- Biotechnology

- Antibody Discovery Market

Antibody Discovery Market Size, Share, and Growth Forecast, 2025 - 2032

Antibody Discovery Market by Methods (Phage Display, Hybridoma, Others), Antibody Type (Humanized Antibody, Human Antibody, Chimeric Antibody, Murine Antibody), End-use (Pharmaceutical and Biotechnology Industry, Research Laboratory, Academic Laboratory), and Regional Analysis for 2025 - 2032

Antibody Discovery Market Size and Trends Analysis

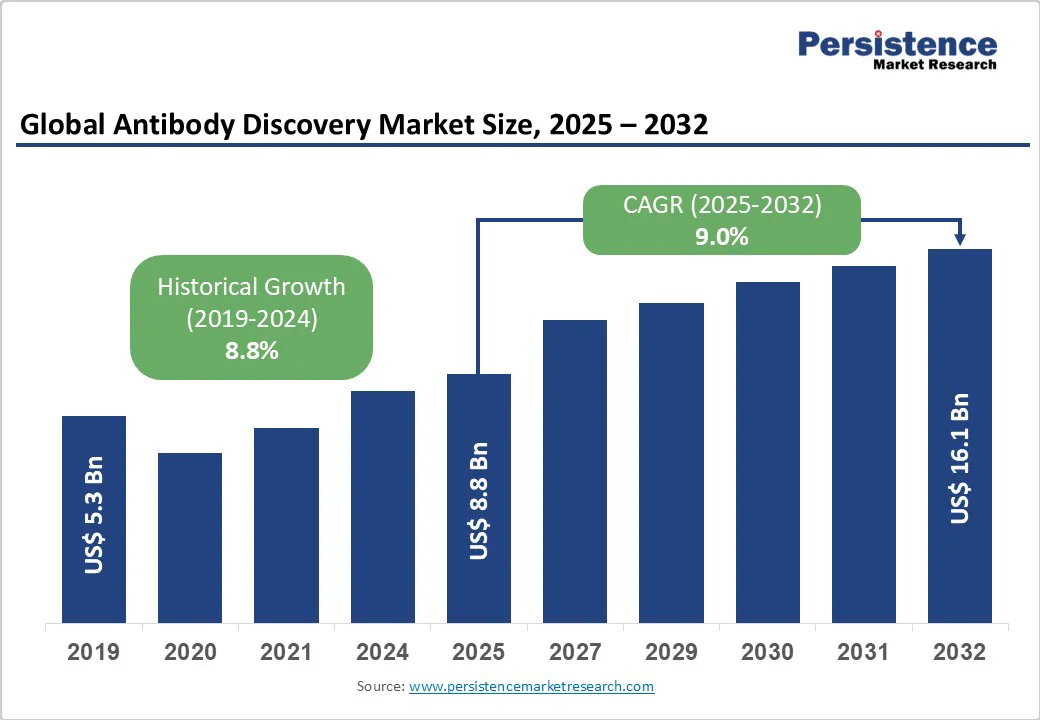

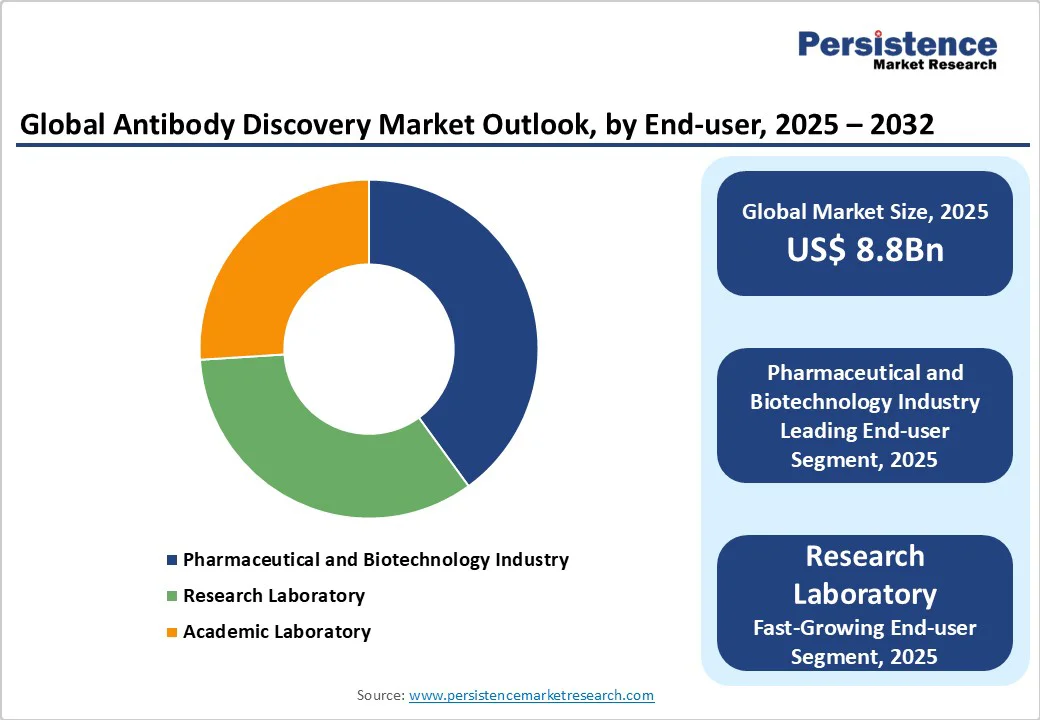

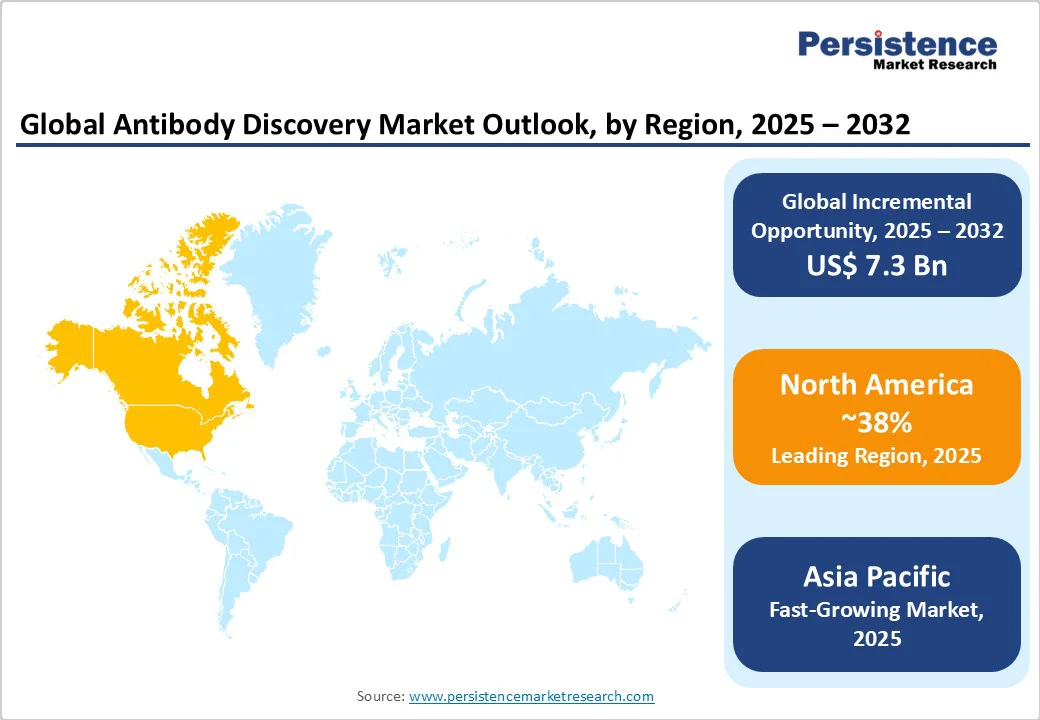

The global antibody discovery market size is likely to be valued at US$8.8 Bn in 2025. It is expected to reach US$16.1 Bn by 2032, growing at a CAGR of 9.0% during the forecast period from 2025 to 2032, driven by the escalating demand for biologics in treating complex diseases, advancements in high-throughput screening technologies, and the rise of personalized medicine approaches across the pharmaceutical and biotechnology sectors. The demand for innovative antibody solutions in oncology, autoimmune disorders, and infectious diseases has significantly boosted market expansion.

