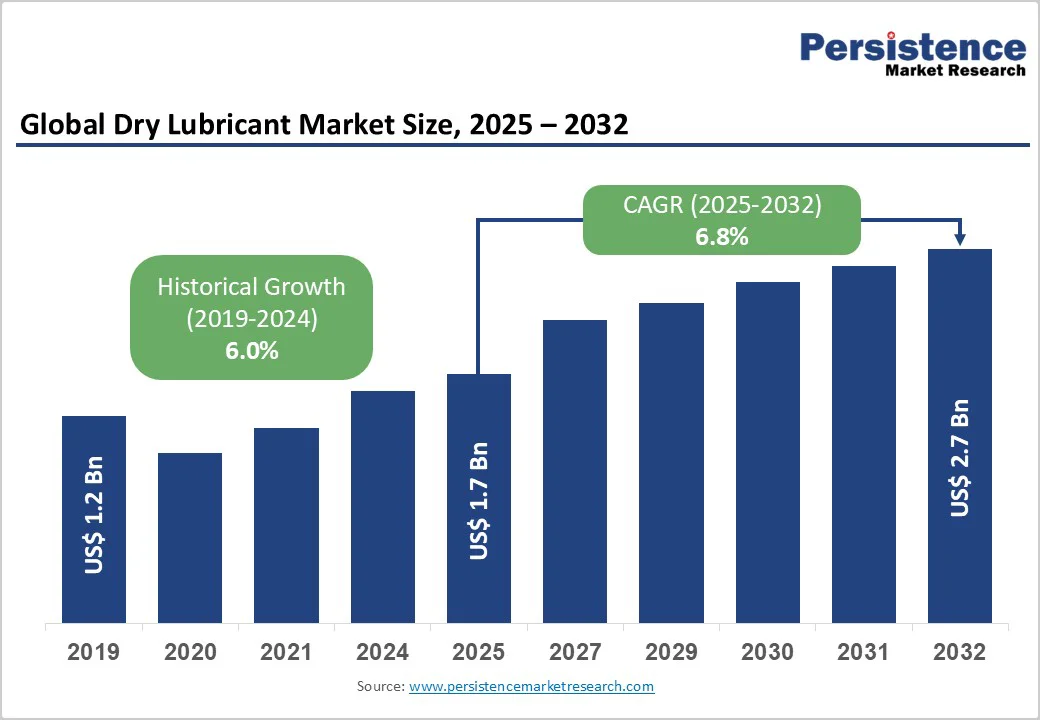

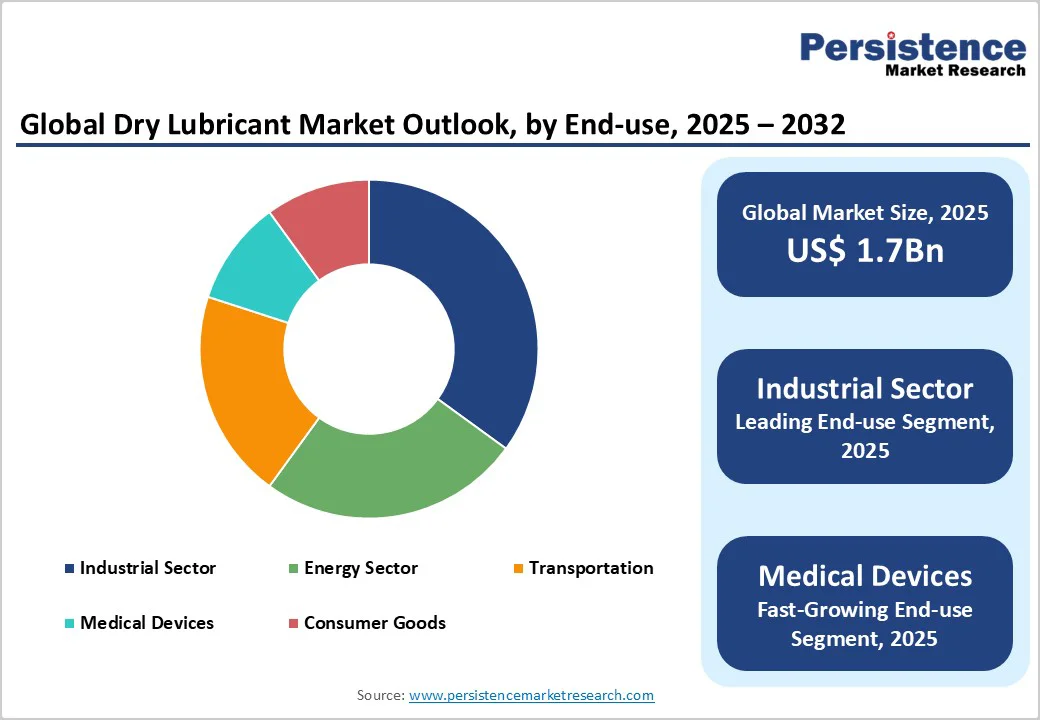

The global dry lubricant market size is likely to be valued US$ US$1.7 Billion in 2025, estimated to reach US$2.7 Billion by 2032 growing at a CAGR of 6.8% during the forecast period from 2025 to 2032.

The market is experiencing robust growth driven by increasing demand for low-maintenance, high-performance lubricants in harsh environments, rising adoption in automotive and aerospace for friction reduction, and advancements in solid lubricant technologies such as PTFE and graphite.

