- Medical Devices

- Body Composition Monitor and Scale Market

Body Composition Monitor and Scale Market Size, Share, and Growth Forecast, 2026 - 2033

Body Composition Monitor and Scale Market Size, Share, and Growth Forecast, 2026 - 2033

Body Composition Monitor and Scale Market Share and Trends Analysis

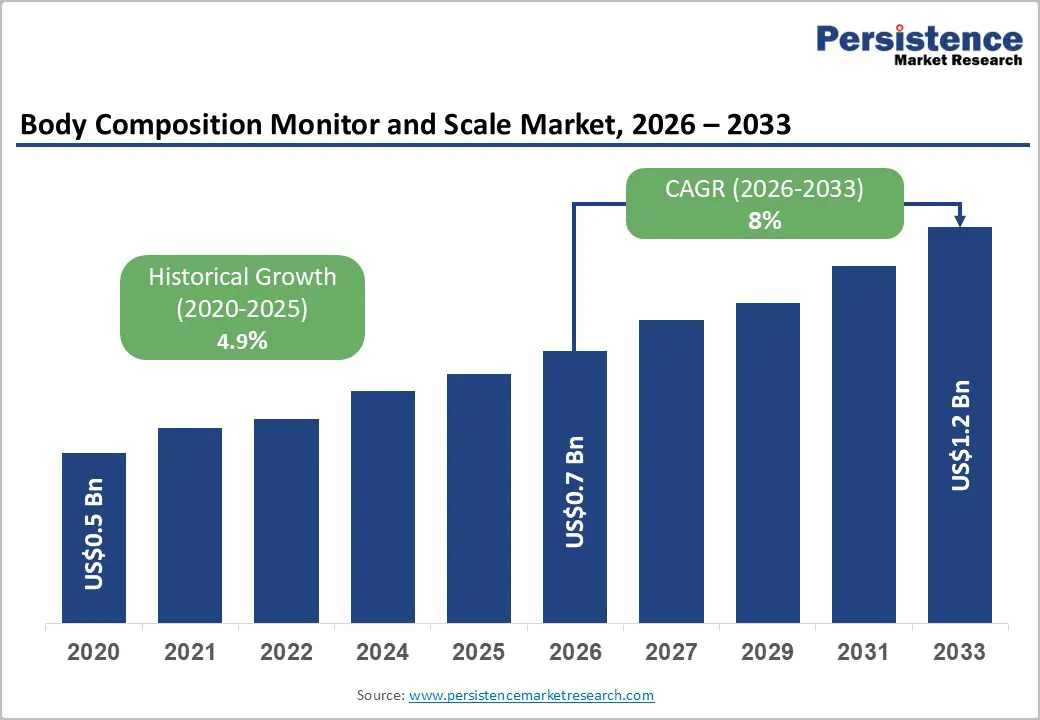

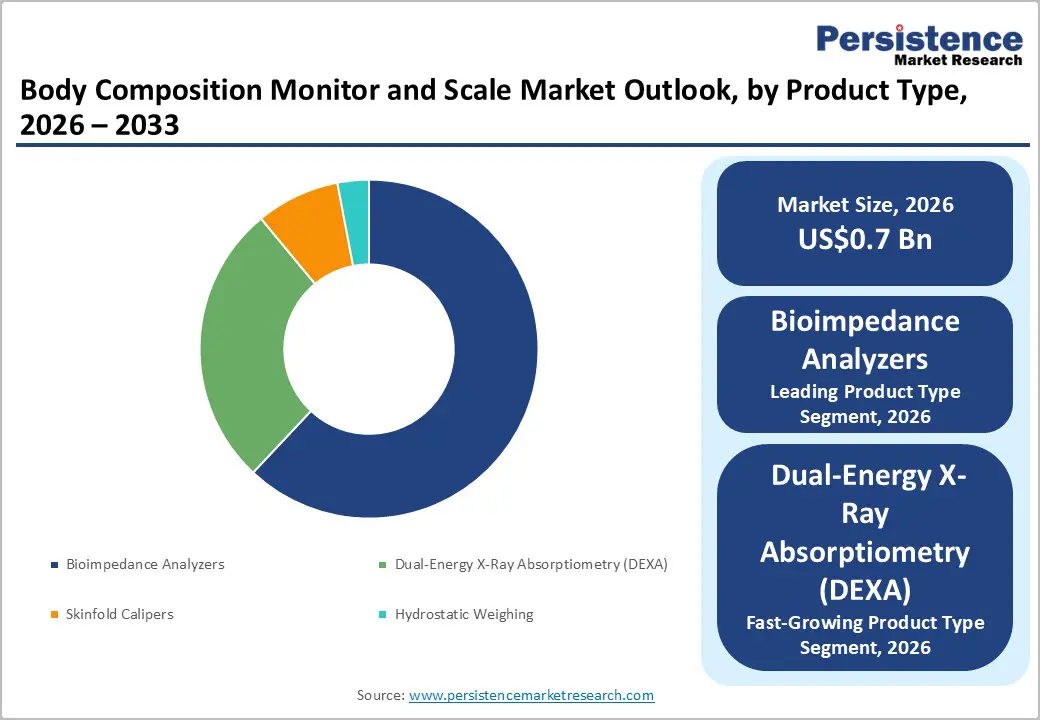

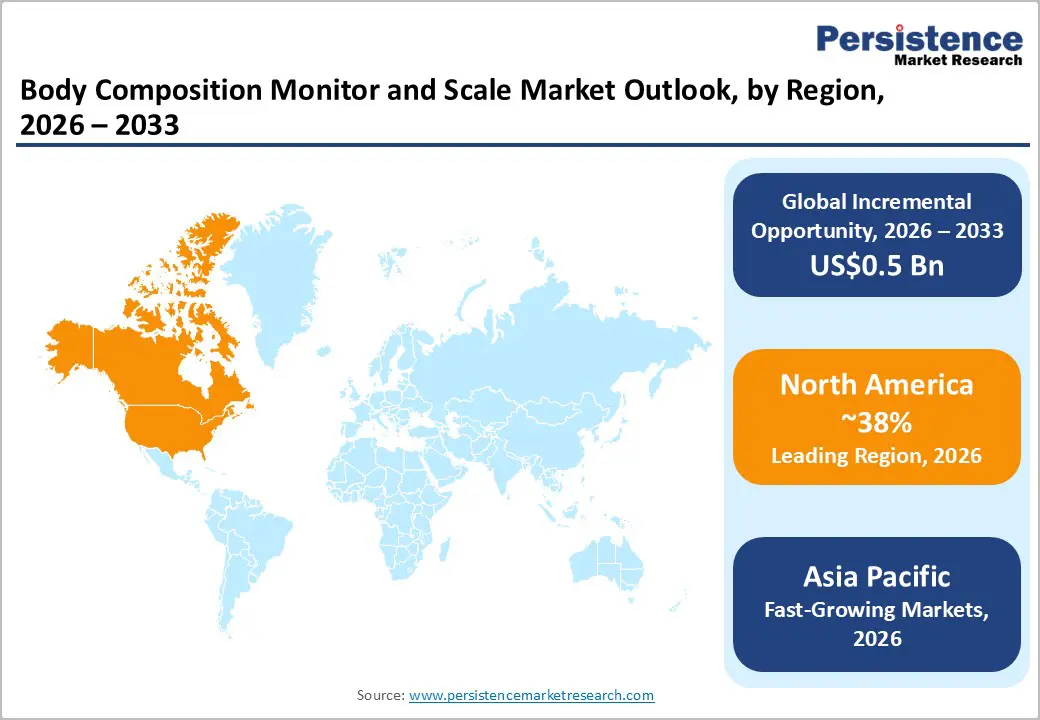

The global body composition monitor and scale market size is likely to be valued at US$ 0.7 billion in 2026, and is projected to reach US$ 1.2 billion by 2033, growing at a CAGR of 8% during the forecast period 2026−2033.

