- Healthcare Services

- Antinuclear Antibody Test Market

Antinuclear Antibody Test Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Antinuclear Antibody Test Market by Product (Reagents and Assay Kits, Systems, Software and Services), Technique (ELISA, Immunofluorescence Assay, Multiplex Assay), Application (Rheumatoid Arthritis, Systemic Lupus Erythematosus, Sjögren’s Syndrome, Scleroderma, Others), End User (Hospitals, Clinical Laboratories, Physician Office Laboratories, Others), and Regional Analysis from 2026 to 2033

Antinuclear Antibody Test Market Size and Trends

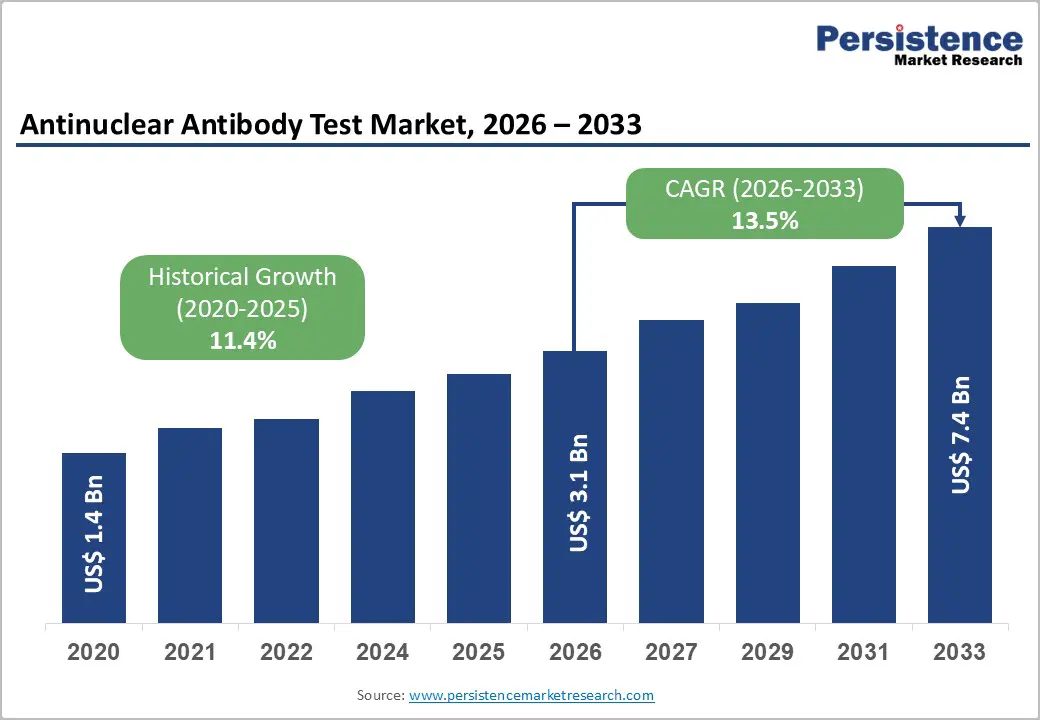

The global antinuclear antibody test market is estimated to grow from US$ 3.1 Bn in 2026 to US$ 7.4 Bn by 2033. The market is projected to record a CAGR of 13.5% during the forecast period from 2026 to 2033.

