- Media & Entertainment

- Smart Wearable Devices Market

Smart Wearable Devices Market Size, Share, and Growth Forecast, 2026 - 2033

Smart Wearable Devices Market by Product Type (Smartwatches, Fitness Trackers, Smart Glasses, Smart Clothing, Wearable Medical Devices), Application (Health & Fitness, Entertainment & Media, Safety & Security, Fashion & Lifestyle, Industrial & Enterprise), Technology (Bluetooth, Wi-Fi, Near Field Communication (NFC), Global Positioning System (GPS), Radio Frequency Identification (RFID)), and Regional Analysis for 2026 - 2033

Smart Wearable Devices Market Share and Trends Analysis

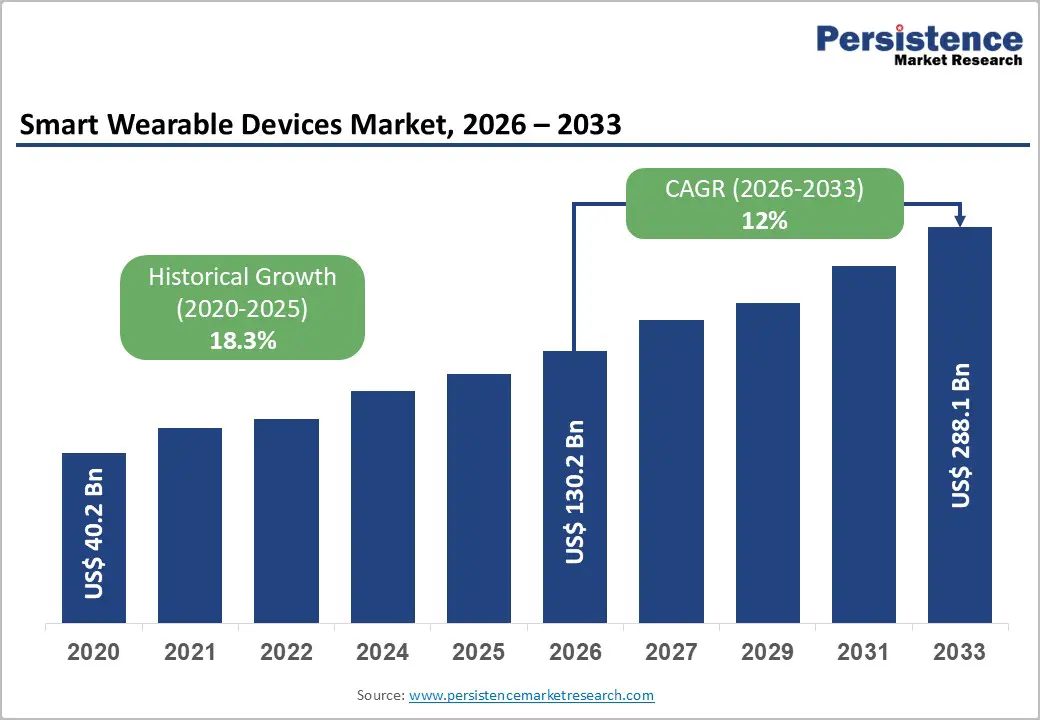

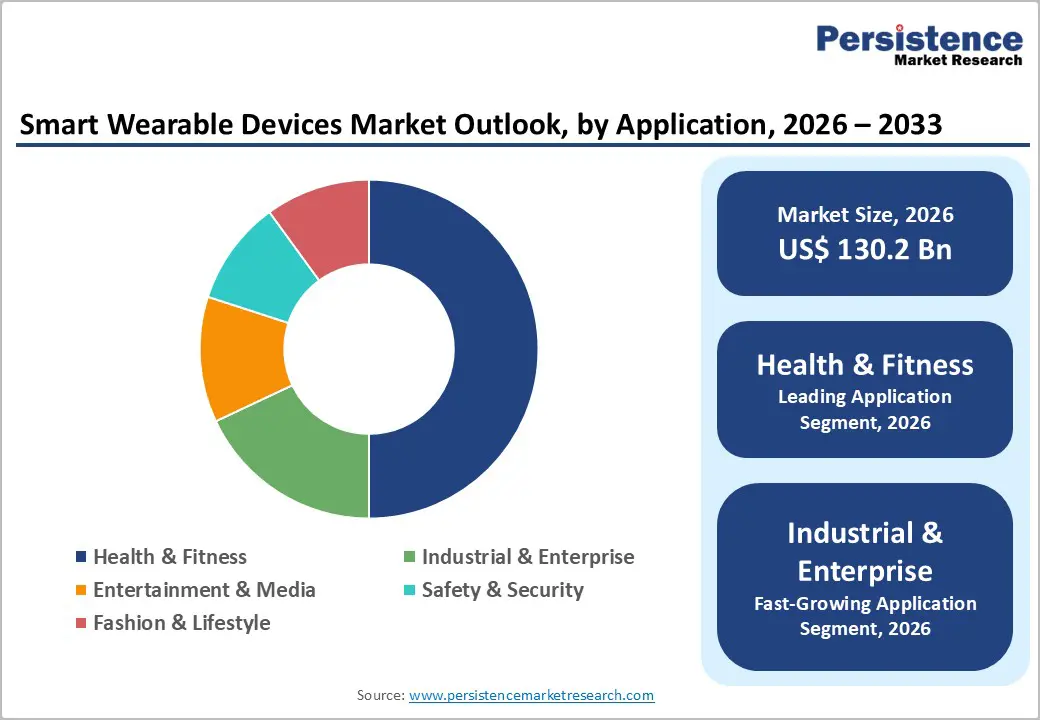

The global smart wearable devices market size is likely to be valued at US$ 130.2 billion in 2026, and is projected to reach US$ 288.1 billion by 2033, growing at a CAGR of 12% during the forecast period 2026−2033. Market expansion is driven by sustained double-digit growth reflecting structural integration of digital health monitoring, consumer electronics innovation, and connected-care infrastructure across developed and emerging economies. Rising prevalence of lifestyle-related chronic conditions, as reported by the World Health Organization (WHO), increases the demand for continuous biometric monitoring and supports the adoption of wearable-enabled preventive healthcare models. Aging demographics across North America, Europe, and East Asia further elevate long-term demand for remote health supervision and early risk detection tools.

Healthcare system digitization initiatives supported by regulatory authorities such as the U.S. Food and Drug Administration (FDA) and the European Commission (EC) accelerate approval pathways for software-integrated medical wearables, strengthening institutional confidence and commercial deployment. The convergence of AI, sensor miniaturization, and cloud-based analytics enhances device precision and user engagement, while the expansion of 5G telecommunications networks and rising smartphone penetration improve interoperability and real-time health data transmission across care ecosystems.