The market is driven by a convergence of rising global health consciousness, increasing prevalence of lifestyle diseases such as obesity and diabetes, and the growing adoption of personal wellness technology. The proliferation of connected health ecosystems integrating body composition monitors with smartphones, wearables, and telehealth platforms has materially expanded both the addressable market and consumer engagement depth. Technological advancements in bioelectrical impedance analysis (BIA), multi-frequency segmental measurement, and AI-driven health analytics are enabling more accurate and clinically relevant insights. Growing institutional demand from hospitals, fitness centers, sports science institutes, and corporate wellness programs is further supplementing strong consumer-grade growth across developed and emerging economies alike.

Key Industry Highlights

- Dominant Region: North America is set to command approximately 38% market share in 2026, owing to the high prevalence of obesity and related health disorders in the region.

- Fastest-growing Market: The Asia Pacific market is likely to be the fastest-growing through 2033, aided by rising healthcare expenditure and increasing awareness about fitness.

- Dominant Product Type: Bio-impedance analyzers are poised to dominate with nearly 62% revenue share in 2026, due to their convenience, affordability, and non-invasive design.

- Fastest-growing Product Type: Dual-energy X-ray absorptiometry (DEXA) is set to be the fastest-growing segment through 2033, since it provides detailed images and data on bone density, fat distribution, and lean body mass.

- Prime Drivers: Aging populations worldwide are increasing the demand for muscle mass and bone density monitoring, while corporate wellness programs are expanding business-to-business (B2B) sales through employee health incentives.

- Major Opportunities: Wearable tech integration can stoke the demand for seamless data syncing in personal health ecosystems, with regulatory shift toward preventive care opening reimbursed channels for clinical adoption.

| Key Insights | Details |

|---|---|

|

Body Composition Monitor and Scale Market Size (2026E) |

US$ 0.7 Bn |

|

Market Value Forecast (2033F) |

US$1.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Prevalence of Obesity and Non-Communicable Diseases (NCDs)

The World Health Organization (WHO) reports that over 1 billion people are living with obesity, while 2.5 billion adults are overweight, representing 43% prevalence. Rates have more than doubled in adults and quadrupled in adolescents since 1990. Non communicable diseases (NCDs) such as type 2 diabetes, cardiovascular disease, and metabolic syndrome are closely linked to body composition indicators such as visceral fat and lean muscle mass. Health systems are prioritizing accurate measurement to enable early risk detection, which is driving demand for body composition devices. Governments are embedding preventive monitoring into national health strategies, which is strengthening institutional adoption.

Public health frameworks are reinforcing this shift through structured programs and policy alignment. The U.S. Centers for Disease Control and Prevention (CDC), for example, is advancing early detection through initiatives such as the National Diabetes Prevention Program, while the European Union (EU) is implementing chronic disease strategies focused on proactive screening. These efforts are supporting integration of monitoring technologies into clinical workflows and standard care pathways. Healthcare providers are using these tools to track outcomes and reduce long term costs, while consumers are adopting home-based solutions for routine health management. This convergence of policy and technology is expanding market access and will have accelerated innovation in body composition analysis.

Expansion of Digital Health Ecosystems and Wearable Integration

The global digital health market is expanding and is accelerating the adoption of body composition monitors through connected ecosystems. Platforms such as Apple Health, Google Fit, and Samsung Health are integrating data from smart scales, wearables, and nutrition applications into unified dashboards. Consumers are prioritizing seamless synchronization and real time insights, which is increasing device usage and retention. Manufacturers are designing interoperable products to align with these platforms, which is shortening purchase cycles and strengthening ecosystem lock in.