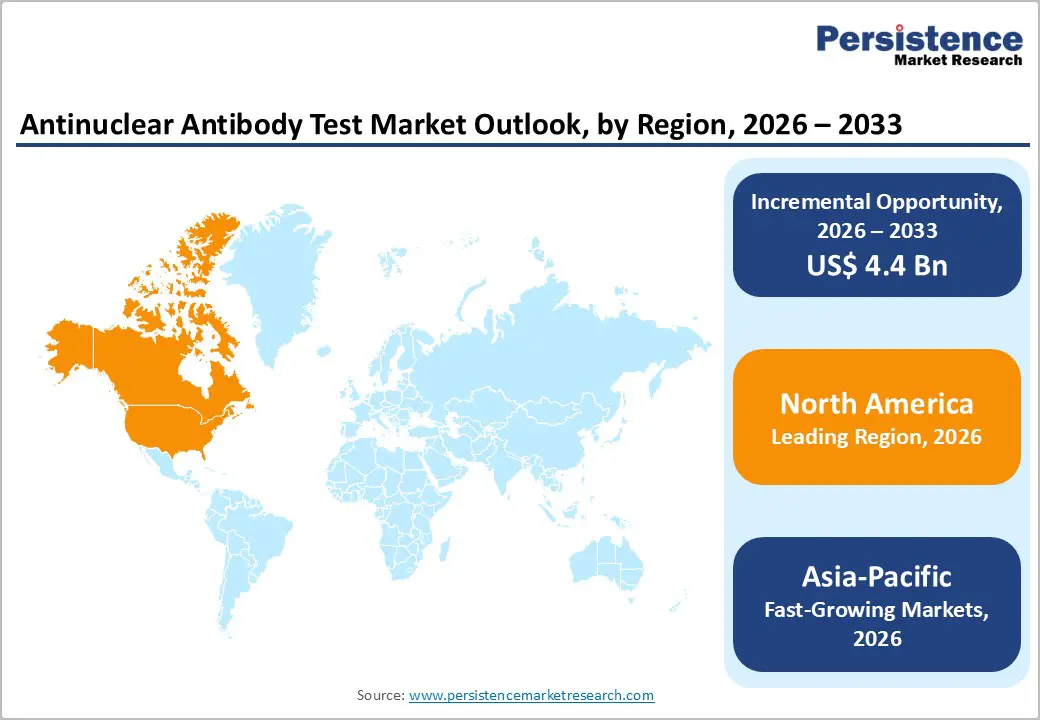

The global antinuclear antibody test market is expanding steadily, fueled by digital platforms, healthcare analytics, and data-driven research. North America dominates with advanced research infrastructure and strong regulations, while Asia-Pacific is the fastest-growing region, driven by healthcare expansion, government initiatives, rising clinical trials, and increasing investments in outsourced biomarker testing services