Key Industry Highlights

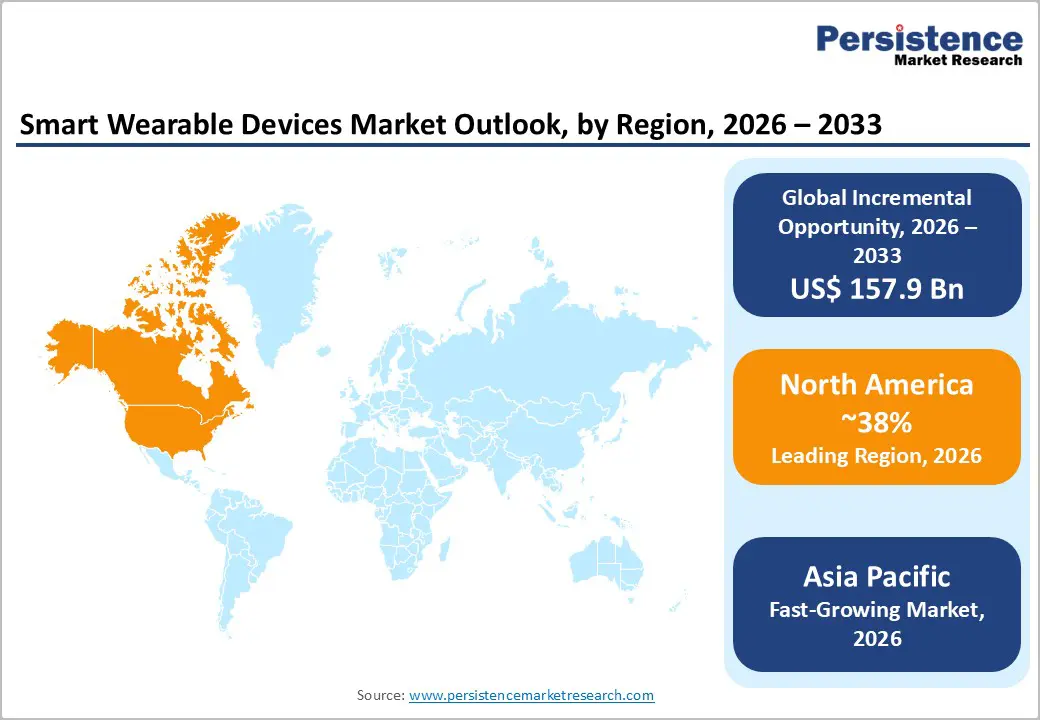

- Dominant Region: By 2026, North America is expected to command roughly 38% market share, driven by digital health maturity and wearable integration into care programs.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by scalable manufacturing and rising adoption.

- Leading Application: Health & fitness is set to lead in 2026, powered by preventive health awareness and wearable adoption.

- Fastest-growing Application: Industrial & enterprise is anticipated to be the fastest-growing segment from 2026 to 2033, driven by workplace safety, productivity analytics, and digital adoption.

- February 2026: Apple launched AI-driven wearables, including smart glasses, a pendant, and upgraded AirPods, to enhance personal computing and Siri functionality.

| Key Insights | Details |

|---|---|

|

Smart Wearable Devices Market Size (2026E) |

US$ 130.2 Bn |

|

Market Value Forecast (2033F) |

US$ 288.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12% |

|

Historical Market Growth (CAGR 2020 to 2025) |

18.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Preventive Healthcare and Remote Monitoring Ecosystems

Growth in preventive healthcare and remote monitoring stands as a primary driver due to sustained shifts in public health priorities and care delivery models. National health systems are formally moving from reactive treatment toward early detection and continuous risk management, embedding digital health into standard care pathways, as outlined in official public health policy frameworks such as those of the U.K.’s National Health Service (NHS) for 2025-2026 that emphasize earlier diagnosis and prevention of avoidable illness through digital approaches. The availability of real-time vital signs and biometric data enables healthcare professionals to detect deviations from baseline health status before acute events occur, supporting clinical decision-making without requiring frequent physical consultations. Continuous streams of physiological metrics enhance patient engagement with their own health profiles and improve adherence to treatment regimens, which, in turn, reduce avoidable hospital admissions and lower strain on primary care resources.

At a population level, formal adoption of remote monitoring is supported by government digital health strategies that integrate electronic health records, telehealth platforms, and preventive programs into mainstream services. Health systems pursuing digital transformation are expanding connectivity between providers and patients and allocating funding to digital infrastructures that complement preventive screening and chronic condition management services. Official U.K. policy documents for 2025 commit to moving from analogue to digital models and from illness response to prevention across care pathways, reinforcing the systemic imperative for technologies that provide continuous oversight of health status.

Technological Convergence and Semiconductor Innovation

Convergence of advanced technologies and innovation in semiconductors underpins the performance and viability of modern connected devices. Microelectronics and chip design directly determine power efficiency, sensor responsiveness and data-processing capability in compact form factors; improvements in transistor density and integrated circuitry enable multi-modal sensing, extended battery life and real-time analytics that were previously unachievable at scale. U.S. federal guidance from the CHIPS for America emphasizes that semiconductors are integral to consumer electronics, communication systems, advanced computing, medical devices and emerging AI infrastructure, illustrating their foundational role across technology stacks.

Innovation in semiconductor materials and fabrication processes reduces component size and cost while enhancing computational throughput, enabling tighter integration of digital health, connectivity, sensing and user-interface technologies in portable form factors. Breakthroughs in heterogeneous integration, packaging and low-power system-on-chip architectures support complex workloads within constrained thermal and energy budgets, allowing devices to perform continuous monitoring and adaptive feedback without sacrificing user experience or reliability. Government support for research and fabrication infrastructure expands domestic capacity for advanced logic and sensor chips, thereby improving supply resilience and accelerating the deployment of next-generation platforms.