Key Industry Highlights

- Leading Region: North America, holding a 38% market share in 2025, driven by the presence of major biotech hubs in the U.S., high adoption of advanced discovery platforms, and strong demand for therapeutic antibodies in clinical trials.

- Fastest-growing Region: Asia Pacific is emerging as the fastest-growing market, fueled by rapid biomedical research developments, increasing government investments in life sciences infrastructure, and growing demand for antibody-based therapies in countries such as China and India.

- Dominant Method: Phage Display, commanding nearly 46% market share, due to its versatility in generating diverse antibody libraries, rapid screening capabilities, and widespread adoption in drug discovery pipelines.

- Leading Antibody Type: Humanized Antibody, accounting for over 48% of market revenue, driven by the need for reduced immunogenicity and improved safety profiles in therapeutic applications.

| Key Insights | Details |

|---|---|

|

Antibody Discovery Market Size (2025E) |

US$8.8 Bn |

|

Market Value Forecast (2032F) |

US$16.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

9.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.8% |

Market Dynamics

Driver - Advancements in Biotechnology and High-Throughput Technologies

The antibody discovery market is driven by the growing demand for targeted therapies in treating complex diseases, such as cancer, autoimmune disorders, and infectious diseases. Antibodies offer high specificity and low toxicity, making them essential for precision medicine. For instance, monoclonal antibodies such as pembrolizumab and trastuzumab have transformed oncology by providing more effective and safer treatment options compared to traditional chemotherapy. Advancements in methods such as phage display and hybridoma are further accelerating the discovery of novel antibodies with improved binding affinity and stability.

The rise of humanized and fully human antibodies is addressing immunogenicity concerns, enhancing clinical success rates. The increasing adoption of antibody-based drugs by the pharmaceutical and biotechnology industry is driving substantial investment in R&D. For example, several leading biotech firms are leveraging AI-integrated antibody discovery platforms to shorten development timelines. Additionally, academic and research laboratories are contributing by identifying new therapeutic targets, which both government and private funding support. Collectively, these factors are driving innovation and expanding the global pipeline of antibody therapeutics.

Restraint - High development and regulatory costs

The antibody discovery market faces high development and regulatory costs associated with bringing antibody-based therapies to market. Developing monoclonal antibodies requires advanced infrastructure, specialized technologies, and highly skilled expertise, all of which significantly increase R&D expenses. For instance, the cost of developing a single monoclonal antibody drug can exceed billions of dollars when factoring in preclinical research, clinical trials, and manufacturing scale-up.

The regulatory framework governing biologics is stringent, requiring extensive testing to ensure both safety and efficacy. This results in longer approval timelines compared to small-molecule drugs. Smaller biotechnology firms, which often drive innovation, may face financial barriers in sustaining long-term research and navigating complex approval pathways. For instance, regulatory agencies such as the FDA and EMA demand comprehensive clinical trial data and strict quality control, creating challenges for new entrants. These high costs and hurdles can delay product launches, limit participation from smaller players, and increase dependence on large pharmaceutical companies for funding and commercialization partnerships, thereby slowing market expansion.

Opportunity - Advancements in modular and AI-integrated bus technologies

The antibody discovery market is driven by advancements in modular and AI-integrated technologies, which are revolutionizing the way antibodies are designed, screened, and optimized. Modular platforms enable researchers to tailor antibody fragments and domains, resulting in highly flexible frameworks that can be rapidly adapted for diverse therapeutic targets. This reduces development complexity and accelerates timelines.