Key Industry Highlights

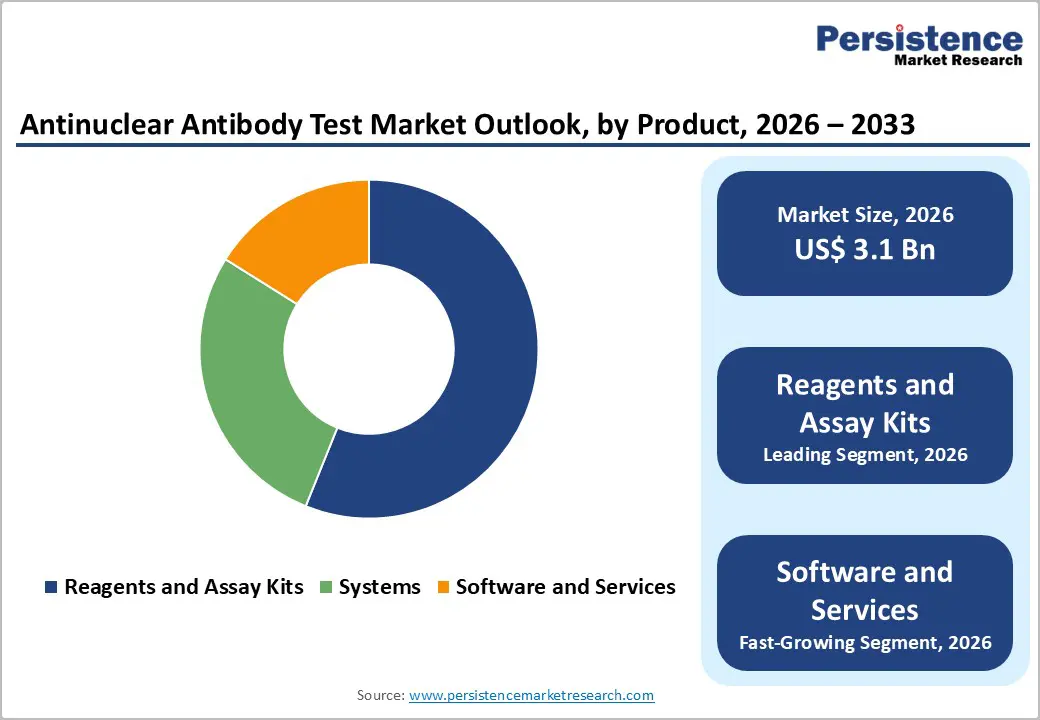

- Dominant Segment: Reagents and assay kits hold the largest share of the antinuclear antibody test market in 2025, accounting for 56.1% share of revenue. Their dominance is driven by widespread use in clinical diagnostics and research, high reproducibility, compatibility with various testing platforms, and essential role in supporting high-throughput, automated, and cost-efficient ANA testing across hospitals, laboratories, and CROs.

- Dominant Region: North America leads the market in 2025 with 42.1% share, supported by advanced research infrastructure, strong presence of CROs and biopharmaceutical companies, and stringent regulatory standards. Asia-Pacific is the fastest-growing region, fueled by expanding clinical research activity, cost-efficient outsourcing, government R&D support, and increasing investments in life sciences.

- Market Drivers: Growth of the antinuclear antibody test market is fueled by rising biopharmaceutical and clinical R&D spending, increasing adoption of precision medicine, growing complexity of autoimmune and chronic disease trials, demand for faster drug development, and advancements in genomics, proteomics, and data-driven diagnostic analytics.

- Market Opportunity: Key opportunities include predictive and surrogate biomarker discovery, AI-driven data interpretation, multi-omics integration, autoimmune and oncology-focused research, partnerships with CROs, and expansion of outsourcing services across emerging markets with increasing clinical trial activity.

| Key Insights | Details |

|---|---|

| Antinuclear Antibody Test Market Size (2026E) | US$ 3.1 Bn |

| Market Value Forecast (2033F) | US$ 7,4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.4% |

Market Dynamics

Driver: Increasing prevalence of autoimmune diseases globally

The rising prevalence of autoimmune diseases worldwide is expected to drive the antinuclear antibody test market growth in the foreseeable future, finds Persistence Market Research. These tests are considered fundamental in diagnosing systemic autoimmune disorders, including scleroderma, Sjögren’s syndrome, and Systemic Lupus Erythematosus (SLE). As per a 2023 report by the Global Burden of Disease Study published in The Lancet, autoimmune diseases have surged in incidence by nearly 19% over the last decade. It is due to the improved diagnostic awareness and environmental triggers, including lifestyle changes and pollution.

The epidemiological trend has further resulted in a proportional surge in ANA testing volumes globally. Data from the U.S. Centers for Disease Control and Prevention (CDC) and other health organizations highlight that approximately five percent of the U.S. population is now affected by one or more autoimmune diseases. This growth directly correlates with high ANA test requisitions in both primary care and specialty clinics. Rheumatologists are relying on ANA screening as a frontline tool not only to confirm suspected autoimmune disorders but also to monitor disease progression.

Restraints: Diagnostic uncertainty limits widespread adoption of ANA testing

The possibility of false positives and non-specific results significantly hinders the widespread adoption of ANA tests by creating diagnostic uncertainty. Recent studies, including a 2024 publication in Arthritis & Rheumatology, show that up to 20 to 30% of healthy individuals, primarily older adults, are likely to exhibit low-titer positive ANA results without any underlying autoimmune disease. This high background positivity reduces physician confidence in the test’s specificity and complicates clinical interpretation.

The Indirect Immunofluorescence Assay (IIFA), which is a gold standard for ANA testing, is subjective and operator-dependent, contributing to occasional misclassification. A 2023 comparative study from Clinical Chemistry demonstrated that inter-laboratory concordance rates for ANA IIFA patterns can be as low as 70%. This variability is specifically challenging in small-scale labs and community hospitals lacking specialized personnel, thereby hampering test adoption in resource-constrained settings.

