- Biotechnology

- Combination Antibody Therapy Market

Combination Antibody Therapy Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Combination Antibody Therapy Market by Therapy Type (Chemotherapy/Antibody, Antibody/Antibody, Conjugated Antibodies, Bispecific Antibodies), Indication (Lung Cancer, Blood Cancer, Breast Cancer, Colorectal Cancer, Autoimmune & Inflammatory Diseases, Others), End-user (Hospitals, Cancer research institutes, Specialty clinics, Ambulatory Surgical Center (ASC)), and Regional Analysis from 2026 - 2033

Combination Antibody Therapy Market Share and Trends Analysis

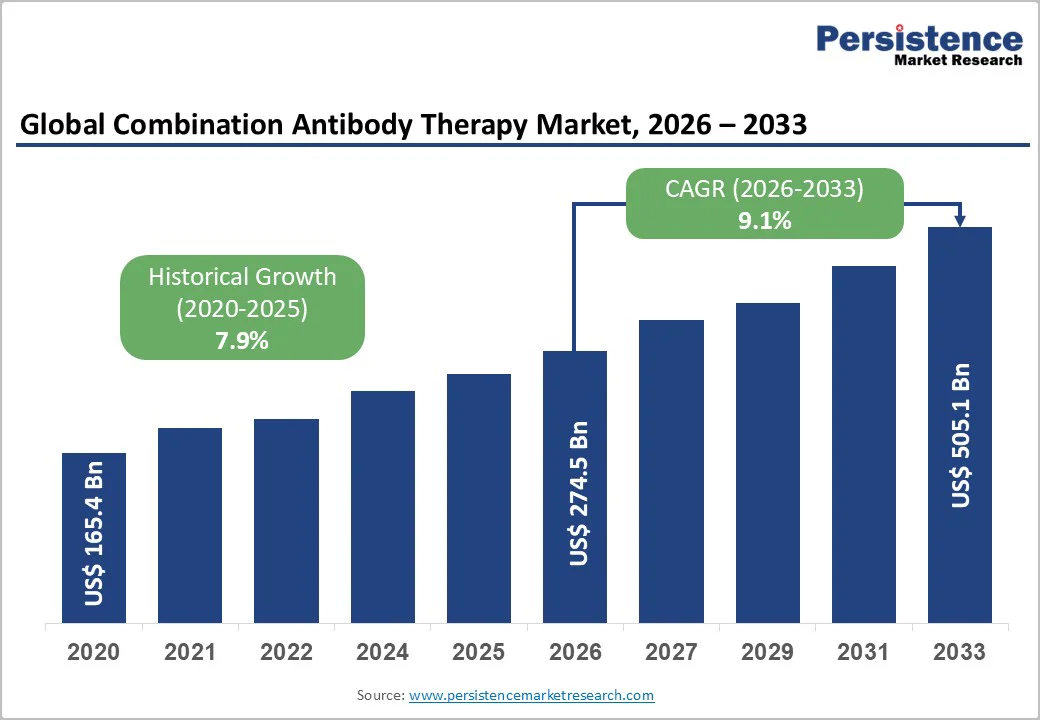

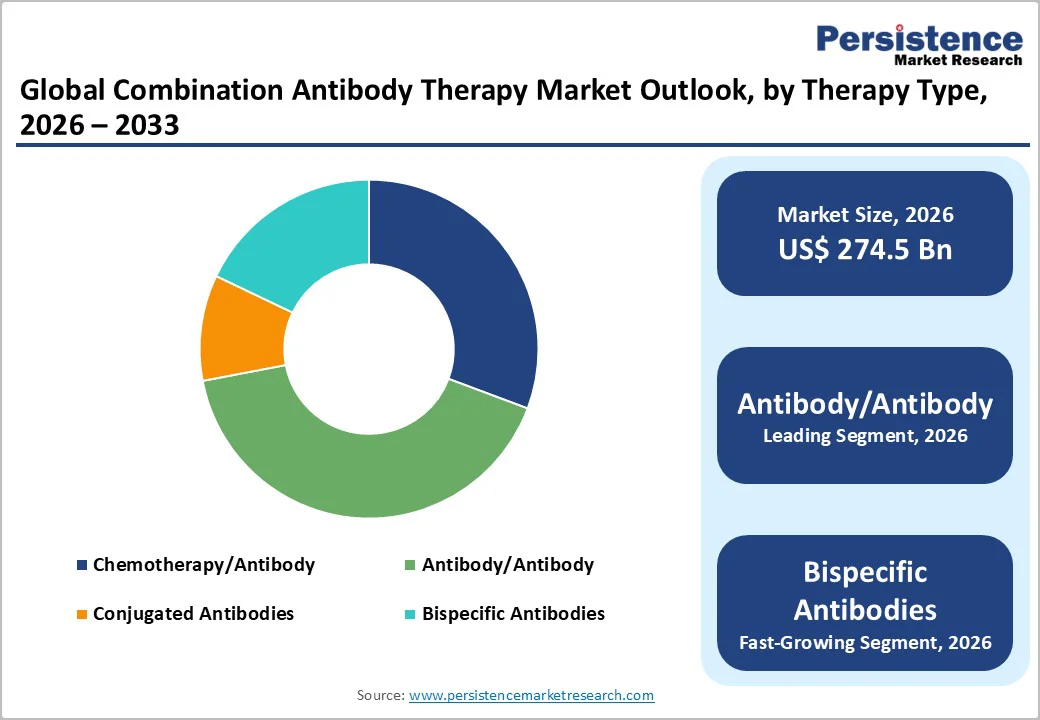

The global combination antibody therapy market size is valued at US$ 274.5 billion in 2026 and projected to reach US$ 505.1 billion by 2033, growing at a CAGR of 13.9% during the forecast period from 2026 to 2033.