AI-driven tools are being increasingly integrated into antibody discovery workflows, enabling the predictive modeling of antibody–antigen interactions, the virtual screening of vast libraries, and the optimization of binding affinity and stability. For instance, companies are leveraging machine learning algorithms to identify lead candidates more quickly, thereby reducing their dependency on costly trial-and-error laboratory processes. These technologies not only lower R&D costs but also improve success rates in clinical translation. Furthermore, pharmaceutical and biotechnology firms are collaborating with AI-focused startups to enhance drug pipelines, ensuring quicker responses to emerging health challenges such as cancer and infectious diseases. The integration of modular and AI-based approaches thus offers a transformative opportunity to expand therapeutic applications, increase efficiency, and strengthen competitiveness in the antibody discovery market.

Category-wise Analysis

Methods Insights

Phage display is expected to dominate, accounting for approximately 46% of the market share in 2025. Its dominance stems from its cost-effectiveness, rapid library generation cycles, and ease of integration with high-throughput screening for applications such as therapeutic antibody development and diagnostics. Phage display platforms, such as those offered by Danaher Corporation and Eurofins Scientific, enable real-time affinity maturation, diverse epitope mapping, and seamless scalability across missions, making them a preferred choice for industries such as pharmaceutical R&D and biotechnology. Their modular designs also reduce upfront costs, driving adoption among startups and SMEs.

The hybridoma segment is the fastest-growing, driven by industries with high-specificity requirements, such as monoclonal antibody production for immunotherapy. Hybridoma technology provides greater reliability and purity in antibody isolation, making it an attractive option for large enterprises with complex therapeutic needs. The growing focus on personalized vaccines and bispecific antibodies, such as those in Roche’s initiatives, is accelerating the adoption of hybridoma systems in regions such as North America and Europe, with significant growth potential in high-stakes applications.

Antibody Type Insights

Humanized antibody leads the antibody discovery market, holding a 48% share in 2025. The segment’s dominance is driven by the need for enhanced safety and reduced immune responses in clinical applications, particularly in fully humanized constructs for the treatment of chronic diseases. These antibodies streamline integration with delivery systems, minimize adverse events, and improve patient outcomes, making them critical for providers such as Genentech and AstraZeneca.

The chimeric antibody segment is the fastest-growing, driven by the rapid evolution of hybrid constructs that balance efficacy and manufacturability. The rise in combination therapies and the increasing demand for cost-effective engineering have spurred the adoption of chimeric platforms in this sector. The Asia Pacific region, with its booming biologics manufacturing, is driving rapid adoption in this segment.

End-Use Insights

The pharmaceutical and biotechnology industry holds the largest market share, accounting for approximately 40% of revenue in 2025. This end-use allows vendors such as Charles River Laboratories and Genscript to maintain close relationships with customers, offer tailored discovery services, and provide dedicated support. It is particularly dominant in applications with complex requirements, such as oncology and autoimmune therapies, where customized antibody solutions are critical.

The research laboratory end-use is the fastest-growing, driven by the increasing adoption of advanced discovery technologies and the rise of collaborative consortia for novel target identification. These platforms offer seamless access to modular tools, enabling faster development and integration with other lab services. The growing popularity of academic-industry partnerships is accelerating the adoption of discovery solutions through this end-use, particularly in North America and the Asia Pacific.

Regional Insights

North America Antibody Discovery Market Trends

North America is projected to hold a 38% market share in 2025, driven by the strong presence of established biotech and pharmaceutical hubs in the U.S. The region benefits from high adoption of advanced discovery platforms such as phage display, hybridoma, and AI-integrated antibody screening, which accelerate R&D pipelines. Additionally, robust funding from both government agencies, such as the NIH and private investors supports continuous innovation in antibody-based therapeutics.

The U.S. also leads in clinical trial activity, with a significant share of ongoing trials focused on monoclonal antibodies for oncology, autoimmune disorders, and infectious diseases. Moreover, the growing demand for targeted and personalized medicines is driving investments in the development of humanized and fully human antibodies. Canada further strengthens the regional landscape through its expanding biotechnology clusters and academic research collaborations. Collectively, these factors make North America a key hub for antibody discovery and commercialization, ensuring sustained leadership in the global market.

Europe Antibody Discovery Market Trends

Europe is emerging as a key player in the antibody discovery market, driven by strong institutional frameworks and collaborative research programs. Regulatory bodies, including the European Medicines Agency (EMA), along with national agencies such as the UK’s MHRA, France’s ANSM, and Germany’s BfArM, are actively supporting the development of biologics, particularly in oncology, autoimmune disorders, infectious diseases, and regenerative medicine.