Opportunity: Introduction of multiplex ANA methods enhances diagnostic specificity

The introduction of multiplex methods in ANA testing is changing autoimmune disease testing by enabling the simultaneous detection of multiple autoantibodies with high specificity and efficiency. Multiplex platforms use bead-based or microarray technologies to assess dozens of autoantibodies in one run, thereby lowering the time and sample volume required. A 2023 clinical validation study in the Journal of Clinical Immunology revealed that multiplex ANA assays increased diagnostic yield by detecting clinically relevant autoantibodies missed by conventional indirect immunofluorescence.

Key companies such as Thermo Fisher Scientific and Bio-Rad Laboratories have innovated these multiplex platforms with extended autoantibody panels made for systemic lupus erythematosus and other connective tissue diseases. This targeted profiling enables clinicians to differentiate disease subtypes more accurately, resulting in personalized treatment strategies. For example, Bio-Rad’s BioPlex 2200 system, extensively used in North America, reported a 25% improvement in diagnostic confidence in 2024 compared to standalone ANA testing.

Category-wise Analysis

By Product, Reagents and Assay Kits Dominates the Antinuclear Antibody Test Market

Based on product, the market is divided into reagents and assay kits, systems, and software and services. Out of these, the reagents and assay kits segment will likely account for a share of around 56.1% in 2025 due to their key role in ensuring standardized, reproducible, and accurate diagnostics, essential for managing complex autoimmune diseases. High-quality reagents, including fluorescent-labeled antibodies and cell substrates, directly impact the sensitivity and specificity of ANA tests. EUROIMMUN’s HEp-2 cell substrates, for instance, have demonstrated improved detection rates in a 2023 study published in Clinical Rheumatology.

Software and services have also emerged as essential product categories due to the rising complexity and volume of test data generated by modern diagnostic platforms. Automated IIFA, combined with multiplex technologies, produces vast amounts of imaging and serological data that require innovative interpretation tools. Novel software solutions, often powered by machine learning and AI, are important in standardizing ANA pattern recognition. It helps in lowering subjective variability and improving diagnostic accuracy.

By Technique, Immunofluorescence Assay dominates due to high sensitivity, detailed nuclear patterns, and clinical gold-standard status

Immunofluorescence Assay (IFA) dominates the antinuclear antibody test market because it remains the clinical gold standard for ANA detection, offering broadly recognized and clinically validated performance metrics that support its continued preference in diagnostic workflows. IFA using HEp2 cell substrates can detect a wide range of autoantibodies and visualize detailed nuclear staining patterns, which provide clinicians with both qualitative pattern information and quantitative titers, a capability many solid phase methods lack. For example, studies report 100% ANA positivity by IFA in childhood systemic lupus erythematosus (SLE) cases versus only 55% by enzyme immunoassay in the same cohort, demonstrating clearly higher detection sensitivity in certain diseases. IFA’s high sensitivity (often >90% in systemic rheumatic diseases) and ability to support nuanced interpretation of autoimmune profiles underpins its sustained utilization in clinical laboratories worldwide.

Regional Insights

North America Antinuclear Antibody Test Market Trends

North America dominates the antinuclear antibody test market with 42.1% share in 2025, because the region has a high prevalence of autoimmune diseases and world class diagnostic infrastructure that enables widespread screening and specialized laboratory services. In the United States, about 8% of the population (over 50 million people) are affected by autoimmune disorders, driving demand for tests such as ANA panels for early detection and disease monitoring.Government supported research funding and robust insurance reimbursement systems further facilitate adoption of advanced diagnostics.Additionally, Canada’s surveillance of conditions like rheumatoid arthritis, affecting roughly 1.2% of adults, underscores regional disease burden and testing needs. These epidemiological and healthcare system advantages collectively sustain North America’s market leadership.