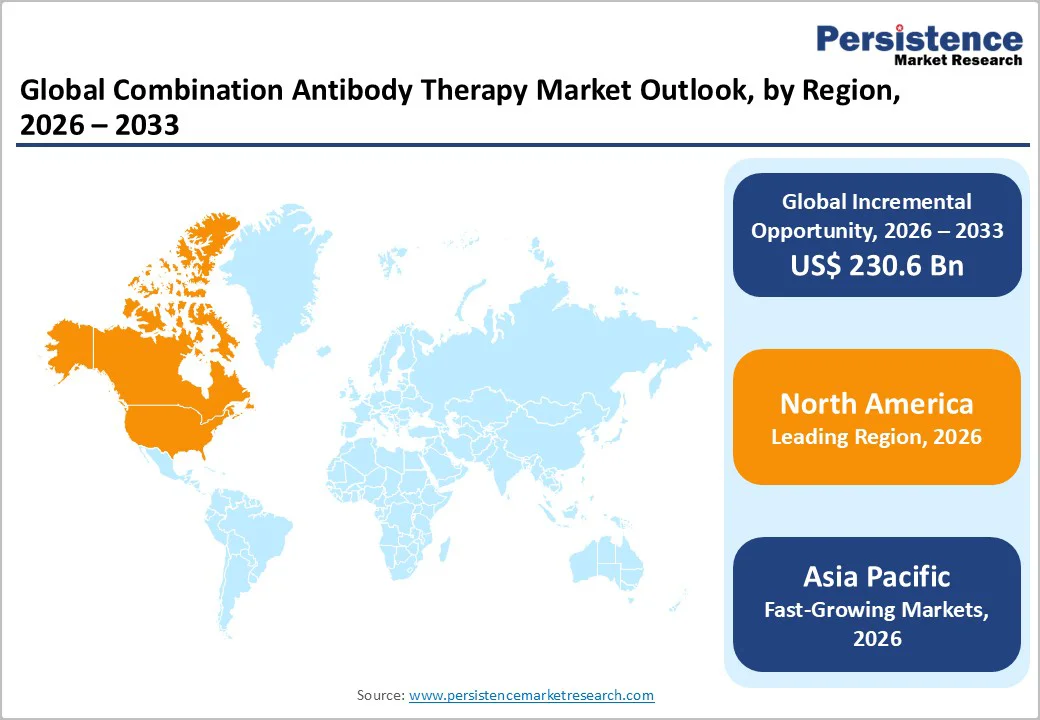

The combination antibody therapy market is growing steadily, driven by rising chronic diseases, increasing biologics patent expiries, and strong demand for cost-effective targeted treatments. North America leads with robust R&D and streamlined regulatory support. Asia Pacific is the fastest-growing regional market, supported by expanding healthcare access, rapid biosimilar uptake, and strengthening local biologics manufacturing.

Key Industry Highlights

- Dominant Segment: Antibody/Antibody therapies dominate the 2025 market with 41.3 % share, due to their strong adoption in oncology and immunology, superior synergistic effects, rising use of bispecific combinations, and growing clinician preference for multi-targeted regimens that outperform single-agent biologics in complex, treatment-resistant conditions.

- Dominant Region: North America holds 46.6% share due to clear FDA pathways, high biologic spending, rapid clinical uptake, and payer-driven optimization of combination regimens. Europe follows closely, while Asia Pacific grows fastest with expanding biologics production and rising therapy affordability.

- Market Drivers: Market growth is fueled by rising cancer and autoimmune cases, advancement in bispecific and conjugated platforms, patent expiries, supportive regulations, improved clinical outcomes of combinations, and strong physician preference for multi-targeted antibody strategies.

- Market Opportunity: Key opportunities include oncology and immunology combinations, bispecific and ADC pairings, expanding into emerging markets, developing cost-efficient manufacturing, and forming global collaborations to accelerate clinical development, regulatory approvals, and commercialization of innovative combination antibody therapies.

| Key Insights | Details |

|---|---|

|

Global Combination Antibody Therapy Market Size (2026E) |

US$ 274.5 Bn |

|

Market Value Forecast (2033F) |

US$ 505.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.9% |

Market Dynamics

Driver - Synergistic Efficacy of Antibody Combinations

The synergistic efficacy of combination antibody therapies is a major growth driver, as using two antibodies together can block multiple cancer or immune pathways simultaneously, delivering significantly stronger outcomes than monotherapy. Evidence from a large meta-analysis of nine randomized trials in advanced non-small-cell lung cancer showed that adding an EGFR-targeting antibody to standard chemotherapy reduced the risk of death by about 9% and increased treatment response rates by nearly 28%.

Dual-antibody regimens such as trastuzumab plus pertuzumab in HER2-positive breast cancer or nivolumab plus ipilimumab in melanoma have consistently demonstrated higher tumor shrinkage and prolonged survival compared with single agents. Recent clinical results with next-generation bispecific antibodies further reinforce this benefit—for example, a PD-1/VEGF bispecific extended progression-free survival to 7.1 months versus 4.8 months with standard therapy, reflecting nearly a 54% reduction in disease progression risk. These synergistic advantages continue to accelerate clinical adoption and market expansion.

Restraints - Complex Manufacturing and Scalability Challenges

Complex manufacturing and scalability challenges significantly restrain the combination antibody therapy market because producing two antibodies or a bispecific molecule requires longer timelines, higher failure risk, and more stringent quality control than standard biologics. Cell-line development for a single antibody typically takes 5–6 months, and scaling two separate antibodies or a complex bispecific structure can extend this substantially.