These regulatory initiatives are complemented by substantial public and private funding for research and development (R&D), enabling the adoption of advanced and modular antibody discovery platforms. European biotech clusters are increasingly focusing on multi-target therapeutics and humanized antibodies, leveraging high-throughput screening, phage display, and AI-integrated platforms to drive innovation. Collaborative programs between academic institutions and pharmaceutical companies are further enhancing pipeline development and accelerating the transition from preclinical to clinical studies. This ecosystem fosters innovation, reduces time-to-market for novel biologics, and strengthens Europe’s position as a leading hub for antibody discovery and therapeutic development.

Asia Pacific Antibody Discovery Market Trends

Asia Pacific is positioned as the fastest-growing market for antibody discovery, supported by rapid advancements in biomedical research and rising government investments in life sciences infrastructure. Countries such as China, India, and Japan are leading the region’s expansion, with China accelerating its biologics pipeline through initiatives like the National Natural Science Foundation and the 14th Five-Year Plan for Bioeconomy. Meanwhile, India’s Department of Biotechnology continues to launch cost-effective discovery programs with global collaborations. Japan, through the Japan Agency for Medical Research and Development (AMED), is focusing on precision antibody therapies and next-generation platforms.

The increasing need for targeted antibodies to support oncology screening, infectious disease surveillance, vaccine development, and chronic disease management is driving demand for compact, efficient, and modular discovery tools. Similarly, the surge in biopharma outsourcing to expand R&D capacities across underserved therapeutic areas is boosting commercial adoption. Private players and emerging biotech startups are also contributing by leveraging phage display and hybridoma technologies to deliver affordable solutions. With supportive government policies, advancements in AI-enabled discovery platforms, and expanding applications in personalized medicine, the Asia Pacific is expected to dominate future biologics innovation, creating substantial opportunities for platform vendors.

Competitive Landscape

The global antibody discovery market is characterized by intense competition, regional strengths, and a mix of global and niche players. In developed regions such as North America and Europe, large firms such as Danaher Corporation, Eurofins Scientific, and Charles River Laboratories dominate through scale, advanced R&D capabilities, and established partnerships with pharma giants. In the Asia Pacific, rapid biomedical developments and increasing demand for scalable platforms are attracting significant investments from both international players, such as Genscript Technology Corporation and Sartorius AG, and regional vendors. Companies are focusing on technological innovation, modular methods, and strategic alliances to gain a competitive edge.

The development of AI-powered and high-throughput discovery tools has emerged as a key differentiator, enabling faster adoption in oncology, immunology, and infectious disease sectors. Strategic collaborations, acquisitions, and digital-first approaches for R&D and commercialization are further intensifying the competitive landscape. The industry exhibits a dual nature, consolidated at the top by global leaders while remaining fragmented across numerous regional and niche players catering to local preferences and cost-sensitive segments.

Key Developments

- In May 2025, Danaher Corporation announced a strategic partnership to scale precision medicine through digital and computational pathology products, integrating AI-assisted algorithms to enhance patient targeting for antibody-drug conjugates.

- In June 2025, Twist Bioscience expanded its in vivo antibody discovery services with the launch of a humanized transgenic mouse model, enhancing the generation of high-affinity antibodies for therapeutic applications.

Companies Covered in Antibody Discovery Market

- Danaher Corporation

- Eurofins Scientific

- Evotec

- Twist Bioscience

- Charles River Laboratories

- Genscript Technology Corporation

- Biocytogen

- Sartorius AG

- Fairjourney Biologics S.A

- Creative Biolabs

- Others

Frequently Asked Questions

The global antibody discovery market is projected to reach US$ 8.8 Bn in 2025.

Advancements in biotechnology and high-throughput technologies are a key driver.

The antibody discovery market is poised to witness a CAGR of 9.0% from 2025 to 2032.

Innovative collaboration models and technological integration are key opportunities.

Danaher Corporation, Eurofins Scientific, Evotec, and Charles River Laboratories are key players.