Data Privacy, Cybersecurity, and Regulatory Compliance Complexity

Corporate adoption of connected devices encounters major friction from obligations around the protection of personal data, network security, and compliance with evolving statutory regimes across jurisdictions. Heightened expectations for safeguarding sensitive health and behavioral information require implementation of robust encryption, secure storage protocols, and explicit user consent frameworks, elevating engineering and operational costs and prolonging development cycles. In the U.K., an official government survey found that 43% of organizations reported experiencing a cybersecurity breach or attack in the previous year, underscoring the pervasive threat landscape that influences risk management strategies and investment prioritization in enterprise systems rather than ancillary endpoints such as consumer wearables.

Regulatory scrutiny in advanced markets demands demonstrable adherence to stringent standards such as multi-factor authentication, secure provisioning, and audit trails, driving up certification costs and elongating time-to-market for new iterations. Overlapping regimes such as the European Union (EU)’s General Data Protection Regulation (GDPR), the U.K.’s Data Act 2025, and sector-specific rules in healthcare require discrete compliance pathways, legal interpretations, and documentation practices. Cybersecurity risk assessments and reporting obligations at the board level introduce governance overhead, while penalties for noncompliance expose firms to financial exposure and reputational loss.

Device Accuracy Limitations and Clinical Validation Barriers

Inconsistencies in sensor output and limited clinical validation constrain confidence in health metrics and slow medical uptake. Wearable sensors are subject to physiological, motion, and environmental interference, leading to variable measurements across users and settings and undermining the reliability of vital signs such as heart rate, blood oxygen, and blood pressure compared with clinical reference methods. This variability stems from differences in skin-to-sensor contact, calibration drift and algorithmic interpretation, which can produce divergent readings for identical conditions and reduce the actionable value of the data in high-stakes care pathways.

Regulatory performance requirements demand rigorous evidence of safety and effectiveness that goes beyond proof of concept. Authorities such as the U.S. FDA require clinical performance testing that demonstrates devices function as intended under expected conditions of use, including real-world populations and varied physiologies, and not just controlled laboratory environments. Meeting these requirements entails extensive, often costly trials to generate statistically meaningful clinical validity data for diverse use cases and intended patient populations.

Integration with Digital Therapeutics and Value-Based Care Models

Health delivery models that link digital therapies with value-oriented payment frameworks create measurable clinical outcomes and financial incentives for providers to adopt continuous, personalized care pathways. Real-world care quality and cost-efficiency metrics are central to value-based care, in which reimbursement is tied to performance outcomes rather than service volume. Continuous biometric and behavioral data streams from wearable sensors feed directly into adaptive care plans, enabling early risk identification, dynamic therapeutic adjustments, and evidence-based interventions.

Wearable-sourced data enhances provider and payer decision support by quantifying patient engagement, therapeutic adherence, and longitudinal health metrics, enabling predictive risk stratification and targeted interventions. Integrating software-mediated therapeutic protocols with traditional care workflows strengthens population health management, supports predictive modeling, and reduces preventable acute care episodes. Government strategy documents emphasize interoperable health information exchange as foundational to value advancement, reinforcing investment in digital tools that link patient-generated data with clinical and administrative systems for comprehensive care oversight.

Implementation with AI and IoT

Accelerating the adoption of AI and Internet of Things (IoT) technologies presents a significant opportunity as these technologies enable devices to transition from basic activity trackers to intelligent systems capable of real-time health diagnostics and context-aware insights. Embedded AI algorithms transform raw sensor data into predictive analytics, personalized recommendations, and pattern recognition, enhancing decision support and user engagement. At the same time, IoT connectivity facilitates seamless communication between wearables, cloud platforms, healthcare systems, and other endpoint devices, ensuring continuous data exchange and remote monitoring. The convergence of these technologies underpins smarter, adaptive ecosystems that support preventive care, chronic condition management, and workforce health solutions, expanding use cases beyond traditional fitness tracking.

Stronger institutional backing reinforces confidence in these technology frameworks; the U.S. government’s investment in advanced research and development in AI signals prioritization of intelligent health technologies for future innovation. According to data collected by U.S. federal scientific agencies, IoT installations are expected to exceed 55 billion connected devices by 2025, generating unprecedented volumes of health and operational data for AI systems to process and analyze. Wide deployment of 5G networks, sensor miniaturization, and cloud analytics further enhance device accuracy, scalability, and interoperability.