Large-volume biologics production also carries measurable failure rates: contamination incidents in ≥1,000-liter bioreactor runs occur at roughly 2.3%, and industry data indicate an average batch failure about every 40 weeks, leading to major financial and supply setbacks. Bispecifics and engineered antibody combinations also show lower overall yields because of more difficult purification and higher aggregation risk. These technical hurdles make it challenging to meet rising clinical demand, increase manufacturing costs, delay commercialization timelines, and ultimately slow broader adoption of combination antibody therapies despite their strong therapeutic promise.

Opportunity - Growth of bispecific, trispecific, and ADC–antibody combinations

The rapid growth of bispecific, trispecific, and ADC–antibody combinations is a major opportunity: these platforms enable multi-target engagement and targeted payload delivery, improving response in resistant tumors. Clinical activity is extensive over 250 clinical trials involving more than 100 distinct T-cell-engaging bispecifics registered, reflecting intense development momentum. Regulatory attention and pipeline depth are evident: the FDA and developers flagged a record ~63 ADC-related designations in 2024, signaling accelerated review interest. Antibody therapeutics continue to expand broadly the U.S. regulatory record, shows hundreds of antibody-based approvals over recent decades, providing an established pathway for engineered combos. As ADC approvals accumulate and bispecifics advance through late-stage trials, combination formats (bispecific + mAb, ADC + mAb) are positioned to translate into faster clinical adoption and commercial uptake, especially in oncology indications with high unmet need. These statistics from clinical trial registries and regulatory reports justify the strong market upside for next-generation combination antibody strategies.

Category-wise Analysis

By Therapy Type, Antibody/Antibody Dominates the Combination Antibody Therapy Market

Antibody/Antibody occupies 43.1% share of the global market in 2025, because they build on the strongest and most established foundation in biologics. The FDA has approved over 150 monoclonal antibody products, of which nearly 96 are standard IgG mAbs, compared with only about 14 bispecific antibodies and 13 antibody-drug conjugates. This large installed base gives dual-mAb regimens clear advantages well-validated mechanisms, predictable safety profiles, streamlined CMC processes, and familiarity among clinicians. Regulatory pathways are also more mature for traditional antibodies, reducing development risk and accelerating approval timelines. As a result, developers prioritize antibody–antibody combinations, especially in oncology and autoimmune diseases, where pairing existing mAbs offers faster translation into clinical benefit and broader real-world adoption.

By Indication, Lung Cancer is Gaining Traction Due to High Prevalence, Costly Biologics, And Rapid Originator Replacement

Lung cancer dominates the combination antibody therapy market because it represents the highest global disease burden and the greatest need for advanced multi-targeted treatments. Worldwide, lung cancer recorded about 2.5 million new cases in 2022 and caused over 1.8 million deaths, making it the leading cause of cancer mortality. In the U.S. alone, there were 218,893 new cases in 2022 and 131,584 deaths in 2023. Across OECD countries, lung cancer accounts for roughly 20% of all cancer-related deaths. These severe outcomes drive intense investment in antibody combinations, including PD-1/CTLA-4 pairings, EGFR-targeting combinations, and emerging bispecifics, because they improve survival in advanced or resistant disease, making lung cancer the largest and most commercially significant indication in this market.

Regional Insights

North America Combination Antibody Therapy Market Trends

North America dominates the combination antibody therapy market with a 46.6% share in 2025, due to its strong biologics innovation, regulatory support, and high adoption rates. The region accounted for approximately 44% of the global biologics market in 2024, led by the U.S.’s robust R&D infrastructure. In 2024, the U.S. FDA approved 16 new biologics, including 13 monoclonal antibodies, marking one of the highest annual approval counts in recent years. Biologic therapies represent around 37% of total U.S. drug spending, reflecting widespread clinical use and payer support. The combination of clear regulatory pathways, established manufacturing capabilities, and significant healthcare expenditure enables rapid clinical adoption of antibody combinations. These factors collectively reinforce North America’s leading position in the global combination antibody therapy market.