The market is further propelled by innovations in boron-based and synthetic dry films, catering to preferences for eco-friendly and high-temperature resistant materials. The growing acceptance of dry lubricant as alternatives to traditional oils, especially in food processing and electronics, is a key growth factor.

Key Industry Highlights:

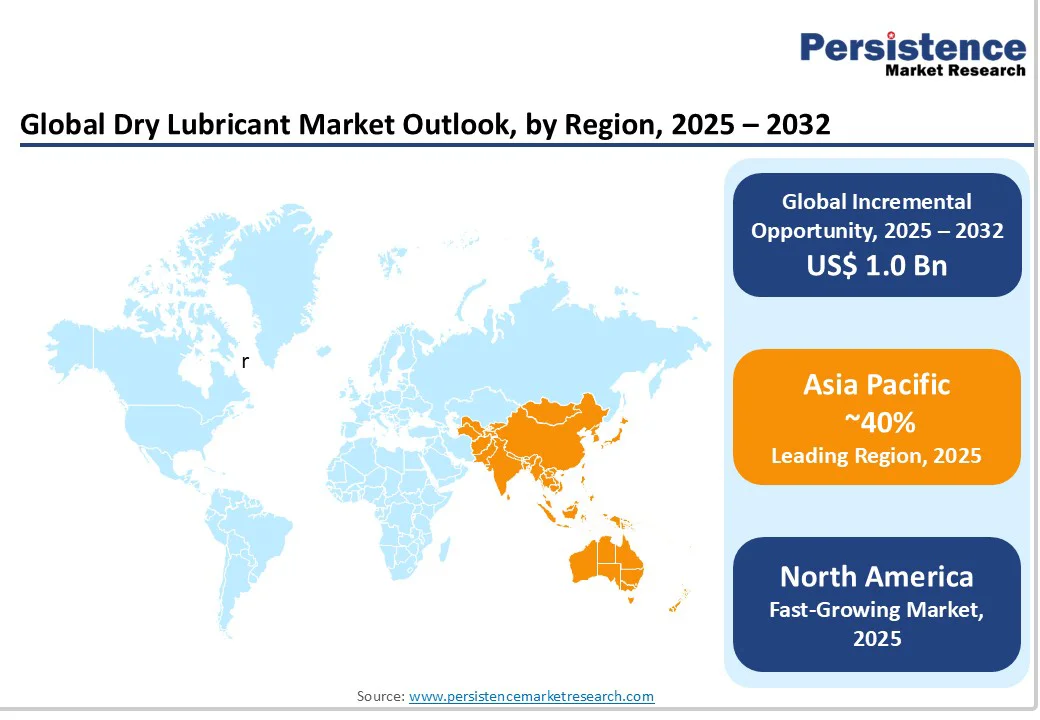

- Leading Region: Asia Pacific, commanding a 40% market share in 2025, demand for high-performance, low-maintenance, and eco-friendly lubricants is rising as industries focus on improving operational efficiency, reducing downtime, and meeting stringent environmental standards