Corporate wellness programs are extending this demand into enterprise settings through structured preventive health initiatives. Employers are deploying monitoring tools across office and remote environments to improve workforce health outcomes. Human resource (HR) teams are collaborating with device providers to enable scalable adoption, which is embedding body composition tracking into routine assessments. Organizations are benefiting from reduced absenteeism and improved productivity, while suppliers are introducing enterprise grade solutions with secure data management and cohort analytics. Policy support for workplace health technology is reinforcing this shift, which is widening B2B channels and sustaining market growth.

Accuracy Limitations and Consumer Trust Deficit

Consumer-grade BIA scales lead product volumes but face credibility issues due to inconsistent readings. Variables such as hydration status, recent activity, and posture are affecting output, which reduces user trust in home settings. Consumers are questioning daily fluctuations, while clinicians are avoiding endorsement of low-cost devices for decision-making. Manufacturers are issuing standardized usage protocols to improve consistency, yet variability across user conditions remains a constraint on adoption and upgrade cycles.

This limitation is widening the gap between consumer devices and clinical systems such as DEXA, which delivers higher diagnostic accuracy. Although cost restricts widespread access to DEXA, it defines performance benchmarks that BIA devices must approach. Companies are advancing multi-frequency sensors and adaptive algorithms to improve precision and reduce error margins. Ongoing validation studies and regulatory guidance on performance transparency are strengthening user confidence. Hybrid solutions are emerging to balance affordability with improved accuracy, which is supporting adoption across both personal and clinical applications.

High Cost of Clinically Accurate Devices and Limited Reimbursement

Professional-grade body composition systems such as DEXA and air displacement plethysmography (ADP) are carrying high capital costs, which is limiting adoption to large hospitals and specialized clinics. Smaller practices and fitness centers are prioritizing core equipment, while mid-range BIA devices with clinical accuracy still require significant investment. Providers are balancing cost against diagnostic value, which is slowing deployment across resource-constrained settings. Manufacturers are introducing financing and leasing options, yet upfront expenditure remains a primary barrier.

Reimbursement gaps are further restricting uptake, as insurance frameworks lack consistent coverage for body composition assessments. Healthcare administrators are hesitating to allocate budgets without clear payer support, which is sustaining reliance on basic measurement methods. Policymakers and insurers are evaluating these tools as preventive diagnostics, with an aim to improve funding pathways. Vendors are engaging with stakeholders to demonstrate long-term cost savings from early intervention, while localized production is reducing price points in emerging markets. Standardized coverage and flexible procurement models are expected to expand access and drive adoption across healthcare systems.

Integration with RPM and Telehealth

Remote care adoption is positioning body composition monitors as core tools in remote patient monitoring (RPM) programs for conditions such as obesity, diabetes, and heart failure. Providers are tracking longitudinal metrics to adjust treatment without in-person visits, while connected devices are transmitting data directly to care teams. This integration is improving clinical outcomes and reducing hospital utilization. Regulators are supporting deployment through updated digital health frameworks, which is accelerating adoption across care settings.

In the United States, the Centers for Medicare & Medicaid Services (CMS) is expanding reimbursement for RPM devices, including connected body composition systems. European markets are implementing similar incentives to promote digital health integration. Payers are recognizing preventive value, which is driving clinical uptake and compliance alignment. Suppliers are prioritizing secure platforms and interoperable workflows, enabling physicians to derive actionable insights while patients engage through app-based feedback. This shift is embedding body composition analysis into virtual care delivery models.

AI-Driven Personalized Health Insights

Next-generation personalized health insights are using artificial intelligence (AI) and machine learning (ML) to interpret individual health data and deliver tailored recommendations. Systems are analyzing trends in body fat, muscle mass, hydration, and metabolic indicators to generate actionable guidance beyond basic tracking. These platforms are learning from historical patterns and are refining outputs over time, which improves accuracy and relevance for each user. This approach is shifting monitoring from static measurement to dynamic, insight-led decision support.

In body composition monitoring, AI is identifying subtle physiological changes and linking them with lifestyle inputs such as sleep, activity, and nutrition. This integrated view is enabling early risk detection and more precise interventions before conditions escalate. Users are receiving contextual recommendations that reflect personal behavior rather than population averages. Providers are leveraging these insights to support preventive care models, which is strengthening engagement and long-term health outcomes.