Category-wise Analysis

Product Type Insights

Smartwatches are anticipated to secure around 45% of the smart wearable devices market revenue share in 2026, reflecting multi-functionality, ecosystem integration, and broad consumer acceptance. Integration with smartphone operating systems enables seamless notifications, payment functions, navigation, and health monitoring within a single interface. Clinical-grade heart rhythm monitoring features receive regulatory clearances from authorities, including the U.S. FDA, enhancing medical credibility. Retail penetration through electronics chains and online platforms strengthens accessibility. Corporate wellness adoption supports volume expansion. Continuous innovation in battery life, display technology, and third-party application ecosystems sustains replacement cycles.

Wearable medical devices are expected to be the fastest-growing segment during the 2026-2033 forecast period, driven by clinical acceptance, reimbursement models for remote patient monitoring, and the prevalence of chronic diseases. Continuous glucose monitoring patches and ambulatory cardiac monitors align with hospital-at-home strategies promoted by public health authorities. Provider preference for evidence-based data collection enhances institutional procurement. Technological advances improve sensor precision and user adherence. Integration with telehealth platforms increases accessibility in rural regions. Regulatory approvals validating medical-grade performance strengthen trust among clinicians and insurers.

Application Insights

Health & fitness extracts are poised to dominate, with a forecasted market share of over 50% in 2026, driven by increased awareness of preventive healthcare, cultural acceptance of self-tracking, and expanded retail distribution. Public health campaigns led by the World Health Organization emphasize physical activity monitoring, encouraging consumer adoption. Fitness ecosystems integrating mobile applications and wearable analytics foster sustained engagement. Digital commerce platforms expand global reach, enabling subscription-based coaching services. Consumer trust in biometric tracking strengthens recurring usage. Corporate wellness initiatives further enlarge demand across enterprise channels.

Industrial & enterprise is estimated to be the fastest-growing segment from 2026 to 2033, fueled by workplace safety regulations, productivity analytics, and digital transformation strategies. Smart helmets and biometric badges monitor worker fatigue and environmental exposure. Regulatory agencies mandate occupational health monitoring across high-risk sectors. Manufacturers deploy wearables to optimize workflow efficiency and reduce accident-related liabilities. Integration with enterprise resource planning systems enhances data-driven decision-making. Rising investment in Industry 4.0 infrastructure supports scalable deployment.

Regional Insights

North America Smart Wearable Devices Market Trends

By 2026, North America is expected to lead with an estimated 38% share of the smart wearable devices market, supported by a mature digital health ecosystem, strong consumer purchasing power, and strong alignment between technology developers and healthcare systems. Market concentration of global technology leaders accelerates the commercialization of advanced sensor platforms, AI-enabled analytics, and semiconductor innovation. Deep capital availability through venture funding and public markets sustains rapid product iteration cycles and large-scale marketing deployment. Widespread integration of wearable data into employer-sponsored wellness programs and value-based care frameworks strengthens recurring demand beyond discretionary consumer purchases.

Dominance is further reinforced by regulatory clarity and structured approval pathways that encourage development of software-integrated medical-grade wearables. Institutional confidence in digital therapeutics and remote patient monitoring solutions expands clinical utilization, particularly in chronic disease management and post-acute supervision. Strong retail distribution networks, direct-to-consumer channels, and subscription-based digital health services enhance monetization and customer retention. Insurance reimbursement pilots for remote monitoring programs stimulate adoption among healthcare providers seeking to optimize costs and improve patient engagement metrics.

Europe Smart Wearable Devices Market Trends

Europe maintains a significant market share driven by coordinated digital health strategies under frameworks implemented by the EC. Germany, France, and Nordic countries invest in telemedicine infrastructure, advanced regulatory compliance, and interoperability standards that accelerate adoption of intelligent wearable technologies. High disposable incomes support premium device adoption, while widespread broadband and smartphone penetration enable seamless device-to-device and cloud-based analytics connectivity. Leading technology firms focus on miniaturized sensors, integrated artificial intelligence, and enhanced battery efficiency, producing devices that combine lifestyle tracking with clinically relevant biometric insights.