Europe Antinuclear Antibody Test Market Trends

Europe is an important region in the antinuclear antibody test market because it has a high burden of autoimmune and related conditions, strong public healthcare systems, and widespread adoption of advanced diagnostic protocols. According to the European Centre for Disease Prevention and Control, autoimmune diseases affect tens of millions of Europeans, creating substantial demand for ANA and related diagnostics. The European Union has dedicated significant research funding, such as through the Horizon Europe program with €95.5 billion for research and innovation (including healthcare and diagnostics), which supports development and deployment of improved immunologic assays. Additionally, countries like Germany, France, and the United Kingdom maintain well established laboratory networks and national screening initiatives, which help integrate ANA testing into routine clinical practice and strengthen regional market relevance.

Asia-Pacific Antinuclear Antibody Test Market Trends

Asia Pacific is the fastest growing region in the antinuclear antibody test market due to a rising burden of autoimmune conditions, expanding healthcare infrastructure, and increased access to diagnostic services. For instance, approximately 50 million autoimmune cases were reported across Asia Pacific in 2023, with notable growth in China and India, boosting demand for ANA and related immunologic tests. Immunologic testing facilities in Japan grew by 15% from 2021–2024, enhancing diagnostic access. Government initiatives and rising healthcare investment, such as programs in India that increased autoimmune testing volumes by about 30% have further accelerated uptake of complex diagnostics. These demographic and system level trends underpin rapid regional expansion for ANA testing.

Market Competitive Landscape

Leading antinuclear antibody test market companies focus on advanced analytics, AI-driven diagnostic platforms, and integrated service offerings. Key priorities include ensuring data interoperability, regulatory compliance, and optimizing laboratory workflow efficiency. Investments in genomics, proteomics, and multi-omics technologies improve autoantibody detection accuracy, while collaborations with biopharmaceutical firms, CROs, and academic institutions accelerate clinical translation, expand diagnostic capabilities, and drive global adoption of ANA testing across research and clinical laboratories.

Key Industry Developments:

- In November 2025, Thermo Fisher Scientific announced that its EXENT system, a first-of-its-kind solution designed to support rapid and accurate diagnosis of multiple myeloma, received FDA clearance. The system enables laboratories to perform comprehensive testing for multiple myeloma with improved speed and clarity, supporting earlier detection and better-informed clinical decision-making. This clearance marks a significant step in expanding access to advanced diagnostic technologies for hematologic malignancies.

- In March 2025, Helix announced a new comprehensive clinico-genomic virtual registry of autoimmune disease patients. It consists of more than 23,000 individuals with conditions such as multiple sclerosis, lupus, Crohn's, rheumatoid arthritis, and more. A key feature of the autoimmune virtual registry includes the development of over 15 significant autoimmune lab results, including antinuclear antibody tests and erythrocyte sedimentation rate.

- In June 2023, Immuno Concepts received FDA clearance for its IgG Anti-nDNA Fluorescent Test System, designed for use with the Image Navigator® platform. The approval allows laboratories to utilize the system for precise detection of anti-double-stranded DNA antibodies, enhancing diagnostic accuracy for autoimmune conditions such as systemic lupus erythematosus. This clearance expands Immuno Concepts’ diagnostic offerings and supports more efficient, reliable autoimmune testing in clinical laboratories.

Companies Covered in Antinuclear Antibody Test Market

- Trinity Biotech Plc.

- ERBA Diagnostics Mannheim GmbH

- Antibodies Incorporated

- Inova Diagnostics, Inc.

- Bio-Rad Laboratories, Inc.

- Thermo Fisher Scientific, Inc.

- ZEUS Scientific, Inc.

- Immuno Concepts NA Ltd.

- EUROIMMUN Medizinische Labordiagnostika AG

- Alere Inc.

- Others

Frequently Asked Questions

The global antinuclear antibody test market is projected to be valued at US$ 3.1 Bn in 2026.

Rising autoimmune disease prevalence, precision medicine adoption, advanced diagnostics, R&D spending, and complex clinical trials drive growth.

The global antinuclear antibody test market is poised to witness a CAGR of 13.5% between 2026 and 2033..

Opportunities include AI-driven analysis, predictive biomarker discovery, multi-omics integration, autoimmune research, CRO collaborations, and emerging markets.