Category-wise Analysis

Product Type Insights

Bioelectrical impedance analyzers are most likely to lead with about 62% of the body composition monitor and scale market revenue share in 2026, supported by low cost, ease of use, and non-invasive operation. These devices are passing a mild electrical current through body tissues to estimate fat mass, muscle composition, and related metrics. Users are favoring quick results and simple workflows across home and clinical settings, which is driving large scale adoption. This accessibility is positioning BIA as the primary technology for routine body composition monitoring.

Dual energy X-ray absorptiometry is slated to emerge as the fastest-growing product from 2026 to 2033 due to its proven superior diagnostic accuracy. These systems are providing detailed insights into bone density, fat distribution, and lean mass, which supports clinical decision making. High equipment costs and operational complexity are limiting usage to hospitals and research centers. Healthcare providers are relying on DEXA for precise assessments in areas such as osteoporosis and obesity management, which is strengthening its role in advanced care pathways.

End-User Insights

Hospitals are expected to hold roughly 45.4% of the body composition monitor and scale market share in 2026, driven by clinical reliance on body composition analysis for diagnosis and monitoring of conditions such as obesity, eating disorders, and metabolic disorders. These facilities are using detailed metrics on fat mass, muscle composition, and related indicators to design targeted treatment plans and track patient progress. Advanced systems such as DEXA are known to deliver high precision outputs, which is improving care quality and supporting effective disease management across clinical pathways.

Fitness centers are set to become the fastest-growing end-user during the 2026-2033 forecast period, boosted by rising focus on health and wellness. These facilities are deploying body composition tools to track member progress, set measurable goals, and customize training and nutrition plans. Trainers are using data on fat loss and muscle gain to refine programs, while users are staying engaged through visible results. This integration is enhancing service value, improving retention, and positioning body composition monitoring as a core offering in competitive fitness environments.

Regional Insights

North America Body Composition Monitor and Scale Market

North America is forecast to account for almost 38% of the body composition monitor and scale market value in 2026, led by the United States through advanced healthcare infrastructure and high wellness spending. Corporate wellness programs are expanding access to monitoring tools, while the U.S. Food and Drug Administration (FDA) is enabling faster device approvals through the 510(k) pathway with established safety standards. Strong research investment is supporting product innovation, which is aligning devices with diverse clinical and consumer needs.

Growth is accelerating through policy support and rising chronic disease burden. The CMS is actively expanding reimbursement for remote patient monitoring, which includes connected body composition devices. Increasing obesity prevalence is driving demand for continuous tracking, while digital health funding is advancing app integrated solutions. E-commerce channels are improving accessibility, and competition among established and emerging brands is intensifying innovation. This environment is embedding body composition monitoring into routine care and preventive health strategies.

Europe Body Composition Monitor and Scale Market Trends

Europe is the second-largest market for body composition monitors, supported by strong healthcare systems in Germany, the United Kingdom, France, and Spain. Germany is driving clinical adoption through its statutory health insurance system, the Gesetzliche Krankenversicherung (GKV), while the United Kingdom is integrating monitoring tools under the National Health Service (NHS) Long Term Plan. Providers are using these devices to track patient outcomes and refine treatment pathways. Manufacturers are focusing on clinically validated designs to meet institutional requirements and improve adoption across public health systems.

Regulatory alignment under the European Union (EU) Medical Device Regulation (MDR 2017/745) is strengthening product quality and market entry standards. This framework is filtering out low-quality devices and is favoring established suppliers of medical-grade solutions. National initiatives in France and Spain are addressing obesity and are expanding private healthcare infrastructure, which is increasing demand. Insurers are supporting compliant technologies that reduce long term costs, while providers are adopting advanced diagnostic systems for precision care. Ongoing regulatory streamlining is expected to support next generation connected devices and enable broader interoperability across healthcare networks.