- Fastest-growing Region: North America is the fastest-growing segment, due to strong investments in aerospace, automotive, and advanced manufacturing sectors.

- Dominant Product Type: PTFE (Polytetrafluoroethylene) Lubricants, holding approximately 40% of the market share, due to their low friction and versatility.

- Leading Application: Automotive, accounting for over 30% of market revenue, driven by engine and chassis protection needs.

- Leading End-use: Industrial Sector, contributing nearly 45% of market revenue, owing to heavy machinery applications.

- Key Market Driver: Industries seek lubricants that reduce wear, friction, and downtime, especially in harsh environments such as dust, high heat, or heavy loads.

- Growth Opportunity: Advancements in boron-based lubricants for medical devices, enabling sterile and biocompatible applications.

| Key Insights | Details |

|---|---|

|

Dry Lubricant Market Size (2025E) |

US$ 1.7 Bn |

|

Market Value Forecast (2032F) |

US$ 2.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.0% |

Market Dynamics

Driver - Rising demand for low-maintenance lubricants in harsh environments

The increasing demand for low-maintenance, contamination-free lubricants in harsh environments is a primary driver of the dry lubricant market. PTFE-based lubricants are widely recognized for their exceptional low-friction properties, offering a friction coefficient as low as 0.05.

This characteristic makes them highly effective in reducing energy losses and wear in mechanical systems, particularly in automotive applications. In automotive bearings, PTFE coatings significantly enhance operational efficiency by minimizing resistance between moving parts, ensuring smoother rotation, and reducing heat generation.

PTFE-based lubricants are chemically inert and resistant to corrosion, making them suitable for harsh environments where conventional oils and greases may degrade quickly. For instance, 3M’s dry films have demonstrated significant wear reduction in aerospace gears, supporting FAA standards and reducing downtime costs.

The growing food processing industry has accelerated adoption, with increased investments in clean technology. The emphasis on sustainable, oil-free lubrication, aligned with environmental regulations and guidelines, continues to drive market growth, particularly in high-output regions such as Asia Pacific and North America.

Restraint - Higher costs and limited high-temperature performance

The higher costs and performance limitations of dry lubricants pose significant restraints on market growth. Advanced dry film lubricant formulations, such as specialty coatings such as Molykote, face adoption challenges in cost-sensitive sectors due to higher production and material costs compared to conventional liquid lubricants.

Performance limitations, including temperature thresholds for certain graphite- or boron-based variants, can lead to premature wear or failure in high-heat or extreme operational environments.

Regulatory compliance, particularly for food-grade, medical, and aerospace applications, requires extensive testing and certification, extending development timelines and increasing operational expenses. Manufacturing complexities, such as achieving uniform thin-film coatings or precise nanoparticle dispersion, add further technical barriers.

Additionally, limited availability of certain raw materials and specialized equipment can restrict large-scale production. For example, approvals by Henkel Corporation have faced 25% cost overruns due to biocompatibility testing. Smaller manufacturers struggle against leaders like Dow Corning, limiting penetration in markets where liquid oils offer broader temperature ranges.

Opportunity - Expansion in medical devices and electronics with bio-based dry films

Advancements in bio-based dry films and their applications in medical devices and electronics present significant growth opportunities for the dry lubricant market. Boron-based lubricants offer sterile, non-toxic solutions, enhancing reliability and performance in medical devices, surgical tools, and precision instruments. Synthetic coatings are increasingly used in semiconductor manufacturing and electronics, improving miniaturization, reducing stiction, and ensuring smooth operation of delicate components.