Structured institutional adoption reinforces market stability and growth potential. Insurance and healthcare organizations increasingly incorporate wearable data for chronic condition management, remote patient monitoring, and patient engagement programs, generating recurring demand beyond individual consumers. Corporate wellness programs leverage biometric insights to optimize productivity and reduce operational healthcare costs. Mature digital infrastructure facilitates real-time analytics, predictive modeling, and integration with telemedicine and electronic health records, improving operational efficiency and service quality.

Asia Pacific Smart Wearable Devices Market Trends

Asia Pacific is forecasted to be the fastest-growing market for smart wearable devices between 2026 and 2033, stimulated by scalable manufacturing ecosystems, cost-competitive innovation, and rapidly increasing adoption across diverse consumer segments. High-volume production capabilities enable delivery of advanced devices at lower price points, expanding reach among middle-income populations. Targeted research and development investments support localized product customization, addressing specific preferences such as extended battery life, multifunctional connectivity, and integrated health monitoring. Expanding digital infrastructure, including widespread 4G and emerging 5G networks, enhances real-time data processing, cloud analytics, and seamless device interoperability.

Enterprise and institutional uptake further accelerates growth, with deployments in logistics, industrial safety, and remote workforce monitoring delivering measurable operational efficiencies. Biometric data integration in telehealth and preventive care programs provides scalable solutions that optimize resource allocation and improve health outcomes. Policy support for smart city initiatives and digital public health projects fosters pilot implementations, signaling strong market potential to technology developers. Localized app ecosystems and payment platforms strengthen value propositions, increasing user engagement and retention.

Competitive Landscape

The global smart wearable devices market structure demonstrates moderate concentration, with Apple, Samsung, Garmin, Fitbit, and Huawei dominating the market in terms of revenue. Market dynamics emphasize ecosystem integration, where devices operate seamlessly with smartphones, cloud services, and health management platforms, delivering enhanced user experiences. Advanced sensor accuracy differentiates product offerings, enabling precise tracking of biometrics such as heart rate, blood oxygen, sleep patterns, and activity metrics. Brand recognition and loyalty significantly influence consumer choice, as established firms leverage global marketing, device interoperability, and after-sales service networks to maintain competitive advantage.

Barriers to entry remain high due to regulatory compliance, semiconductor sourcing challenges, and platform interoperability requirements. Firms must navigate medical device standards, data privacy regulations, and cross-border certification protocols to ensure safe and compliant product deployment. Securing reliable semiconductor supply chains is critical for performance and production scalability, while compatibility with multiple operating systems and third-party applications is essential to attract and retain users within established ecosystems.

Key Industry Developments

- In February 2026, Sarvam AI announced plans to launch its smart wearable, a made-in-India smart eyewear product, in May alongside a strategic partnership with HMD to bring artificial intelligence technology to feature phones and extend AI access across device categories.

- In February 2026, the Singapore-MIT Alliance for Research and Technology (SMART) launched a Wearable Imaging for Transforming Elderly Care research initiative to develop the first wearable ultrasound imaging system for real-time chronic condition monitoring and earlier clinical intervention.

- In December 2025, Wearable Devices Ltd. announced new gesture control enhancements for its smart glasses platform, introducing customized presets and Mudra Link application compatibility to streamline onboarding and deliver more intuitive cross-brand touchless interaction.

Companies Covered in Smart Wearable Devices Market

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Garmin Ltd.

- Fitbit, Inc.

- Huawei Device Co., Ltd.

- Xiaomi.

- Sony Semiconductor Solutions Corporation

- Polar Electro

- Withings

- Dexcom, Inc.

Frequently Asked Questions

The global smart wearable devices market is projected to reach US$ 130.2 billion in 2026.

Rising demand for preventive healthcare, remote monitoring, and integration of advanced sensor and AI technologies is driving the market.

The market is poised to witness a CAGR of 12% from 2026 to 2033.

Integration with digital therapeutics and expansion into emerging markets present key growth opportunities for the market.

Some of the key market players include Apple Inc., Samsung Electronics Co., Ltd., Garmin Ltd., Fitbit, Inc., and Huawei Device Co., Ltd.