Asia Pacific Body Composition Monitor and Scale Market Trends

Asia Pacific is poised to stand out as the fastest-growing market for body composition monitors and scales, driven by rising health awareness and economic expansion in China, India, and ASEAN members. China is scaling production under the Healthy China 2030 framework, which promotes preventive care and expands access to consumer devices. Cost-efficient manufacturing is lowering entry barriers, while digital platforms are enabling app-based tracking for routine health management. This combination is strengthening both domestic adoption and export competitiveness.

Regulatory standards are pushing companies such as Tanita and Omron to enhance BIA accuracy, which is improving global benchmarks. India is expanding demand through digital health initiatives and connected device adoption, while ASEAN markets such as Indonesia and Vietnam are witnessing early growth due to rising healthcare spending. Suppliers are offering tiered products to match varied income levels, and fitness ecosystems are integrating monitoring tools into training programs. Policy alignment and innovation in portable devices are expected to expand institutional use and consumer uptake, which is positioning the region as a key driver of global market dynamics.

Competitive Landscape

The global body composition monitor and scale market structure is moderately consolidated, with leading players such as Tanita Corporation, Omron Healthcare, InBody, Seca, and KERN & SOHN accounting for about 45% to 50% share. These firms are shaping market dynamics through strong product portfolios and global distribution networks. Competition is intensifying as companies introduce advanced devices aligned with evolving clinical and consumer requirements.

Market participants are focusing on research and development (R&D) to deliver more accurate, user-friendly, and connected solutions. Continuous product upgrades and technology integration are strengthening differentiation, while strategic partnerships and acquisitions are expanding market reach. This approach is enabling companies to address diverse end-user segments and reinforce long-term positioning in a rapidly evolving digital health landscape.

Key Industry Developments

- In February 2026, Taylor introduced connected smart scales featuring advanced wellness metrics via a retractable handle with eight contact points for precise upper- and lower-body composition analysis. Integrated with the Taylor Precision Hub App, the scales support up to eight users, track metrics such as body fat, muscle mass, hydration, and body mass index (BMI), and offer multi-language interfaces for detailed health insights.

- In November 2025, Wyze launched the Ultra BodyScan, its first smart scale with segmented body composition analysis using eight electrodes on the platform and a retractable handle for upper-body metrics across arms, legs, and torso. It tracks 13 metrics such as weight, body fat, muscle mass, BMI, bone density, and hydration, plus Wi-Fi/Bluetooth syncing for up to eight users.

- In October 2025, RunStar expanded its smart scale portfolio with three new 8-electrode models featuring upgraded foot pads, ITO coating for larger sensors, offline data storage, and enhanced displays. The lineup includes the 8E SmartScan Ultra Body Fat Scale, offering eight real-time metrics, voice prompts, and DEXA-validated accuracy, alongside two space-efficient variants for personalized wellness tracking.

Companies Covered in Body Composition Monitor and Scale Market

- Tanita Corporation

- Omron Healthcare, Inc.

- InBody Co., Ltd.

- Withings

- Seca GmbH & Co. KG

- KERN & SOHN GmbH

- Xiaomi Corporation

- Fitbit

- Beurer GmbH

- A&D Medical

- Renpho Inc.

- Garmin Ltd.

- Hologic, Inc.

- Lunar

- COSMED Srl

Frequently Asked Questions

The global body composition monitor and scale market is projected to reach US$ 0.7 billion in 2026.

Rising obesity rates and chronic diseases, and technological advances in bioimpedance and app integration are driving the market.

The market is poised to witness a CAGR of 8% from 2026 to 2033.

The developing economies of Asia Pacific offer high growth opportunities due to large-scale urbanization and robust local manufacturing capabilities, with telehealth synergies and AI analytics unlocking B2B expansion in corporate wellness.

Tanita Corporation, Omron Healthcare, Inc., InBody Co., Ltd, Seca GmbH & Co. KG, and KERN & SOHN GmbH are some of the key players in the market.