Eco-friendly and bio-based formulations simplify regulatory compliance and support sustainable manufacturing practices. Advances in nanotechnology improve adhesion, durability, and thermal stability, expanding the range of applications. These lubricants are also finding use in aerospace, automotive, and energy sectors, where high-performance, residue-free coatings are critical for efficiency and component longevity. With ongoing innovation, collaborations between chemical manufacturers, OEMs, and research institutions are accelerating the development of customized, high-performance solutions.

Category-wise Analysis

Product Type Insights

PTFE (Polytetrafluoroethylene) Lubricants dominate the market, account 40% of the share in 2025, owing to their exceptional low friction, chemical resistance, and thermal stability. These properties make them highly suitable for automotive, aerospace, and industrial applications, where they reduce wear, enhance efficiency, and extend component life, supporting high-performance and reliability requirements in demanding operational environments.

Graphite-Based Lubricants are the fastest-growing segment, driven by their exceptional high-temperature stability, even up to 600°C, making them ideal for industrial furnaces and heavy machinery. Their excellent thermal conductivity, low friction, and resistance to oxidation support energy, power generation, and manufacturing applications, leading to rapid adoption across industries requiring reliable, high-performance lubrication under extreme conditions.

Application Insights

Automotive leads with 30% share, driven by their extensive use in chassis, engine, and transmission components. Dry lubricants reduce friction, wear, and noise, enhancing vehicle performance and longevity. Their ability to withstand high temperatures and harsh operating conditions makes them essential for improving efficiency, reliability, and maintenance in modern automotive applications.

Electronics is the fastest-growing, driven by increasing demand for precision coatings in semiconductors, sensors, and IoT devices. Dry lubricants provide ultra-thin, residue-free protection, reducing wear and friction in miniature components. Their reliability under high temperatures and compact designs makes them essential for enhancing performance and longevity in advanced electronic applications.

End-use Insights

Industrial Sector holds 45% share, utilizing these products to enhance the performance of heavy machinery and equipment operating in harsh, dusty, or high-friction environments. Dry lubricants reduce wear, corrosion, and maintenance needs, ensuring longer equipment life, improved efficiency, and reliability in industries such as mining, manufacturing, and construction.

Medical Devices is the fastest-growing, driven by the need for biocompatible coatings in implants, surgical tools, and precision instruments. Dry lubricants reduce friction, wear, and contamination without introducing harmful residues, ensuring patient safety, device longevity, and consistent performance, supporting the increasing demand for advanced, minimally invasive, and high-precision medical technologies.

Regional Insights

Asia Pacific Dry Lubricant Market Trends

Asia Pacific commands around 40% share and is the leading region. The region’s growth is driven by rapid industrialization, a booming manufacturing base, and the expansion of the electronics and automotive sectors in countries such as China, India, Japan, and South Korea. The increasing adoption of clean and environmentally friendly lubricants is fueled by stringent regulations and growing awareness of sustainable industrial practices.

China, as a manufacturing powerhouse, contributes significantly to market demand through its expansive automotive, aerospace, and electronics industries, where dry lubricants are used to reduce friction, wear, and maintenance requirements.

India’s industrial modernization and rising production in electronics and machinery create strong demand for high-performance, long-lasting lubrication solutions. The growth is further supported by the adoption of advanced manufacturing technologies that require precise, residue-free lubrication. With strategic investments from global and regional players, the Asia Pacific market continues to expand rapidly.

North America Dry Lubricant Market Trends

North America accounts for 20% in 2025, is the fastest-growing region, fueled by extensive research and development in the aerospace and automotive sectors across the U.S. and Canada. Aerospace companies are increasingly adopting high-performance dry lubricants to improve component durability, reduce maintenance, and enhance thermal and frictional efficiency in aircraft systems. In the automotive industry, innovations focused on lightweighting and fuel efficiency are driving the use of advanced dry films, particularly PTFE-based formulations, which offer excellent low-friction performance and long service life.