Europe Combination Antibody Therapy Market Trends

Europe is a key region in the combination antibody therapy market due to its mature regulatory framework and strong focus on biosimilars. Since 2006, the EMA has approved 86 biosimilar medicines, reflecting long-standing support for biologic alternatives. In 2024 alone, 28 new biosimilars were recommended, including treatments for cancer and immune-mediated diseases, highlighting Europe’s leadership in enabling affordable access. European guidelines allow biosimilars to be considered interchangeable with reference products, supported by over one million patient-treatment years of safety data, demonstrating robust clinical confidence. These factors, combined with high physician familiarity and payer support for cost-effective biologics, make Europe an important region for launching and scaling combination antibody therapies, especially for oncology and immunology indications.

Asia Pacific Combination Antibody Therapy Market Trends

Asia Pacific is the fastest-growing region in the combination antibody therapy market due to expanding biologics manufacturing capacity, increasing healthcare access, and rising affordability initiatives. China and India are major contributors, with China producing over 20% of the world’s biopharmaceutical active ingredients and India supplying more than 50% of global vaccines, reflecting strong biologics expertise.

Regulatory agencies across the region, including China’s NMPA and India’s CDSCO, have streamlined approval pathways for biosimilars and combination therapies, encouraging local development and adoption. Additionally, government initiatives such as China’s “Made in China 2025” and India’s biotechnology development policies have accelerated domestic production. The combination of lower manufacturing costs, increasing clinical trial activity, and growing physician and patient access supports rapid adoption, positioning Asia Pacific as the fastest-growing market for combination antibody therapies.

Competitive Landscape

Leading companies in the combination antibody therapy market prioritize precise manufacturing, advanced formulations, and strict quality control. They invest in monoclonal antibodies and protein biosimilars, optimize production consistency, and forge partnerships with healthcare providers. R&D focuses on improving efficacy, safety, and cost-effectiveness, supporting chronic disease treatment, wider patient access, and accelerated global biosimilar adoption.

Key Industry Developments:

- In November 2025, Biogen and Dayra Therapeutics announced a research collaboration to discover and develop oral macrocyclic peptides targeting a range of immunological conditions. The partnership aimed to leverage Dayra’s peptide platform alongside Biogen’s expertise in immunology to accelerate the development of innovative oral therapies, potentially offering patients more convenient treatment options for chronic immune-related diseases.

- In October 2025, Eisai and Biogen announced the U.S. availability of LEQEMBI® IQLIK™ (lecanemab-irmb) subcutaneous injection as a maintenance dose for treating early Alzheimer’s disease. The approval provided patients with a more convenient administration option, supporting ongoing management of early-stage Alzheimer’s and expanding access to innovative anti-amyloid therapy in the United States.

- In July 2024, Biogen completed its acquisition of HI-Bio, strengthening its portfolio in innovative biologics. The acquisition aimed to enhance Biogen’s research and development capabilities, expand its biologics pipeline, and accelerate the delivery of advanced therapies to patients worldwide.

Companies Covered in Combination Antibody Therapy Market

- Biogen Inc.

- Roche Holdings AG

- Seattle Genetics Inc.

- Seagen (Pfizer)

- Eli Lilly and Company

- Sanofi

- Amgen

- Genmab

- Merck & Co.

- Novartis

- AstraZeneca

- Others

Frequently Asked Questions

The global combination antibody therapy market is projected to be valued at US$ 274.5 Bn in 2026.

Rising chronic diseases, biologic patent expiries, synergistic efficacy of antibody combinations, regulatory support, and growing physician and payer adoption drive the market.

The global combination antibody therapy market is poised to witness a CAGR of 9.1% between 2026 and 2033.

Opportunities include oncology and immunology combinations, bispecific and ADC pairings, emerging market expansion, cost-effective manufacturing, and strategic global partnerships.

Biogen Inc., Roche Holdings AG, Seattle Genetics Inc., Seagen (Pfizer), Eli Lilly and Company, Sanofi.