The trend toward environmentally friendly and non-toxic lubricants is also gaining momentum, aligning with broader sustainability goals. Interestingly, the U.K., while geographically part of Europe, exhibits similar market dynamics, driven by Ministry of Defence (MoD) projects and robust university-led R&D initiatives in bio-based and high-performance lubricants. Collaborative efforts between industrial players and research institutions are fostering the development of customized solutions tailored for extreme conditions.

Europe Dry Lubricant Market Trends

Europe holds about 25% market share, led by Germany and France emerging as key contributors. The region’s growth is strongly influenced by strict environmental regulations, particularly the EU REACH standards, which encourage the adoption of sustainable and non-toxic lubrication solutions across industrial and consumer applications. Compliance with these regulations has driven manufacturers to develop advanced dry films that reduce friction and wear while minimizing environmental impact.

Germany, with its robust automotive and engineering sectors, leads the market by integrating dry lubricants in vehicle components, industrial machinery, and precision equipment to improve efficiency and reduce emissions. France also contributes significantly, supported by a focus on sustainable manufacturing, aerospace, and energy-efficient industrial processes. The demand for high-performance dry lubricants is further amplified by the push toward lightweight and low-emission technologies in automotive and aerospace industries

Competitive Landscape

The global dry lubricant market is highly competitive, characterized by the presence of several established multinational companies alongside smaller regional players. Market leaders are increasingly focusing on research and development to create high-performance, durable, and environmentally friendly formulations that meet the evolving needs of automotive, aerospace, industrial, and manufacturing sectors. Sustainability has become a major priority, with companies investing in bio-based and non-toxic lubricants that reduce environmental impact while maintaining performance under extreme conditions.

Strategic partnerships and collaborations with original equipment manufacturers (OEMs) and industrial clients are being pursued to develop customized solutions for specific applications, enhancing product relevance and market penetration. Additionally, mergers and acquisitions are common strategies for portfolio diversification, enabling companies to expand product offerings, access new markets, and strengthen their technological capabilities. Investment in advanced manufacturing technologies, such as precision coating and additive production methods, further supports efficiency, consistency, and cost optimization.

Key Developments

- In July 2025, Castrol launched a new MHP lubricant range, offering protection with over 30,000 hours of testing to ensure excellent engine cleanliness and wear protection. Additionally, in March 2025, Saudi Aramco was reported to be exploring a potential bid for BP's Castrol unit, indicating strategic shifts within the company.

- In May 2025, Henkel Corporation has announced a significant expansion of its PTFE (polytetrafluoroethylene) production capabilities to meet the growing demand from the electric vehicle (EV) sector. This strategic move aims to enhance the performance and efficiency of EV components, particularly in areas requiring high thermal stability and low friction.

Companies Covered in Dry Lubricant Market

- 3M

- Henkel Corporation

- Dow Corning

- Castrol Limited

- Sun Coating Company

- OKS Speciality Lubricants

- SCCS Industries LLC (DYNACRON)

- Everlube

- CHP

- Metal Coatings Corp

- SKF AB

- Others

Frequently Asked Questions

The global dry lubricant market is projected to reach US$1.7 Billion in 2025, driven by demand for low-maintenance lubricants in industrial applications.

The market is driven by industrial machinery growth to US$ 500 Bn by 2030 and food processing expansion, necessitating clean solid lubricant solutions.

The market is poised to witness a CAGR of 6.8% from 2025 to 2032, supported by innovations in bio-based lubricants.

Advancements in boron-based lubricants for medical devices and electronics offer opportunities for sterile, high-performance applications.

3M, Henkel Corporation, Dow Corning, Castrol Limited, and SKF AB lead through innovations in PTFE and boron-based dry lubricants.